The global engineering plastics market has been witnessing steady growth in recent years, driven by the increasing demand for lightweight, durable, and high-performance materials across various industries. Engineering plastics are a group of polymers that exhibit superior mechanical, thermal, and electrical properties, making them suitable for a wide range of applications. These materials are widely used in automotive, electrical and electronics, consumer goods, packaging, and construction sectors, among others.

Meaning

Engineering plastics are a type of advanced materials that are designed to meet specific performance requirements. Unlike commodity plastics, which are commonly used for general applications, engineering plastics offer enhanced mechanical, thermal, and chemical properties. These materials are typically used in demanding applications where traditional materials such as metals and ceramics fall short. Engineering plastics provide a balance of strength, stiffness, toughness, and dimensional stability, making them highly desirable in various industries.

Executive Summary

The global engineering plastics market is experiencing robust growth due to the increasing demand for lightweight and high-performance materials across multiple sectors. The market is driven by factors such as the growing automotive industry, rising demand for electrical and electronic products, and the need for sustainable packaging solutions. Key players in the market are focusing on product innovation and strategic partnerships to gain a competitive edge. However, the market also faces challenges such as price volatility of raw materials and environmental concerns related to plastic waste.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The global engineering plastics market is expected to grow at a CAGR of X% during the forecast period.

The automotive industry is a major consumer of engineering plastics, driven by the need for lightweight materials to improve fuel efficiency and reduce emissions.

The electrical and electronics sector is another significant end-user of engineering plastics, driven by the increasing demand for high-performance materials in electronic components.

The Asia Pacific region dominates the global engineering plastics market, with China being the largest consumer and producer of engineering plastics.

The market is witnessing a trend towards the development of bio-based and recyclable engineering plastics to address environmental concerns.

Market Drivers

Increasing demand from the automotive industry: The automotive sector is a major driver of the engineering plastics market. The need for lightweight materials to improve fuel efficiency and reduce vehicle weight has led to the widespread adoption of engineering plastics in automotive applications.

Growing electrical and electronics industry: The rapid expansion of the electrical and electronics industry, driven by technological advancements and increasing consumer electronics consumption, is boosting the demand for engineering plastics. These materials are used in connectors, switches, insulators, and other electronic components.

Rising demand for sustainable packaging solutions: With the growing focus on environmental sustainability, there is a rising demand for engineering plastics in packaging applications. These materials offer lightweight and recyclable alternatives to traditional packaging materials such as glass and metal.

Technological advancements in material development: Ongoing research and development activities have resulted in the introduction of advanced engineering plastics with improved properties. This has expanded the application scope of engineering plastics across various industries.

Market Restraints

Price volatility of raw materials: Engineering plastics are derived from petrochemical feedstocks, and fluctuations in crude oil prices can impact the cost of raw materials. Price volatility poses a challenge for market players in terms of planning and pricing strategies.

Environmental concerns related to plastic waste: The increasing focus on sustainability and plastic waste management is a significant challenge for the engineering plastics market. The disposal and recycling of engineering plastics can be complex, and there is a need for more efficient recycling technologies.

Regulatory restrictions on certain plastic additives: Some additives used in engineering plastics, such as flame retardants, have come under scrutiny due to environmental and health concerns. Regulatory restrictions on the use of certain additives can impact the market growth.

Market Opportunities

Growing demand from emerging economies: Rapid industrialization and urbanization in emerging economies present significant opportunities for the engineering plastics market. The rising middle-class population, increasing disposable incomes, and expanding industrial sectors in countries like India, China, and Brazil are driving the demand for engineering plastics.

Advancements in 3D printing technology: 3D printing, also known as additive manufacturing, is gaining traction across industries. Engineering plastics are widely used as materials for 3D printing, and the growing adoption of this technology is expected to create new opportunities for the market.

Focus on lightweight materials in aerospace industry: The aerospace industry is increasingly focusing on lightweight materials to improve fuel efficiency and reduce emissions. Engineering plastics offer excellent strength-to-weight ratio and can find significant applications in aircraft interiors, components, and structural parts.

Market Dynamics

The global engineering plastics market is dynamic and influenced by various factors. The market dynamics include:

Technological advancements: Continuous research and development activities drive the introduction of new and improved engineering plastics with enhanced properties, expanding the application scope of these materials.

Mergers and acquisitions: Key players in the market are engaging in strategic mergers and acquisitions to expand their product portfolios, enhance their market presence, and gain a competitive advantage.

Shifting consumer preferences: Changing consumer preferences towards lightweight, durable, and sustainable materials are influencing the demand for engineering plastics across industries.

Government regulations: Regulatory frameworks related to plastic waste management, recycling, and the use of certain additives impact the engineering plastics market. Compliance with environmental regulations is essential for market players.

Economic factors: Economic growth, industrial development, and infrastructure investments in different regions impact the demand for engineering plastics. Economic factors such as GDP growth, per capita income, and consumer spending patterns influence market dynamics.

Regional Analysis

The global engineering plastics market is geographically segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. The Asia Pacific region dominates the market, both in terms of consumption and production. The region is witnessing significant growth due to the presence of major manufacturing hubs, such as China and India. These countries have a large consumer base for engineering plastics, driven by the automotive, electrical and electronics, and consumer goods industries. North America and Europe also hold substantial market shares due to the well-established automotive and aerospace industries in these regions.

Competitive Landscape

Leading Companies in Global Engineering Plastic Market:

BASF SE

Covestro AG

SABIC

Mitsubishi Engineering-Plastics Corporation

Evonik Industries AG

LG Chem Ltd.

Dow

EMS-Chemie Holding AG

Lanxess AG

RTP Company

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

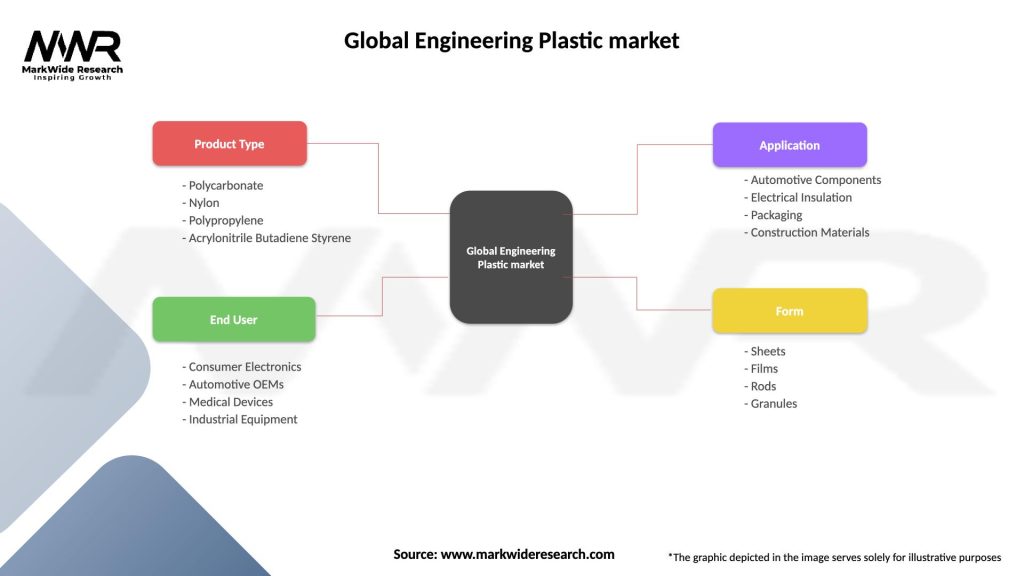

The engineering plastics market can be segmented based on type, application, and region. By type, the market can be segmented into polyamide, polycarbonate, acrylonitrile butadiene styrene (ABS), polyoxymethylene (POM), polybutylene terephthalate (PBT), and others. By application, the market can be segmented into automotive, electrical and electronics, consumer goods, packaging, construction, and others. Regionally, the market can be segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Category-wise Insights

Polyamide (PA):

Polyamide is one of the most widely used engineering plastics due to its excellent mechanical strength, heat resistance, and chemical resistance properties.

It finds extensive applications in the automotive industry for manufacturing engine components, fuel systems, and interior parts.

The electrical and electronics industry also utilizes polyamide in connectors, switches, and electronic housings.

Polycarbonate (PC):

Polycarbonate is a transparent and impact-resistant engineering plastic with high heat resistance.

It is commonly used in the automotive industry for manufacturing headlights, interior trim, and electrical components.

The electrical and electronics sector also utilizes polycarbonate in the production of LED lighting, optical discs, and electronic displays.

Acrylonitrile Butadiene Styrene (ABS):

ABS is a versatile engineering plastic known for its excellent impact resistance, heat resistance, and dimensional stability.

It is extensively used in the automotive industry for manufacturing interior trim, instrument panels, and exterior parts.

ABS is also popular in the consumer goods industry for producing appliances, toys, and luggage.

Polyoxymethylene (POM):

POM, also known as acetal, is a high-strength engineering plastic with excellent dimensional stability and low friction properties.

It finds applications in the automotive industry for manufacturing gears, bearings, and fuel system components.

The electrical industry also utilizes POM in electrical connectors, switches, and insulators.

Polybutylene Terephthalate (PBT):

PBT is a thermoplastic engineering plastic with good electrical insulation properties and excellent resistance to chemicals and heat.

It is commonly used in the automotive industry for manufacturing connectors, sensors, and electrical housings.

PBT also finds applications in the electrical and electronics industry for producing switches, sockets, and circuit breakers.

Key Benefits for Industry Participants and Stakeholders

The engineering plastics market offers lucrative opportunities for manufacturers, suppliers, and distributors to expand their business operations.

The growing demand for lightweight and high-performance materials presents a chance to cater to the needs of various industries, including automotive, electrical and electronics, and packaging.

Strategic partnerships and collaborations with end-users can lead to long-term contracts and ensure a stable customer base.

Investing in research and development activities can lead to the development of innovative products and provide a competitive edge in the market.

The growing focus on sustainability and recyclability opens avenues for the development of bio-based and eco-friendly engineering plastics.

SWOT Analysis

Strengths:

Engineering plastics offer superior mechanical, thermal, and electrical properties compared to traditional materials.

The market is driven by the growing demand from key industries such as automotive and electrical and electronics.

Continuous research and development activities lead to the introduction of advanced engineering plastics with enhanced properties.

Weaknesses:

Price volatility of raw materials impacts the profitability of market players.

Environmental concerns related to plastic waste management pose challenges for the market.

Regulatory restrictions on certain plastic additives can limit the growth potential.

Opportunities:

Emerging economies present significant growth opportunities for the engineering plastics market.

Advancements in 3D printing technology create new applications for engineering plastics.

The aerospace industry’s focus on lightweight materials opens avenues for engineering plastics.

Threats:

The availability of alternative materials such as metals and composites can pose a threat to the engineering plastics market.

Economic downturns and geopolitical factors can impact the market growth.

Intense competition among market players can lead to pricing pressures.

Market Key Trends

Bio-based and recyclable engineering plastics: The market is witnessing a trend towards the development of bio-based engineering plastics derived from renewable resources. Additionally, there is an increasing focus on recycling engineering plastics to address environmental concerns and promote a circular economy.

Lightweight materials for automotive applications: With the growing emphasis on fuel efficiency and emission reduction, the automotive industry is adopting lightweight materials such as engineering plastics. These materials help in reducing the overall weight of vehicles while maintaining structural integrity.

Technological advancements in material development: Ongoing research and development efforts are leading to the introduction of engineering plastics with improved properties. Advancements in polymer science, additives, and processing technologies are enabling the production of high-performance engineering plastics with enhanced strength, heat resistance, and durability.

Electric vehicle (EV) revolution: The shift towards electric vehicles presents significant opportunities for the engineering plastics market. Engineering plastics are used in various components of electric vehicles, including battery enclosures, connectors, and thermal management systems.

Covid-19 Impact

The Covid-19 pandemic had a significant impact on the global engineering plastics market. The outbreak led to disruptions in the supply chain, manufacturing activities, and reduced demand across industries. The automotive industry, one of the major consumers of engineering plastics, experienced a downturn due to production shutdowns and lower consumer demand. However, the market showed resilience as the demand gradually recovered with the easing of restrictions and the resumption of economic activities. The pandemic highlighted the importance of sustainability and the need for reliable supply chains, leading to increased focus on bio-based and recyclable engineering plastics.

Key Industry Developments

Product Innovation: Market players are focusing on product innovation to cater to the evolving needs of end-users. Companies are investing in the development of advanced engineering plastics with improved properties, such as enhanced heat resistance, flame retardancy, and recyclability.

Strategic Partnerships: Key industry players are engaging in strategic partnerships and collaborations to expand their market presence and enhance their product portfolios. Partnerships with end-users and research institutions facilitate the development of tailored solutions and ensure a competitive edge in the market.

Capacity Expansions: Several companies are investing in capacity expansions to meet the growing demand for engineering plastics. Expansion projects help in increasing production capabilities, ensuring a reliable supply chain, and strengthening the market position of companies.

Analyst Suggestions

Focus on Sustainable Solutions: Market players should prioritize the development of bio-based and recyclable engineering plastics to address environmental concerns and meet the increasing demand for sustainable materials.

Research and Development: Continuous investment in research and development activities is crucial to stay ahead in the competitive market. Companies should strive to develop innovative products with enhanced properties to cater to specific industry requirements.

Collaborations with End-Users: Establishing strong partnerships with end-users can provide valuable insights into market trends, customer preferences, and emerging application areas. Collaborations can lead to long-term contracts and a steady customer base.

Geographical Expansion: Exploring opportunities in emerging economies can contribute to market growth. Companies should consider expanding their presence in regions with significant industrial development and growing consumer markets.

Future Outlook

The global engineering plastics market is expected to witness steady growth in the coming years. The increasing demand for lightweight, high-performance materials in various industries, coupled with technological advancements in material development, will drive market growth. The focus on sustainability, bio-based materials, and recyclability will shape the future of the engineering plastics market. The automotive and electrical and electronics sectors are anticipated to remain key end-users, while emerging applications in sectors such as aerospace, healthcare, and 3D printing will contribute to market expansion.

Conclusion

The global engineering plastics market is experiencing growth driven by the demand for lightweight, durable, and high-performance materials across industries. The market offers opportunities for manufacturers, suppliers, and distributors to cater to the evolving needs of end-users. The market dynamics are influenced by technological advancements, mergers and acquisitions, shifting consumer preferences, government regulations, and economic factors. The Asia Pacific region dominates the market, with China as the largest consumer and producer of engineering plastics. The market is highly competitive, and key players are focusing on product innovation, partnerships, and capacity expansions to gain a competitive edge. The future outlook for the engineering plastics market is positive, with a focus on sustainability, bio-based materials, and emerging applications driving market growth.

What is Engineering Plastic?

Engineering plastics are a group of plastic materials that have superior mechanical and thermal properties compared to standard plastics. They are commonly used in applications such as automotive components, electrical housings, and industrial machinery due to their strength and durability.

What are the key players in the Global Engineering Plastic market?

Key players in the Global Engineering Plastic market include BASF, DuPont, and SABIC, which are known for their innovative solutions and extensive product portfolios. These companies focus on developing high-performance materials for various applications, including automotive, electronics, and consumer goods, among others.

What are the growth factors driving the Global Engineering Plastic market?

The Global Engineering Plastic market is driven by the increasing demand for lightweight materials in the automotive industry and the growing need for high-performance components in electronics. Additionally, advancements in manufacturing technologies and the rise of sustainable materials are contributing to market growth.

What challenges does the Global Engineering Plastic market face?

The Global Engineering Plastic market faces challenges such as fluctuating raw material prices and environmental concerns regarding plastic waste. Additionally, competition from alternative materials like metals and ceramics can hinder market expansion.

What opportunities exist in the Global Engineering Plastic market?

Opportunities in the Global Engineering Plastic market include the development of bio-based engineering plastics and the expansion of applications in the aerospace and medical sectors. The increasing focus on sustainability and recycling initiatives also presents new avenues for growth.

What trends are shaping the Global Engineering Plastic market?

Trends shaping the Global Engineering Plastic market include the rise of smart materials that respond to environmental changes and the integration of advanced manufacturing techniques like 3D printing. Additionally, the push for lightweight and energy-efficient solutions in various industries is influencing product development.

Leading Companies in Global Engineering Plastic Market:

BASF SE

Covestro AG

SABIC

Mitsubishi Engineering-Plastics Corporation

Evonik Industries AG

LG Chem Ltd.

Dow

EMS-Chemie Holding AG

Lanxess AG

RTP Company

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.