444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The France oral anti-diabetic drug market represents a critical component of the nation’s healthcare landscape, addressing the growing prevalence of diabetes mellitus across French populations. Market dynamics indicate substantial growth potential driven by increasing diabetes incidence, aging demographics, and evolving treatment paradigms. The French healthcare system’s emphasis on comprehensive diabetes management has created a robust environment for oral anti-diabetic medications, with healthcare providers increasingly adopting innovative therapeutic approaches.

Current market trends demonstrate significant adoption of next-generation oral anti-diabetic drugs, including SGLT-2 inhibitors, DPP-4 inhibitors, and GLP-1 receptor agonists. The market exhibits strong growth momentum with a projected CAGR of 6.2% over the forecast period, reflecting both increased patient populations and enhanced treatment accessibility through France’s universal healthcare coverage. Regional distribution shows concentrated demand in urban centers including Paris, Lyon, and Marseille, where specialized diabetes care centers drive prescription volumes.

Healthcare infrastructure in France supports comprehensive diabetes management through integrated care models, with approximately 78% of diabetic patients receiving regular monitoring and medication management. The market benefits from strong pharmaceutical research and development activities, with French biotech companies contributing to global innovation in oral diabetes therapeutics.

The France oral anti-diabetic drug market refers to the comprehensive ecosystem encompassing the development, manufacturing, distribution, and consumption of oral medications specifically designed to manage diabetes mellitus within French healthcare settings. This market includes various therapeutic classes of medications that help regulate blood glucose levels through different mechanisms of action, providing patients with convenient oral administration alternatives to injectable treatments.

Market scope encompasses traditional medications such as metformin and sulfonylureas, alongside newer therapeutic classes including dipeptidyl peptidase-4 inhibitors, sodium-glucose co-transporter-2 inhibitors, and alpha-glucosidase inhibitors. The market operates within France’s regulated healthcare framework, where prescription patterns are influenced by clinical guidelines, reimbursement policies, and physician preferences based on patient-specific factors.

Therapeutic significance extends beyond simple glucose control, with modern oral anti-diabetic drugs offering additional benefits such as cardiovascular protection, weight management, and reduced hypoglycemia risk. The market serves both Type 2 diabetes patients, who represent the majority of cases, and specific Type 1 diabetes patients who may benefit from adjunctive oral therapies alongside insulin treatment.

Strategic analysis of the France oral anti-diabetic drug market reveals a dynamic landscape characterized by robust growth potential and evolving therapeutic preferences. The market demonstrates strong fundamentals driven by increasing diabetes prevalence, with approximately 5.1% of the French population currently diagnosed with diabetes, creating sustained demand for effective oral therapeutic options.

Key market drivers include demographic shifts toward an aging population, lifestyle-related diabetes risk factors, and enhanced diagnostic capabilities leading to earlier disease detection. The French healthcare system’s commitment to preventive care and chronic disease management provides a supportive environment for oral anti-diabetic drug adoption, with reimbursement policies facilitating patient access to innovative treatments.

Competitive dynamics feature established pharmaceutical companies alongside emerging biotech firms developing next-generation therapies. Market leaders focus on differentiated product portfolios, with emphasis on combination therapies and personalized treatment approaches. Innovation trends prioritize medications offering superior efficacy, improved safety profiles, and enhanced patient convenience through reduced dosing frequencies.

Future outlook indicates continued market expansion supported by pipeline developments, regulatory approvals for new therapeutic classes, and growing emphasis on precision medicine approaches in diabetes management. The market is positioned for sustained growth with increasing integration of digital health technologies and personalized treatment protocols.

Market intelligence reveals several critical insights shaping the France oral anti-diabetic drug landscape. Primary insights demonstrate the following key market characteristics:

Strategic implications of these insights indicate opportunities for pharmaceutical companies to focus on combination products, personalized therapy approaches, and enhanced patient support programs to capture growing market segments.

Primary market drivers propelling growth in the France oral anti-diabetic drug market encompass demographic, clinical, and healthcare system factors. Demographic transitions represent the most significant driver, with France’s aging population creating sustained demand for diabetes management solutions. The proportion of individuals over 65 years continues expanding, correlating directly with increased diabetes incidence and medication requirements.

Lifestyle-related factors contribute substantially to market growth, including rising obesity rates, sedentary lifestyles, and dietary changes associated with urbanization. These factors drive Type 2 diabetes prevalence, creating expanding patient populations requiring long-term oral medication management. Healthcare awareness campaigns and improved screening programs result in earlier diabetes detection, leading to increased prescription volumes and extended treatment durations.

Clinical advancement drivers include development of safer, more effective oral therapies with improved side effect profiles. Modern medications offering cardiovascular benefits, weight management properties, and reduced hypoglycemia risk drive physician adoption and patient compliance. Treatment guideline evolution increasingly recommends early intensive therapy and combination approaches, supporting market expansion for multiple therapeutic classes.

Healthcare system drivers encompass France’s commitment to chronic disease management, comprehensive reimbursement policies, and integrated care models. The emphasis on preventive care and long-term health outcomes creates favorable conditions for oral anti-diabetic drug utilization, with healthcare providers incentivized to optimize diabetes management through appropriate medication selection.

Significant market restraints impact the France oral anti-diabetic drug market despite overall positive growth trends. Cost containment pressures within the French healthcare system create challenges for premium-priced innovative medications, with health authorities increasingly scrutinizing cost-effectiveness ratios and demanding robust clinical evidence for reimbursement approvals.

Generic competition represents a substantial restraint, particularly for established therapeutic classes where patent expiration enables lower-cost alternatives. This dynamic pressures branded manufacturers to demonstrate clear clinical advantages and economic value propositions to maintain market share. Regulatory complexity associated with drug approval processes, safety monitoring requirements, and post-market surveillance creates barriers for new market entrants and delays product launches.

Clinical limitations of certain oral therapies restrict market expansion, including contraindications in patients with kidney disease, heart failure, or other comorbidities. These limitations necessitate alternative treatment approaches and reduce the addressable patient population for specific medication classes. Side effect profiles of some oral anti-diabetic drugs, including gastrointestinal issues, hypoglycemia risk, and potential cardiovascular concerns, impact physician prescribing patterns and patient adherence.

Market saturation in certain therapeutic segments creates competitive pressures and limits growth potential for established products. Healthcare budget constraints and increasing focus on cost-effective treatment protocols may favor generic alternatives over innovative branded medications, particularly in price-sensitive market segments.

Substantial market opportunities exist within the France oral anti-diabetic drug market, driven by unmet medical needs and evolving treatment paradigms. Personalized medicine represents a significant opportunity, with advances in pharmacogenomics enabling tailored therapy selection based on individual patient characteristics, genetic profiles, and metabolic responses.

Combination therapy development offers extensive opportunities for pharmaceutical companies to create fixed-dose combinations addressing multiple pathophysiological mechanisms simultaneously. These products provide enhanced convenience, improved compliance, and potentially superior clinical outcomes compared to separate medication regimens. Digital health integration creates opportunities for connected medication management systems, smart pill technologies, and patient monitoring platforms that enhance treatment effectiveness.

Emerging therapeutic targets present opportunities for next-generation oral anti-diabetic drugs addressing novel mechanisms of action. Research into gut microbiome modulation, circadian rhythm regulation, and metabolic pathway optimization may yield innovative treatment options. Pediatric diabetes management represents an underserved market segment with growing need for age-appropriate oral therapeutic options.

Market expansion opportunities include development of oral therapies for Type 1 diabetes adjunctive treatment, prediabetes intervention, and diabetes prevention in high-risk populations. Healthcare technology integration enables opportunities for medication adherence monitoring, real-time glucose management, and predictive analytics supporting optimal therapy selection and dosing optimization.

Complex market dynamics shape the France oral anti-diabetic drug landscape through interconnected clinical, economic, and regulatory factors. Supply chain dynamics involve pharmaceutical manufacturers, distributors, pharmacies, and healthcare providers working within France’s regulated healthcare framework to ensure consistent medication availability and quality standards.

Competitive dynamics feature intense rivalry among established pharmaceutical companies and emerging biotech firms developing innovative therapies. Market leaders leverage extensive clinical evidence, established physician relationships, and comprehensive patient support programs to maintain competitive advantages. Pricing dynamics reflect negotiations between manufacturers and French health authorities, with reimbursement decisions significantly influencing market access and adoption rates.

Clinical practice dynamics evolve continuously as new evidence emerges regarding optimal treatment protocols, combination therapy approaches, and personalized medicine strategies. Physician prescribing patterns adapt to updated clinical guidelines, safety data, and real-world effectiveness studies. Patient dynamics include changing preferences for convenient dosing regimens, minimal side effects, and comprehensive diabetes management approaches.

Regulatory dynamics encompass ongoing safety monitoring, post-market surveillance requirements, and evolving approval pathways for innovative therapies. Technology dynamics increasingly influence market development through digital health solutions, artificial intelligence applications, and connected medication management systems that enhance treatment outcomes and patient engagement.

Comprehensive research methodology employed for analyzing the France oral anti-diabetic drug market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability. Primary research includes structured interviews with healthcare professionals, pharmaceutical industry executives, regulatory officials, and patient advocacy groups to gather firsthand insights into market trends, challenges, and opportunities.

Secondary research encompasses analysis of published clinical studies, regulatory filings, healthcare databases, and industry reports to establish market baselines and identify emerging trends. Quantitative analysis utilizes prescription data, healthcare utilization statistics, and epidemiological studies to quantify market size, growth rates, and segmentation patterns.

Qualitative research methods include focus groups with healthcare providers and patients to understand treatment preferences, barriers to adoption, and unmet medical needs. Market modeling employs statistical techniques and forecasting algorithms to project future market trends based on demographic changes, clinical developments, and regulatory scenarios.

Data validation processes ensure research accuracy through triangulation of multiple sources, expert review panels, and sensitivity analysis of key assumptions. MarkWide Research methodology incorporates real-world evidence analysis, health economics evaluation, and competitive intelligence gathering to provide comprehensive market insights for stakeholders across the pharmaceutical value chain.

Regional market analysis reveals distinct patterns across French territories, with significant variations in diabetes prevalence, healthcare infrastructure, and medication utilization. Île-de-France region, encompassing Paris and surrounding areas, represents the largest market segment with 22% of national prescription volume, driven by high population density, specialized diabetes centers, and comprehensive healthcare facilities.

Auvergne-Rhône-Alpes demonstrates strong market presence with 14% market share, supported by major urban centers including Lyon and established pharmaceutical industry presence. The region benefits from advanced healthcare infrastructure and active clinical research programs contributing to innovative therapy adoption. Provence-Alpes-Côte d’Azur accounts for 11% of market volume, with Mediterranean lifestyle factors influencing diabetes prevalence and treatment patterns.

Northern regions including Hauts-de-France and Grand Est show higher diabetes prevalence rates correlating with socioeconomic factors and lifestyle patterns, creating concentrated demand for oral anti-diabetic medications. Rural regions face unique challenges including limited specialist availability and longer distances to healthcare facilities, influencing prescription patterns toward primary care-managed therapies.

Overseas territories including French Guiana, Martinique, and Réunion exhibit elevated diabetes rates with prevalence exceeding 8% in some areas, creating specialized market opportunities for culturally appropriate treatment approaches and telemedicine-supported care models.

Competitive landscape in the France oral anti-diabetic drug market features established pharmaceutical giants alongside innovative biotech companies developing next-generation therapies. Market leaders maintain strong positions through comprehensive product portfolios, extensive clinical evidence, and established healthcare provider relationships.

Competitive strategies focus on clinical differentiation, real-world evidence generation, and comprehensive patient support programs. Companies invest heavily in post-market studies demonstrating long-term safety and effectiveness to maintain competitive advantages in reimbursement negotiations and clinical guideline recommendations.

Market segmentation analysis reveals distinct categories based on therapeutic class, patient demographics, and clinical applications. By therapeutic class, the market divides into several key segments with varying growth trajectories and competitive dynamics.

By Drug Class:

By Patient Type:

By Distribution Channel:

Category-specific analysis provides detailed insights into performance and trends across major therapeutic classes within the France oral anti-diabetic drug market. Metformin category maintains market leadership through proven efficacy, excellent safety profile, and cost-effectiveness, with generic formulations ensuring broad accessibility across patient populations.

DPP-4 inhibitor category demonstrates strong growth momentum driven by superior tolerability profiles and low hypoglycemia risk. This category benefits from extensive clinical evidence supporting cardiovascular safety and effectiveness in diverse patient populations, including elderly individuals and those with renal impairment. Market penetration continues expanding as physicians gain confidence in long-term safety data.

SGLT-2 inhibitor category represents the fastest-growing segment with annual growth rates exceeding 18%, driven by compelling cardiovascular and renal outcome data. These medications offer unique benefits including weight loss, blood pressure reduction, and heart failure prevention, creating strong clinical differentiation. Adoption patterns show particular strength among cardiologists and nephrologists treating diabetic patients with comorbidities.

Combination therapy category exhibits robust growth as clinical guidelines increasingly recommend multi-mechanism approaches for optimal glucose control. Fixed-dose combinations provide enhanced patient convenience and improved adherence compared to separate medications. Innovation focus centers on developing novel combinations addressing complementary pathophysiological mechanisms while minimizing side effect profiles.

Industry participants across the France oral anti-diabetic drug market realize substantial benefits through strategic positioning and value creation opportunities. Pharmaceutical manufacturers benefit from sustained demand driven by chronic disease management requirements, enabling predictable revenue streams and long-term patient relationships supporting brand loyalty and market share retention.

Healthcare providers gain access to diverse therapeutic options enabling personalized treatment approaches based on individual patient characteristics, comorbidities, and treatment preferences. The availability of multiple oral therapy classes supports clinical flexibility and optimization of diabetes management protocols. Treatment outcomes improve through access to innovative medications offering superior efficacy and safety profiles.

Patients benefit from convenient oral administration routes, reduced injection burden, and improved quality of life compared to insulin-dependent regimens. Modern oral therapies offer enhanced tolerability, reduced hypoglycemia risk, and additional health benefits including cardiovascular protection and weight management. Healthcare accessibility through universal coverage ensures equitable access to essential diabetes medications.

Healthcare systems realize cost-effectiveness benefits through prevention of diabetes complications, reduced hospitalizations, and improved long-term health outcomes. Economic advantages include lower overall healthcare costs through effective chronic disease management and prevention of expensive complications requiring intensive medical interventions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends are reshaping the France oral anti-diabetic drug market through technological innovation, clinical advancement, and evolving patient care models. Personalized medicine emerges as a dominant trend, with pharmacogenomic testing and biomarker analysis enabling individualized therapy selection based on genetic profiles and metabolic characteristics.

Digital health integration represents a significant trend transforming diabetes management through connected devices, mobile applications, and artificial intelligence-powered treatment optimization. These technologies enable real-time glucose monitoring, medication adherence tracking, and predictive analytics supporting clinical decision-making. Telemedicine adoption accelerates, particularly in rural areas, improving access to specialist diabetes care and medication management.

Combination therapy trends show increasing preference for fixed-dose combinations addressing multiple pathophysiological mechanisms simultaneously. This approach improves patient convenience, enhances adherence, and potentially delivers superior clinical outcomes compared to separate medication regimens. Innovation focus shifts toward developing combinations with complementary mechanisms of action and minimal side effect overlap.

Value-based care trends emphasize outcomes-based pricing models and real-world evidence generation demonstrating long-term clinical and economic benefits. Patient-centric approaches prioritize quality of life improvements, treatment satisfaction, and shared decision-making in therapy selection. Sustainability trends drive development of environmentally friendly packaging and manufacturing processes addressing climate change concerns.

Recent industry developments highlight significant advances in oral anti-diabetic drug innovation, regulatory approvals, and market expansion strategies. Regulatory approvals for next-generation SGLT-2 inhibitors and novel combination products expand treatment options and drive market growth through enhanced clinical capabilities.

Clinical trial developments demonstrate promising results for innovative oral therapies targeting novel mechanisms of action, including gut microbiome modulation and circadian rhythm regulation. These developments indicate potential future market expansion through breakthrough therapeutic approaches. MarkWide Research analysis indicates increasing investment in precision medicine approaches and biomarker-guided therapy selection.

Strategic partnerships between pharmaceutical companies and technology firms accelerate development of digital health solutions integrated with oral diabetes medications. These collaborations create comprehensive diabetes management ecosystems combining medication therapy with digital monitoring and support services. Manufacturing developments include establishment of advanced production facilities and supply chain optimization initiatives ensuring consistent medication availability.

Market access developments encompass expanded reimbursement coverage for innovative therapies and streamlined approval processes for combination products. Research collaborations between academic institutions and pharmaceutical companies advance understanding of diabetes pathophysiology and identify new therapeutic targets for oral medication development.

Strategic recommendations for stakeholders in the France oral anti-diabetic drug market emphasize innovation, differentiation, and value demonstration. Pharmaceutical companies should prioritize development of combination therapies addressing multiple pathophysiological mechanisms while maintaining favorable safety profiles and patient convenience.

Investment priorities should focus on personalized medicine capabilities, including pharmacogenomic testing integration and biomarker-guided therapy selection. Companies should develop comprehensive patient support programs encompassing medication adherence monitoring, lifestyle counseling, and digital health integration to differentiate their offerings and improve treatment outcomes.

Market entry strategies for new participants should emphasize clinical differentiation through superior efficacy, safety, or convenience compared to existing therapies. Regulatory strategy should incorporate early engagement with French health authorities and robust real-world evidence generation supporting reimbursement applications and clinical guideline inclusion.

Healthcare providers should adopt evidence-based treatment protocols incorporating latest clinical guidelines and real-world effectiveness data. Technology integration recommendations include implementation of digital health platforms supporting medication management, patient monitoring, and treatment optimization. Collaboration strategies should emphasize multidisciplinary care teams and integrated diabetes management approaches maximizing patient outcomes while optimizing resource utilization.

Future market outlook for the France oral anti-diabetic drug market indicates sustained growth driven by demographic trends, clinical innovation, and evolving treatment paradigms. Market expansion is projected to continue with compound annual growth rates of 5.8% over the next five years, supported by increasing diabetes prevalence and adoption of innovative therapeutic approaches.

Innovation pipeline developments suggest emergence of breakthrough oral therapies targeting novel mechanisms including gut-brain axis modulation, metabolic pathway optimization, and immune system regulation. These advances may revolutionize diabetes treatment through enhanced efficacy and reduced side effect profiles. Personalized medicine adoption will accelerate, with genetic testing and biomarker analysis becoming standard components of therapy selection protocols.

Digital health integration will transform diabetes management through artificial intelligence-powered treatment optimization, predictive analytics, and connected medication management systems. MWR projections indicate that digital therapeutics will complement oral medications in comprehensive diabetes care ecosystems, improving patient outcomes and healthcare efficiency.

Market consolidation trends may emerge as companies seek to build comprehensive diabetes care portfolios through strategic acquisitions and partnerships. Regulatory evolution will likely streamline approval processes for combination products and digital health solutions while maintaining rigorous safety standards. Healthcare delivery models will increasingly emphasize value-based care and outcomes-focused treatment approaches, creating opportunities for innovative oral therapies demonstrating superior long-term clinical and economic benefits.

The France oral anti-diabetic drug market represents a dynamic and expanding healthcare sector characterized by robust growth potential, clinical innovation, and evolving treatment paradigms. Market fundamentals remain strong, supported by increasing diabetes prevalence, aging demographics, and comprehensive healthcare coverage ensuring broad medication access across patient populations.

Key success factors for market participants include clinical differentiation, value demonstration, and comprehensive patient support programs addressing the full spectrum of diabetes management needs. The market benefits from France’s advanced healthcare infrastructure, strong pharmaceutical industry presence, and commitment to evidence-based treatment protocols supporting optimal patient outcomes.

Future opportunities encompass personalized medicine advancement, digital health integration, and development of innovative combination therapies addressing multiple pathophysiological mechanisms. Strategic positioning requires focus on clinical excellence, real-world evidence generation, and collaborative approaches with healthcare providers and technology partners.

Market outlook indicates continued expansion driven by demographic trends, clinical innovation, and evolving healthcare delivery models emphasizing value-based care and patient-centric treatment approaches. The France oral anti-diabetic drug market is well-positioned for sustained growth, offering significant opportunities for stakeholders committed to advancing diabetes care through innovative therapeutic solutions and comprehensive patient support services.

What is Oral Anti-Diabetic Drug?

Oral Anti-Diabetic Drugs are medications used to manage blood sugar levels in individuals with diabetes. They work by various mechanisms, including increasing insulin sensitivity, stimulating insulin secretion, or reducing glucose production in the liver.

What are the key players in the France Oral Anti-Diabetic Drug Market?

Key players in the France Oral Anti-Diabetic Drug Market include Sanofi, Novo Nordisk, Merck, and AstraZeneca, among others. These companies are involved in the development and distribution of various oral anti-diabetic medications.

What are the growth factors driving the France Oral Anti-Diabetic Drug Market?

The growth of the France Oral Anti-Diabetic Drug Market is driven by the increasing prevalence of diabetes, rising awareness about diabetes management, and advancements in drug formulations. Additionally, the aging population contributes to the demand for effective diabetes treatments.

What challenges does the France Oral Anti-Diabetic Drug Market face?

The France Oral Anti-Diabetic Drug Market faces challenges such as stringent regulatory requirements, high competition among pharmaceutical companies, and the potential side effects associated with some oral anti-diabetic medications. These factors can impact market growth and drug adoption.

What opportunities exist in the France Oral Anti-Diabetic Drug Market?

Opportunities in the France Oral Anti-Diabetic Drug Market include the development of new drug classes, personalized medicine approaches, and the integration of digital health technologies for better diabetes management. These innovations can enhance treatment outcomes and patient adherence.

What trends are shaping the France Oral Anti-Diabetic Drug Market?

Trends in the France Oral Anti-Diabetic Drug Market include the increasing focus on combination therapies, the rise of generics, and the growing emphasis on patient-centric care. Additionally, there is a trend towards the use of real-world evidence to support drug efficacy and safety.

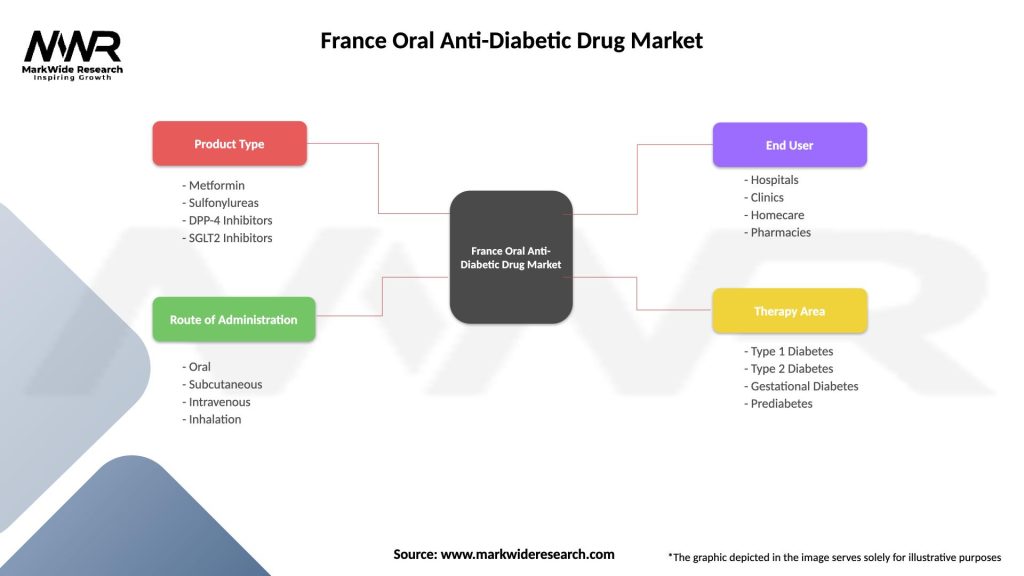

France Oral Anti-Diabetic Drug Market

| Segmentation Details | Description |

|---|---|

| Product Type | Metformin, Sulfonylureas, DPP-4 Inhibitors, SGLT2 Inhibitors |

| Route of Administration | Oral, Subcutaneous, Intravenous, Inhalation |

| End User | Hospitals, Clinics, Homecare, Pharmacies |

| Therapy Area | Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, Prediabetes |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the France Oral Anti-Diabetic Drug Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.