444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe warehouse robots market represents a transformative sector within the broader automation and logistics industry, experiencing unprecedented growth driven by technological advancements and evolving supply chain demands. European businesses are increasingly adopting robotic solutions to enhance operational efficiency, reduce labor costs, and meet the growing demands of e-commerce and omnichannel retail operations.

Market dynamics indicate that the European region is witnessing substantial adoption of warehouse automation technologies, with countries like Germany, the United Kingdom, France, and the Netherlands leading the charge. The market encompasses various robotic solutions including autonomous mobile robots (AMRs), automated guided vehicles (AGVs), robotic picking systems, and collaborative robots (cobots) designed specifically for warehouse operations.

Growth projections suggest the market is expanding at a compound annual growth rate (CAGR) of 12.8%, driven by increasing labor shortages, rising operational costs, and the need for enhanced accuracy in order fulfillment processes. Technology integration with artificial intelligence, machine learning, and Internet of Things (IoT) capabilities is further accelerating market adoption across diverse industry verticals.

Regional distribution shows that Western Europe accounts for approximately 68% of the market share, while Eastern European countries are emerging as significant growth markets due to expanding manufacturing and logistics sectors. The market’s evolution reflects broader trends toward Industry 4.0 implementation and digital transformation initiatives across European enterprises.

The Europe warehouse robots market refers to the comprehensive ecosystem of robotic technologies, systems, and solutions specifically designed for warehouse and distribution center operations across European countries. This market encompasses the development, manufacturing, deployment, and maintenance of various robotic systems that automate material handling, inventory management, order picking, sorting, and packaging processes within warehouse environments.

Warehouse robots in this context include autonomous mobile robots that navigate warehouse floors independently, robotic arms for picking and placing operations, automated storage and retrieval systems, and collaborative robots that work alongside human workers. These systems integrate advanced technologies such as computer vision, artificial intelligence, sensor fusion, and cloud connectivity to optimize warehouse operations and improve overall supply chain efficiency.

Market scope extends beyond hardware to include software platforms, integration services, maintenance support, and consulting services that enable successful implementation and operation of robotic warehouse solutions. The market serves diverse industries including e-commerce, retail, automotive, pharmaceuticals, food and beverage, and manufacturing sectors across the European region.

European warehouse robotics has emerged as a critical component of modern supply chain infrastructure, driven by the region’s strong manufacturing base, advanced technological capabilities, and increasing demand for automated solutions. The market demonstrates robust growth potential with significant investments from both established players and innovative startups focusing on next-generation warehouse automation technologies.

Key market drivers include the rapid expansion of e-commerce activities, which has increased by 23% annually in recent years, creating unprecedented demand for efficient order fulfillment capabilities. Labor shortages across European countries, particularly in logistics and warehousing sectors, have accelerated the adoption of robotic solutions as businesses seek to maintain operational continuity and competitiveness.

Technology advancement in areas such as machine learning algorithms, sensor technologies, and battery efficiency has significantly improved the performance and cost-effectiveness of warehouse robots. The integration of 5G connectivity and edge computing capabilities is enabling real-time decision-making and enhanced coordination between multiple robotic systems within warehouse environments.

Market segmentation reveals diverse applications across various robotic categories, with autonomous mobile robots representing the fastest-growing segment due to their flexibility and relatively lower implementation costs. The pharmaceutical and healthcare sectors show particularly strong adoption rates, driven by stringent accuracy requirements and regulatory compliance needs.

Strategic insights from comprehensive market analysis reveal several critical trends shaping the European warehouse robots landscape:

Market intelligence indicates that successful implementations typically achieve operational efficiency improvements of 35-45% while reducing labor-related costs and improving accuracy in order fulfillment processes. These insights guide strategic decision-making for businesses considering warehouse automation investments.

Primary market drivers propelling the European warehouse robots market include several interconnected factors that create compelling business cases for automation adoption:

E-commerce Growth represents the most significant driver, with online retail sales continuing to expand rapidly across European markets. The demand for faster delivery times, accurate order fulfillment, and efficient returns processing has created operational pressures that traditional manual processes cannot adequately address. Consumer expectations for same-day and next-day delivery services require warehouse operations to achieve unprecedented levels of speed and accuracy.

Labor Market Challenges across Europe, including aging populations, skills shortages, and increasing labor costs, are driving businesses to seek automated alternatives. The logistics and warehousing sectors face particular challenges in attracting and retaining qualified workers, making robotic solutions increasingly attractive for maintaining operational continuity.

Operational Efficiency Requirements push organizations to optimize their warehouse operations through automation. Robotic systems can operate continuously, reduce error rates, and provide consistent performance levels that human workers cannot match over extended periods. Productivity improvements of up to 40% are commonly achieved through strategic robot deployment.

Technology Maturation has reached a point where warehouse robots offer reliable, cost-effective solutions with reasonable return on investment timelines. Advances in battery technology, sensor capabilities, and artificial intelligence have made robotic systems more practical and accessible for businesses of various sizes.

Regulatory Support from European governments through Industry 4.0 initiatives, digitalization programs, and automation incentives creates favorable conditions for warehouse robot adoption. Government policies promoting technological innovation and competitiveness encourage businesses to invest in advanced automation technologies.

Market restraints present significant challenges that may limit the pace of warehouse robot adoption across European markets:

High Initial Investment requirements represent the primary barrier for many businesses, particularly small and medium-sized enterprises. The capital expenditure for comprehensive warehouse automation systems, including robots, infrastructure modifications, and integration services, can be substantial and may require extended payback periods that some organizations cannot accommodate.

Technical Complexity associated with implementing and maintaining robotic systems creates operational challenges. Organizations must develop new technical capabilities, train personnel, and establish maintenance protocols that may strain existing resources. Integration difficulties with legacy warehouse management systems can further complicate implementation processes.

Workforce Concerns regarding job displacement and changing skill requirements create resistance to automation initiatives. Employee concerns about job security and the need for extensive retraining programs can slow adoption rates and create organizational challenges during implementation phases.

Regulatory Uncertainties surrounding safety standards, liability issues, and operational guidelines for warehouse robots create hesitation among potential adopters. Evolving regulations and compliance requirements may impact implementation timelines and increase overall project costs.

Technology Limitations in certain applications, such as handling irregular or fragile items, limit the scope of robotic automation. Current technology may not adequately address all warehouse operations, requiring continued reliance on human workers for specific tasks.

Emerging opportunities within the European warehouse robots market present significant potential for growth and innovation:

Small and Medium Enterprise (SME) Adoption represents a substantial untapped market segment. As robotic technologies become more affordable and accessible, smaller businesses can benefit from automation solutions previously available only to large enterprises. Robotics-as-a-Service (RaaS) models are making advanced automation accessible through subscription-based pricing structures.

Industry-Specific Solutions offer opportunities for specialized robotic applications tailored to unique sector requirements. The pharmaceutical industry, with its stringent quality control and traceability requirements, presents particular growth potential for specialized warehouse automation solutions.

Cross-Border E-commerce expansion creates demand for sophisticated warehouse operations capable of handling complex international shipping requirements, customs procedures, and multi-language processing capabilities. Robotic systems can provide the accuracy and efficiency needed for these complex operations.

Sustainability Initiatives align with European environmental goals, creating opportunities for energy-efficient robotic solutions that reduce carbon footprints and support corporate sustainability objectives. Green warehouse concepts incorporating renewable energy and efficient automation systems represent growing market opportunities.

Technology Integration with emerging technologies such as 5G networks, edge computing, and advanced AI algorithms creates opportunities for next-generation warehouse automation solutions that offer enhanced performance and capabilities.

Market dynamics within the European warehouse robots sector reflect complex interactions between technological advancement, economic factors, and evolving business requirements:

Supply Chain Disruptions experienced during recent global events have highlighted the importance of resilient and flexible warehouse operations. Organizations are increasingly recognizing that robotic automation can provide operational continuity and adaptability during challenging circumstances. Resilience planning now commonly includes automation components to reduce dependency on human labor availability.

Competitive Pressures drive businesses to seek operational advantages through advanced automation technologies. Companies that successfully implement warehouse robots often achieve significant competitive advantages in terms of cost efficiency, service quality, and operational flexibility. Market differentiation increasingly depends on operational excellence enabled by automation technologies.

Technology Evolution continues to reshape market dynamics as new capabilities emerge and existing technologies improve. The integration of artificial intelligence and machine learning enables robots to adapt to changing conditions and optimize their performance over time. Adaptive systems can learn from operational data and continuously improve their efficiency.

Partnership Ecosystems are developing between robot manufacturers, system integrators, software providers, and end-users to create comprehensive automation solutions. These collaborative relationships enable more effective implementations and ongoing support for complex warehouse automation projects.

Investment Patterns show increasing venture capital and private equity interest in warehouse automation technologies, driving innovation and market expansion. Funding availability supports both established companies and startups developing next-generation robotic solutions.

Comprehensive research methodology employed for analyzing the European warehouse robots market incorporates multiple data collection and analysis approaches to ensure accuracy and reliability:

Primary Research involves extensive interviews with industry executives, technology providers, system integrators, and end-users across various European countries. These interviews provide firsthand insights into market trends, challenges, and opportunities from stakeholders directly involved in warehouse automation projects.

Secondary Research encompasses analysis of industry reports, company financial statements, patent filings, and regulatory documents to understand market structure, competitive landscape, and technological developments. Data triangulation from multiple sources ensures comprehensive market understanding.

Market Surveys conducted among warehouse operators, logistics managers, and technology decision-makers provide quantitative insights into adoption patterns, investment priorities, and future planning considerations. Survey responses help validate market trends and identify emerging opportunities.

Technology Assessment includes evaluation of robotic systems, software platforms, and integration capabilities to understand current market offerings and future development directions. Performance benchmarking provides insights into competitive positioning and technology maturity levels.

Regional Analysis examines market conditions, regulatory environments, and economic factors across different European countries to identify regional variations and growth opportunities. This geographic perspective ensures comprehensive market coverage and localized insights.

Regional market analysis reveals distinct patterns and opportunities across European countries, with varying adoption rates and market characteristics:

Germany leads the European warehouse robots market, accounting for approximately 28% of regional adoption. The country’s strong manufacturing base, advanced technology infrastructure, and supportive government policies create favorable conditions for warehouse automation. German companies are particularly focused on high-precision applications and integration with existing manufacturing systems.

United Kingdom represents a significant market driven by robust e-commerce growth and logistics sector expansion. Brexit-related supply chain adaptations have accelerated automation adoption as companies seek to optimize operations and reduce dependencies. UK market share represents approximately 22% of European adoption.

France demonstrates strong growth in warehouse automation, particularly in the automotive and luxury goods sectors. French companies are emphasizing collaborative robotics and human-robot integration approaches. The market benefits from government digitalization initiatives and Industry 4.0 support programs.

Netherlands leverages its strategic location as a European logistics hub to drive warehouse automation adoption. The country’s advanced port facilities and distribution networks create demand for sophisticated robotic solutions capable of handling high-volume, time-sensitive operations.

Nordic Countries including Sweden, Denmark, and Norway show high adoption rates driven by labor cost considerations and technology-forward business cultures. These markets particularly favor sustainable and energy-efficient robotic solutions aligned with regional environmental priorities.

Eastern Europe represents emerging growth markets with increasing manufacturing and logistics activities. Countries like Poland, Czech Republic, and Hungary are experiencing rapid warehouse automation adoption as they become regional distribution hubs for multinational companies.

Competitive landscape within the European warehouse robots market features a diverse mix of established automation companies, specialized robotics firms, and emerging technology startups:

Market competition is intensifying as companies differentiate through technology innovation, industry specialization, and comprehensive service offerings. Strategic partnerships between robot manufacturers and system integrators are becoming increasingly common to provide end-to-end automation solutions.

Innovation focus areas include artificial intelligence integration, improved battery life, enhanced safety features, and simplified deployment processes. Companies are investing heavily in research and development to maintain competitive advantages and address evolving customer requirements.

Market segmentation analysis reveals diverse applications and technology categories within the European warehouse robots market:

By Robot Type:

By Application:

By Industry Vertical:

Autonomous Mobile Robots (AMRs) represent the fastest-growing segment within the European warehouse robots market, driven by their flexibility and relatively lower implementation complexity. AMR adoption has increased by 45% annually as businesses appreciate their ability to adapt to changing warehouse layouts and requirements without infrastructure modifications.

Robotic picking systems demonstrate strong growth in e-commerce applications where accuracy and speed are critical success factors. These systems integrate computer vision and artificial intelligence to handle diverse product types and packaging requirements. Picking accuracy improvements of up to 99.5% are commonly achieved through robotic implementation.

Collaborative robots (cobots) are gaining traction in applications where human expertise remains valuable while benefiting from robotic assistance. These systems focus on augmenting human capabilities rather than replacing workers entirely, addressing workforce concerns while improving operational efficiency.

Industry-specific solutions are emerging as companies recognize the value of specialized robotic systems tailored to unique sector requirements. Pharmaceutical applications, for example, require specialized handling capabilities for temperature-sensitive products and regulatory compliance features.

Software integration capabilities are becoming increasingly important as businesses seek comprehensive automation solutions that integrate with existing warehouse management systems, enterprise resource planning platforms, and supply chain management tools.

Warehouse operators benefit from significant operational improvements through robotic automation implementation:

Technology providers gain access to expanding market opportunities and revenue streams:

System integrators benefit from increased demand for comprehensive automation solutions and specialized expertise in robotic system implementation and optimization.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial Intelligence Integration represents a fundamental trend transforming warehouse robotics capabilities. AI-powered systems can learn from operational data, optimize performance over time, and adapt to changing conditions without human intervention. Machine learning algorithms enable robots to improve their efficiency and accuracy through experience.

Human-Robot Collaboration is evolving from simple coexistence to sophisticated partnership models where robots and humans work together to optimize warehouse operations. Collaborative approaches address workforce concerns while maximizing the benefits of both human expertise and robotic capabilities.

Cloud-Based Management systems are enabling centralized control and monitoring of distributed robotic fleets. Cloud connectivity provides real-time visibility, predictive maintenance capabilities, and performance optimization across multiple warehouse locations.

Modular and Scalable Solutions are becoming increasingly important as businesses seek flexible automation options that can grow with their operations. Modular designs allow incremental implementation and customization based on specific operational requirements.

Sustainability Focus drives development of energy-efficient robotic systems and sustainable warehouse operations. Green automation initiatives align with European environmental regulations and corporate sustainability objectives.

Industry 4.0 Integration connects warehouse robots with broader manufacturing and supply chain systems, creating comprehensive automation ecosystems. System integration enables end-to-end visibility and optimization across entire value chains.

Recent industry developments highlight the dynamic nature of the European warehouse robots market and emerging trends shaping its future:

Technology Partnerships between established automation companies and AI specialists are creating next-generation robotic solutions with enhanced intelligence and adaptability. These collaborations combine hardware expertise with advanced software capabilities to deliver comprehensive automation platforms.

Acquisition Activity in the market reflects consolidation trends as larger companies acquire specialized robotics firms to expand their technology portfolios and market reach. Strategic acquisitions enable rapid capability development and market expansion.

Pilot Programs and proof-of-concept implementations are becoming more common as businesses test robotic solutions before full-scale deployment. These programs help organizations understand implementation requirements and potential benefits while minimizing risks.

Regulatory Developments include updated safety standards and operational guidelines for warehouse robotics, providing clearer frameworks for implementation and operation. Standardization efforts help reduce implementation complexity and improve interoperability between different systems.

Investment Announcements from major logistics companies and retailers demonstrate growing confidence in warehouse automation technologies. Capital commitments signal market maturity and long-term growth potential.

Innovation Centers and research facilities focused on warehouse automation are being established across Europe, fostering technology development and collaboration between industry and academia.

Strategic recommendations for market participants based on comprehensive analysis of current trends and future opportunities:

For Warehouse Operators: MarkWide Research recommends starting with pilot implementations to understand operational impacts and requirements before full-scale deployment. Focus on applications with clear return on investment and minimal integration complexity to build internal expertise and confidence.

Technology Selection should prioritize flexibility and scalability over advanced features that may not provide immediate value. Choose solutions that can integrate with existing systems and adapt to changing operational requirements over time.

For Technology Providers: Develop industry-specific solutions that address unique sector requirements and regulatory compliance needs. Specialization strategies can create competitive advantages and premium pricing opportunities in targeted market segments.

Partnership Development with system integrators and service providers is essential for delivering comprehensive solutions and ongoing support. Ecosystem approaches provide better customer experiences and higher success rates for complex implementations.

For Investors: Focus on companies with strong technology differentiation, proven implementation track records, and comprehensive service capabilities. Market leaders with established customer bases and recurring revenue models offer more stable investment opportunities.

Geographic Expansion opportunities exist in Eastern European markets where warehouse automation adoption is accelerating. Early market entry can establish competitive positions in high-growth regions.

Future market outlook for European warehouse robots indicates continued strong growth driven by technological advancement and evolving business requirements. Market expansion is expected to accelerate as robotic solutions become more accessible and cost-effective for businesses of all sizes.

Technology evolution will focus on enhanced artificial intelligence capabilities, improved human-robot collaboration, and greater integration with broader supply chain systems. Next-generation robots will offer increased autonomy, better adaptability, and more sophisticated decision-making capabilities.

Market penetration is projected to increase significantly across industry verticals, with particular growth expected in healthcare, pharmaceuticals, and food processing sectors. Adoption rates may reach 60-70% among large warehouse operators within the next five years.

Geographic expansion will continue as Eastern European countries develop their logistics infrastructure and manufacturing capabilities. Regional growth patterns suggest balanced development across the European market with emerging opportunities in previously underserved areas.

Innovation focus will emphasize sustainability, energy efficiency, and circular economy principles aligned with European environmental objectives. Green robotics solutions will become increasingly important for regulatory compliance and corporate sustainability goals.

Investment levels are expected to remain strong as businesses recognize the strategic importance of warehouse automation for competitive positioning and operational resilience. MWR analysis suggests continued venture capital and private equity interest in innovative warehouse robotics companies.

The Europe warehouse robots market represents a dynamic and rapidly evolving sector with substantial growth potential driven by technological advancement, changing business requirements, and favorable market conditions. Market analysis reveals strong adoption trends across diverse industry verticals and geographic regions, supported by compelling business cases for automation implementation.

Key success factors for market participants include technology innovation, industry specialization, comprehensive service offerings, and strategic partnerships that deliver end-to-end automation solutions. Companies that can effectively address implementation challenges while demonstrating clear value propositions are positioned for significant growth opportunities.

Future prospects remain highly positive as warehouse automation becomes increasingly essential for competitive operations in the digital economy. The convergence of artificial intelligence, robotics, and connectivity technologies will continue to create new possibilities for warehouse optimization and supply chain efficiency.

Strategic positioning in this market requires understanding of regional variations, industry-specific requirements, and evolving technology capabilities. Organizations that invest in warehouse robotics today are building foundations for long-term operational excellence and competitive advantage in the European marketplace.

What is Warehouse Robots?

Warehouse robots are automated machines designed to assist in various tasks within a warehouse environment, such as picking, packing, sorting, and transporting goods. They enhance operational efficiency and accuracy in inventory management.

What are the key players in the Europe Warehouse Robots Market?

Key players in the Europe Warehouse Robots Market include companies like Kiva Systems, Fetch Robotics, and GreyOrange, which are known for their innovative robotic solutions for warehouse automation, among others.

What are the main drivers of the Europe Warehouse Robots Market?

The main drivers of the Europe Warehouse Robots Market include the increasing demand for automation in logistics, the need for improved efficiency in supply chain operations, and the rising labor costs that push companies to adopt robotic solutions.

What challenges does the Europe Warehouse Robots Market face?

Challenges in the Europe Warehouse Robots Market include high initial investment costs, the complexity of integrating robots with existing systems, and concerns regarding job displacement among warehouse workers.

What opportunities exist in the Europe Warehouse Robots Market?

Opportunities in the Europe Warehouse Robots Market include advancements in artificial intelligence and machine learning, which can enhance robot capabilities, and the growing trend of e-commerce, which increases the demand for efficient warehouse operations.

What trends are shaping the Europe Warehouse Robots Market?

Trends shaping the Europe Warehouse Robots Market include the rise of collaborative robots that work alongside human workers, the integration of IoT technology for real-time data tracking, and the development of autonomous mobile robots for flexible warehouse layouts.

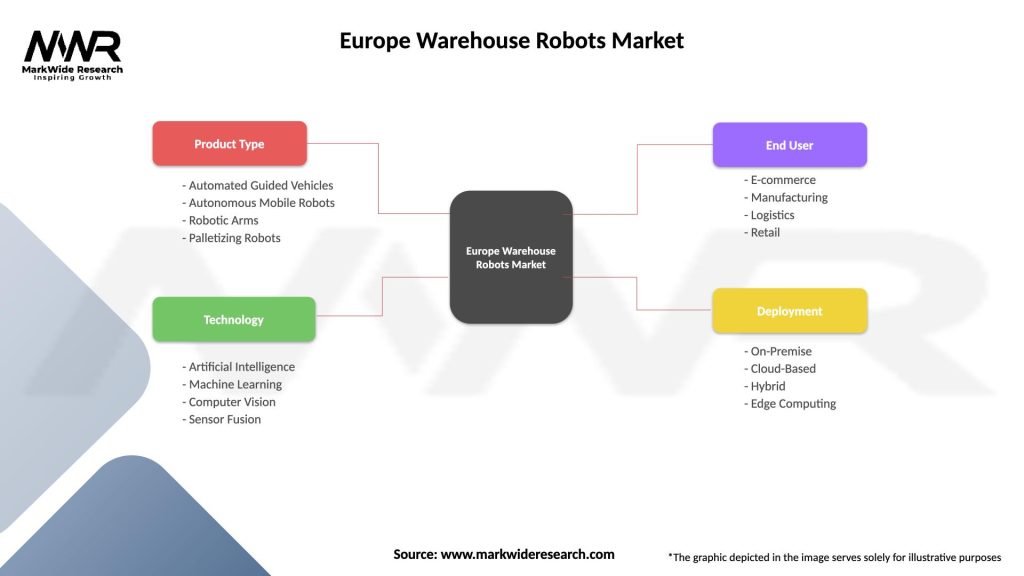

Europe Warehouse Robots Market

| Segmentation Details | Description |

|---|---|

| Product Type | Automated Guided Vehicles, Autonomous Mobile Robots, Robotic Arms, Palletizing Robots |

| Technology | Artificial Intelligence, Machine Learning, Computer Vision, Sensor Fusion |

| End User | E-commerce, Manufacturing, Logistics, Retail |

| Deployment | On-Premise, Cloud-Based, Hybrid, Edge Computing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Warehouse Robots Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.