444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The global ducted air conditioning unit market is a rapidly growing sector within the HVAC (Heating, Ventilation, and Air Conditioning) industry. Ducted air conditioning systems are designed to provide efficient and uniform cooling or heating throughout a building or a specific area. These systems consist of a central unit that cools or heats the air and distributes it through a network of ducts and vents installed in the walls, floors, or ceilings.

Ducted air conditioning units offer several advantages over traditional cooling or heating solutions. They provide centralized control, allowing users to set and maintain the desired temperature across different zones or rooms. Additionally, ducted systems are known for their discreet and aesthetically pleasing design as most of the components are hidden within the building’s structure.

Executive Summary

The global ducted air conditioning unit market has witnessed significant growth in recent years, driven by factors such as rising urbanization, increasing disposable incomes, and the growing demand for energy-efficient cooling and heating solutions. The market is highly competitive, with numerous players offering a wide range of products and services to cater to the diverse needs of residential, commercial, and industrial sectors.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Asia Pacific Dominance: Asia Pacific accounts for over 40% of global demand, driven by rapid urbanization in China, India, Southeast Asia, and Australia’s commercial construction boom.

VRF Adoption: Variable refrigerant flow ducted systems are growing at a CAGR of 10–12%, owing to their superior part-load efficiency and zoning flexibility.

Energy Efficiency Push: Government incentives and green building certifications (LEED, BREEAM) accelerate replacement of fixed-speed ducted units with inverter-driven models, reducing energy consumption by up to 30%.

Refrigerant Transition: Shift from high-GWP HFC-410A to lower-GWP alternatives (R-32, R-452B) is a key driver of product innovation and regulatory compliance.

Smart HVAC Integration: Growth in connected HVAC solutions—leveraging predictive analytics and remote monitoring—enhances system reliability and reduces lifecycle costs.

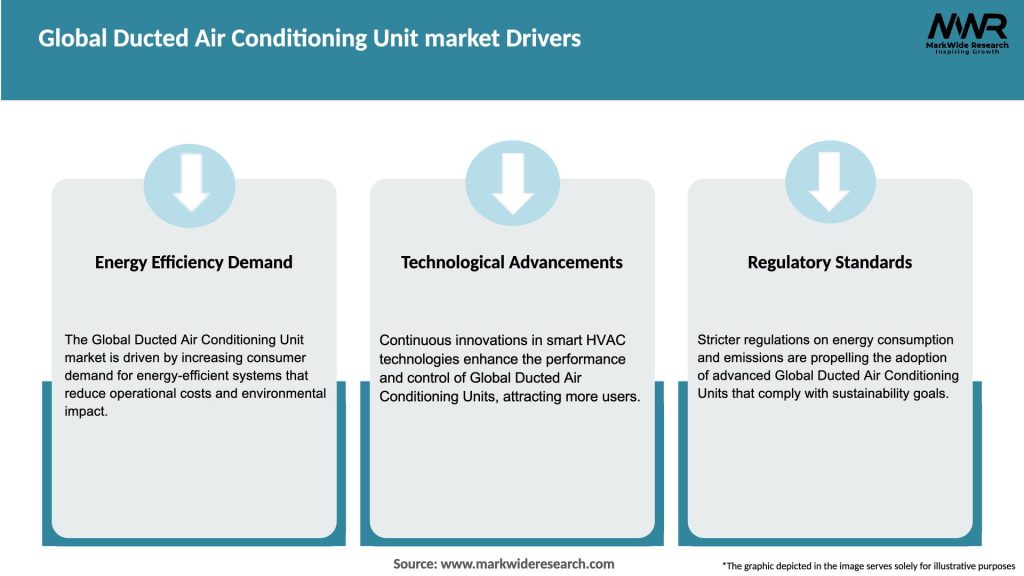

Market Drivers

Construction Growth: Expansion of residential complexes, commercial real estate, hospitality, and healthcare infrastructure in emerging and developed markets increases system installations.

Climate Change & Comfort Demand: Rising global temperatures and consumer expectations for indoor comfort propel demand for high-capacity, reliable ducted solutions.

Regulatory Environment: Stricter energy performance standards (e.g., U.S. DOE efficiency levels, EU Ecodesign) and refrigerant regulations drive uptake of high-efficiency, low-GWP systems.

Technology Advancements: Inverter-driven compressors, EC fan motors, heat recovery, and VRF strategies improve efficiency, reduce operating costs, and support net-zero building goals.

Retrofit & Replacement Market: Aging ducted units in developed regions prompt retrofit projects and upgrades to meet modern performance criteria and sustainability targets.

Market Restraints

High Upfront Costs: Capital expenditure for high-efficiency ducted VRF and smart systems can be 20–30% higher than conventional units, deterring cost-sensitive projects.

Installation Complexity: Ductwork design, space constraints, and skilled labor requirements add to project timelines and costs.

Maintenance Requirements: Periodic duct cleaning, filter replacement, and refrigerant leak detection are essential to maintain performance and indoor air quality.

Energy Infrastructure Variability: In regions with unreliable power supply or high electricity tariffs, operational costs can offset efficiency gains.

Competition from Alternatives: Split-system and ductless mini-split solutions offer lower-cost, room-by-room comfort, competing in residential and light commercial segments.

Market Opportunities

Integrated Building Solutions: Bundling ducted HVAC with BMS, lighting, and renewables (solar PV, heat pumps) creates holistic energy management offerings.

District Cooling Applications: Large-scale chilled water networks employing centralized chillers and ducted air handlers offer efficiency benefits in hot-climate urban districts.

Indoor Air Quality (IAQ) Focus: Incorporation of HEPA filtration, UV-C disinfection, and humidity control in ducted systems addresses health and wellness trends.

Light Commercial Market: Growth in data centers, server rooms, and laboratories requiring precise environmental control presents specialized ducted solution demand.

Modular & Prefabricated Systems: Factory-built duct modules and plug-and-play units reduce onsite labor and speed installation in high-volume residential developments.

Market Dynamics

Consolidation & Partnerships: M&A among HVAC legacy players and technology entrants accelerates portfolio expansion into smart, low-GWP solutions.

Service Models Evolution: OEMs and service providers offering performance-based maintenance contracts and remote diagnostics to ensure uptime and optimize lifecycle costs.

Digital Twin & Simulation: CFD and digital-twin modeling of duct networks and control algorithms enhance design accuracy, reduce commissioning errors, and improve comfort outcomes.

Training & Certification: Growth of HVAC training programs and certifications (e.g., LEED HVAC designer, BREEAM assessor) builds technical capacity for complex ducted projects.

Sustainable Finance: Green bonds and ESG-linked financing for commercial building upgrades support investments in high-efficiency ducted systems.

Regional Analysis

Asia Pacific: Rapid urban construction in China, India, and Southeast Asia; strong growth in Australia’s high-rise residential and commercial sectors; local manufacturing hubs lower costs.

North America: Mature market with significant retrofit activity; California Title 24 and DOE efficiency standards drive high-efficiency ducted model sales; established service networks.

Europe: High adoption of heat pump-based ducted systems; stringent Ecodesign and F-gas regulations; Scandinavian markets lead in geothermal integration.

Middle East & Africa: Demand for large-capacity rooftop ducted units in GCC projects; public-private megaprojects (Expo 2020, NEOM) increase luxury residential and commercial installations.

Latin America: Infrastructure modernization in Brazil and Mexico; rising commercial real estate and healthcare construction; market evolving toward inverter-driven ducted AC.

Competitive Landscape

Leadingcompanies in the Global Ducted Air Conditioning Unit Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The ducted air conditioning unit market can be segmented based on various factors, including:

Category-wise Insights

1. Single-zone Ducted Systems: Single-zone ducted systems refer to those designed to provide cooling or heating to a single area or room. These systems are commonly used in residential buildings where individual temperature control is desired. Single-zone ducted systems are relatively simpler in design and installation, making them a cost-effective solution for smaller spaces.

2. Multi-zone Ducted Systems: Multi-zone ducted systems are designed to provide cooling or heating to multiple zones or rooms within a building. These systems offer greater flexibility and control as they allow different areas to be maintained at different temperatures simultaneously. Multi-zone ducted systems are commonly used in larger residential properties, commercial buildings, and institutions where diverse temperature requirements exist.

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Electrification of Heating: Widespread adoption of heat-pump–based ducted systems replacing gas furnaces in cold climates.

IoT & Smart Controls: Remote diagnostics, voice control integration, and adaptive learning algorithms optimize comfort and efficiency.

Natural Refrigerants: Pilot projects using R-290 (propane) and CO₂ reef-friendly refrigerants for ultra-low GWP operation.

Prefabricated MEP Solutions: Factory-assembled duct and unit modules reduce onsite labor and accelerate project timelines.

Health & Wellness Features: Systems incorporating bipolar ionization, UVC sterilization, and HEPA filtration to improve indoor air quality and occupant well-being.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the ducted air conditioning unit market. The initial outbreak led to disruptions in the global supply chain, affecting manufacturing and distribution activities. Lockdowns and restrictions on construction and commercial activities further slowed down market growth.

However, as restrictions eased and economies began to recover, the market witnessed a gradual rebound. The need for improved indoor air quality and ventilation in buildings to reduce the risk of virus transmission has increased the demand for ducted air conditioning units. Additionally, the trend of remote work and increased time spent at home has led to higher demand for residential HVAC systems.

Key Industry Developments

Analyst Suggestions

Future Outlook

The global ducted air conditioning unit market is expected to witness steady growth in the coming years. Factors such as increasing urbanization, rising disposable incomes, and the need for energy-efficient cooling and heating solutions are expected to drive market expansion. Technological advancements, such as the integration of smart controls and IoT, will further enhance the market’s growth potential. However, challenges such as regulatory frameworks, environmental concerns, and economic uncertainties may pose obstacles to market growth. Manufacturers and industry participants should stay abreast of market trends, invest in research and development, and adapt to evolving customer needs to maintain a competitive edge.

Conclusion

The global ducted air conditioning unit market presents promising opportunities for manufacturers, suppliers, and industry participants. With increasing demand for energy-efficient and sustainable HVAC solutions, the market is expected to grow steadily in the coming years. Technological advancements, smart controls, and the integration of IoT offer avenues for innovation and differentiation. To thrive in the competitive landscape, companies should focus on product innovation, expansion into emerging markets, and collaboration with building automation companies. Continuous investment in research and development, along with a customer-centric approach, will be crucial to success in the dynamic ducted air conditioning unit market.

What is Ducted Air Conditioning Unit?

A Ducted Air Conditioning Unit is a centralized cooling system that distributes conditioned air through a network of ducts to various rooms or areas within a building. It is commonly used in residential and commercial settings for efficient temperature control.

What are the key players in the Global Ducted Air Conditioning Unit market?

Key players in the Global Ducted Air Conditioning Unit market include Daikin Industries, Mitsubishi Electric, Carrier Global Corporation, and Trane Technologies, among others.

What are the main drivers of the Global Ducted Air Conditioning Unit market?

The main drivers of the Global Ducted Air Conditioning Unit market include the increasing demand for energy-efficient cooling solutions, rising urbanization, and the growing trend of smart home technologies that enhance user comfort.

What challenges does the Global Ducted Air Conditioning Unit market face?

The Global Ducted Air Conditioning Unit market faces challenges such as high installation costs, maintenance complexities, and regulatory pressures regarding energy efficiency and environmental impact.

What opportunities exist in the Global Ducted Air Conditioning Unit market?

Opportunities in the Global Ducted Air Conditioning Unit market include advancements in inverter technology, the integration of IoT for smart controls, and the increasing focus on sustainable and eco-friendly cooling solutions.

What trends are shaping the Global Ducted Air Conditioning Unit market?

Trends shaping the Global Ducted Air Conditioning Unit market include the shift towards variable refrigerant flow systems, the adoption of energy-efficient models, and the growing popularity of multi-zone systems that allow for customized climate control.

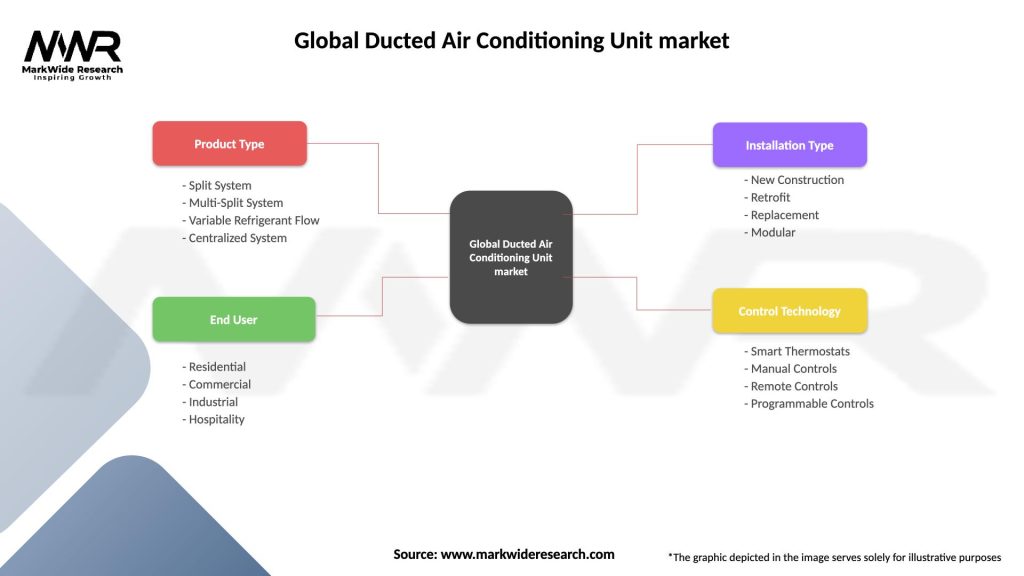

Global Ducted Air Conditioning Unit market

| Segmentation Details | Description |

|---|---|

| Product Type | Split System, Multi-Split System, Variable Refrigerant Flow, Centralized System |

| End User | Residential, Commercial, Industrial, Hospitality |

| Installation Type | New Construction, Retrofit, Replacement, Modular |

| Control Technology | Smart Thermostats, Manual Controls, Remote Controls, Programmable Controls |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leadingcompanies in the Global Ducted Air Conditioning Unit Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA