The global embedded security for the Internet of Things (IoT) market has witnessed significant growth in recent years. With the rapid proliferation of connected devices and the increasing integration of IoT solutions across various industries, the need for robust security measures has become paramount. Embedded security plays a crucial role in safeguarding IoT devices and networks from cyber threats, unauthorized access, data breaches, and other security vulnerabilities. This market analysis aims to provide insights into the current state and future prospects of the global embedded security for IoT market.

Embedded security refers to the integration of security mechanisms directly into the hardware and software components of IoT devices. It involves implementing encryption, authentication, access control, secure boot, secure firmware updates, and other security measures at the device level. These embedded security solutions provide end-to-end protection, ensuring the confidentiality, integrity, and availability of data transmitted and stored within IoT ecosystems.

Executive Summary

The executive summary of this market analysis report presents a concise overview of the key findings, market trends, and future outlook of the global embedded security for IoT market. It highlights the significant growth opportunities and challenges faced by industry participants, along with the impact of the COVID-19 pandemic on the market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Projection: The market is expected to surpass USD 7 billion by 2030, up from approximately USD 3 billion in 2024.

Hardware Security Focus: Secure elements and embedded TPMs account for over 60% of revenue share, driven by demand for hardware-enforced device identity and key protection.

Software Integration: Secure bootloaders, firmware signing, and runtime integrity checks are increasingly packaged as turnkey software libraries, simplifying adoption for OEMs.

Edge Security Adoption: Growth of edge AI and analytics in manufacturing and smart cities is pushing security closer to the device, reducing reliance on network-based protections.

Standards & Certification: Certifications such as Common Criteria EAL 6+ and FIPS 140-3 are becoming procurement prerequisites in critical sectors like healthcare and energy.

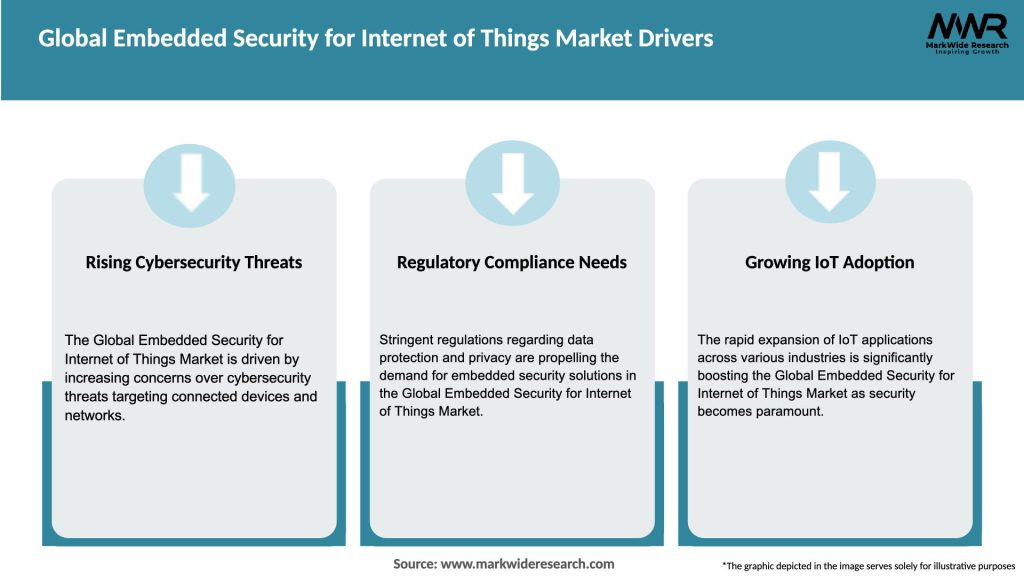

Market Drivers

Rising Cyber Threats: IoT devices represent an expanding attack surface for botnets, ransomware, and supply-chain attacks, necessitating robust embedded protections.

Regulatory Compliance: Laws like Europe’s RED directive and California’s SB-327 require manufacturers to embed baseline security measures (unique credentials, secure update mechanisms).

Device Proliferation: With over 30 billion connected devices forecast by 2030, scalable embedded security solutions are essential to manage identity, trust, and confidentiality at IoT scale.

Edge Computing Growth: Shifting data processing to the edge heightens the need for local encryption, secure boot, and tamper detection within endpoint hardware.

Supply-Chain Assurance: Growing emphasis on hardware provenance and silicon authentication to prevent counterfeit chips and ensure integrity of IoT devices.

Complexity of Integration: OEMs face steep learning curves integrating hardware security designs, requiring specialized expertise and tooling.

Legacy Device Inertia: Existing IoT deployments often lack retrofit paths for embedded security, extending vulnerability exposure.

Fragmented Standards: A plethora of overlapping specifications (e.g., PSA Certified, IoXt Alliance profiles) can confuse buyers seeking clear compliance roadmaps.

Performance Trade-offs: Security features such as encryption and secure boot can impact device performance, power draw, and boot time in resource-constrained endpoints.

Market Opportunities

Lightweight Cryptography: Development of ultra-efficient algorithms (e.g., NIST’s post-quantum finalists) tailored for constrained devices will broaden embedded security adoption.

Security in AIoT: As AI workloads move to the edge, embedding secure enclaves for model protection, data confidentiality, and intellectual-property safeguarding presents new avenues.

Subscription-Based Security: Managed security services bundled with hardware (Security-as-a-Service) offer OEMs recurring revenue and simplified update models.

Functional Safety Convergence: Merging ISO 26262 functional safety features with security modules in automotive SoCs unlocks opportunities in autonomous and connected vehicles.

Developer Ecosystems: Expanding value-added toolchains, reference designs, and open-source frameworks (e.g., OP-TEE) will lower barriers for system designers.

Market Dynamics

Platform Consolidation: Semiconductor leaders are integrating secure elements directly into mainstream microcontroller families, reducing the need for external security chips.

Cloud-Device Partnerships: Alliances among cloud providers (AWS IoT, Azure Sphere) and hardware vendors deliver end-to-end secure provisioning and lifecycle management services.

M&A Activity: Strategic acquisitions of security-IP houses and software startups by major SoC vendors accelerate in-house capabilities and broaden product suites.

Open Standards Push: Initiatives like PSA Certified and FiRa Consortium’s UWB security profile drive interoperability and certification frameworks.

Vertical-Specific Solutions: Customized offerings—for example, HIPAA-compliant modules for healthcare wearables or IEC 62443-aligned devices for industrial control systems—are gaining prominence.

Regional Analysis

North America: Largest market share, fueled by early adoption in industrial IoT, automotive telematics, and smart buildings, alongside strong regulatory and certification infrastructure.

Europe: Growth driven by GDPR data-privacy requirements, RED 2014/53/EU security mandates, and robust smart-city pilots with integrated security roadmaps.

Asia-Pacific: Fastest CAGR, led by China’s domestic semiconductor push, South Korea’s smart factory rollouts, and Japan’s connected automotive investments.

Latin America: Emerging deployments in energy and agriculture, with government incentives for protected IoT networks in critical infrastructure.

Middle East & Africa: Selective adoption in oil & gas, utilities, and defense sectors, often through partnerships with global security vendors and systems integrators.

Competitive Landscape

Leading Companies in the Global Embedded Security for Internet of Things Market:

Infineon Technologies AG

NXP Semiconductors N.V.

STMicroelectronics N.V.

Microchip Technology Inc.

Renesas Electronics Corporation

Texas Instruments Incorporated

Intel Corporation

Cisco Systems, Inc.

Gemalto NV (Thales Group)

IDEMIA

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

By Hardware Component: Secure Elements (SE), TPM/ Root-of-Trust Modules, Hardware Crypto Accelerators, Secure Microcontrollers.

By Software Solution: Secure Bootloaders, Firmware Signing/Verification, Secure OTA Update Frameworks, Trusted Execution Environments (TEEs).

By End-Use Industry: Industrial Automation, Automotive, Healthcare, Smart Home & Building, Consumer Electronics, Energy & Utilities.

Secure Elements: Highly tamper-resistant chips providing isolated storage for keys and certificates; ideal for payment terminals and smart cards.

Hardware Crypto Accelerators: Offload compute-intensive cryptography (AES, ECC, SHA) from main CPU, improving throughput and power efficiency.

Trusted Execution Environments (TEEs): Software-isolated zones leveraging TrustZone or similar architectures for secure app execution and credential management.

Secure Bootloaders: Ensure authenticity and integrity of firmware at each boot cycle, preventing unauthorized code from running.

Secure OTA Updates: End-to-end encrypted and authenticated update pipelines that protect device fleets from supply-chain attacks.

Key Benefits for Industry Participants and Stakeholders

Enhanced Device Trust: Hardware-based roots of trust foster strong device identity, preventing counterfeit and identity spoofing.

Data Protection: End-to-end encryption and secure storage guard sensitive data at rest and in transit, bolstering privacy compliance.

Operational Continuity: Early detection of firmware anomalies and secure update processes reduce downtime from malware or misconfiguration.

Regulatory Alignment: Integrated security modules simplify meeting global mandates, reducing audit and certification burdens.

Brand Reputation: Demonstrable “secure by design” credentials enhance customer confidence and differentiate products in crowded markets.

SWOT Analysis Strengths:

Hardware-anchored security reduces attack surface and resists software exploits.

Broad ecosystem support from semiconductor vendors, OS providers, and cloud platforms.

Scalability across diverse IoT form factors and performance envelopes.

Weaknesses:

Increased BOM cost and design complexity for highly cost-sensitive consumer devices.

Long design cycles and certification processes can delay time to market.

AI-Enhanced Threat Detection: Embedding lightweight anomaly-detection algorithms on device to identify malicious behavior in real time.

Open-Source Security Frameworks: Community-driven projects (e.g., Zephyr, OP-TEE) simplifying integration and accelerating time to prototype.

Post-Quantum Readiness: Early support for quantum-resistant algorithms (e.g., CRYSTALS-Kyber) in hardware accelerators.

Covid-19 Impact The pandemic accelerated adoption of remote monitoring and contactless IoT solutions in healthcare, manufacturing, and logistics—heightening awareness of endpoint security risks. Supply-chain disruptions prompted device makers to localize secure element sourcing and adopt over-the-air update mechanisms to patch vulnerabilities without physical access. Moreover, remote workforce expansions increased dependence on secure home-office IoT gateways, driving embedded security requirements in consumer routers and peripherals.

Key Industry Developments

Arm’s acquisition of Treasure Data enabled integration of cloud-hosted device-management with on-chip TrustZone.

NXP and Wipro partnership launched a secure provisioning service for large-scale IoT rollouts in industrial and energy sectors.

Infineon released OPTIGA™ Connect: a turnkey solution combining secure elements with cloud lifecycle services.

Microchip’s acquisition of Secure Thingz enriched its portfolio with CertX and EmSPARK security-certification toolchains.

Analyst Suggestions

Adopt “Security by Design”: Incorporate embedded security modules early in product development to avoid retrofits and cost overruns.

Leverage Certification: Pursue recognized certifications (PSA, Common Criteria) to build market trust and facilitate procurement by regulated buyers.

Embrace Ecosystems: Partner with cloud and OS vendors to offer integrated hardware-software security stacks, reducing complexity for OEMs.

Invest in Post-Quantum Research: Prototype and roadmap quantum-resistant cryptography to future-proof device fleets.

Educate Developers: Provide accessible SDKs, reference designs, and training to accelerate adoption among hardware and firmware engineers.

Future Outlook Embedded security will become a de facto requirement for virtually all IoT deployments as attack sophistication grows and regulatory expectations solidify. We anticipate convergence of security, safety, and functional-safety features into unified SoC platforms—particularly in automotive, healthcare, and industrial segments. Subscription-based management services will proliferate, offering device makers predictable revenue streams and cumulative security intelligence. As edge AI accelerates, secure enclaves that protect both data and ML models will emerge as critical components of tomorrow’s smart, autonomous systems.

Conclusion The Global Embedded Security for IoT market is entering a phase of strategic maturation, where hardware-anchored trust, seamless software integration, and certified lifecyle services converge to protect expansive device networks. Stakeholders who embed robust security early, align with open standards, and partner across cloud and semiconductor ecosystems will capture leadership positions. In an era defined by ubiquitous connectivity, embedded security is not merely an add-on—but the essential foundation for resilient, trustworthy IoT solutions.

What is Global Embedded Security for Internet of Things?

Global Embedded Security for Internet of Things refers to the integration of security measures within IoT devices to protect against unauthorized access, data breaches, and cyber threats. This includes hardware and software solutions designed to ensure the integrity and confidentiality of data transmitted between devices.

Which companies are leading in the Global Embedded Security for Internet of Things market?

Leading companies in the Global Embedded Security for Internet of Things market include Gemalto, Infineon Technologies, and Microchip Technology, among others.

What are the key drivers of growth in the Global Embedded Security for Internet of Things market?

Key drivers of growth in the Global Embedded Security for Internet of Things market include the increasing number of connected devices, rising concerns over data privacy and security, and the growing adoption of IoT in various sectors such as healthcare, automotive, and smart cities.

What challenges does the Global Embedded Security for Internet of Things market face?

The Global Embedded Security for Internet of Things market faces challenges such as the complexity of securing diverse IoT devices, the rapid pace of technological advancements, and the lack of standardized security protocols across different platforms.

What opportunities exist in the Global Embedded Security for Internet of Things market?

Opportunities in the Global Embedded Security for Internet of Things market include the development of advanced encryption technologies, the rise of edge computing, and the increasing demand for secure IoT solutions in industries like manufacturing and smart home applications.

What trends are shaping the Global Embedded Security for Internet of Things market?

Trends shaping the Global Embedded Security for Internet of Things market include the integration of artificial intelligence for threat detection, the shift towards decentralized security models, and the growing emphasis on regulatory compliance and data protection standards.

Leading Companies in the Global Embedded Security for Internet of Things Market:

Infineon Technologies AG

NXP Semiconductors N.V.

STMicroelectronics N.V.

Microchip Technology Inc.

Renesas Electronics Corporation

Texas Instruments Incorporated

Intel Corporation

Cisco Systems, Inc.

Gemalto NV (Thales Group)

IDEMIA

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.