The Fuel Cell Electric Vehicles (FCEVs) market represents a transformative shift towards sustainable transportation, leveraging hydrogen fuel cell technology to power electric motors. FCEVs are gaining prominence as zero-emission vehicles (ZEVs), offering longer driving ranges and shorter refueling times compared to battery electric vehicles (BEVs).

Meaning

Fuel Cell Electric Vehicles (FCEVs) utilize hydrogen as a primary fuel source, which undergoes electrochemical reactions in fuel cells to generate electricity for powering electric motors. These vehicles emit only water vapor and heat as byproducts, contributing significantly to reducing greenhouse gas emissions and air pollutants.

Executive Summary

The global FCEVs market is experiencing accelerated growth driven by increasing environmental regulations, advancements in hydrogen infrastructure, and automaker investments in clean energy technologies. Key market players are focused on expanding hydrogen refueling networks, enhancing vehicle performance, and lowering production costs to drive market adoption.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Technological Advancements: Evolution from proton exchange membrane (PEM) to solid oxide fuel cells (SOFCs), improvements in fuel cell efficiency, and development of lightweight hydrogen storage tanks.

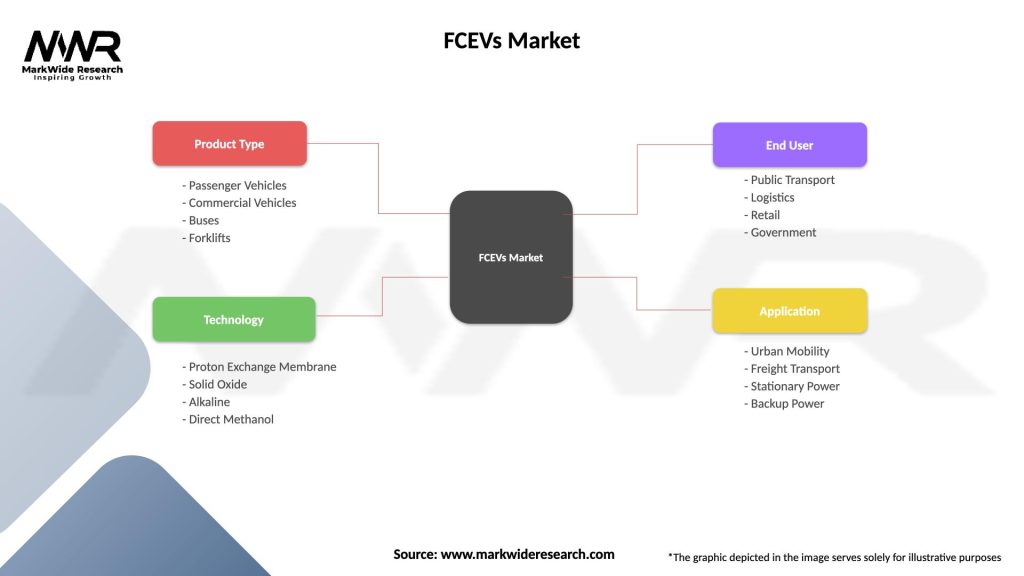

Market Segmentation: Segmented by vehicle type (passenger cars, buses, trucks), fuel cell type (PEMFC, AFC, SOFC), and region (North America, Europe, Asia-Pacific).

Regulatory Landscape: Government incentives, emissions standards (California ZEV mandate, European Green Deal), and hydrogen infrastructure investments influencing market growth.

Market Drivers

Environmental Regulations: Stringent emission norms and targets driving automakers towards zero-emission vehicle solutions like FCEVs.

Hydrogen Infrastructure Expansion: Investment in hydrogen refueling stations and infrastructure development supporting FCEV adoption.

Longer Driving Range: Comparable range and refueling times to internal combustion engine vehicles, enhancing consumer acceptance and convenience.

Reduced Total Cost of Ownership (TCO): Lower fuel costs and maintenance expenses compared to traditional vehicles, improving economic feasibility.

Technology Advancements: Innovations in fuel cell durability, efficiency, and cost reduction enhancing vehicle performance and reliability.

Market Restraints

Infrastructure Development: Limited hydrogen refueling infrastructure outside of key markets, impacting consumer adoption and market expansion.

Production Costs: High initial costs associated with fuel cell stack manufacturing and hydrogen storage technologies affecting vehicle affordability.

Hydrogen Supply Chain: Challenges in hydrogen production, storage, and distribution impacting fuel availability and cost competitiveness.

Consumer Awareness and Education: Limited awareness about FCEV benefits, refueling processes, and hydrogen safety standards hindering market penetration.

Competitive Technologies: Growing competition from battery electric vehicles (BEVs) with expanding charging networks and declining battery costs posing a challenge to FCEV market growth.

Market Opportunities

Hydrogen Infrastructure Investment: Expansion of hydrogen refueling networks in key regions, including Europe, Japan, California, and China.

Fleet and Commercial Applications: Growth opportunities in fleet operations (buses, trucks) and commercial vehicles requiring longer driving ranges and rapid refueling.

Government Incentives: Subsidies, tax credits, and grants supporting FCEV adoption, hydrogen infrastructure development, and R&D investments.

Technology Collaboration: Partnerships between automakers, fuel cell manufacturers, and energy companies for joint research, pilot projects, and infrastructure deployment.

Hydrogen Production Innovation: Advancements in renewable hydrogen production (electrolysis, biomass conversion) enhancing fuel sustainability and cost-effectiveness.

Market Dynamics

The FCEVs market dynamics are shaped by regulatory policies, infrastructure investments, technological advancements, consumer preferences for sustainable mobility solutions, and strategic collaborations across the automotive and energy sectors.

Regional Analysis

North America: Leadership in hydrogen infrastructure development (California, Northeastern U.S.), ZEV mandates, and government incentives driving FCEV market growth.

Europe: European Green Deal initiatives, CO2 reduction targets, and expansion of hydrogen refueling networks supporting FCEV adoption across passenger and commercial vehicle segments.

Asia-Pacific: Investment in hydrogen infrastructure (Japan, South Korea), government policies promoting clean energy vehicles, and growth in automotive production driving regional market expansion.

Rest of the World: Emerging markets in Latin America, Middle East, and Africa focusing on hydrogen infrastructure development, regulatory frameworks, and pilot projects promoting FCEV adoption.

Competitive Landscape

Leading Companies in FCEVs Market

Toyota Motor Corporation

Honda Motor Co., Ltd.

Hyundai Motor Company

Mercedes-Benz

BMW AG

Ford Motor Company

General Motors

Nissan Motor Corporation

Ballard Power Systems

Plug Power Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Application: OEM installations, fleet operations, commercial vehicles, and government initiatives.

Category-wise Insights

Passenger Vehicles: Adoption of FCEVs in consumer markets, government incentives, and expansion of hydrogen refueling networks supporting market growth.

Commercial Vehicles: Use of FCEVs in fleets, delivery trucks, and public transportation requiring longer driving ranges, rapid refueling, and environmental compliance.

Infrastructure Development: Role of hydrogen refueling stations, regulatory policies, and public-private partnerships in expanding market accessibility and consumer acceptance.

Key Benefits for Industry Participants and Stakeholders

Environmental Sustainability: Contribution to reducing greenhouse gas emissions, improving air quality, and achieving carbon neutrality goals.

Energy Security: Diversification of energy sources, reducing dependency on fossil fuels, and leveraging renewable hydrogen production technologies.

Technological Innovation: Advancements in fuel cell efficiency, durability, and hydrogen storage enhancing vehicle performance and reliability.

Economic Growth: Job creation in the hydrogen economy, development of new supply chains, and growth opportunities in clean energy industries.

Market Leadership: Competitive advantage in sustainable mobility solutions, brand differentiation, and market positioning as industry leaders in fuel cell technology.

SWOT Analysis

Strengths:

Technological leadership in hydrogen fuel cell development, vehicle integration, and infrastructure deployment.

Strategic partnerships with energy companies, government agencies, and automotive OEMs for market expansion and technology deployment.

Consumer demand for zero-emission vehicles (ZEVs), regulatory support, and incentives driving market adoption.

Weaknesses:

High initial costs associated with fuel cell stack manufacturing, hydrogen infrastructure development, and consumer affordability.

Limited hydrogen refueling infrastructure outside of key markets impacting consumer accessibility and market expansion.

Competition from battery electric vehicles (BEVs) with expanding charging networks and declining battery costs posing a challenge to FCEV market growth.

Opportunities:

Expansion of hydrogen refueling networks, government incentives, and policy support promoting FCEV adoption.

Growth in fleet and commercial applications requiring longer driving ranges, rapid refueling, and environmental compliance.

Technological advancements in fuel cell efficiency, hydrogen production, and renewable energy integration supporting market competitiveness.

Threats:

Infrastructure development challenges, including hydrogen production, storage, distribution, and regulatory uncertainties impacting market growth.

Competitive pressures from BEVs with advancing battery technologies, charging infrastructure expansion, and consumer preferences for electric vehicles.

Economic factors, supply chain disruptions, and geopolitical issues affecting hydrogen availability, pricing, and market scalability.

Market Key Trends

Hydrogen Infrastructure Expansion: Growth in hydrogen refueling stations, investments in production facilities, and infrastructure deployment supporting FCEV market accessibility.

Technology Advancements: Development of next-generation fuel cell stacks, hydrogen storage solutions, and vehicle integration enhancing performance and reliability.

Policy and Regulatory Support: Government incentives, ZEV mandates, emissions standards, and carbon reduction targets driving FCEV adoption and market expansion.

Consumer Awareness: Education initiatives, public acceptance, and experience with FCEV technology contributing to market growth and consumer preference.

Global Collaboration: International partnerships, research alliances, and industry consortia advancing hydrogen economy initiatives, fuel cell innovation, and market scalability.

Covid-19 Impact

The Covid-19 pandemic has influenced the FCEVs market through:

Supply Chain Disruptions: Disruptions in global supply chains, component shortages, and manufacturing delays impacting production schedules and vehicle deliveries.

Economic Uncertainty: Fluctuations in consumer demand, purchasing behavior, and financial constraints affecting automotive sales and market growth.

Policy Adjustments: Government stimulus packages, recovery plans, and incentives supporting clean energy investments, infrastructure projects, and industry resilience.

Technological Resilience: Continued R&D investments, innovation in digital platforms, virtual sales channels, and remote operations adapting to pandemic challenges.

Environmental Awareness: Emphasis on sustainability, climate action, and resilience strategies driving long-term investments in renewable energy and zero-emission vehicles.

Key Industry Developments

Recent developments in the FCEVs market include:

Hyundai NEXO Expansion: Hyundai Motor Company expanding NEXO fuel cell vehicle availability, hydrogen refueling infrastructure partnerships, and market penetration.

Toyota Mirai Series: Toyota Motor Corporation launching next-generation Mirai models, advancing hydrogen fuel cell technology, and global market expansion initiatives.

Government Initiatives: European Green Deal, California ZEV mandates, and national hydrogen strategies supporting FCEV deployment, infrastructure investments, and market growth.

Technology Collaboration: Ballard Power Systems, Plug Power, and fuel cell manufacturers collaborating on fuel cell stack development, durability improvements, and cost reduction initiatives.

Infrastructure Investments: Expansion of hydrogen refueling networks in Japan, Germany, California, and South Korea supporting FCEV adoption, consumer accessibility, and market expansion.

Analyst Suggestions

Industry analysts recommend:

Strategic Partnerships: Collaboration between automakers, fuel cell manufacturers, energy companies, and government agencies for infrastructure development, market expansion, and technology deployment.

Investment in R&D: Focus on fuel cell efficiency, durability, cost reduction, and hydrogen production technologies to enhance vehicle performance, reliability, and market competitiveness.

Consumer Education: Awareness campaigns, experience centers, and digital platforms promoting FCEV benefits, hydrogen refueling processes, safety standards, and environmental sustainability.

Regulatory Engagement: Advocacy for supportive policies, incentives, ZEV mandates, emissions standards, and regulatory frameworks promoting FCEV adoption, infrastructure investments, and market growth.

Market Expansion Strategies: Expansion into fleet and commercial applications, development of hydrogen supply chains, and international market entry strategies leveraging regional partnerships and market demand.

Future Outlook

The future outlook for the Fuel Cell Electric Vehicles (FCEVs) market is optimistic, driven by:

Advancements in Hydrogen Technologies: Development of next-generation fuel cell stacks, hydrogen storage solutions, and infrastructure advancements enhancing vehicle performance and market competitiveness.

Infrastructure Expansion: Growth in hydrogen refueling networks, government investments, and policy support promoting FCEV adoption across passenger, commercial, and public transportation sectors.

Market Penetration: Increasing consumer acceptance, regulatory incentives, and technological innovation supporting global market expansion, industry resilience, and sustainable mobility solutions.

Global Collaboration: International partnerships, research alliances, and industry consortia advancing hydrogen economy initiatives, fuel cell innovation, and market scalability.

Climate Action: Emphasis on carbon neutrality, environmental sustainability, and zero-emission transportation strategies driving long-term investments in clean energy and FCEV technologies.

Conclusion

In conclusion, the Fuel Cell Electric Vehicles (FCEVs) market is poised for significant growth, driven by technological advancements, infrastructure expansion, regulatory incentives, and consumer demand for sustainable mobility solutions. Stakeholders are urged to focus on innovation, strategic partnerships, regulatory engagement, and market expansion strategies to capitalize on emerging opportunities and navigate the evolving landscape of clean transportation.

What is FCEVs?

FCEVs, or Fuel Cell Electric Vehicles, are vehicles that use hydrogen fuel cells to power electric motors. They are known for their zero-emission capabilities and are considered a sustainable alternative to traditional gasoline-powered vehicles.

What are the key players in the FCEVs Market?

Key players in the FCEVs Market include Toyota, Honda, Hyundai, and Nikola Corporation. These companies are actively involved in the development and production of fuel cell technologies and vehicles, among others.

What are the main drivers of growth in the FCEVs Market?

The main drivers of growth in the FCEVs Market include increasing environmental regulations, advancements in hydrogen production technologies, and growing consumer demand for sustainable transportation solutions. Additionally, government incentives for clean energy vehicles are also contributing to market expansion.

What challenges does the FCEVs Market face?

The FCEVs Market faces challenges such as the high cost of fuel cell technology, limited hydrogen refueling infrastructure, and competition from battery electric vehicles. These factors can hinder widespread adoption and market growth.

What opportunities exist in the FCEVs Market?

Opportunities in the FCEVs Market include the potential for partnerships in hydrogen infrastructure development, advancements in fuel cell efficiency, and the expansion of FCEVs into commercial sectors like public transportation and logistics. These developments can enhance the market’s growth prospects.

What trends are shaping the FCEVs Market?

Trends shaping the FCEVs Market include increasing investments in hydrogen fuel technology, collaborations between automotive manufacturers and energy companies, and a growing focus on sustainability in transportation. These trends are driving innovation and adoption in the sector.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.