444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe non-dairy yogurt market represents a dynamic and rapidly expanding segment within the broader plant-based food industry. Consumer preferences are shifting dramatically toward healthier, sustainable alternatives to traditional dairy products, with non-dairy yogurt emerging as a leading category. The market encompasses various plant-based alternatives including almond, coconut, soy, oat, and cashew-based yogurt products that cater to diverse dietary requirements and taste preferences.

Market growth is being driven by increasing lactose intolerance awareness, rising veganism, environmental consciousness, and growing health awareness among European consumers. The region’s sophisticated retail infrastructure and strong consumer purchasing power create favorable conditions for premium non-dairy yogurt products. Innovation in flavors, textures, and nutritional profiles continues to attract both health-conscious consumers and those seeking indulgent alternatives to dairy yogurt.

Regional dynamics vary significantly across European markets, with Nordic countries and Germany leading in adoption rates, while Southern European markets show increasing acceptance. The market demonstrates robust growth potential with annual growth rates exceeding 12% in several key segments, particularly in organic and probiotic-enhanced varieties.

The Europe non-dairy yogurt market refers to the commercial ecosystem encompassing the production, distribution, and consumption of plant-based yogurt alternatives across European countries. These products are manufactured using various plant-based ingredients such as nuts, seeds, grains, and legumes, processed to achieve yogurt-like consistency and taste profiles while providing nutritional benefits without dairy components.

Non-dairy yogurt products serve multiple consumer segments including lactose-intolerant individuals, vegans, health-conscious consumers, and environmentally aware buyers seeking sustainable food options. The market includes both established multinational brands and emerging local producers offering innovative formulations, flavors, and packaging solutions tailored to European consumer preferences.

Market scope encompasses retail channels including supermarkets, health food stores, online platforms, and specialty organic retailers. The category continues evolving with technological advancements in fermentation processes, texture enhancement, and nutritional fortification to closely mimic traditional dairy yogurt characteristics while offering unique plant-based benefits.

Europe’s non-dairy yogurt market demonstrates exceptional growth momentum driven by fundamental shifts in consumer behavior and dietary preferences. The market benefits from increasing awareness of plant-based nutrition, environmental sustainability concerns, and rising incidence of dairy allergies and intolerances across European populations. Product innovation remains at the forefront, with manufacturers developing sophisticated formulations that deliver superior taste, texture, and nutritional profiles.

Key market drivers include the expanding vegan population, which has grown by approximately 25% over the past three years in major European markets. Health consciousness continues rising, with over 40% of consumers actively seeking products with reduced sugar content and enhanced protein profiles. Sustainability concerns influence purchasing decisions, with environmentally conscious consumers representing a significant and growing market segment.

Competitive landscape features both established dairy companies diversifying into plant-based alternatives and specialized non-dairy brands gaining market share through innovation and targeted marketing. The market shows strong potential for continued expansion, supported by favorable regulatory environments, increasing retail availability, and growing consumer acceptance of plant-based alternatives across diverse European demographics.

Consumer behavior analysis reveals significant insights driving market evolution. European consumers increasingly prioritize health benefits, with probiotic-enhanced non-dairy yogurts gaining particular traction among health-conscious demographics. Flavor preferences vary by region, with berry and vanilla varieties leading in Northern Europe while Mediterranean flavors show growing popularity in Southern markets.

Health consciousness serves as the primary driver propelling market growth across European regions. Increasing awareness of lactose intolerance, affecting approximately 65% of the global adult population, creates substantial demand for dairy alternatives. Digestive health benefits associated with plant-based yogurts, particularly those containing live cultures and probiotics, attract health-focused consumers seeking functional food options.

Environmental sustainability concerns significantly influence purchasing decisions, with consumers increasingly aware of dairy farming’s environmental impact. Plant-based alternatives offer reduced carbon footprints, lower water usage, and decreased land requirements, appealing to environmentally conscious European consumers. Ethical considerations regarding animal welfare further drive adoption among consumers seeking cruelty-free food options.

Dietary trend adoption including veganism, vegetarianism, and flexitarian lifestyles continues expanding across European markets. The growing popularity of plant-based diets, supported by celebrity endorsements and social media influence, creates favorable conditions for non-dairy yogurt acceptance. Nutritional advantages such as lower saturated fat content, absence of cholesterol, and enhanced fiber content appeal to health-conscious demographics seeking balanced nutrition options.

Price sensitivity remains a significant barrier to widespread adoption, with non-dairy yogurts typically commanding premium prices compared to conventional dairy alternatives. Cost considerations particularly impact price-conscious consumers and families with limited disposable income, potentially limiting market penetration in certain demographic segments. Manufacturing complexities and specialized ingredients contribute to higher production costs, translating to elevated retail prices.

Taste and texture challenges continue affecting consumer acceptance, despite significant improvements in product formulations. Some consumers remain dissatisfied with the mouthfeel, consistency, or flavor profiles of plant-based alternatives compared to traditional dairy yogurt. Sensory expectations established through lifelong dairy consumption create high standards for alternative products to meet or exceed.

Limited shelf life and storage requirements pose logistical challenges for retailers and consumers. Many non-dairy yogurts require refrigeration and have shorter expiration dates than conventional alternatives, potentially limiting distribution efficiency and consumer convenience. Supply chain complexities associated with sourcing quality plant-based ingredients and maintaining product freshness create operational challenges for manufacturers and retailers.

Product innovation presents substantial opportunities for market expansion through development of enhanced formulations, novel flavors, and improved nutritional profiles. Technological advances in fermentation processes, protein enhancement, and texture optimization enable manufacturers to create products more closely resembling traditional dairy yogurt while offering unique plant-based benefits.

Emerging markets within Eastern Europe offer significant growth potential as consumer awareness increases and retail infrastructure develops. Market penetration opportunities exist in traditionally dairy-focused regions where non-dairy alternatives remain underrepresented. Educational marketing campaigns highlighting health benefits and environmental advantages can drive adoption in these developing markets.

Channel diversification through online retail, subscription services, and direct-to-consumer models creates new revenue streams and customer engagement opportunities. Partnership opportunities with fitness centers, health clinics, and wellness programs can expand market reach to targeted consumer segments. Collaboration with foodservice providers and restaurants enables product integration into dining experiences, increasing consumer exposure and trial opportunities.

Supply chain evolution reflects the market’s maturation, with ingredient suppliers developing specialized plant-based components optimized for yogurt production. Manufacturing capabilities continue advancing through investment in specialized equipment and processing technologies designed specifically for non-dairy applications. Quality control standards and regulatory compliance requirements drive operational improvements across the production ecosystem.

Consumer education plays a crucial role in market development, with brands investing significantly in marketing campaigns highlighting nutritional benefits, environmental advantages, and taste improvements. Retail partnerships facilitate product placement and promotional activities that increase consumer awareness and trial rates. In-store demonstrations and sampling programs prove effective in converting curious consumers to regular purchasers.

Competitive intensity increases as both established dairy companies and specialized plant-based brands compete for market share. Innovation cycles accelerate with companies racing to develop superior formulations, unique flavors, and enhanced nutritional profiles. Strategic acquisitions and partnerships reshape the competitive landscape as larger corporations seek to establish or strengthen their plant-based portfolios.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the Europe non-dairy yogurt market. Primary research includes extensive consumer surveys, industry expert interviews, and retailer feedback collection across major European markets. Focus groups and taste-testing sessions provide qualitative insights into consumer preferences, purchasing behaviors, and product satisfaction levels.

Secondary research encompasses analysis of industry reports, regulatory filings, company financial statements, and trade association data. Market monitoring includes tracking of product launches, pricing trends, promotional activities, and distribution channel developments across European markets. Competitive intelligence gathering focuses on brand positioning, marketing strategies, and innovation pipelines of key market participants.

Data validation processes ensure information accuracy through cross-referencing multiple sources and expert verification. Statistical analysis employs advanced modeling techniques to identify trends, correlations, and growth patterns within the market data. Regular updates and continuous monitoring maintain research relevance and accuracy as market conditions evolve rapidly in this dynamic sector.

Northern European markets including Germany, Netherlands, and Scandinavian countries lead in non-dairy yogurt adoption rates, with market penetration exceeding 15% in urban areas. Consumer sophistication in these regions drives demand for premium, organic, and artisanal varieties. Strong environmental consciousness and high disposable incomes support market growth, with consumers willing to pay premium prices for sustainable alternatives.

Western European markets including France, United Kingdom, and Belgium demonstrate steady growth with increasing retail availability and consumer acceptance. Market development varies by country, with the UK showing particularly strong growth following increased health awareness campaigns. French consumers show growing interest in organic and locally-sourced varieties, while Belgian markets favor chocolate and dessert-inspired flavors.

Southern European markets including Italy, Spain, and Portugal represent emerging opportunities with growth rates approaching 18% annually in key segments. Traditional dairy cultures in these regions initially created resistance, but younger demographics increasingly embrace plant-based alternatives. Mediterranean flavor profiles and locally-sourced ingredients appeal to regional taste preferences and cultural values.

Eastern European markets show developing potential with increasing urbanization, rising incomes, and growing health consciousness. Market entry strategies focus on education and gradual introduction through premium retail channels. Consumer acceptance grows steadily as product availability increases and prices become more competitive with traditional dairy alternatives.

Market leadership features a diverse mix of established multinational corporations and innovative plant-based specialists competing across different segments and price points. Brand positioning strategies vary from health-focused messaging to environmental sustainability and taste superiority claims.

Competitive strategies emphasize product innovation, sustainable sourcing, and targeted marketing to specific consumer segments. Market consolidation trends include acquisitions of smaller innovative brands by larger corporations seeking to strengthen their plant-based portfolios and market presence.

By Base Ingredient: The market segments into distinct categories based on primary plant-based components used in production. Almond-based yogurts lead in premium segments, offering creamy texture and neutral flavor profiles. Coconut-based varieties provide rich, indulgent options popular in dessert categories. Soy-based products offer high protein content appealing to fitness-conscious consumers, while oat-based alternatives provide sustainable, locally-sourced options with growing popularity.

By Distribution Channel: Retail segmentation reflects diverse consumer shopping preferences and accessibility requirements. Supermarket chains dominate sales volume with approximately 60% market share, providing mainstream accessibility and competitive pricing. Health food stores cater to specialized consumer segments seeking organic and premium varieties. Online channels show rapid growth, particularly among younger demographics and subscription-based purchasing models.

By Product Type: Functional segmentation addresses specific consumer needs and usage occasions. Plain varieties serve as versatile bases for customization and cooking applications. Flavored options include fruit, vanilla, and dessert-inspired varieties targeting indulgent consumption. Probiotic-enhanced products appeal to health-conscious consumers seeking digestive benefits, while protein-fortified varieties target fitness and nutrition-focused segments.

Organic segment demonstrates exceptional growth potential with annual growth rates exceeding 20% in several European markets. Premium positioning allows organic varieties to command higher margins while appealing to health-conscious and environmentally aware consumers. Certification requirements and supply chain complexities create barriers to entry, benefiting established organic brands with proven sourcing capabilities.

Probiotic category represents the fastest-growing functional segment, driven by increasing awareness of gut health benefits. Scientific research supporting probiotic benefits creates marketing opportunities and justifies premium pricing. Product development focuses on strain selection, viability maintenance, and flavor masking to deliver effective probiotic benefits without compromising taste.

Protein-enhanced varieties target fitness enthusiasts and health-conscious consumers seeking nutritional optimization. Plant-based protein sources including pea, hemp, and rice proteins enable manufacturers to create high-protein formulations comparable to Greek yogurt. Marketing emphasizes muscle building, satiety, and meal replacement benefits to differentiate from standard varieties.

Dessert-inspired flavors expand market appeal beyond health-focused consumers to include indulgence-seeking demographics. Innovation opportunities include seasonal flavors, limited editions, and collaboration with popular dessert brands. Premium ingredients and artisanal positioning justify higher price points while creating differentiation in crowded market segments.

Manufacturers benefit from expanding market opportunities, premium pricing potential, and brand differentiation possibilities within the growing plant-based sector. Innovation capabilities enable development of unique formulations and flavors that command higher margins than commodity dairy products. Sustainability positioning appeals to environmentally conscious consumers and supports corporate social responsibility initiatives.

Retailers gain from higher margin products, increased customer traffic, and enhanced brand positioning as health and sustainability advocates. Category growth drives incremental sales and basket size increases as consumers explore plant-based alternatives. Premium product positioning supports overall store profitability while attracting affluent, health-conscious customer segments.

Consumers receive diverse nutritional benefits including reduced saturated fat, increased fiber, and elimination of dairy allergens and lactose. Environmental benefits include reduced carbon footprint and water usage compared to traditional dairy production. Flavor variety and innovation provide exciting alternatives to conventional yogurt while supporting personal health and ethical values.

Supply chain partners including ingredient suppliers, packaging companies, and logistics providers benefit from growing demand and premium product positioning. Specialized requirements for plant-based ingredients and sustainable packaging create opportunities for differentiation and value-added services. Long-term growth prospects support investment in specialized capabilities and infrastructure development.

Strengths:

Weaknesses:

Opportunities:

Threats:

Functional enhancement emerges as a dominant trend with manufacturers incorporating probiotics, prebiotics, vitamins, and minerals to create health-focused formulations. Personalized nutrition concepts drive development of targeted products for specific health conditions, age groups, and lifestyle requirements. Advanced fermentation techniques enable creation of products with enhanced bioavailability and digestive benefits.

Sustainable packaging initiatives gain momentum as brands respond to environmental concerns and regulatory pressures. Circular economy principles influence packaging design with emphasis on recyclability, compostability, and reduced material usage. Innovative packaging solutions including edible films and plant-based containers create differentiation opportunities while supporting sustainability goals.

Flavor innovation expands beyond traditional profiles to include exotic fruits, spices, and cultural fusion concepts. Seasonal offerings and limited-edition flavors create excitement and encourage trial among existing customers. Collaboration with celebrity chefs and food influencers drives flavor development and marketing initiatives targeting younger demographics.

Technology integration includes smart packaging with freshness indicators, QR codes linking to nutritional information, and augmented reality experiences. Direct-to-consumer models leverage technology for subscription services, personalized recommendations, and customer engagement platforms. Data analytics enable better understanding of consumer preferences and purchasing patterns for targeted marketing initiatives.

Strategic acquisitions reshape the competitive landscape as major food corporations acquire innovative plant-based brands to strengthen their alternative protein portfolios. MarkWide Research analysis indicates increasing consolidation activity with over 30% of major deals involving non-dairy yogurt companies in recent years. These transactions provide smaller brands with distribution capabilities while offering larger corporations access to innovation and specialized expertise.

Manufacturing investments include construction of dedicated plant-based production facilities and conversion of existing dairy plants to accommodate alternative products. Capacity expansion reflects growing demand and enables economies of scale that support competitive pricing. Advanced processing equipment specifically designed for plant-based applications improves product quality and production efficiency.

Regulatory developments include updated labeling requirements, health claim approvals, and sustainability certification programs. European Union initiatives supporting sustainable food systems create favorable conditions for plant-based product development and marketing. Standardization of nutritional labeling helps consumers make informed comparisons between dairy and non-dairy alternatives.

Research partnerships between manufacturers and academic institutions advance understanding of plant-based nutrition, fermentation processes, and consumer preferences. Innovation collaborations accelerate product development timelines and enable access to cutting-edge technologies and scientific expertise. Clinical studies supporting health benefits provide marketing advantages and regulatory approval opportunities.

Product differentiation remains critical for success in the increasingly competitive market environment. MWR analysts recommend focusing on unique value propositions such as superior taste, enhanced nutrition, or sustainable sourcing to justify premium pricing and build brand loyalty. Innovation in texture, flavor, and functional benefits creates competitive advantages that are difficult for competitors to replicate quickly.

Market education initiatives should address consumer misconceptions about plant-based nutrition and highlight specific benefits compared to dairy alternatives. Targeted marketing campaigns focusing on taste, health benefits, and environmental impact can accelerate consumer adoption and trial rates. Partnerships with health professionals and nutritionists provide credible endorsements that influence purchasing decisions.

Distribution strategy optimization includes balancing premium positioning with accessibility through mainstream retail channels. Channel diversification reduces dependency on single distribution partners while maximizing market reach across different consumer segments. Online presence and direct-to-consumer capabilities become increasingly important for customer engagement and data collection.

Supply chain resilience requires diversification of ingredient sources and development of long-term supplier relationships. Vertical integration opportunities in key ingredients or packaging materials can provide cost advantages and quality control benefits. Investment in sustainable sourcing practices supports brand positioning while ensuring long-term ingredient availability.

Market expansion is projected to continue at robust rates with compound annual growth rates exceeding 15% expected across major European markets over the next five years. Consumer acceptance will broaden as product quality improvements and increased availability drive trial and repeat purchase behavior. Generational shifts toward plant-based eating patterns support long-term growth sustainability.

Technology advancement will enable significant improvements in taste, texture, and nutritional profiles, addressing current barriers to widespread adoption. Fermentation innovations and protein enhancement techniques will create products increasingly comparable to dairy yogurt while offering unique plant-based benefits. Artificial intelligence and machine learning applications will optimize formulations and predict consumer preferences.

Market maturation will bring increased competition, pricing pressure, and consolidation among smaller players. Successful brands will differentiate through innovation, sustainability credentials, and strong consumer relationships. Premium segments will continue growing as consumers prioritize quality and health benefits over price considerations.

Regulatory evolution will likely include enhanced sustainability reporting requirements and potential carbon pricing mechanisms that favor plant-based alternatives. Health claim approvals for specific probiotic strains and nutritional benefits will create marketing advantages for scientifically-backed products. International trade agreements may facilitate ingredient sourcing and market expansion opportunities.

Europe’s non-dairy yogurt market represents a compelling growth opportunity driven by fundamental shifts in consumer preferences toward healthier, more sustainable food choices. The market demonstrates strong momentum across multiple dimensions including product innovation, retail expansion, and consumer acceptance. Key success factors include superior product quality, effective marketing, and strategic distribution partnerships that maximize market reach and consumer accessibility.

Industry participants who invest in research and development, sustainable sourcing, and consumer education will be best positioned to capitalize on the significant growth opportunities ahead. The market’s evolution from niche health food category to mainstream consumer staple creates substantial value creation potential for stakeholders across the entire value chain. Long-term prospects remain highly favorable as demographic trends, environmental concerns, and health consciousness continue supporting plant-based food adoption throughout European markets.

What is Non-dairy Yogurt?

Non-dairy yogurt is a plant-based alternative to traditional yogurt, made from ingredients such as almond, coconut, soy, or oat milk. It is often fortified with probiotics and can be used in similar applications as dairy yogurt, including smoothies, desserts, and breakfast bowls.

What are the key players in the Europe Non-dairy Yogurt Market?

Key players in the Europe Non-dairy Yogurt Market include Alpro, Oatly, and Danone, which offer a variety of plant-based yogurt products. These companies are focusing on innovation and expanding their product lines to cater to the growing demand for non-dairy alternatives among consumers.

What are the growth factors driving the Europe Non-dairy Yogurt Market?

The Europe Non-dairy Yogurt Market is driven by increasing health consciousness among consumers, a rise in lactose intolerance, and the growing trend of veganism. Additionally, the demand for clean-label products and sustainable food options is contributing to market growth.

What challenges does the Europe Non-dairy Yogurt Market face?

Challenges in the Europe Non-dairy Yogurt Market include competition from traditional dairy products and the perception of taste and texture differences. Additionally, the higher cost of production for plant-based ingredients can limit market penetration.

What opportunities exist in the Europe Non-dairy Yogurt Market?

Opportunities in the Europe Non-dairy Yogurt Market include the potential for product innovation, such as new flavors and formulations, and the expansion into emerging markets. There is also a growing interest in functional foods that offer health benefits, which can be leveraged by brands.

What trends are shaping the Europe Non-dairy Yogurt Market?

Trends in the Europe Non-dairy Yogurt Market include the rise of organic and non-GMO products, as well as the incorporation of superfoods like chia seeds and probiotics. Additionally, there is an increasing focus on sustainable packaging and environmentally friendly production methods.

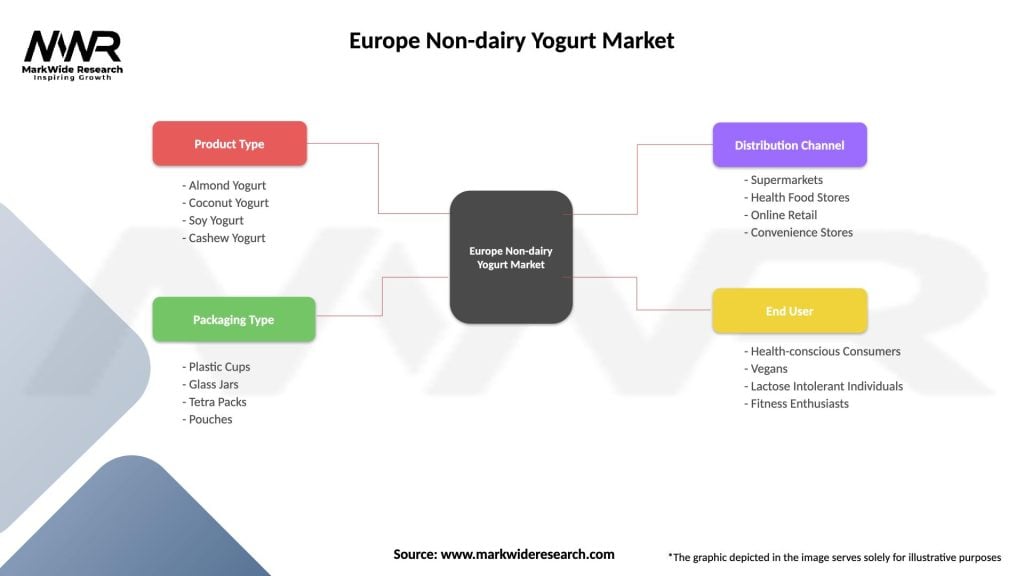

Europe Non-dairy Yogurt Market

| Segmentation Details | Description |

|---|---|

| Product Type | Almond Yogurt, Coconut Yogurt, Soy Yogurt, Cashew Yogurt |

| Packaging Type | Plastic Cups, Glass Jars, Tetra Packs, Pouches |

| Distribution Channel | Supermarkets, Health Food Stores, Online Retail, Convenience Stores |

| End User | Health-conscious Consumers, Vegans, Lactose Intolerant Individuals, Fitness Enthusiasts |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Non-dairy Yogurt Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.