The fluid catalytic cracker (FCC) market is experiencing steady growth globally, driven by the increasing demand for refined petroleum products, growing investments in refinery expansion and modernization projects, and rising focus on enhancing fuel efficiency and meeting environmental regulations. Fluid catalytic crackers play a crucial role in the petroleum refining industry by converting heavy hydrocarbon feedstocks into valuable gasoline, diesel, and petrochemical products.

Meaning

Fluid catalytic cracking (FCC) is a key refining process used in petroleum refineries to convert high-boiling, low-value hydrocarbon fractions into lighter, more valuable products such as gasoline, diesel, and propylene. The process involves the use of a fluidized bed reactor and a catalyst to break down large hydrocarbon molecules into smaller, more desirable molecules through cracking reactions, enabling the production of higher yields of valuable fuels and chemicals.

Executive Summary

The fluid catalytic cracker market is witnessing steady growth, driven by the increasing demand for transportation fuels, petrochemical feedstocks, and cleaner-burning fuels. Key market players are focusing on technology advancements, capacity expansions, and strategic partnerships to capitalize on emerging opportunities and address evolving customer needs in the global refining industry.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Demand for Transportation Fuels: The increasing consumption of gasoline, diesel, and aviation fuels, driven by population growth, urbanization, and economic development, is driving the demand for fluid catalytic cracking units to produce high-quality fuels with improved performance and environmental attributes.

Petrochemical Feedstock Demand: Fluid catalytic crackers play a critical role in the production of propylene, a key feedstock for the petrochemical industry, to meet growing demand for plastics, chemicals, and synthetic materials in various end-use sectors such as packaging, construction, and automotive.

Regulatory Compliance and Environmental Concerns: Refiners are investing in FCC technologies and catalyst formulations to meet stringent environmental regulations, reduce emissions of sulfur oxides (SOx), nitrogen oxides (NOx), and volatile organic compounds (VOCs), and improve the environmental performance of refining operations.

Market Drivers

Increasing Refining Capacity Expansion Projects: The ongoing investments in refinery expansion and modernization projects, particularly in emerging markets such as Asia Pacific and the Middle East, are driving the demand for fluid catalytic cracking units to upgrade heavy crude oils and produce higher-value refined products for domestic and export markets.

Focus on Fuel Quality and Performance: Refiners are adopting advanced FCC technologies and catalyst formulations to improve the octane rating, cetane number, and distillation properties of gasoline and diesel fuels, meeting regulatory specifications, enhancing engine performance, and reducing emissions in vehicles and aircraft.

Shifting Demand for Petrochemicals: The growing demand for petrochemical feedstocks such as propylene, butylene, and aromatics, driven by the expansion of downstream industries such as plastics, resins, and fibers, is driving the need for fluid catalytic cracking units to optimize yields and compositions of valuable chemical intermediates.

Market Restraints

Capital Intensive Nature of FCC Projects: The high capital costs associated with the design, construction, and commissioning of fluid catalytic cracking units may pose a barrier to entry for some refiners, especially small and independent operators with limited financial resources or access to project financing.

Technological Complexity and Operational Risks: Fluid catalytic cracking is a complex and highly engineered process involving sophisticated equipment, catalyst management systems, and operating parameters, which may present operational challenges, safety risks, and reliability concerns for refiners.

Competition from Alternative Conversion Processes: Refiners have alternative conversion processes such as hydrocracking, coking, and hydrotreating, which compete with fluid catalytic cracking for feedstock flexibility, product yields, and operational flexibility, especially in regions with stringent environmental regulations or low-value crude oils.

Market Opportunities

Retrofit and Revamp Projects: The retrofit and revamp of existing fluid catalytic cracking units with advanced technologies, catalyst formulations, and process enhancements offer opportunities for refiners to improve unit performance, increase throughput, and expand product slate without significant capital investment.

Integration with Downstream Operations: Integrating fluid catalytic cracking units with downstream refining and petrochemical complexes enables refiners to maximize value creation, optimize product distribution, and capture synergies between FCC products and downstream processing units such as alkylation, aromatics, and olefins production.

Collaboration with Technology Providers: Collaborating with technology licensors, engineering firms, and catalyst suppliers enables refiners to access state-of-the-art FCC technologies, proprietary catalyst formulations, and technical expertise to optimize unit performance, troubleshoot operational challenges, and achieve operational excellence.

Market Dynamics

The fluid catalytic cracker market is influenced by various dynamics, including crude oil prices, refining margins, regulatory policies, technological advancements, and market competition. Refiners need to adapt to these dynamics, optimize their refining strategies, and invest in technology upgrades to remain competitive and profitable in the evolving market landscape.

Regional Analysis

The fluid catalytic cracker market is segmented into regions such as North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Asia Pacific dominates the market, driven by rapid industrialization, urbanization, and growing demand for transportation fuels and petrochemicals in countries such as China, India, and Southeast Asia. However, North America and the Middle East are significant markets, supported by abundant crude oil resources, advanced refining infrastructure, and strategic access to global markets.

Competitive Landscape

Leading Companies in the Fluid Catalytic Cracker Market:

Exxon Mobil Corporation

Royal Dutch Shell plc

Chevron Corporation

BASF SE

Honeywell UOP

Albemarle Corporation

DuPont de Nemours, Inc.

W. R. Grace & Co.

Axens

TechnipFMC plc

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

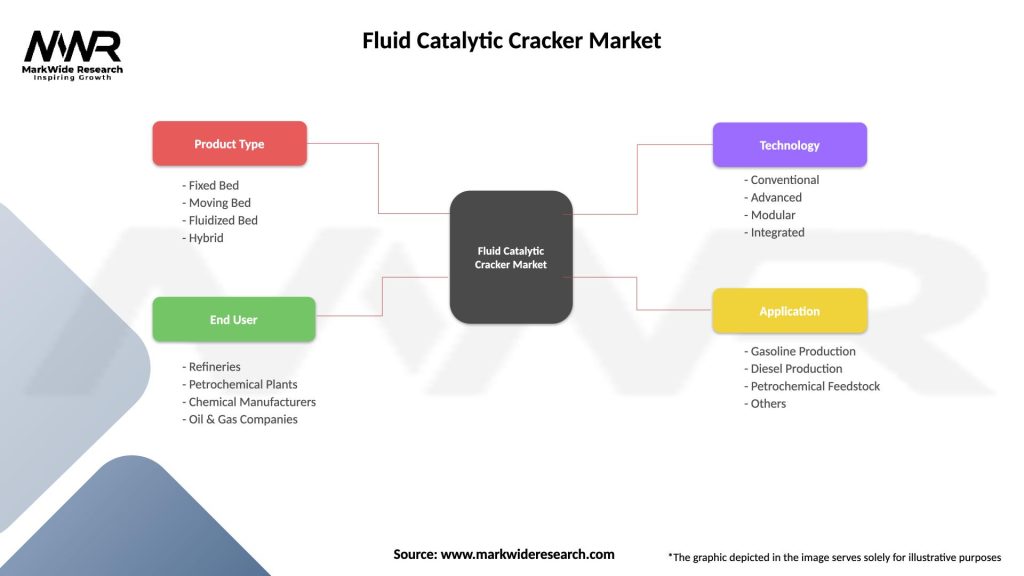

The fluid catalytic cracker market is segmented based on technology type, catalyst type, application, end-user industry, and geography. Technology types include conventional FCC, advanced FCC, and residue fluid catalytic cracking (RFCC), while catalyst types encompass zeolite-based, metal-based, and mixed-metal oxide catalyst formulations.

Category-wise Insights

Conventional FCC Technology: Conventional fluid catalytic cracking technology is the most widely used FCC process in the refining industry, characterized by its versatility, reliability, and proven performance in converting heavy feedstocks into high-value products such as gasoline and diesel fuels.

Advanced FCC Technology: Advanced fluid catalytic cracking technologies incorporate process enhancements, reactor design improvements, and catalyst innovations to achieve higher conversion rates, selectivity, and flexibility in processing diverse feedstocks and optimizing product yields.

Residue Fluid Catalytic Cracking (RFCC): Residue fluid catalytic cracking units are specialized FCC units designed to process heavier, more challenging feedstocks such as vacuum residues, atmospheric bottoms, and heavy crude oils, producing lighter products and reducing residue disposal costs.

Key Benefits for Industry Participants and Stakeholders

Increased Refining Flexibility: Fluid catalytic cracking units enable refiners to process a wide range of feedstocks, including light and heavy crude oils, vacuum gas oils, and bitumens, providing flexibility to adjust operations based on market conditions, crude availability, and product demand.

Enhanced Product Yields and Quality: FCC technologies and catalyst formulations improve product selectivity, yield distributions, and product quality parameters such as octane number, cetane index, and sulfur content, enhancing the value of refined products and meeting customer specifications.

Compliance with Environmental Regulations: Advanced FCC technologies and catalysts help refiners comply with stringent environmental regulations by reducing emissions of sulfur oxides (SOx), nitrogen oxides (NOx), particulate matter (PM), and volatile organic compounds (VOCs), minimizing environmental impact and ensuring regulatory compliance.

SWOT Analysis

Strengths: Versatility, flexibility, and efficiency in converting heavy feedstocks into valuable products, proven track record in refining operations.

Weaknesses: Capital-intensive nature, operational complexity, and environmental compliance challenges.

Opportunities: Retrofit and revamp projects, integration with downstream operations, collaboration with technology providers.

Threats: Volatility in crude oil prices, regulatory uncertainties, competition from alternative conversion processes.

Market Key Trends

Digitalization and Process Optimization: Refiners are adopting digital technologies, data analytics, and artificial intelligence (AI) tools to optimize fluid catalytic cracking operations, improve process efficiency, and reduce energy consumption, operating costs, and emissions.

Sustainability and Carbon Management: There is a growing focus on sustainability and carbon management in the refining industry, driving the development of low-carbon and carbon-neutral FCC technologies, catalysts, and processes to mitigate greenhouse gas emissions and address climate change concerns.

Circular Economy and Waste Valorization: Refiners are exploring opportunities to convert refinery by-products, waste streams, and co-products into value-added products such as biofuels, biochemicals, and renewable fuels using fluid catalytic cracking technologies and biorefining processes, promoting resource efficiency and waste valorization.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the fluid catalytic cracker market, leading to fluctuations in crude oil prices, changes in product demand patterns, and disruptions in refining operations. While the pandemic has temporarily reduced fuel consumption and refining margins, it has also accelerated digital transformation initiatives, innovation efforts, and sustainability initiatives in the refining industry, driving long-term resilience and competitiveness.

Key Industry Developments

Launch of Next-Generation FCC Technologies: Key market players have introduced next-generation fluid catalytic cracking technologies with enhanced catalyst formulations, reactor designs, and process control strategies to improve conversion efficiency, product selectivity, and reliability in refining operations.

Adoption of Renewable Feedstocks: Refiners are exploring the use of renewable feedstocks such as bio-oils, vegetable oils, and waste fats for fluid catalytic cracking applications to produce renewable fuels, bio-based chemicals, and sustainable products, aligning with decarbonization goals and circular economy principles.

Collaboration for Innovation and Sustainability: Industry stakeholders are collaborating with research institutions, government agencies, and technology providers to develop innovative FCC solutions, advance sustainability initiatives, and address emerging challenges such as carbon management, energy efficiency, and environmental stewardship.

Analyst Suggestions

Invest in Technology Upgrades: Refiners should invest in technology upgrades, catalyst replacements, and process optimizations to improve the performance, reliability, and sustainability of fluid catalytic cracking units, reducing emissions, minimizing operating costs, and enhancing competitiveness.

Diversify Product Slate: Diversifying product slate by optimizing FCC operations, adjusting product yields, and exploring co-processing opportunities enables refiners to adapt to changing market dynamics, capture value from different product streams, and maximize profitability in the refining industry.

Collaborate for Innovation and Sustainability: Collaboration with technology providers, research institutions, and industry partners fosters innovation, accelerates technology development, and promotes sustainability initiatives in the refining industry, driving long-term growth, and resilience in the global market.

Future Outlook

The fluid catalytic cracker market is expected to grow steadily in the coming years, driven by increasing demand for transportation fuels, petrochemical feedstocks, and cleaner-burning fuels worldwide. Key market players are focusing on technology advancements, sustainability initiatives, and collaboration efforts to address evolving market trends, regulatory requirements, and customer needs, ensuring continued growth and competitiveness in the global refining industry.

Conclusion

In conclusion, the fluid catalytic cracker market plays a vital role in the petroleum refining industry by converting heavy hydrocarbon feedstocks into valuable fuels and chemicals. By adopting advanced FCC technologies, catalyst formulations, and process optimizations, refiners can improve conversion efficiency, product yields, and environmental performance, enhancing their competitiveness and sustainability in the global market. Market players need to invest in technology upgrades, diversify product slate, and collaborate for innovation and sustainability to capitalize on emerging opportunities and achieve long-term growth in the fluid catalytic cracker market.

What is Fluid Catalytic Cracker?

Fluid Catalytic Cracker (FCC) is a crucial technology in petroleum refining that converts heavy fractions of crude oil into lighter, more valuable products such as gasoline and diesel. It utilizes a catalyst to facilitate the cracking process, enhancing efficiency and yield.

What are the key players in the Fluid Catalytic Cracker Market?

Key players in the Fluid Catalytic Cracker Market include companies like Honeywell UOP, Axens, and Technip Energies, which provide advanced FCC technologies and catalysts. These companies are known for their innovative solutions and extensive experience in refining processes, among others.

What are the growth factors driving the Fluid Catalytic Cracker Market?

The Fluid Catalytic Cracker Market is driven by the increasing demand for cleaner fuels and the need for efficient refining processes. Additionally, the rise in global energy consumption and the shift towards more sustainable refining technologies are significant growth factors.

What challenges does the Fluid Catalytic Cracker Market face?

The Fluid Catalytic Cracker Market faces challenges such as the high operational costs associated with advanced FCC units and the need for continuous technological upgrades. Environmental regulations and the pressure to reduce emissions also pose significant challenges for refiners.

What opportunities exist in the Fluid Catalytic Cracker Market?

Opportunities in the Fluid Catalytic Cracker Market include the development of new catalysts that enhance efficiency and reduce environmental impact. Additionally, the growing trend of petrochemical integration in refineries presents avenues for innovation and expansion.

What trends are shaping the Fluid Catalytic Cracker Market?

Trends in the Fluid Catalytic Cracker Market include the adoption of digital technologies for process optimization and the increasing focus on sustainability. Moreover, advancements in catalyst technology are leading to improved performance and lower emissions in FCC operations.

Leading Companies in the Fluid Catalytic Cracker Market:

Exxon Mobil Corporation

Royal Dutch Shell plc

Chevron Corporation

BASF SE

Honeywell UOP

Albemarle Corporation

DuPont de Nemours, Inc.

W. R. Grace & Co.

Axens

TechnipFMC plc

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.