444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The European EV battery systems market represents one of the most dynamic and rapidly evolving sectors within the continent’s automotive industry. As Europe accelerates its transition toward sustainable transportation, the demand for advanced battery technologies has reached unprecedented levels. The market encompasses a comprehensive range of battery solutions, including lithium-ion, solid-state, and emerging next-generation technologies specifically designed for electric vehicles.

Market dynamics indicate robust growth driven by stringent environmental regulations, substantial government incentives, and increasing consumer acceptance of electric mobility. The European Union’s ambitious climate targets, including the plan to ban internal combustion engine vehicles by 2035, have created a compelling environment for battery system manufacturers. Current market trends show a 12.8% annual growth rate in battery system adoption across major European markets, with Germany, France, and the Netherlands leading the charge.

Technological advancement remains at the forefront of market development, with European manufacturers investing heavily in research and development to enhance energy density, reduce charging times, and improve overall battery performance. The integration of smart battery management systems and advanced thermal management technologies has positioned European battery solutions as globally competitive alternatives to Asian counterparts.

The European EV battery systems market refers to the comprehensive ecosystem of battery technologies, manufacturing capabilities, and supply chain networks dedicated to powering electric vehicles across European territories. This market encompasses the design, production, distribution, and servicing of battery packs, cells, and related components specifically engineered for electric passenger vehicles, commercial trucks, buses, and two-wheelers.

Battery systems in this context include not only the physical battery cells and packs but also the sophisticated battery management systems, thermal regulation technologies, charging infrastructure compatibility features, and safety mechanisms that ensure optimal performance and longevity. The market extends beyond traditional automotive applications to include energy storage solutions for grid integration and vehicle-to-grid technologies.

European market characteristics distinguish this sector through its emphasis on sustainability, circular economy principles, and advanced manufacturing standards. The market prioritizes environmentally responsible sourcing of raw materials, efficient recycling processes, and the development of battery technologies that align with Europe’s broader decarbonization objectives.

Market transformation across Europe’s EV battery systems sector reflects a fundamental shift in automotive manufacturing and energy storage technologies. The convergence of regulatory pressure, technological innovation, and consumer demand has created an environment where battery systems have become the critical differentiator in electric vehicle performance and market success.

Key market drivers include the European Green Deal initiatives, which have accelerated investment in clean transportation technologies by 68% over the past three years. Major automotive manufacturers have committed substantial resources to battery technology development, with several establishing dedicated battery manufacturing facilities across strategic European locations.

Competitive landscape features a mix of established automotive suppliers, specialized battery manufacturers, and emerging technology companies. European companies are increasingly focusing on developing proprietary battery chemistries and manufacturing processes that reduce dependence on Asian supply chains while maintaining cost competitiveness and performance standards.

Market segmentation reveals diverse applications across passenger vehicles, commercial transportation, and stationary energy storage systems. The passenger vehicle segment currently dominates market share, while commercial vehicle applications show the highest growth potential due to fleet electrification initiatives and urban emission regulations.

Strategic market insights reveal several critical trends shaping the European EV battery systems landscape:

Market maturation indicators suggest that European battery systems are transitioning from early adoption phase to mainstream market acceptance, with 43% of European consumers now considering electric vehicles as their next purchase option.

Regulatory frameworks serve as the primary catalyst for European EV battery systems market expansion. The European Union’s comprehensive climate legislation, including the Fit for 55 package and the proposed ban on internal combustion engines by 2035, creates mandatory demand for electric vehicle technologies. These regulations establish clear market signals that drive long-term investment decisions and strategic planning across the automotive value chain.

Environmental consciousness among European consumers has reached critical mass, with sustainability considerations increasingly influencing purchasing decisions. The growing awareness of climate change impacts and air quality concerns in urban areas has created strong consumer pull for clean transportation solutions. This shift in consumer preferences provides sustainable demand foundation for battery system manufacturers.

Technological advancement in battery chemistry and manufacturing processes continues to improve the value proposition of electric vehicles. Recent breakthroughs in energy density, charging speed, and battery longevity have addressed many historical concerns about electric vehicle adoption. The development of solid-state batteries and advanced lithium-ion technologies promises further performance improvements.

Government incentives across European markets provide substantial financial support for electric vehicle adoption and battery technology development. These incentives include purchase subsidies, tax benefits, infrastructure investment, and research grants that reduce market barriers and accelerate technology deployment.

Infrastructure development in charging networks removes a significant adoption barrier for electric vehicles. The rapid expansion of fast-charging infrastructure across European highways and urban areas increases consumer confidence in electric vehicle viability for long-distance travel and daily use applications.

Raw material dependencies present significant challenges for European battery manufacturers, particularly regarding critical minerals like lithium, cobalt, and rare earth elements. The concentration of these resources in geopolitically sensitive regions creates supply chain vulnerabilities and price volatility that can impact market stability and growth trajectories.

High capital requirements for battery manufacturing facilities represent substantial barriers to market entry and expansion. The establishment of gigafactory-scale production facilities requires billions in investment, creating challenges for smaller companies and potentially limiting competitive dynamics within the market.

Technical complexity in battery system integration and manufacturing processes demands specialized expertise and advanced manufacturing capabilities. The need for precise quality control, safety compliance, and performance optimization creates operational challenges that can limit production scalability and market responsiveness.

Recycling infrastructure limitations pose long-term sustainability concerns as the first generation of electric vehicle batteries approaches end-of-life. The lack of established recycling processes and facilities could create environmental challenges and resource recovery inefficiencies that impact market sustainability.

Competition from established markets in Asia, particularly China and South Korea, presents ongoing challenges for European manufacturers seeking to establish market leadership. The mature manufacturing ecosystems and cost advantages in Asian markets create competitive pressure on European battery system providers.

Commercial vehicle electrification represents a substantial growth opportunity as European cities implement zero-emission zones and logistics companies seek to reduce operational costs. The commercial vehicle segment offers higher value per unit and longer replacement cycles, creating attractive market dynamics for battery system providers.

Energy storage integration beyond automotive applications opens new market segments for battery manufacturers. Grid-scale energy storage, residential energy systems, and industrial applications provide diversification opportunities that leverage existing battery technologies while addressing broader energy transition needs.

Second-life applications for automotive batteries create additional revenue streams and support circular economy objectives. Batteries that no longer meet automotive performance requirements can serve stationary energy storage applications, extending their useful life and improving overall economics.

Advanced manufacturing technologies including automation, artificial intelligence, and digital twin technologies offer opportunities to improve production efficiency and product quality while reducing costs. European manufacturers can leverage these technologies to maintain competitive advantages despite higher labor costs.

Strategic partnerships with automotive OEMs, technology companies, and research institutions provide opportunities to accelerate innovation and market penetration. Collaborative development programs can share risks and costs while accelerating time-to-market for new technologies.

Export potential to other regions as European battery technologies mature and achieve cost competitiveness. The reputation for quality and sustainability associated with European manufacturing could create export opportunities to markets with similar regulatory and consumer preferences.

Supply and demand dynamics within the European EV battery systems market reflect the rapid transformation of the automotive industry. Current demand significantly exceeds supply capacity, creating favorable pricing conditions for manufacturers while highlighting the urgent need for production capacity expansion. This supply-demand imbalance is expected to persist through the mid-2020s as vehicle electrification accelerates faster than battery production capacity can scale.

Competitive dynamics are evolving as traditional automotive suppliers compete with specialized battery manufacturers and new market entrants. The market is witnessing increased vertical integration as automotive OEMs seek to secure battery supply and capture value across the battery value chain. This trend is reshaping traditional supplier relationships and creating new competitive landscapes.

Technology evolution continues to drive market dynamics as next-generation battery technologies promise significant performance improvements. The transition from current lithium-ion technologies to solid-state batteries and other advanced chemistries creates both opportunities and risks for market participants. Companies must balance investments in current technologies with preparation for future technology transitions.

Pricing dynamics reflect the interplay between raw material costs, manufacturing scale, and competitive pressure. While battery costs have declined significantly over the past decade, recent increases in raw material prices have created upward pressure on battery system costs. Market participants are implementing various strategies to manage cost pressures while maintaining profitability.

Regulatory dynamics continue to shape market development through evolving safety standards, environmental requirements, and performance specifications. The implementation of new regulations creates both compliance costs and market opportunities for companies that can meet or exceed regulatory requirements.

Comprehensive market analysis employs multiple research methodologies to ensure accuracy and completeness of market insights. Primary research includes extensive interviews with industry executives, technology experts, and market participants across the European EV battery systems value chain. These interviews provide qualitative insights into market trends, competitive dynamics, and future development directions.

Secondary research encompasses analysis of industry reports, company financial statements, patent filings, and regulatory documents to establish quantitative market foundations. This research provides historical market data, technology development trends, and competitive positioning information essential for market analysis.

Market modeling utilizes advanced analytical techniques to project market development scenarios based on various assumptions about technology adoption, regulatory implementation, and economic conditions. These models incorporate multiple variables to provide robust market forecasts and sensitivity analysis.

Expert validation ensures research findings align with industry expertise and market realities. Independent industry experts review research methodologies, data sources, and analytical conclusions to verify accuracy and completeness of market insights.

Data triangulation combines multiple data sources and research methodologies to validate market findings and reduce analytical bias. This approach ensures that market insights reflect comprehensive understanding of complex market dynamics rather than single-source perspectives.

Germany dominates the European EV battery systems market with approximately 32% market share, driven by its strong automotive manufacturing base and substantial government support for electric vehicle adoption. German automotive OEMs have made significant investments in battery technology development and manufacturing capacity, positioning the country as a regional leader in battery systems innovation.

France represents the second-largest market with 18% market share, benefiting from strong government incentives and a growing network of charging infrastructure. French companies are focusing on battery recycling and circular economy applications, creating unique market positioning within the European landscape.

Netherlands and Norway demonstrate the highest per-capita adoption rates of electric vehicles, with combined market share of 15%. These markets serve as early adoption indicators for new battery technologies and provide valuable insights into consumer preferences and market development patterns.

United Kingdom maintains significant market presence despite Brexit-related challenges, with 14% market share supported by ambitious climate targets and substantial private sector investment in battery manufacturing facilities. The UK market emphasizes advanced battery chemistry development and manufacturing process innovation.

Italy and Spain represent emerging markets with combined 12% market share, showing rapid growth potential as electric vehicle adoption accelerates. These markets benefit from favorable climate conditions for electric vehicle operation and growing consumer acceptance of sustainable transportation solutions.

Nordic countries including Sweden, Denmark, and Finland collectively account for 9% market share, with strong emphasis on sustainability and environmental performance. These markets prioritize battery recycling and renewable energy integration in battery manufacturing processes.

Market leadership in European EV battery systems reflects a diverse ecosystem of established automotive suppliers, specialized battery manufacturers, and emerging technology companies. The competitive landscape continues to evolve as companies adapt to changing market demands and technological requirements.

Strategic positioning varies among competitors, with some focusing on cost leadership while others emphasize technology innovation or sustainability credentials. The market supports multiple competitive strategies as different customer segments prioritize various value propositions.

Partnership strategies are increasingly important as companies seek to leverage complementary capabilities and share development risks. Joint ventures, technology licensing agreements, and supply partnerships are common approaches to market development and competitive positioning.

By Battery Type:

By Vehicle Type:

By Application:

By Capacity Range:

Passenger Vehicle Segment represents the largest market category, driven by consumer adoption of electric vehicles and automotive OEM electrification strategies. This segment emphasizes energy density, charging speed, and cost optimization to meet consumer expectations for vehicle performance and affordability. Recent developments include improved battery management systems and thermal regulation technologies that enhance vehicle range and reliability.

Commercial Vehicle Applications show the highest growth potential as fleet operators seek to reduce operational costs and comply with urban emission regulations. Commercial vehicle batteries require different optimization parameters, emphasizing durability, fast charging capabilities, and total cost of ownership rather than maximum energy density. This segment benefits from predictable usage patterns and centralized charging infrastructure.

Energy Storage Integration creates new market opportunities beyond traditional automotive applications. Vehicle-to-grid technologies enable electric vehicles to serve as distributed energy storage resources, providing grid stabilization services and additional revenue streams for vehicle owners. This application requires specialized battery management systems and grid integration capabilities.

Technology Categories reflect different performance and cost trade-offs suitable for various applications. Lithium-ion batteries continue to dominate current applications, while solid-state technologies promise significant performance improvements for future applications. The market supports multiple technology approaches as different applications prioritize various performance characteristics.

Manufacturing Categories distinguish between different production approaches and scale requirements. Large-scale gigafactory production emphasizes cost efficiency and volume capacity, while specialized manufacturing focuses on advanced technologies and customized solutions for specific applications.

Automotive Manufacturers benefit from improved vehicle performance characteristics, reduced emissions compliance costs, and access to new market segments. Electric vehicle platforms enable innovative vehicle designs and features not possible with internal combustion engines. Battery system integration provides opportunities for vertical integration and value chain control.

Battery Manufacturers gain access to large-scale market opportunities with long-term growth potential. The automotive market provides volume demand that supports manufacturing scale economies and technology development investments. Strategic partnerships with automotive OEMs create stable revenue streams and collaborative development opportunities.

Consumers receive improved vehicle performance, reduced operating costs, and environmental benefits from electric vehicle adoption. Advanced battery systems provide longer vehicle range, faster charging times, and improved reliability compared to earlier electric vehicle technologies. Government incentives and improving charging infrastructure reduce adoption barriers.

Energy Sector Stakeholders benefit from grid integration opportunities and distributed energy storage capabilities. Electric vehicle batteries can provide grid stabilization services, peak demand management, and renewable energy integration support. These applications create additional revenue opportunities and improve overall energy system efficiency.

Environmental Stakeholders achieve significant emission reductions and air quality improvements from transportation electrification. Battery recycling and circular economy applications support sustainable resource utilization and waste reduction objectives. The transition to electric vehicles contributes to broader climate change mitigation goals.

Economic Development benefits include job creation in manufacturing, research and development, and supporting industries. The battery systems market attracts substantial investment and creates high-value employment opportunities in engineering, manufacturing, and technology development.

Strengths:

Weaknesses:

Opportunities:

Threats:

Solid-state Battery Development represents the most significant technological trend, promising substantial improvements in energy density, safety, and charging speed. European companies are investing heavily in solid-state technology development, with several manufacturers planning commercial deployment within the next five years. This technology could provide competitive advantages for European manufacturers.

Manufacturing Localization continues as companies seek to reduce supply chain risks and transportation costs. The establishment of gigafactory-scale production facilities across Europe creates regional manufacturing capabilities and reduces dependence on Asian suppliers. This trend supports supply chain resilience and local economic development.

Circular Economy Integration becomes increasingly important as the first generation of electric vehicle batteries approaches end-of-life. Companies are developing comprehensive recycling processes and second-life applications that recover valuable materials and extend battery utility. This trend supports sustainability objectives and resource efficiency.

Smart Battery Systems incorporate advanced monitoring, diagnostics, and optimization capabilities that improve performance and longevity. These systems use artificial intelligence and machine learning to optimize charging patterns, predict maintenance needs, and maximize battery life. Smart systems provide competitive differentiation and improved user experiences.

Fast Charging Technologies address consumer concerns about charging time and convenience. Developments in battery chemistry and thermal management enable charging speeds that approach conventional vehicle refueling times. Fast charging capabilities are becoming essential for consumer acceptance and market growth.

Vehicle-to-Grid Integration expands battery system utility beyond vehicle propulsion to include grid services and energy storage applications. This trend creates additional revenue opportunities for vehicle owners and supports renewable energy integration. MarkWide Research indicates that vehicle-to-grid applications could represent 15% of total battery system value by 2030.

Strategic Partnerships between automotive OEMs and battery manufacturers are reshaping industry structure and competitive dynamics. Recent joint ventures and technology licensing agreements demonstrate the importance of collaborative approaches to battery system development and manufacturing. These partnerships share risks and costs while accelerating technology deployment.

Manufacturing Capacity Expansion continues across Europe as companies respond to growing demand and seek to establish market leadership. Several gigafactory projects are under construction or planning, representing billions in investment and substantial employment creation. This expansion supports supply chain localization and competitive positioning.

Technology Breakthroughs in battery chemistry and manufacturing processes provide performance improvements and cost reductions. Recent developments include improved cathode materials, advanced electrolyte formulations, and innovative manufacturing techniques that enhance battery performance while reducing production costs.

Regulatory Developments continue to shape market requirements and opportunities. New safety standards, environmental regulations, and performance specifications create compliance requirements while potentially providing competitive advantages for companies that exceed minimum standards.

Investment Activity remains robust as venture capital, private equity, and strategic investors support battery technology development and manufacturing capacity expansion. This investment activity demonstrates market confidence and provides capital for continued innovation and growth.

Recycling Infrastructure development addresses long-term sustainability requirements and resource recovery opportunities. New recycling facilities and processes are being established to handle growing volumes of end-of-life batteries while recovering valuable materials for new battery production.

Technology Investment should prioritize next-generation battery chemistries and manufacturing processes that provide sustainable competitive advantages. Companies should balance investments in current technologies with preparation for future technology transitions. Focus areas include solid-state batteries, advanced manufacturing automation, and smart battery management systems.

Supply Chain Strategy requires careful balance between cost optimization and supply security. Companies should develop diversified supplier relationships while investing in regional supply chain capabilities. Raw material sourcing strategies should emphasize sustainability and ethical sourcing practices that align with European values and regulations.

Partnership Development becomes increasingly important as market complexity and capital requirements exceed individual company capabilities. Strategic partnerships should focus on complementary capabilities, shared risk management, and accelerated market development. Joint ventures and technology licensing can provide access to markets and technologies while sharing development costs.

Market Positioning should emphasize unique value propositions that differentiate European battery systems from Asian competitors. Potential differentiation factors include sustainability credentials, advanced technology features, and superior customer service. Premium positioning may be more sustainable than cost competition in certain market segments.

Regulatory Compliance requires proactive engagement with evolving standards and requirements. Companies should participate in standard-setting processes and ensure that product development anticipates future regulatory requirements. Compliance capabilities can provide competitive advantages in regulated markets.

Sustainability Integration should be comprehensive, covering raw material sourcing, manufacturing processes, product design, and end-of-life management. Sustainability credentials are becoming increasingly important for consumer acceptance and regulatory compliance. Companies should develop measurable sustainability metrics and transparent reporting processes.

Market growth prospects remain exceptionally strong as electric vehicle adoption accelerates across European markets. MWR analysis projects continued robust expansion driven by regulatory requirements, improving technology performance, and growing consumer acceptance. The market is expected to maintain double-digit growth rates through the remainder of the decade.

Technology evolution will continue to drive market development as next-generation battery technologies achieve commercial viability. Solid-state batteries are expected to begin commercial deployment in premium vehicle applications by the mid-2020s, with broader market adoption following as manufacturing scales and costs decline. These technologies will provide significant performance improvements and competitive opportunities.

Manufacturing landscape will be transformed by substantial capacity expansion and technology advancement. European battery manufacturing capacity is projected to increase by over 400% by 2030, supporting supply chain localization and competitive positioning. Advanced manufacturing technologies will improve efficiency and reduce costs while maintaining quality standards.

Market maturation will bring increased competition and market segmentation as the industry evolves from early growth phase to mainstream market acceptance. Companies will need to develop clear competitive positioning and value propositions to succeed in increasingly competitive markets. Market consolidation may occur as smaller companies struggle to achieve necessary scale.

Sustainability requirements will become increasingly stringent as environmental regulations evolve and consumer awareness grows. Companies that establish leadership in sustainable practices and circular economy applications will be better positioned for long-term success. Sustainability will transition from competitive advantage to market requirement.

Integration opportunities beyond traditional automotive applications will create new market segments and revenue streams. Energy storage, grid services, and industrial applications will provide diversification opportunities for battery manufacturers. These applications may offer higher margins and more stable demand patterns than automotive markets.

The European EV battery systems market stands at a critical juncture where regulatory support, technological advancement, and market demand converge to create unprecedented growth opportunities. The market has evolved from early experimental phase to mainstream commercial viability, with established manufacturing capabilities and proven technology performance.

Strategic positioning for long-term success requires balanced investment in current technologies and next-generation development, comprehensive supply chain strategies, and strong sustainability credentials. Companies that can navigate the complex interplay of technology, regulation, and market dynamics while maintaining competitive cost structures will be best positioned for market leadership.

Market transformation will continue as electric vehicle adoption accelerates and battery technologies advance. The European market’s emphasis on sustainability, quality, and innovation creates opportunities for differentiation and premium positioning. Success will require continuous adaptation to evolving market requirements and competitive dynamics while maintaining focus on core value propositions that resonate with European consumers and regulatory frameworks.

What is EV Battery Systems?

EV Battery Systems refer to the technologies and components used to store and manage energy in electric vehicles, including battery packs, management systems, and charging infrastructure.

What are the key players in the European EV Battery Systems Market?

Key players in the European EV Battery Systems Market include companies like LG Chem, Samsung SDI, and Northvolt, which are involved in the production and development of advanced battery technologies, among others.

What are the main drivers of the European EV Battery Systems Market?

The main drivers of the European EV Battery Systems Market include the increasing demand for electric vehicles, government incentives for clean energy, and advancements in battery technology that enhance performance and reduce costs.

What challenges does the European EV Battery Systems Market face?

Challenges in the European EV Battery Systems Market include supply chain disruptions, the high cost of raw materials, and the need for extensive charging infrastructure to support widespread EV adoption.

What opportunities exist in the European EV Battery Systems Market?

Opportunities in the European EV Battery Systems Market include the potential for innovation in battery recycling technologies, the development of solid-state batteries, and partnerships between automakers and battery manufacturers to enhance production capabilities.

What trends are shaping the European EV Battery Systems Market?

Trends shaping the European EV Battery Systems Market include the shift towards sustainable battery materials, the integration of artificial intelligence in battery management systems, and the growing focus on energy density and charging speed improvements.

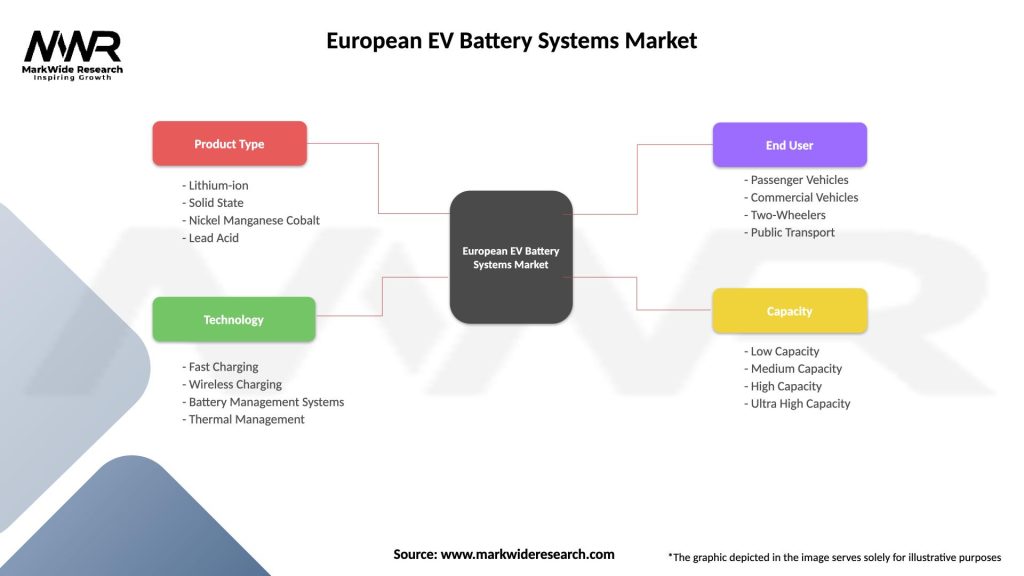

European EV Battery Systems Market

| Segmentation Details | Description |

|---|---|

| Product Type | Lithium-ion, Solid State, Nickel Manganese Cobalt, Lead Acid |

| Technology | Fast Charging, Wireless Charging, Battery Management Systems, Thermal Management |

| End User | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Public Transport |

| Capacity | Low Capacity, Medium Capacity, High Capacity, Ultra High Capacity |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the European EV Battery Systems Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.