444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Suite #BAA205 Torrance, CA 90503 USA

24/7 Customer Support

Email us at

Corporate User License

Unlimited User Access, Post-Sale Support, Free Updates, Reports in English & Major Languages, and more

$2450

Market Overview

The student loan market in Germany serves as a crucial financial resource for students pursuing higher education, offering funding for tuition fees, living expenses, and other educational costs. With a well-established higher education system and a strong emphasis on academic excellence, Germany attracts a significant number of domestic and international students seeking quality education and career opportunities. The student loan market in Germany plays a vital role in promoting educational access, supporting student success, and fostering social mobility and economic development.

Meaning

The student loan market in Germany refers to the financial ecosystem comprising government-sponsored loan programs, private lending institutions, and nonprofit organizations that provide funding to students pursuing higher education. Student loans in Germany may cover tuition fees, living expenses, books, supplies, and other educational-related costs, enabling students to pursue their academic goals and advance their careers. These loans may be offered on favorable terms, including low-interest rates, flexible repayment options, and borrower-friendly features, to promote access and affordability in higher education.

Executive Summary

The student loan market in Germany has experienced significant growth in recent years, driven by increasing demand for higher education, rising tuition costs, and the need for financial assistance among students and families. Government-sponsored loan programs, such as BAföG (Federal Training Assistance Act), play a central role in providing affordable and accessible financing options to eligible students, while private lenders offer supplementary loans with competitive terms and borrower benefits. The student loan market in Germany offers numerous opportunities for industry participants and stakeholders, but it also faces challenges such as affordability concerns, regulatory complexities, and borrower debt burdens. Understanding the key market insights, drivers, restraints, and dynamics is essential for stakeholders to navigate the evolving landscape of the student loan market in Germany and promote positive outcomes for borrowers.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The student loan market in Germany operates in a dynamic environment influenced by economic conditions, demographic trends, policy changes, and technological advancements. These dynamics shape the availability, accessibility, and affordability of student loans, impacting borrower outcomes and market performance. Understanding the market dynamics is essential for stakeholders to identify opportunities, mitigate risks, and adapt to evolving trends in the student loan market.

Regional Analysis

The student loan market in Germany exhibits regional variations due to differences in educational infrastructure, economic development, demographic composition, and cultural preferences. Regional disparities in access to higher education, financial aid availability, and loan utilization may impact borrower experiences and outcomes across different regions in Germany. Understanding regional nuances and market dynamics is critical for stakeholders to tailor their strategies and interventions to address local needs and promote equitable access to higher education financing.

Competitive Landscape

Leading Companies for Germany Student Loan Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

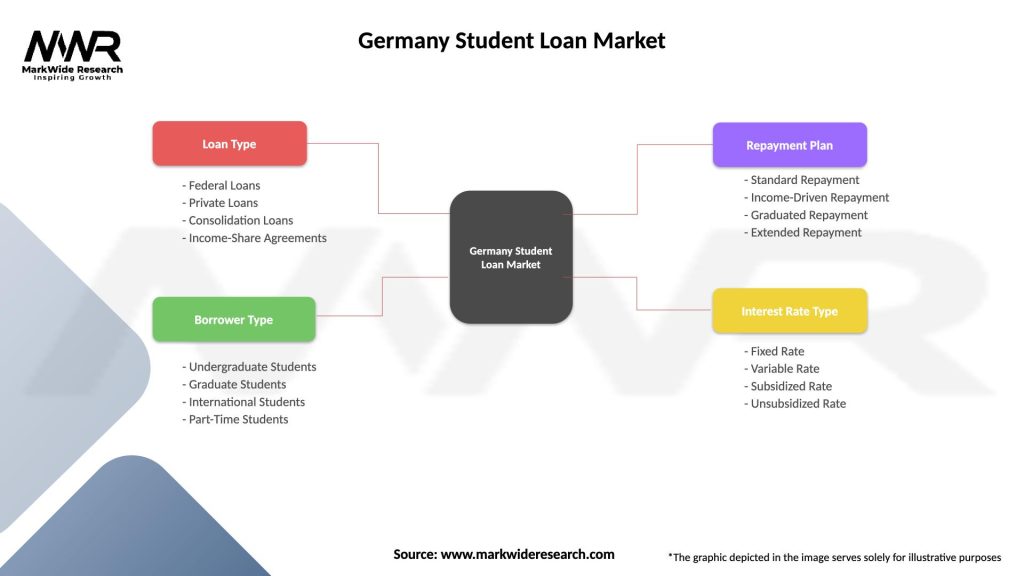

Segmentation

The student loan market in Germany can be segmented based on various factors, including:

Segmentation provides insights into the diverse needs, preferences, and behaviors of borrowers in the student loan market in Germany, enabling stakeholders to tailor their products, services, and marketing strategies to specific market segments.

Category-wise Insights

Category-wise insights offer a comprehensive understanding of the diverse funding sources and financing mechanisms available to students in the student loan market in Germany, facilitating informed decision-making and financial planning for higher education.

Key Benefits for Borrowers and Stakeholders

The student loan market in Germany offers several benefits for borrowers and stakeholders:

Key benefits for borrowers and stakeholders underscore the importance of student loans as a critical financial tool for accessing higher education, promoting educational opportunity, and fostering socioeconomic mobility in Germany.

SWOT Analysis

A SWOT analysis provides an overview of the strengths, weaknesses, opportunities, and threats in the student loan market in Germany:

Strengths:

Weaknesses:

Opportunities:

Threats:

Understanding these factors through a SWOT analysis helps stakeholders identify strategic priorities, mitigate risks, capitalize on opportunities, and address challenges in the student loan market in Germany.

Market Key Trends

Market key trends reflect the evolving landscape of the student loan market in Germany, driven by technological advancements, consumer preferences, regulatory changes, and market dynamics.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the student loan market in Germany, affecting borrowers, lenders, and policymakers. Some key impacts include:

The COVID-19 impact underscores the importance of resilience, adaptability, and collaboration in navigating crises and promoting positive outcomes in the student loan market in Germany.

Key Industry Developments

Key industry developments reflect ongoing efforts to promote borrower financial wellness, improve loan affordability, and strengthen regulatory oversight in the student loan market in Germany.

Analyst Suggestions

Analyst suggestions provide actionable recommendations for borrowers to navigate the student loan market effectively, manage their debt responsibly, and achieve financial success in Germany.

Future Outlook

The student loan market in Germany is expected to evolve in response to changing demographics, economic conditions, technological advancements, and regulatory reforms. Some key trends and developments shaping the future outlook of the market include:

The future outlook of the student loan market in Germany is characterized by opportunities for innovation, collaboration, and positive change, as stakeholders work together to promote access, affordability, and student success in higher education financing.

Conclusion

The student loan market in Germany plays a vital role in supporting access, affordability, and success in higher education, providing financial assistance to students pursuing their academic aspirations. Government-sponsored loan programs, private lending options, and nonprofit initiatives offer diverse financing solutions to meet the diverse needs of students and families.

While the student loan market presents opportunities for borrowers and stakeholders, it also faces challenges such as affordability concerns, debt burdens, and regulatory complexities. Addressing these challenges requires collaboration, innovation, and strategic interventions to promote positive outcomes for borrowers and ensure the long-term sustainability of student financing.

What is Germany Student Loan?

Germany Student Loan refers to financial assistance provided to students in Germany to help cover their educational expenses, including tuition fees, living costs, and study materials. These loans can be offered by government bodies, banks, or private institutions.

What are the key players in the Germany Student Loan Market?

Key players in the Germany Student Loan Market include KfW Bank, Deutsche Bank, and Sparkasse, which provide various loan products tailored for students. These institutions compete to offer favorable terms and conditions to attract borrowers among others.

What are the growth factors driving the Germany Student Loan Market?

The growth of the Germany Student Loan Market is driven by increasing enrollment in higher education, rising tuition costs, and a growing awareness of financial aid options among students. Additionally, government initiatives to support education financing contribute to market expansion.

What challenges does the Germany Student Loan Market face?

The Germany Student Loan Market faces challenges such as rising student debt levels, concerns over repayment burdens, and regulatory changes that may affect loan terms. These factors can impact student borrowing behavior and lender policies.

What opportunities exist in the Germany Student Loan Market?

Opportunities in the Germany Student Loan Market include the development of innovative loan products, partnerships with educational institutions, and the integration of digital platforms for easier loan management. These advancements can enhance accessibility and user experience for students.

What trends are shaping the Germany Student Loan Market?

Trends in the Germany Student Loan Market include a shift towards income-driven repayment plans, increased use of technology for loan applications, and a focus on financial literacy programs for students. These trends aim to improve financial outcomes for borrowers.

Germany Student Loan Market

| Segmentation Details | Description |

|---|---|

| Loan Type | Federal Loans, Private Loans, Consolidation Loans, Income-Share Agreements |

| Borrower Type | Undergraduate Students, Graduate Students, International Students, Part-Time Students |

| Repayment Plan | Standard Repayment, Income-Driven Repayment, Graduated Repayment, Extended Repayment |

| Interest Rate Type | Fixed Rate, Variable Rate, Subsidized Rate, Unsubsidized Rate |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies for Germany Student Loan Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Trusted by Global Leaders

Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified

Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights

Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support

Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access

Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion

We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance

Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

ISO AND IAF CERTIFIED

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

ISO AND IAF CERTIFIED

Suite #BAA205 Torrance, CA 90503 USA

24/7 Customer Support

Email us at