The fluid end module market serves the oil and gas industry by providing critical components for high-pressure pumping equipment used in drilling and hydraulic fracturing operations. Fluid end modules are integral parts of hydraulic fracturing pumps, responsible for pressurizing and pumping fluids such as water, proppants, and chemicals into oil and gas wells. As such, they play a vital role in enabling efficient and productive well stimulation processes.

Meaning:

Fluid end modules are complex components of hydraulic fracturing pumps, consisting of various parts such as liners, pistons, valves, and seals. These modules endure extreme pressure and abrasion during pumping operations, requiring durable materials and precise engineering to ensure reliability and performance in harsh operating environments. Fluid end modules are essential for delivering high-pressure fluid streams needed for hydraulic fracturing, a key process in the extraction of oil and gas from unconventional reservoirs.

Executive Summary:

The fluid end module market is driven by the demand for hydraulic fracturing services in the oil and gas industry, particularly in shale formations. As drilling activity increases and wells require more intensive fracturing treatments, the demand for high-quality fluid end modules is expected to grow. Manufacturers in this market focus on producing durable, high-performance modules that can withstand the rigors of hydraulic fracturing operations while maximizing pump efficiency and uptime.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Growing Demand for Hydraulic Fracturing: The expansion of hydraulic fracturing operations, especially in shale basins, is driving the demand for fluid end modules. These modules are essential components of high-pressure pumps used in well stimulation activities.

Technological Advancements: Manufacturers are investing in research and development to innovate new materials, designs, and manufacturing processes for fluid end modules. Advanced materials such as ceramic composites and coatings are being utilized to enhance durability and performance.

Focus on Reliability and Durability: End users prioritize reliability and durability when selecting fluid end modules. Modules must withstand high-pressure, high-temperature conditions and resist abrasion and corrosion to ensure prolonged operational life.

Aftermarket Services: Aftermarket services such as maintenance, repair, and replacement parts play a crucial role in the fluid end module market. Manufacturers and service providers offer comprehensive support to ensure optimal performance and uptime of pumping equipment.

Market Drivers:

Increasing Oil and Gas Production: The growing demand for oil and gas, coupled with advancements in extraction technologies, is driving increased drilling activity and hydraulic fracturing operations, driving demand for fluid end modules.

Shale Revolution: The development of shale resources has transformed the oil and gas industry, leading to a surge in hydraulic fracturing activity. Fluid end modules are essential components of fracturing pumps used in shale formations.

Focus on Operational Efficiency: Oil and gas operators prioritize efficiency and productivity in well stimulation operations. High-performance fluid end modules enable pumps to operate at maximum efficiency, reducing downtime and enhancing overall productivity.

Stringent Regulatory Standards: Regulatory standards for well construction and operation necessitate the use of reliable and high-quality equipment. Fluid end modules must comply with industry standards and safety regulations to ensure safe and efficient pumping operations.

Market Restraints:

Cyclical Nature of the Oil and Gas Industry: The fluid end module market is subject to the cyclical nature of the oil and gas industry, with fluctuations in drilling activity and oil prices impacting demand for hydraulic fracturing services and equipment.

Price Volatility: The volatility of oil prices and market uncertainty can affect investment decisions and capital expenditures in the oil and gas sector, leading to fluctuations in demand for fluid end modules.

Environmental Concerns: Environmental regulations and public opposition to hydraulic fracturing can pose challenges for the fluid end module market. Operators must adhere to strict environmental standards, which may impact drilling activity and demand for fracturing services.

Market Opportunities:

Expansion into Emerging Markets: Emerging markets present opportunities for growth in the fluid end module market, as countries seek to develop their oil and gas resources using hydraulic fracturing technologies.

Technological Innovation: Innovation in materials, design, and manufacturing processes offers opportunities for manufacturers to differentiate their products and capture market share. Advanced materials and coatings can improve performance and durability of fluid end modules.

Aftermarket Services: The aftermarket segment represents a significant opportunity for manufacturers to provide value-added services such as maintenance, repair, and spare parts. Establishing strong aftermarket support capabilities can enhance customer loyalty and generate recurring revenue.

Diversification of Product Portfolio: Manufacturers can diversify their product portfolio to offer a range of fluid end modules catering to different pump sizes, pressure ratings, and operating conditions. Customization options and modular designs can meet the diverse needs of oil and gas operators.

Market Dynamics:

The fluid end module market is influenced by various factors including oil and gas prices, drilling activity, technological advancements, regulatory developments, and environmental considerations. Manufacturers must navigate these dynamics to seize opportunities and address challenges effectively.

Regional Analysis:

The fluid end module market exhibits regional variations in terms of demand, production, and regulatory landscape. Key regions for the fluid end module market include:

North America: North America is the largest market for fluid end modules, driven by extensive hydraulic fracturing activity in shale basins such as the Permian Basin, Bakken Formation, and Eagle Ford Shale.

Europe: Europe has a significant market for fluid end modules, particularly in countries with active oil and gas exploration and production activities such as Norway and the United Kingdom.

Asia Pacific: Asia Pacific is an emerging market for fluid end modules, driven by growing energy demand and increasing investment in unconventional oil and gas resources in countries such as China and Australia.

Middle East and Africa: The Middle East and Africa region has opportunities for the fluid end module market, particularly in countries with significant reserves of unconventional hydrocarbons such as Saudi Arabia and Algeria.

Competitive Landscape:

Leading Companies in the Fluid End Module Market:

Gardner Denver Holdings, Inc.

Weir Group PLC

National Oilwell Varco, Inc.

Forum Energy Technologies, Inc.

Schlumberger Limited

TechnipFMC plc

Weatherford International plc

General Electric Company

Flowserve Corporation

Baker Hughes Company

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

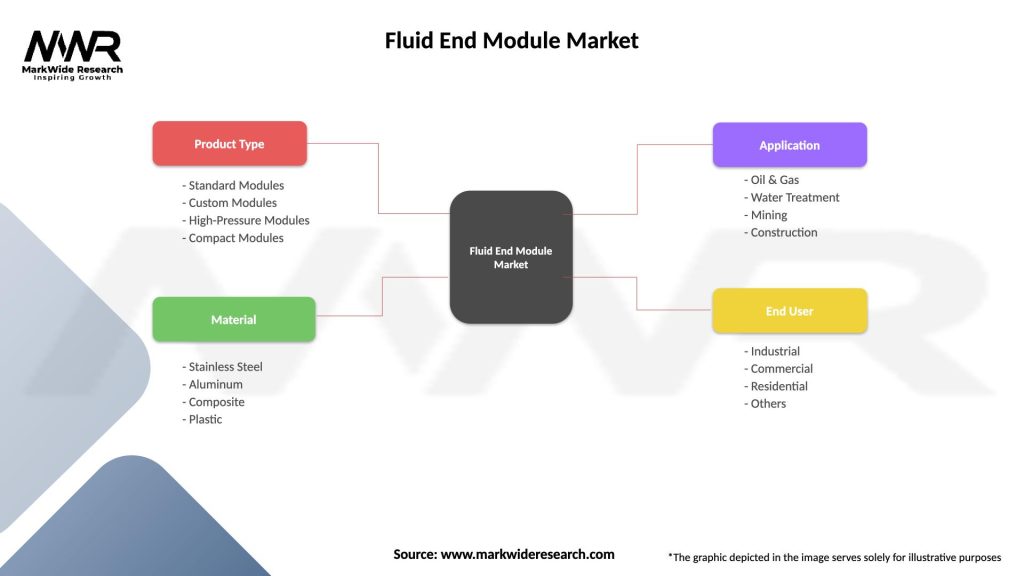

Segmentation:

The fluid end module market can be segmented based on various factors including pump type, pressure rating, material, and application. Segmentation provides insights into market trends, customer preferences, and growth opportunities.

By Pump Type: Triplex pumps, quintuplex pumps, duplex pumps

By Pressure Rating: Low-pressure, high-pressure

By Material: Carbon steel, stainless steel, ceramic

By Application: Onshore, offshore

Category-wise Insights:

Triplex Pumps: Triplex pumps are widely used in hydraulic fracturing operations due to their high-pressure capabilities and reliability. Fluid end modules for triplex pumps are in high demand, particularly in shale basins.

Quintuplex Pumps: Quintuplex pumps are gaining popularity for their efficiency and reduced maintenance requirements. Fluid end modules for quintuplex pumps offer higher flow rates and improved performance.

Duplex Pumps: Duplex pumps are used in less demanding applications where lower pressure ratings are sufficient. Fluid end modules for duplex pumps cater to a niche market segment with specific requirements.

Key Benefits for Industry Participants and Stakeholders:

Enhanced Pump Performance: High-quality fluid end modules contribute to the overall performance and efficiency of hydraulic fracturing pumps, enabling operators to achieve higher flow rates and pressures.

Increased Pump Reliability: Durable and reliable fluid end modules minimize downtime and maintenance costs, ensuring continuous pumping operations and maximizing well productivity.

Improved Safety: Well-designed fluid end modules enhance safety by reducing the risk of equipment failures, leaks, and accidents during pumping operations, protecting personnel and assets.

Cost Savings: Efficient fluid end modules help operators optimize pumping operations, reduce energy consumption, and lower operating costs, resulting in overall cost savings for well stimulation activities.

SWOT Analysis:

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the fluid end module market:

Weaknesses: Dependence on oil and gas industry cycles, price sensitivity, regulatory challenges, competition from alternative technologies.

Opportunities: Expansion into emerging markets, development of advanced materials and coatings, aftermarket service growth, partnerships and collaborations.

Threats: Volatility in oil and gas prices, environmental regulations, geopolitical risks, disruptive technologies.

Understanding these factors helps manufacturers and stakeholders formulate strategies to capitalize on strengths, address weaknesses, seize opportunities, and mitigate threats in the fluid end module market.

Market Key Trends:

Technological Advancements: Continuous innovation in materials, design, and manufacturing processes is driving the development of high-performance fluid end modules with improved durability, efficiency, and reliability.

Digitalization and Connectivity: Integration of digital technologies such as IoT sensors, data analytics, and predictive maintenance enables real-time monitoring, diagnostics, and optimization of fluid end module performance.

Environmental Sustainability: Growing emphasis on environmental sustainability is driving the adoption of eco-friendly materials, energy-efficient designs, and recycling initiatives in fluid end module manufacturing.

Market Consolidation: Consolidation trends in the oilfield services industry are influencing the fluid end module market, with mergers, acquisitions, and strategic alliances reshaping the competitive landscape.

Covid-19 Impact:

The Covid-19 pandemic has had a significant impact on the fluid end module market, leading to disruptions in drilling activity, reduced oil prices, and financial constraints for oil and gas operators. However, the pandemic has also accelerated digital transformation initiatives and automation trends in the industry, driving demand for advanced fluid end modules with remote monitoring and control capabilities.

Key Industry Developments:

Product Innovations: Manufacturers are developing innovative fluid end module designs with improved materials, coatings, and performance features to meet the evolving needs of the oil and gas industry.

Partnerships and Collaborations: Collaborative partnerships between fluid end module manufacturers, oilfield service providers, and technology firms enable knowledge sharing, technology transfer, and joint development of customized solutions.

Aftermarket Services Expansion: Aftermarket services such as maintenance, repair, and spare parts supply are expanding to meet the growing demand for aftermarket support and ensure optimal performance and uptime of fluid end modules.

Global Market Expansion: Key players in the fluid end module market are expanding their geographic presence and production capabilities to cater to growing demand in emerging markets and strengthen their competitive position globally.

Analyst Suggestions:

Focus on Innovation: Manufacturers should prioritize research and development to innovate new materials, designs, and technologies for fluid end modules that enhance performance, reliability, and sustainability.

Customer-Centric Approach: Adopting a customer-centric approach, manufacturers should understand customer needs, preferences, and pain points to tailor product offerings, services, and support solutions that deliver value and enhance customer satisfaction.

Diversification and Differentiation: Manufacturers should diversify their product portfolio and differentiate their offerings through customization, modularity, and value-added features that address specific application requirements and market segments.

Strategic Partnerships: Collaborative partnerships, alliances, and ecosystems with oil and gas operators, equipment suppliers, and technology providers can drive innovation, market expansion, and customer engagement, leveraging complementary strengths and capabilities.

Future Outlook:

The future outlook for the fluid end module market is positive, driven by factors such as increasing drilling activity, technological advancements, digital transformation, and growing demand for energy. Manufacturers that innovate, collaborate, and adapt to market trends and customer needs are well-positioned to capitalize on emerging opportunities, expand market share, and drive growth in the global fluid end module market.

Conclusion:

The fluid end module market plays a crucial role in providing essential components for high-pressure pumping equipment used in hydraulic fracturing operations in the oil and gas industry. As the demand for hydraulic fracturing services continues to grow, driven by increasing energy demand and advancements in extraction technologies, the fluid end module market is poised for steady growth and innovation. Manufacturers that invest in technology, innovation, customer-centric strategies, and collaborative partnerships are well-positioned to succeed in this dynamic and competitive market.

What is Fluid End Module?

A Fluid End Module is a critical component in high-pressure pumping systems, primarily used in oil and gas extraction, water treatment, and industrial applications. It facilitates the efficient transfer of fluids under high pressure, ensuring optimal performance and reliability.

What are the key players in the Fluid End Module Market?

Key players in the Fluid End Module Market include companies such as Baker Hughes, Schlumberger, and Halliburton, which are known for their innovative solutions and extensive product offerings in fluid handling technologies. These companies focus on enhancing the efficiency and durability of fluid end modules, among others.

What are the main drivers of the Fluid End Module Market?

The Fluid End Module Market is driven by the increasing demand for efficient fluid handling in various industries, including oil and gas, mining, and chemical processing. Additionally, advancements in technology and the need for reliable equipment in high-pressure applications contribute to market growth.

What challenges does the Fluid End Module Market face?

Challenges in the Fluid End Module Market include the high costs associated with advanced materials and manufacturing processes, as well as the need for regular maintenance and replacement. Additionally, fluctuating oil prices can impact investment in new fluid handling technologies.

What opportunities exist in the Fluid End Module Market?

Opportunities in the Fluid End Module Market include the growing trend towards automation and digitalization in industrial processes, which can enhance operational efficiency. Furthermore, the increasing focus on sustainable practices and the development of eco-friendly materials present new avenues for growth.

What trends are shaping the Fluid End Module Market?

Current trends in the Fluid End Module Market include the integration of smart technologies for real-time monitoring and predictive maintenance. Additionally, there is a shift towards modular designs that allow for easier upgrades and customization, catering to specific industry needs.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.