The France Business Income Insurance market serves as a critical component of the country’s insurance landscape, providing coverage and financial protection to businesses against income losses resulting from unforeseen events or disruptions. This market plays a crucial role in safeguarding businesses’ financial stability and continuity by compensating for lost revenue and operating expenses during periods of interruption or downtime.

Meaning

Business Income Insurance, also known as Business Interruption Insurance, is a type of coverage designed to protect businesses from financial losses caused by disruptions to their normal operations. These disruptions could arise from various factors, including natural disasters, fires, floods, vandalism, equipment breakdowns, or other unforeseen events. Business Income Insurance typically covers lost income, ongoing expenses, and additional costs incurred to mitigate the impact of the interruption, enabling businesses to recover and resume operations swiftly.

Executive Summary

The France Business Income Insurance market has witnessed steady growth in recent years, driven by increasing awareness among businesses about the importance of risk management and financial protection. With the growing frequency and severity of business interruptions due to factors such as natural disasters, cyber attacks, and supply chain disruptions, there is a rising demand for comprehensive insurance solutions that address the diverse needs of businesses across various sectors.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Risk Awareness: Businesses in France are becoming increasingly aware of the risks they face and the potential financial consequences of business interruptions. This heightened awareness has led to a greater emphasis on risk management strategies and the adoption of insurance solutions like Business Income Insurance to mitigate financial losses.

Regulatory Environment: The regulatory environment governing insurance in France plays a significant role in shaping the Business Income Insurance market. Insurance companies must adhere to strict regulations and standards set forth by regulatory bodies, ensuring transparency, fairness, and consumer protection in the insurance industry.

Industry Resilience: The resilience of businesses in France is a key factor driving the demand for Business Income Insurance. Businesses recognize the importance of financial protection against unforeseen events that could disrupt their operations and jeopardize their financial stability, prompting them to invest in comprehensive insurance coverage.

Emerging Risks: The evolving nature of risks, including cyber threats, geopolitical instability, and climate change-related events, presents new challenges for businesses and insurers alike. As businesses navigate these emerging risks, there is a growing need for innovative insurance solutions that provide adequate coverage and support in times of crisis.

Market Drivers

Increasing Business Interruptions: The frequency and severity of business interruptions in France have been on the rise, driven by factors such as extreme weather events, cyber attacks, and supply chain disruptions. This trend has heightened the demand for Business Income Insurance among businesses seeking financial protection against potential losses.

Complexity of Risks: Businesses are facing increasingly complex and interconnected risks that can have far-reaching consequences for their operations. The need for comprehensive insurance coverage that addresses a wide range of risks, including physical damage, business interruption, and contingent liabilities, is driving the growth of the Business Income Insurance market.

Supply Chain Vulnerabilities: Globalization has made supply chains more vulnerable to disruptions, whether due to natural disasters, geopolitical tensions, or pandemics. Businesses recognize the importance of protecting their supply chains and ensuring business continuity through insurance solutions like Business Income Insurance.

Digital Transformation: The digital transformation of businesses is creating new risks and vulnerabilities that need to be addressed through insurance coverage. As businesses rely more on digital technologies and online platforms, they face increased exposure to cyber threats and data breaches, highlighting the need for specialized insurance solutions.

Market Restraints

Underinsurance: Despite the growing awareness of risks and the importance of insurance, many businesses in France remain underinsured or uninsured against business interruptions. Factors such as cost constraints, lack of awareness, and misconceptions about insurance coverage can hinder businesses from adequately protecting themselves against potential losses.

Complex Claims Process: The claims process for Business Income Insurance can be complex and time-consuming, posing challenges for businesses seeking timely compensation for their losses. Insurers and businesses need to streamline the claims process and improve communication to ensure a smooth and efficient claims experience.

Limited Coverage Options: The availability of coverage options and policy features in the Business Income Insurance market may be limited, particularly for businesses with unique or specialized needs. Insurers need to offer flexible and customizable insurance solutions that address the specific risk profiles and requirements of different businesses.

Regulatory Compliance: Compliance with regulatory requirements and standards can be a challenge for insurers operating in the Business Income Insurance market. Insurers must navigate complex regulatory frameworks and ensure compliance with regulatory requirements while offering innovative and competitive insurance products and services.

Market Opportunities

Risk Management Services: There is a growing opportunity for insurers to offer value-added services related to risk management and loss prevention. By partnering with businesses to assess and mitigate risks, insurers can help businesses improve their resilience and reduce the likelihood and severity of business interruptions.

Tailored Insurance Solutions: Insurers can capitalize on the demand for tailored insurance solutions that address the specific needs and risk profiles of different industries and businesses. By offering customizable coverage options and policy features, insurers can attract a diverse range of clients and enhance their market competitiveness.

Digital Innovation: Digital innovation presents opportunities for insurers to streamline processes, enhance customer experience, and develop innovative insurance products and services. By leveraging technologies such as artificial intelligence, data analytics, and digital platforms, insurers can improve efficiency, reduce costs, and deliver more personalized insurance solutions to businesses.

Partnerships and Alliances: Collaboration and partnerships with other industry stakeholders, including risk management firms, technology providers, and industry associations, can create new opportunities for insurers in the Business Income Insurance market. By combining expertise and resources, insurers can offer comprehensive solutions that address the evolving needs of businesses and provide added value to clients.

Market Dynamics

The France Business Income Insurance market operates in a dynamic environment influenced by various factors such as economic conditions, regulatory changes, technological advancements, and industry trends. Understanding these market dynamics is essential for insurers to identify opportunities, mitigate risks, and adapt their strategies to remain competitive in the market.

Regional Analysis

The France Business Income Insurance market exhibits regional variations influenced by factors such as industry composition, economic activity, and exposure to risks. Key regions driving demand for Business Income Insurance in France include major urban centers, industrial hubs, and regions prone to natural disasters or other disruptive events.

Competitive Landscape

Leading Companies in France Business Income Insurance Market:

AXA Group

CNP Assurances

Groupama

Crédit Agricole Assurances

Generali Group

BNP Paribas Cardif

Société Générale Insurance

Allianz France

Covéa Group

AG2R La Mondiale

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

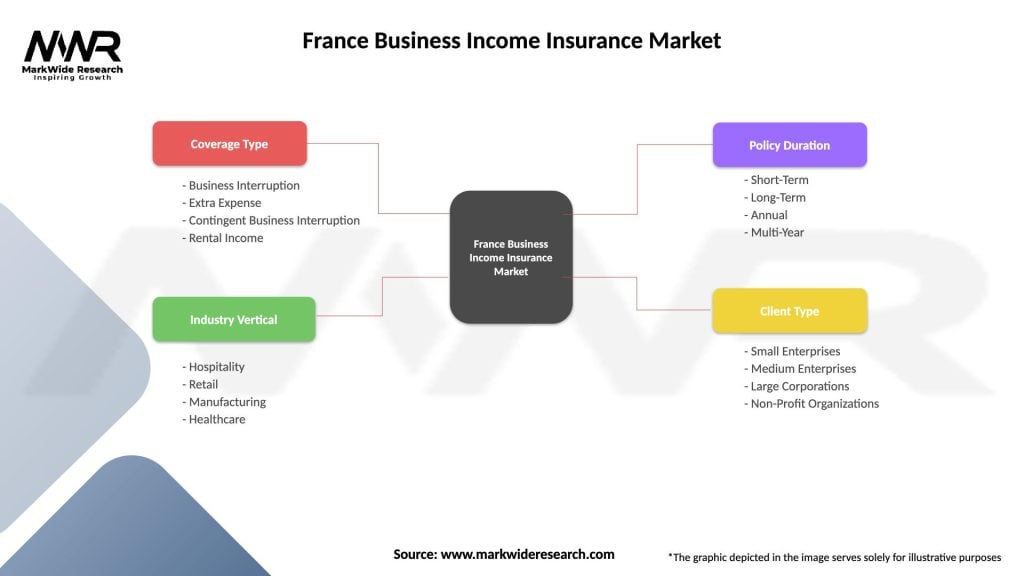

Segmentation

The France Business Income Insurance market can be segmented based on various factors such as industry vertical, business size, coverage type, and policy features. Segmenting the market enables insurers to target specific customer segments with tailored insurance solutions that address their unique needs and risk profiles.

Category-wise Insights

Industry Verticals: Different industry verticals have distinct risk profiles and insurance needs, requiring specialized insurance solutions tailored to their specific requirements. Insurers can develop industry-specific insurance products and services that address the unique challenges and opportunities faced by businesses in each vertical.

Business Size: The insurance needs of small and medium-sized enterprises (SMEs) may differ from those of large corporations, necessitating insurance solutions that are scalable, affordable, and flexible. Insurers can offer customized insurance packages designed to meet the needs of businesses of all sizes, from startups and SMEs to multinational corporations.

Coverage Type: Business Income Insurance can be offered as a standalone policy or as part of a broader insurance package that includes other types of coverage such as property insurance, liability insurance, and cyber insurance. Insurers can tailor coverage options and policy features to align with the specific risk management strategies and preferences of businesses.

Key Benefits for Industry Participants and Stakeholders

The France Business Income Insurance market offers several benefits for industry participants and stakeholders:

Financial Protection: Business Income Insurance provides businesses with financial protection against income losses resulting from business interruptions, enabling them to recover and resume operations swiftly.

Risk Management: Business Income Insurance encourages businesses to adopt proactive risk management strategies and measures to mitigate the likelihood and severity of business interruptions.

Business Continuity: By providing coverage for lost income, ongoing expenses, and additional costs incurred during a business interruption, Business Income Insurance helps businesses maintain continuity and resilience in the face of unforeseen events.

Peace of Mind: Having Business Income Insurance in place gives business owners peace of mind, knowing that they are protected against potential financial losses that could threaten the viability and sustainability of their businesses.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the France Business Income Insurance market:

Strengths:

Comprehensive coverage for business interruptions.

Support for business continuity and resilience.

Diverse range of insurance products and services.

Regulatory compliance and consumer protection.

Weaknesses:

Complex claims process and documentation requirements.

Underinsurance or lack of awareness among businesses.

Limited coverage options for specific industries or risks.

Opportunities:

Growth in demand for tailored insurance solutions.

Digital innovation and technology adoption.

Partnerships and alliances with industry stakeholders.

Expansion into emerging markets and industry verticals.

Threats:

Regulatory changes and compliance requirements.

Competition from domestic and international insurers.

Economic downturns and market volatility.

Emerging risks and uncertainties.

Understanding these factors through a SWOT analysis can help insurers identify areas of strength, address weaknesses, capitalize on opportunities, and mitigate threats in the France Business Income Insurance market.

Market Key Trends

Digitalization: The digital transformation of the insurance industry is driving innovation in Business Income Insurance, with insurers leveraging technologies such as artificial intelligence, data analytics, and digital platforms to enhance customer experience, streamline processes, and deliver more personalized insurance solutions.

Sustainability: There is a growing emphasis on sustainability and environmental stewardship in the insurance industry, with insurers integrating environmental, social, and governance (ESG) factors into their underwriting, risk assessment, and product development processes. Sustainable insurance solutions that promote resilience and risk mitigation are gaining traction in the market.

Customer-Centricity: Insurers are adopting a customer-centric approach to product design, distribution, and service delivery, focusing on understanding and meeting the evolving needs and preferences of businesses. Customer feedback, data analytics, and market insights are driving the development of tailored insurance solutions that provide value and address specific pain points.

Regulatory Compliance: Regulatory compliance and consumer protection remain top priorities for insurers operating in the Business Income Insurance market. Insurers must stay abreast of regulatory changes, adhere to industry standards, and uphold ethical practices to build trust with customers and regulators.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the France Business Income Insurance market, highlighting the importance of business continuity planning and financial protection against unforeseen events. Some key impacts of Covid-19 on the market include:

Increased Awareness: The pandemic has raised awareness among businesses about the importance of risk management and insurance coverage, leading to greater demand for Business Income Insurance as businesses seek to protect themselves against future disruptions.

Claims Activity: Insurers have experienced an increase in claims activity related to business interruptions caused by the pandemic, including claims for lost income, supply chain disruptions, and contingent business interruption losses. The surge in claims has put pressure on insurers to assess and process claims efficiently while maintaining financial stability.

Policy Changes: The pandemic has prompted insurers to review and update their policy wordings, coverage options, and exclusions to address emerging risks and uncertainties. Insurers are refining their underwriting criteria and risk assessment methodologies to better quantify and manage pandemic-related risks in their portfolios.

Digital Transformation: The pandemic has accelerated the digital transformation of the insurance industry, with insurers investing in digital platforms, online distribution channels, and remote service delivery capabilities to adapt to the changing needs and preferences of customers in a post-pandemic world.

Key Industry Developments

Pandemic Response: Insurers have implemented various measures to support businesses affected by the pandemic, including offering premium discounts, grace periods for premium payments, and flexible coverage options to help businesses maintain insurance coverage during challenging times.

Product Innovation: Insurers are innovating and diversifying their product offerings to address emerging risks and market trends, such as cyber insurance, pandemic coverage, and parametric insurance solutions tailored to specific industries and business needs.

Data Analytics: The use of data analytics and predictive modeling is becoming increasingly prevalent in underwriting, risk assessment, and claims management processes. Insurers are leveraging data-driven insights to enhance pricing accuracy, improve risk selection, and optimize claims handling efficiency.

Regulatory Engagement: Insurers are actively engaging with regulators, industry associations, and policymakers to shape regulatory frameworks and standards governing Business Income Insurance. Collaborative efforts aim to promote market stability, consumer protection, and industry resilience in the face of evolving risks and challenges.

Analyst Suggestions

Risk Assessment: Businesses should conduct comprehensive risk assessments to identify potential threats and vulnerabilities that could disrupt their operations and finances. Working with insurers and risk management professionals, businesses can develop customized risk management strategies and insurance solutions that provide adequate protection against business interruptions.

Policy Review: Businesses should review their existing insurance policies, including Business Income Insurance coverage, to ensure they have adequate protection against a wide range of risks and contingencies. Understanding policy terms, coverage limits, and exclusions is essential for making informed decisions and mitigating potential gaps in coverage.

Claims Preparation: Businesses should proactively prepare for potential business interruptions by documenting their operations, financial records, and continuity plans. Maintaining accurate records and documentation can facilitate the claims process and help ensure timely and fair compensation in the event of a covered loss.

Insurance Consultation: Businesses should seek advice and guidance from insurance professionals, brokers, and advisors who specialize in Business Income Insurance and risk management. Working with experienced professionals can help businesses navigate the complexities of insurance coverage, assess their risk exposures, and identify suitable insurance solutions.

Future Outlook

The France Business Income Insurance market is expected to continue growing and evolving in the coming years, driven by factors such as increasing awareness of risks, regulatory developments, technological advancements, and market dynamics. Insurers will need to adapt their strategies, products, and services to meet the evolving needs and preferences of businesses in a rapidly changing business environment.

Conclusion

The France Business Income Insurance market plays a vital role in safeguarding businesses against financial losses caused by business interruptions and disruptions. As businesses face increasingly complex and interconnected risks, the demand for comprehensive insurance solutions like Business Income Insurance is expected to grow. By understanding the market dynamics, emerging trends, and regulatory landscape, insurers can develop innovative and tailored insurance products and services that meet the evolving needs of businesses and contribute to their resilience and success.

What is Business Income Insurance?

Business Income Insurance is a type of coverage that protects businesses from loss of income due to disruptions, such as natural disasters or other unforeseen events. It helps cover ongoing expenses and lost profits during the period of recovery.

What are the key players in the France Business Income Insurance Market?

Key players in the France Business Income Insurance Market include AXA, Allianz, and Generali, which offer various business income protection products tailored to different industries and business sizes, among others.

What are the main drivers of growth in the France Business Income Insurance Market?

The main drivers of growth in the France Business Income Insurance Market include increasing awareness of risk management, the rise in natural disasters, and the growing number of small and medium-sized enterprises seeking financial protection.

What challenges does the France Business Income Insurance Market face?

Challenges in the France Business Income Insurance Market include the complexity of policy terms, the difficulty in accurately assessing business interruption risks, and the potential for underinsurance among businesses.

What opportunities exist in the France Business Income Insurance Market?

Opportunities in the France Business Income Insurance Market include the development of customized insurance products, the integration of technology for better risk assessment, and the increasing demand for coverage among startups and e-commerce businesses.

What trends are shaping the France Business Income Insurance Market?

Trends shaping the France Business Income Insurance Market include the adoption of digital platforms for policy management, a focus on sustainability in insurance practices, and the growing importance of data analytics in underwriting processes.

Leading Companies in France Business Income Insurance Market:

AXA Group

CNP Assurances

Groupama

Crédit Agricole Assurances

Generali Group

BNP Paribas Cardif

Société Générale Insurance

Allianz France

Covéa Group

AG2R La Mondiale

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.