444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The European industrial battery market represents a dynamic and rapidly evolving sector that serves as the backbone of modern industrial operations across the continent. This comprehensive market encompasses a diverse range of battery technologies designed to power industrial equipment, provide backup power solutions, and support critical infrastructure operations. European manufacturers and end-users are increasingly recognizing the strategic importance of reliable, efficient, and sustainable battery solutions in maintaining operational continuity and achieving environmental objectives.

Market dynamics in Europe are characterized by stringent environmental regulations, aggressive decarbonization targets, and a strong emphasis on technological innovation. The region’s industrial battery landscape spans multiple sectors including manufacturing, logistics, telecommunications, healthcare, and renewable energy storage. Growth projections indicate the market is expanding at a robust 8.2% CAGR, driven by increasing demand for uninterrupted power supply systems and the transition toward cleaner energy solutions.

Technological advancement remains a key differentiator in the European market, with lithium-ion technologies gaining significant traction alongside traditional lead-acid solutions. The market benefits from Europe’s strong industrial base, advanced manufacturing capabilities, and supportive regulatory framework that encourages adoption of innovative battery technologies. Regional leadership in sustainability initiatives has positioned Europe as a global benchmark for industrial battery innovation and deployment.

The European industrial battery market refers to the comprehensive ecosystem of battery technologies, systems, and services designed specifically for industrial applications across European countries. This market encompasses the manufacturing, distribution, installation, and maintenance of battery solutions that power industrial equipment, provide backup power for critical systems, and support energy storage requirements in commercial and industrial facilities.

Industrial batteries in this context include various technologies such as lead-acid, lithium-ion, nickel-based, and emerging battery chemistries that are engineered to meet the demanding requirements of industrial environments. These systems must deliver reliable performance under challenging conditions including temperature extremes, vibration, and continuous operation cycles. Market participants include battery manufacturers, system integrators, distributors, and end-users across diverse industrial sectors.

Scope definition extends beyond traditional backup power applications to include energy storage systems for renewable integration, electric vehicle charging infrastructure, and advanced manufacturing processes. The European market is distinguished by its focus on sustainability, circular economy principles, and compliance with stringent environmental and safety regulations that govern industrial battery deployment and lifecycle management.

Market leadership in the European industrial battery sector is characterized by strong technological innovation, regulatory support, and increasing demand for sustainable energy solutions. The market demonstrates remarkable resilience and growth potential, with lithium-ion technologies capturing approximately 42% market share and showing accelerated adoption across multiple industrial applications. Key drivers include digital transformation initiatives, Industry 4.0 implementation, and the urgent need for reliable backup power systems in critical infrastructure.

Competitive dynamics reveal a market structure dominated by both established European manufacturers and emerging technology providers. The sector benefits from substantial investments in research and development, with innovation spending representing nearly 12% of total market revenue. Regional variations show Germany, France, and the United Kingdom leading in market adoption, while Nordic countries demonstrate exceptional growth in renewable energy storage applications.

Future trajectory indicates continued expansion driven by electrification trends, grid modernization projects, and increasing focus on energy security. The market is expected to benefit from European Union initiatives promoting battery manufacturing capabilities and reducing dependence on non-European suppliers. Sustainability considerations are reshaping product development priorities, with circular economy principles influencing design, manufacturing, and end-of-life management strategies.

Strategic insights reveal several critical factors shaping the European industrial battery market landscape:

Market maturity varies significantly across different industrial segments, with telecommunications and data centers showing high adoption rates while emerging sectors like electric vehicle charging infrastructure present substantial growth opportunities. Innovation cycles are accelerating, with new battery chemistries and system architectures entering commercial deployment at an unprecedented pace.

Primary growth drivers propelling the European industrial battery market include the accelerating digital transformation of industrial operations and the critical need for uninterrupted power supply systems. Industry 4.0 initiatives across European manufacturing facilities require reliable backup power solutions to protect sensitive equipment and maintain continuous production processes. The increasing complexity of industrial automation systems has elevated the importance of high-quality battery solutions that can provide seamless power transition during grid disruptions.

Environmental regulations and sustainability mandates are creating substantial demand for cleaner, more efficient battery technologies. European companies are under increasing pressure to reduce their carbon footprint and adopt sustainable practices throughout their operations. Energy efficiency requirements are driving adoption of advanced battery systems that offer superior performance characteristics and longer operational lifespans, contributing to overall sustainability objectives.

Grid modernization and renewable energy integration initiatives across Europe are generating significant demand for industrial-scale energy storage solutions. The intermittent nature of renewable energy sources requires sophisticated battery systems to ensure grid stability and reliable power supply. Infrastructure investments in smart grid technologies and distributed energy resources are creating new market opportunities for advanced battery solutions that can support bidirectional power flow and grid services.

Economic factors including energy cost volatility and the need for operational resilience are motivating industrial facilities to invest in comprehensive battery backup systems. The growing recognition of the economic impact of power disruptions has elevated battery systems from optional equipment to essential infrastructure components in modern industrial operations.

Capital investment requirements represent a significant barrier to market expansion, particularly for small and medium-sized enterprises that may struggle to justify the upfront costs of advanced battery systems. Implementation complexity associated with integrating new battery technologies into existing industrial infrastructure can create substantial technical and logistical challenges that delay adoption decisions.

Technical limitations of current battery technologies, including energy density constraints, temperature sensitivity, and degradation over time, continue to limit applications in certain industrial environments. Safety concerns related to battery thermal runaway, toxic gas emissions, and fire risks require comprehensive safety protocols and specialized handling procedures that increase operational complexity and costs.

Supply chain vulnerabilities have become increasingly apparent, with critical battery materials and components subject to price volatility and availability constraints. The concentration of battery manufacturing in specific geographic regions creates potential supply disruptions that can impact project timelines and cost predictability. Skilled workforce shortages in battery system design, installation, and maintenance limit the industry’s ability to scale operations effectively.

Regulatory uncertainty surrounding emerging battery technologies and evolving safety standards can create hesitation among potential adopters who prefer to wait for clearer regulatory guidance. Disposal and recycling challenges associated with end-of-life battery management add complexity and cost to the total ownership equation, particularly as environmental regulations become more stringent.

Emerging applications in electric vehicle charging infrastructure present substantial growth opportunities as European countries accelerate their transition to electric mobility. The deployment of fast-charging networks requires sophisticated battery systems to manage peak demand and provide grid stabilization services. Commercial opportunities extend to battery-as-a-service models that reduce upfront capital requirements while providing ongoing performance optimization and maintenance services.

Technological advancement in solid-state batteries, advanced lithium chemistries, and alternative battery technologies creates opportunities for early adopters to gain competitive advantages through superior performance characteristics. Integration possibilities with renewable energy systems, particularly solar and wind installations, offer compelling value propositions for industrial facilities seeking to reduce energy costs and environmental impact.

Market expansion opportunities exist in underserved industrial segments and geographic regions where battery adoption remains limited. Eastern European markets show particular promise as industrial modernization accelerates and infrastructure investments increase. The growing focus on energy security and supply chain resilience creates opportunities for European battery manufacturers to capture market share from international competitors.

Service sector growth in battery monitoring, predictive maintenance, and performance optimization represents a significant opportunity for technology providers to develop recurring revenue streams. Circular economy initiatives create new business models around battery refurbishment, second-life applications, and comprehensive recycling services that can generate additional value from battery investments.

Competitive intensity in the European industrial battery market is increasing as traditional manufacturers face competition from innovative technology providers and new market entrants. Market consolidation trends are evident as larger companies acquire specialized battery technology firms to expand their capabilities and market reach. The dynamic nature of battery technology development requires continuous investment in research and development to maintain competitive positioning.

Customer expectations are evolving rapidly, with industrial users demanding higher performance, longer lifespans, and more sophisticated monitoring capabilities from their battery systems. Service requirements are becoming more complex as customers seek comprehensive solutions that include installation, commissioning, monitoring, and maintenance services. The shift toward outcome-based contracting models is changing how battery providers structure their offerings and pricing strategies.

Technology convergence is creating new market dynamics as battery systems become integrated with broader energy management platforms, IoT networks, and artificial intelligence systems. Interoperability requirements are driving standardization efforts while creating opportunities for companies that can provide seamless integration capabilities across diverse industrial environments.

Regulatory evolution continues to shape market dynamics as European authorities develop new standards for battery performance, safety, and environmental impact. Market timing has become increasingly critical as early adoption of emerging technologies can provide significant competitive advantages, while premature investments in unproven solutions carry substantial risks.

Comprehensive analysis of the European industrial battery market employs a multi-faceted research approach combining primary and secondary data sources to ensure accuracy and reliability. Primary research includes extensive interviews with industry executives, technology developers, end-users, and regulatory officials across major European markets. These interviews provide insights into market trends, competitive dynamics, and future development priorities that cannot be captured through secondary sources alone.

Secondary research encompasses analysis of industry reports, company financial statements, patent filings, regulatory documents, and trade association publications. Market sizing methodologies utilize multiple approaches including top-down analysis based on industrial electricity consumption patterns and bottom-up calculations based on equipment installation data and replacement cycles.

Data validation processes include cross-referencing multiple sources, conducting expert reviews, and applying statistical analysis techniques to ensure consistency and accuracy. Regional analysis incorporates country-specific factors including regulatory environments, industrial structure, and economic conditions that influence market development patterns.

Forecasting models integrate historical market data with forward-looking indicators including planned infrastructure investments, regulatory timelines, and technology development roadmaps. Scenario analysis considers multiple potential market development paths based on different assumptions about key variables including technology adoption rates, regulatory changes, and economic conditions.

Germany dominates the European industrial battery market with approximately 28% market share, driven by its strong manufacturing base, advanced automotive industry, and leadership in renewable energy adoption. German industrial facilities demonstrate high adoption rates of sophisticated battery systems, particularly in automotive manufacturing, chemical processing, and precision manufacturing sectors. The country’s commitment to energy transition and Industry 4.0 initiatives creates sustained demand for advanced battery solutions.

France represents the second-largest market with significant growth in nuclear power support systems, telecommunications infrastructure, and industrial automation applications. French market characteristics include strong government support for domestic battery manufacturing and emphasis on energy security considerations. The country’s diverse industrial base creates demand across multiple battery technology segments.

United Kingdom shows robust growth despite Brexit-related uncertainties, with particular strength in data center applications, telecommunications, and offshore renewable energy projects. UK market dynamics are influenced by aggressive net-zero targets and substantial investments in grid modernization and renewable energy infrastructure.

Nordic countries including Sweden, Norway, and Denmark demonstrate exceptional growth rates exceeding 15% annually in renewable energy storage applications. Regional advantages include abundant renewable energy resources, supportive regulatory frameworks, and strong industrial clusters in clean technology sectors. These markets show particular strength in large-scale energy storage and grid stabilization applications.

Eastern European markets including Poland, Czech Republic, and Hungary are emerging as significant growth opportunities driven by industrial modernization and EU infrastructure investments. Market development in these regions is supported by favorable investment climates and growing recognition of battery technology benefits.

Market leadership in the European industrial battery sector is distributed among several key categories of participants, each bringing distinct capabilities and market positioning strategies:

Competitive strategies focus on technological differentiation, regional manufacturing capabilities, and comprehensive service offerings. Market positioning varies from specialized niche players focusing on specific applications to integrated solution providers offering complete battery systems and services. The competitive landscape is characterized by ongoing consolidation as companies seek to achieve scale advantages and expand their technological capabilities.

Innovation leadership remains a critical competitive factor, with companies investing heavily in next-generation battery technologies and advanced manufacturing processes. Partnership strategies are increasingly important as companies collaborate with industrial end-users, system integrators, and technology providers to develop comprehensive solutions.

Technology segmentation reveals distinct market dynamics across different battery chemistries and system architectures:

By Battery Technology:

By Application:

By End-User Industry:

Lead-acid battery segment continues to represent a significant portion of the market despite growing competition from lithium-ion technologies. Market resilience in this category stems from cost advantages, established supply chains, and proven performance in traditional backup power applications. However, growth limitations are evident as customers increasingly prioritize energy density, lifecycle costs, and environmental considerations that favor newer technologies.

Lithium-ion battery adoption is accelerating rapidly across industrial applications, with market penetration reaching approximately 35% in new installations. Technology advantages including higher energy density, faster charging capabilities, and longer lifespans are driving replacement of traditional battery systems. The segment benefits from declining costs and improving safety characteristics that address historical concerns about lithium-ion deployment in industrial environments.

Energy storage applications represent the fastest-growing category, with annual growth rates exceeding 20% in several European markets. Market drivers include renewable energy integration requirements, grid modernization initiatives, and increasing recognition of energy storage value in industrial operations. This category demonstrates particular strength in countries with aggressive renewable energy targets and supportive regulatory frameworks.

UPS applications maintain steady growth driven by increasing digitalization and the critical importance of power reliability in modern industrial operations. Technology evolution in this category focuses on improved efficiency, reduced maintenance requirements, and enhanced monitoring capabilities that provide better visibility into system performance and health status.

Manufacturers benefit from the growing European industrial battery market through expanded revenue opportunities and the ability to leverage advanced manufacturing capabilities. Technology leadership positions enable premium pricing and stronger customer relationships, while scale advantages provide cost competitiveness in increasingly competitive markets. Innovation investments create opportunities for intellectual property development and technology licensing that can generate additional revenue streams.

End-users gain significant operational advantages through improved power reliability, reduced maintenance requirements, and enhanced system monitoring capabilities. Total cost of ownership benefits include lower energy costs, reduced downtime, and improved operational efficiency that can justify initial investment costs. Sustainability benefits help organizations meet environmental objectives and regulatory compliance requirements while potentially qualifying for incentives and favorable financing terms.

System integrators and service providers benefit from growing demand for comprehensive battery solutions that include design, installation, commissioning, and ongoing maintenance services. Service opportunities create recurring revenue streams and deeper customer relationships that provide competitive advantages. Technology partnerships with battery manufacturers enable access to latest innovations and preferred supplier status.

Investors find attractive opportunities in a market characterized by strong growth fundamentals, technological innovation, and supportive regulatory environments. Market dynamics favor companies with strong technology positions, manufacturing capabilities, and comprehensive service offerings. ESG considerations align with growing investor focus on sustainable and responsible investment opportunities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization integration is transforming the industrial battery landscape as manufacturers incorporate IoT sensors, cloud connectivity, and artificial intelligence into battery management systems. Smart battery systems provide real-time monitoring, predictive maintenance capabilities, and remote diagnostics that improve reliability and reduce operational costs. This trend is driving demand for more sophisticated battery solutions that can integrate seamlessly with broader industrial automation and energy management platforms.

Sustainability focus is reshaping product development and market positioning strategies as European companies prioritize environmental responsibility throughout the battery lifecycle. Circular economy principles are influencing design decisions, manufacturing processes, and end-of-life management strategies. Companies are developing comprehensive recycling programs and second-life applications that extend battery value and reduce environmental impact.

Modular system architectures are gaining popularity as industrial users seek flexible, scalable solutions that can adapt to changing requirements. Standardization efforts are reducing complexity and improving interoperability while enabling more cost-effective deployment and maintenance. This trend supports the development of battery-as-a-service models that provide greater flexibility for end-users.

Energy-as-a-service business models are emerging as companies seek to reduce capital expenditure requirements while accessing advanced battery technologies. Performance-based contracting shifts risk from end-users to service providers while ensuring optimal system performance throughout the contract period. This trend is particularly attractive to small and medium-sized enterprises that may lack internal technical expertise.

Manufacturing capacity expansion across Europe is accelerating as companies respond to growing demand and policy initiatives promoting domestic battery production. Northvolt’s expansion of its Swedish gigafactory represents a significant milestone in European battery manufacturing capabilities, while other companies are announcing similar investments across the continent. These developments are reducing European dependence on Asian battery suppliers and creating new employment opportunities.

Technology partnerships between battery manufacturers, automotive companies, and industrial users are accelerating innovation and market development. Collaborative research initiatives are focusing on next-generation battery technologies including solid-state batteries, advanced lithium chemistries, and alternative battery technologies that could transform industrial applications.

Regulatory developments including the European Union’s Battery Regulation are establishing comprehensive requirements for battery performance, sustainability, and end-of-life management. Policy initiatives supporting domestic battery manufacturing and critical materials sourcing are reshaping supply chain strategies and investment priorities across the industry.

Acquisition activity is increasing as companies seek to expand their technological capabilities and market reach. Strategic consolidation is creating larger, more capable organizations that can compete effectively in global markets while serving diverse customer requirements across multiple industrial segments.

MarkWide Research analysis indicates that companies should prioritize technology differentiation and comprehensive service capabilities to succeed in the increasingly competitive European industrial battery market. Investment priorities should focus on advanced battery management systems, predictive maintenance capabilities, and integration with broader industrial automation platforms that provide enhanced value propositions for end-users.

Market positioning strategies should emphasize sustainability credentials, European manufacturing capabilities, and comprehensive lifecycle support that addresses growing customer concerns about environmental impact and supply chain resilience. Partnership development with system integrators, industrial automation providers, and renewable energy developers can create new market opportunities and strengthen competitive positioning.

Geographic expansion strategies should target high-growth markets in Eastern Europe and Nordic countries where industrial modernization and renewable energy adoption are creating substantial demand for advanced battery solutions. Application diversification beyond traditional backup power applications to include energy storage, grid services, and industrial automation can provide new revenue streams and reduce market concentration risks.

Technology roadmap development should balance investments in proven technologies with exploration of emerging solutions that could provide future competitive advantages. Talent acquisition and development programs are essential to address skills shortages and build internal capabilities required for success in rapidly evolving battery technologies and applications.

Long-term prospects for the European industrial battery market remain highly positive, with MWR projections indicating sustained growth driven by electrification trends, renewable energy integration, and industrial digitalization initiatives. Market evolution will be characterized by continued technology advancement, increasing system sophistication, and expanding application diversity that creates new opportunities for innovative companies.

Technology development trajectories suggest that solid-state batteries and advanced lithium chemistries will begin commercial deployment within the next five years, potentially transforming performance characteristics and application possibilities. Cost reduction trends are expected to continue, making advanced battery technologies accessible to broader market segments and accelerating replacement of traditional solutions.

Regulatory environment evolution will likely include more stringent sustainability requirements, enhanced safety standards, and continued support for domestic manufacturing capabilities. Policy initiatives promoting energy security and supply chain resilience will favor European manufacturers and create additional market opportunities for companies with strong regional presence.

Market structure is expected to consolidate around companies with strong technology positions, comprehensive service capabilities, and sustainable business models. Growth opportunities will be most significant for organizations that can successfully integrate battery solutions with broader energy management and industrial automation platforms while maintaining focus on sustainability and customer value creation.

The European industrial battery market represents a dynamic and rapidly evolving sector with exceptional growth potential driven by technological innovation, regulatory support, and increasing industrial demand for reliable, sustainable power solutions. Market fundamentals remain strong across multiple dimensions including technology advancement, application diversity, and supportive policy environments that favor continued expansion and development.

Competitive dynamics are intensifying as traditional manufacturers face competition from innovative technology providers and new market entrants, creating both challenges and opportunities for market participants. Success factors increasingly center on technology differentiation, comprehensive service capabilities, and ability to address evolving customer requirements for sustainability, reliability, and integration with broader industrial systems.

Future market development will be shaped by continued electrification trends, renewable energy integration requirements, and industrial digitalization initiatives that create new applications and expand market opportunities. European industrial battery market participants who can successfully navigate these trends while maintaining focus on innovation, sustainability, and customer value creation are well-positioned to capture significant growth opportunities in this expanding and strategically important market sector.

What is Industrial Battery?

Industrial batteries are energy storage devices designed for use in various industrial applications, including renewable energy systems, electric vehicles, and backup power solutions. They are characterized by their high capacity, durability, and ability to operate in demanding environments.

What are the key players in the European Industrial Battery Market?

Key players in the European Industrial Battery Market include companies such as Siemens, Saft Groupe, and Northvolt, which are involved in the production and development of advanced battery technologies for various applications, including electric mobility and energy storage solutions, among others.

What are the main drivers of growth in the European Industrial Battery Market?

The growth of the European Industrial Battery Market is driven by the increasing demand for renewable energy storage, the rise of electric vehicles, and the need for reliable backup power systems in industrial settings. Additionally, government initiatives promoting sustainable energy solutions contribute to market expansion.

What challenges does the European Industrial Battery Market face?

The European Industrial Battery Market faces challenges such as supply chain disruptions, high production costs, and environmental concerns related to battery disposal and recycling. These factors can hinder the growth and adoption of industrial battery technologies.

What opportunities exist in the European Industrial Battery Market?

Opportunities in the European Industrial Battery Market include advancements in battery technology, such as solid-state batteries and improved recycling methods. Additionally, the increasing investment in electric vehicle infrastructure presents significant growth potential for battery manufacturers.

What trends are shaping the European Industrial Battery Market?

Trends shaping the European Industrial Battery Market include the shift towards sustainable energy solutions, the integration of smart technologies in battery management systems, and the growing focus on circular economy practices in battery production and recycling.

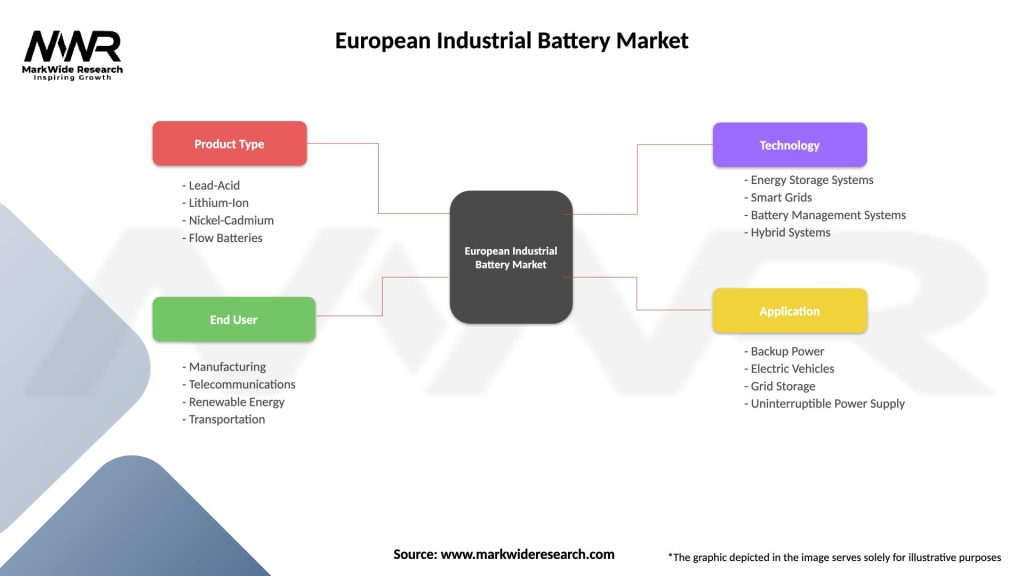

European Industrial Battery Market

| Segmentation Details | Description |

|---|---|

| Product Type | Lead-Acid, Lithium-Ion, Nickel-Cadmium, Flow Batteries |

| End User | Manufacturing, Telecommunications, Renewable Energy, Transportation |

| Technology | Energy Storage Systems, Smart Grids, Battery Management Systems, Hybrid Systems |

| Application | Backup Power, Electric Vehicles, Grid Storage, Uninterruptible Power Supply |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the European Industrial Battery Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.