444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe rigid bulk packaging market represents a cornerstone of the continent’s industrial packaging landscape, serving diverse sectors from chemicals and pharmaceuticals to food and beverages. This dynamic market encompasses a comprehensive range of packaging solutions including intermediate bulk containers (IBCs), drums, boxes, and specialized rigid containers designed for bulk material transportation and storage. European manufacturers have established themselves as global leaders in innovative packaging technologies, driven by stringent regulatory requirements and sustainability mandates.

Market dynamics indicate robust growth potential, with the sector experiencing a 6.2% CAGR driven by increasing industrial production and evolving consumer preferences. The region’s commitment to circular economy principles has catalyzed significant investments in recyclable and reusable packaging solutions. Germany, France, and the United Kingdom emerge as dominant markets, collectively accounting for approximately 58% of regional demand.

Technological advancement continues to reshape the market landscape, with smart packaging solutions and IoT-enabled containers gaining traction among industrial users. The integration of RFID technology and digital tracking systems has enhanced supply chain visibility and operational efficiency. Sustainability initiatives remain paramount, with manufacturers increasingly adopting bio-based materials and implementing closed-loop recycling systems to meet evolving environmental regulations.

The Europe rigid bulk packaging market refers to the comprehensive ecosystem of sturdy, non-flexible containers designed for storing, transporting, and handling large quantities of liquid, semi-liquid, and solid materials across various industrial sectors throughout European territories.

Rigid bulk packaging encompasses various container types including intermediate bulk containers (IBCs), steel and plastic drums, fiber drums, rigid boxes, and specialized containers manufactured from materials such as high-density polyethylene (HDPE), steel, aluminum, and composite materials. These packaging solutions are engineered to withstand substantial weight loads, resist chemical corrosion, and maintain structural integrity during transportation and storage operations.

Key characteristics of rigid bulk packaging include superior durability, stackability for efficient storage, compatibility with automated handling systems, and compliance with international transportation regulations. The market serves critical functions in supply chain management, enabling efficient bulk material distribution while ensuring product safety and regulatory compliance across diverse European industries.

Strategic market analysis reveals the Europe rigid bulk packaging market as a mature yet evolving sector characterized by steady growth and continuous innovation. The market demonstrates resilience across economic cycles, supported by essential industrial applications and increasing demand for sustainable packaging solutions. Chemical industry applications represent the largest segment, accounting for approximately 42% of total market demand.

Competitive landscape features established multinational corporations alongside specialized regional manufacturers, creating a balanced ecosystem of innovation and market stability. Leading companies have invested heavily in research and development, focusing on lightweight designs, enhanced barrier properties, and improved recyclability. Market consolidation trends indicate strategic partnerships and acquisitions aimed at expanding geographical reach and technological capabilities.

Regulatory environment significantly influences market dynamics, with European Union directives on packaging waste and circular economy principles driving innovation in sustainable packaging solutions. The implementation of extended producer responsibility (EPR) schemes has accelerated the adoption of recyclable and reusable packaging formats. Future growth prospects remain positive, supported by industrial expansion, e-commerce growth, and increasing emphasis on supply chain sustainability.

Market segmentation analysis reveals distinct growth patterns across various application sectors and geographical regions. The following insights provide comprehensive understanding of market dynamics:

Emerging trends indicate increasing preference for lightweight yet durable packaging solutions that reduce transportation costs while maintaining product integrity. The integration of digital technologies enables real-time monitoring of container conditions and inventory management, providing significant value to industrial users.

Industrial expansion across European manufacturing sectors serves as the primary catalyst for rigid bulk packaging demand. The region’s robust chemical industry, supported by major production facilities in Germany, Netherlands, and Belgium, generates substantial requirements for specialized packaging solutions. Pharmaceutical manufacturing growth, particularly in biotechnology and specialty drugs, drives demand for high-quality, contamination-free packaging systems.

Sustainability mandates increasingly influence purchasing decisions, with companies prioritizing packaging solutions that align with corporate environmental goals. European Union regulations on single-use plastics and packaging waste have accelerated adoption of reusable and recyclable rigid containers. Cost optimization initiatives drive interest in packaging solutions that reduce total cost of ownership through improved durability and reusability.

Supply chain efficiency requirements promote adoption of standardized packaging formats that integrate seamlessly with automated handling systems. The growth of e-commerce and direct-to-consumer distribution models creates new opportunities for specialized packaging solutions. Quality assurance demands in regulated industries necessitate packaging systems with enhanced traceability and contamination prevention capabilities.

Technological advancement in materials science enables development of lighter, stronger, and more chemically resistant packaging solutions. The integration of smart technologies provides additional value through improved inventory management and supply chain visibility.

High initial investment requirements for specialized rigid bulk packaging systems can deter adoption among smaller manufacturers and cost-sensitive applications. The substantial capital outlay for reusable container systems, while offering long-term benefits, presents cash flow challenges for companies with limited financial resources. Regulatory complexity across different European markets creates compliance challenges and increases operational costs for packaging manufacturers.

Material cost volatility affects pricing stability and profit margins, particularly for steel and polymer-based packaging solutions. Fluctuations in raw material prices can impact customer purchasing decisions and delay investment in new packaging systems. Transportation constraints related to container size and weight limitations affect market penetration in certain applications and geographical regions.

Competition from flexible packaging alternatives presents ongoing challenges, particularly in applications where rigid containers may be over-engineered for specific requirements. The growing popularity of bag-in-box and flexible intermediate bulk containers (FIBCs) in certain applications reduces demand for traditional rigid solutions. Environmental concerns regarding plastic packaging, despite recyclability improvements, continue to influence customer preferences and regulatory policies.

Economic uncertainty and potential recession risks can impact industrial production levels and reduce demand for bulk packaging solutions. Currency fluctuations within the European market affect international trade and pricing strategies for packaging manufacturers.

Circular economy initiatives present significant opportunities for innovative packaging solutions that support waste reduction and resource efficiency. The development of closed-loop recycling systems and take-back programs creates new revenue streams while addressing environmental concerns. Bio-based materials offer potential for differentiation and premium positioning in environmentally conscious market segments.

Digital integration opportunities include development of smart packaging solutions with embedded sensors, RFID tags, and IoT connectivity. These technologies enable real-time monitoring of product conditions, inventory tracking, and predictive maintenance capabilities. Customization services for specialized applications provide opportunities for higher margins and stronger customer relationships.

Emerging markets within Eastern Europe present growth opportunities as industrial development accelerates and regulatory standards align with Western European requirements. The expansion of pharmaceutical and chemical industries in these regions drives demand for high-quality packaging solutions. Export opportunities to developing markets outside Europe leverage the region’s reputation for quality and innovation.

Strategic partnerships with logistics providers and supply chain management companies create opportunities for integrated service offerings. The development of packaging-as-a-service models provides recurring revenue opportunities while reducing customer capital requirements. Acquisition opportunities of smaller specialized manufacturers enable market consolidation and technology acquisition.

Supply chain integration continues to reshape market dynamics, with packaging manufacturers increasingly collaborating with logistics providers and end-users to optimize total supply chain costs. This collaborative approach drives innovation in container design, standardization, and handling systems. Customer consolidation in key industries creates opportunities for strategic partnerships while intensifying competition for major accounts.

Technology convergence between packaging, logistics, and information systems enables new value propositions and service models. The integration of artificial intelligence and machine learning in supply chain optimization creates demand for smart packaging solutions with enhanced data collection capabilities. Sustainability reporting requirements drive demand for packaging solutions with verifiable environmental benefits and lifecycle tracking.

Market maturation in Western European markets shifts focus toward value-added services and technological differentiation rather than volume growth. This evolution favors companies with strong innovation capabilities and customer service excellence. Regulatory harmonization across European markets simplifies compliance requirements and enables more efficient market penetration strategies.

Economic resilience of the packaging industry during economic downturns demonstrates the essential nature of packaging solutions across industrial applications. However, cyclical demand patterns in key end-user industries require flexible manufacturing and inventory management strategies to maintain profitability.

Comprehensive market analysis employs multiple research methodologies to ensure accuracy and reliability of market insights. Primary research includes extensive interviews with industry executives, procurement managers, and technical specialists across various end-user industries. Secondary research encompasses analysis of company financial reports, industry publications, regulatory documents, and trade association data.

Data collection methods include structured surveys, focus group discussions, and expert panel consultations to gather quantitative and qualitative market information. Industry trade shows and conferences provide opportunities for direct market observation and trend identification. Statistical analysis employs advanced modeling techniques to project market trends and validate research findings.

Market segmentation analysis utilizes both top-down and bottom-up approaches to ensure comprehensive coverage of market dynamics. Regional analysis incorporates country-specific economic indicators, regulatory environments, and industrial development patterns. Competitive intelligence gathering includes analysis of patent filings, product launches, and strategic announcements from key market participants.

Quality assurance processes include data triangulation, expert validation, and peer review to ensure research accuracy and reliability. Regular updates and market monitoring provide ongoing insights into evolving market conditions and emerging trends.

Germany maintains its position as the largest European market for rigid bulk packaging, driven by the country’s substantial chemical and automotive industries. The region accounts for approximately 28% of total European demand, supported by major chemical complexes in the Rhine-Ruhr region and Bavaria. German manufacturers lead in technological innovation, particularly in sustainable packaging solutions and automation integration.

France represents the second-largest market, with strong demand from pharmaceutical, food processing, and chemical industries. The country’s focus on luxury goods and specialty chemicals drives demand for premium packaging solutions. French companies demonstrate particular strength in food-grade packaging and pharmaceutical applications, accounting for 18% of regional market share.

United Kingdom maintains significant market presence despite Brexit-related uncertainties, with robust demand from pharmaceutical and specialty chemical sectors. The country’s emphasis on sustainable packaging aligns with EU environmental directives, driving innovation in recyclable materials. UK market dynamics reflect approximately 12% of European demand.

Netherlands and Belgium benefit from strategic locations as European logistics hubs, generating substantial demand for bulk packaging solutions. The concentration of chemical production facilities and port operations drives consistent market growth. Benelux countries collectively represent approximately 15% of market demand.

Eastern European markets demonstrate the highest growth rates, with Poland, Czech Republic, and Hungary leading regional expansion. Industrial development and foreign investment drive increasing demand for quality packaging solutions, with growth rates exceeding 8% annually in key markets.

Market leadership is distributed among several multinational corporations with strong European presence and comprehensive product portfolios. The competitive environment balances global scale advantages with regional specialization and customer service excellence.

Competitive strategies emphasize technological innovation, sustainability leadership, and customer service excellence. Strategic acquisitions and partnerships enable market expansion and technology acquisition. Regional players maintain competitive positions through specialized applications and superior customer service in local markets.

By Material Type:

By Container Type:

By Application Industry:

Chemical Industry Applications continue to dominate market demand, driven by Europe’s substantial petrochemical and specialty chemical production capacity. This segment requires packaging solutions with superior chemical resistance, regulatory compliance, and safety features. Innovation focus includes development of lightweight yet durable containers that reduce transportation costs while maintaining product integrity.

Food and Beverage Packaging demonstrates strong growth potential, particularly in bulk ingredient handling and beverage concentrate applications. Stringent hygiene requirements drive demand for easy-to-clean containers with smooth surfaces and minimal contamination risk. Sustainability trends in this segment emphasize recyclable materials and reduced packaging waste.

Pharmaceutical Applications represent the highest-value segment, requiring specialized containers with validated cleaning procedures, traceability systems, and contamination prevention features. The growth of biotechnology and personalized medicine creates opportunities for smaller-volume, high-specification packaging solutions. Regulatory compliance remains paramount, with containers requiring extensive documentation and validation.

Agricultural Segment benefits from increasing mechanization and precision agriculture trends, driving demand for standardized containers compatible with automated handling systems. Seasonal demand patterns require flexible manufacturing and inventory management strategies to optimize capacity utilization and customer service levels.

Manufacturers benefit from economies of scale in production, standardized designs that reduce complexity, and opportunities for value-added services such as reconditioning and logistics support. The development of reusable container systems creates recurring revenue streams and stronger customer relationships. Innovation capabilities enable premium positioning and differentiation in competitive markets.

End-users realize significant benefits through reduced total cost of ownership, improved supply chain efficiency, and enhanced product safety. Standardized packaging formats enable automation integration and reduce handling costs. Sustainability benefits include reduced packaging waste, improved recyclability, and alignment with corporate environmental goals.

Logistics providers benefit from standardized container dimensions that optimize transportation efficiency and warehouse utilization. The durability of rigid packaging reduces damage rates and associated costs. Digital integration capabilities enhance inventory tracking and supply chain visibility.

Regulatory authorities benefit from improved traceability and compliance monitoring capabilities enabled by advanced packaging systems. Standardized designs facilitate regulatory approval processes and market surveillance activities. Environmental benefits support policy objectives related to waste reduction and circular economy implementation.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability Integration represents the most significant trend shaping market evolution, with manufacturers increasingly adopting bio-based materials, implementing closed-loop recycling systems, and developing packaging solutions with reduced environmental impact. Circular economy principles drive innovation in reusable container systems and take-back programs that create ongoing customer relationships.

Digital Transformation accelerates across the industry, with smart packaging solutions incorporating RFID tags, sensors, and IoT connectivity becoming mainstream. These technologies enable real-time monitoring of container conditions, inventory tracking, and predictive maintenance capabilities. Data analytics provide insights for supply chain optimization and customer service improvement.

Lightweighting Initiatives focus on reducing container weight while maintaining structural integrity and performance characteristics. Advanced materials and design optimization techniques enable significant weight reductions that lower transportation costs and environmental impact. Material innovation includes development of high-strength polymers and composite materials with enhanced properties.

Customization Demand increases as customers seek packaging solutions tailored to specific applications and operational requirements. Modular design approaches enable cost-effective customization while maintaining manufacturing efficiency. Service integration includes comprehensive logistics support, reconditioning services, and supply chain management capabilities.

Strategic acquisitions continue to reshape the competitive landscape, with major players acquiring specialized manufacturers to expand technological capabilities and market reach. Recent consolidation activities focus on sustainability technologies and digital integration capabilities. Partnership agreements between packaging manufacturers and logistics providers create integrated service offerings.

Manufacturing investments in Eastern European markets reflect growing demand and cost optimization strategies. New production facilities incorporate advanced automation and sustainability features to meet evolving market requirements. Technology licensing agreements enable rapid deployment of innovative packaging solutions across multiple markets.

Regulatory developments include implementation of extended producer responsibility schemes and updated packaging waste directives that influence product development strategies. Industry standards evolution addresses emerging applications and technological capabilities, ensuring safety and compatibility across supply chains.

Research collaborations between packaging manufacturers, material suppliers, and academic institutions accelerate innovation in sustainable materials and smart packaging technologies. Pilot programs demonstrate new packaging concepts and validate commercial viability before full-scale market introduction.

Strategic focus should prioritize sustainability leadership and digital integration capabilities to capture emerging market opportunities. Companies should invest in research and development of bio-based materials and smart packaging technologies to differentiate their offerings. Market expansion into Eastern European markets presents attractive growth opportunities with favorable risk-return profiles.

Operational excellence initiatives should emphasize manufacturing efficiency, quality consistency, and customer service capabilities. Implementation of lean manufacturing principles and automation technologies can improve cost competitiveness while maintaining quality standards. Supply chain optimization through strategic partnerships and vertical integration can enhance market position.

Customer relationship management should evolve toward comprehensive service offerings that address total cost of ownership rather than unit price competition. Development of packaging-as-a-service models can create recurring revenue streams and stronger customer loyalty. Technical support capabilities should expand to include supply chain consulting and optimization services.

According to MarkWide Research analysis, companies that successfully integrate sustainability initiatives with digital technologies while maintaining operational excellence will achieve superior market performance and customer satisfaction levels.

Market evolution toward sustainable and intelligent packaging solutions will accelerate over the next decade, driven by regulatory requirements and customer preferences. The integration of circular economy principles will become standard practice, with closed-loop recycling systems and reusable container programs expanding significantly. Growth projections indicate continued expansion at approximately 5.8% CAGR through 2030.

Technological advancement will focus on smart packaging capabilities, with IoT integration becoming standard for high-value applications. Artificial intelligence and machine learning will optimize supply chain operations and predictive maintenance programs. Material innovation will emphasize bio-based alternatives and advanced composites with enhanced performance characteristics.

Regional dynamics will shift toward Eastern European markets, which are expected to demonstrate the highest growth rates as industrial development accelerates. Western European markets will focus on value-added services and premium applications. Market consolidation will continue, with strategic acquisitions enabling technology acquisition and market expansion.

Industry transformation toward service-oriented business models will create new revenue opportunities and customer relationships. The development of comprehensive supply chain solutions will differentiate leading companies from commodity suppliers. MWR projects that successful companies will achieve 15-20% higher profitability through value-added service offerings compared to traditional manufacturing-focused approaches.

The Europe rigid bulk packaging market stands at a pivotal juncture, balancing mature market dynamics with emerging opportunities in sustainability and digital integration. The sector’s resilience during economic uncertainties demonstrates its essential role in European industrial operations, while evolving customer requirements drive continuous innovation and market evolution.

Strategic success in this market requires a comprehensive approach that combines operational excellence with technological innovation and sustainability leadership. Companies that successfully navigate the transition toward circular economy principles while embracing digital transformation will capture the most attractive growth opportunities. The integration of smart packaging technologies and service-oriented business models will differentiate market leaders from traditional commodity suppliers.

Future market dynamics will be shaped by regulatory evolution, technological advancement, and changing customer expectations. The emphasis on total cost of ownership and supply chain optimization creates opportunities for companies that can deliver comprehensive solutions beyond basic packaging products. Regional expansion into Eastern European markets, combined with value-added services in mature Western markets, provides balanced growth strategies for industry participants.

Long-term outlook remains positive, supported by essential industrial applications, sustainability trends, and technological innovation. The market’s evolution toward intelligent, sustainable packaging solutions positions it well for continued growth and value creation across the European industrial landscape.

What is Rigid Bulk Packaging?

Rigid bulk packaging refers to containers that are designed to hold large quantities of products, typically in solid or liquid form. These containers are made from materials such as plastic, metal, or glass and are used across various industries for storage and transportation.

What are the key players in the Europe Rigid Bulk Packaging Market?

Key players in the Europe Rigid Bulk Packaging Market include companies like Schütz GmbH & Co. KGaA, Mauser Group, and Greif, Inc. These companies are known for their innovative packaging solutions and extensive distribution networks, among others.

What are the main drivers of the Europe Rigid Bulk Packaging Market?

The main drivers of the Europe Rigid Bulk Packaging Market include the increasing demand for efficient and sustainable packaging solutions, the growth of the food and beverage industry, and the rising need for safe transportation of hazardous materials.

What challenges does the Europe Rigid Bulk Packaging Market face?

Challenges in the Europe Rigid Bulk Packaging Market include stringent regulations regarding packaging materials, competition from alternative packaging solutions, and fluctuations in raw material prices, which can impact production costs.

What opportunities exist in the Europe Rigid Bulk Packaging Market?

Opportunities in the Europe Rigid Bulk Packaging Market include the growing trend towards eco-friendly packaging solutions, advancements in packaging technology, and the expansion of e-commerce, which increases the demand for bulk packaging.

What trends are shaping the Europe Rigid Bulk Packaging Market?

Trends shaping the Europe Rigid Bulk Packaging Market include the adoption of smart packaging technologies, increased focus on recyclability and sustainability, and the rise of customized packaging solutions to meet specific industry needs.

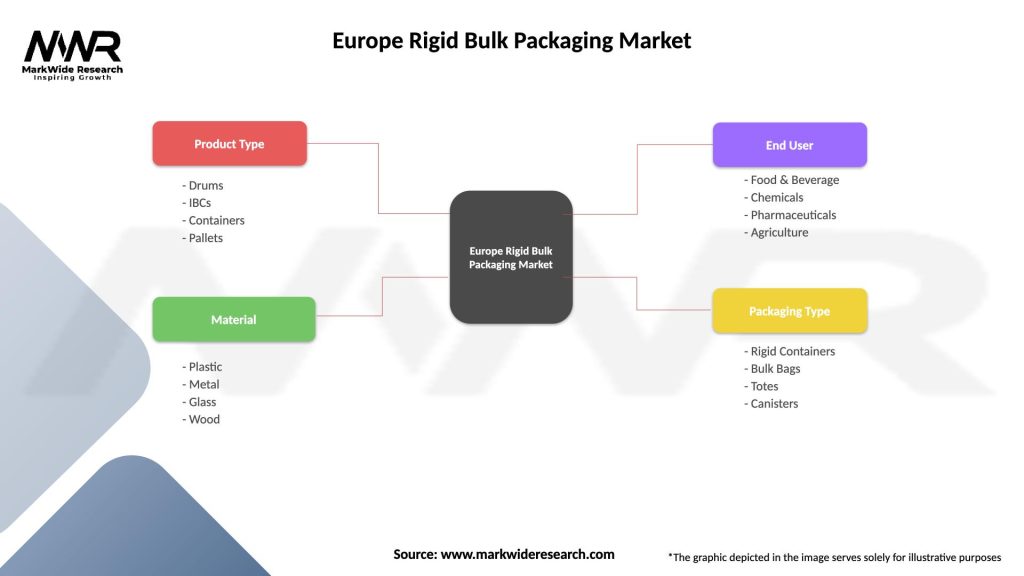

Europe Rigid Bulk Packaging Market

| Segmentation Details | Description |

|---|---|

| Product Type | Drums, IBCs, Containers, Pallets |

| Material | Plastic, Metal, Glass, Wood |

| End User | Food & Beverage, Chemicals, Pharmaceuticals, Agriculture |

| Packaging Type | Rigid Containers, Bulk Bags, Totes, Canisters |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Rigid Bulk Packaging Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.