444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe Healthcare Information Technology (IT) market represents a rapidly evolving landscape that encompasses comprehensive digital solutions designed to enhance healthcare delivery, improve patient outcomes, and streamline operational efficiency across European healthcare systems. This dynamic market includes electronic health records (EHR), hospital information systems, telemedicine platforms, healthcare analytics, and mobile health applications that are transforming how medical professionals deliver care and manage patient data.

Market dynamics indicate substantial growth driven by increasing digitization initiatives, government mandates for electronic health record adoption, and the rising demand for integrated healthcare solutions. The market demonstrates robust expansion with healthcare providers increasingly investing in advanced IT infrastructure to meet evolving patient expectations and regulatory requirements. European countries are leading global healthcare digitization efforts, with significant adoption rates of approximately 78% for EHR systems across major healthcare institutions.

Technological advancement continues to reshape the healthcare IT landscape, with artificial intelligence, machine learning, and cloud-based solutions gaining prominence. The market encompasses diverse segments including clinical information systems, administrative systems, and patient engagement platforms, each contributing to the overall digital transformation of European healthcare. Integration capabilities and interoperability remain critical factors driving market growth, as healthcare organizations seek comprehensive solutions that can seamlessly connect various healthcare processes and stakeholders.

The Europe Healthcare Information Technology (IT) market refers to the comprehensive ecosystem of digital technologies, software solutions, and IT infrastructure specifically designed to support healthcare delivery, management, and administration across European healthcare systems. This market encompasses all technology-enabled solutions that facilitate patient care, clinical decision-making, administrative processes, and healthcare data management within hospitals, clinics, and other healthcare facilities throughout Europe.

Healthcare IT solutions include electronic health records, hospital management systems, telemedicine platforms, medical imaging systems, healthcare analytics tools, and mobile health applications. These technologies enable healthcare providers to digitize patient information, streamline clinical workflows, enhance communication between healthcare professionals, and improve overall healthcare quality and accessibility. The market represents the intersection of healthcare expertise and information technology innovation, creating solutions that address specific European healthcare challenges and regulatory requirements.

Market leadership in European healthcare IT is characterized by strong government support, comprehensive digital health strategies, and increasing private sector investment in healthcare technology solutions. The market demonstrates exceptional growth potential driven by aging populations, chronic disease management needs, and the ongoing digital transformation of healthcare systems across European Union member states and associated countries.

Key market drivers include regulatory mandates for electronic health record adoption, increasing healthcare costs requiring efficiency improvements, and growing patient expectations for digital health services. The market benefits from substantial government funding with healthcare IT investments representing approximately 12% of total healthcare budgets across major European countries. Cloud adoption rates in healthcare IT have reached 65% among European healthcare providers, indicating strong momentum toward scalable, flexible technology solutions.

Competitive dynamics feature a mix of global technology leaders, specialized healthcare IT vendors, and emerging startups focusing on innovative healthcare solutions. The market landscape includes established players offering comprehensive healthcare IT suites alongside niche providers delivering specialized solutions for specific healthcare segments. Market consolidation continues as larger vendors acquire innovative startups to expand their healthcare IT portfolios and enhance their competitive positioning.

Strategic insights reveal several critical factors shaping the European healthcare IT market landscape:

Government initiatives represent the primary catalyst for healthcare IT market growth across Europe. National digital health strategies, substantial public funding for healthcare digitization, and regulatory mandates for electronic health record adoption create a supportive environment for healthcare IT expansion. European Union directives promoting cross-border healthcare data exchange and interoperability standards further accelerate market development.

Demographic pressures from aging populations and increasing chronic disease prevalence drive demand for efficient healthcare IT solutions. Healthcare providers require advanced technology platforms to manage growing patient volumes while maintaining quality care standards. Cost containment pressures motivate healthcare organizations to invest in IT solutions that improve operational efficiency and reduce administrative overhead.

Patient expectations for digital health services continue rising, with consumers demanding convenient access to healthcare information, appointment scheduling, and telemedicine consultations. The COVID-19 pandemic significantly accelerated digital health adoption, with telemedicine utilization rates increasing by 340% during peak pandemic periods. Healthcare workforce shortages across Europe create additional demand for IT solutions that enhance productivity and support clinical decision-making.

Implementation challenges pose significant barriers to healthcare IT adoption, particularly for smaller healthcare providers with limited technical resources and budget constraints. Complex integration requirements, lengthy implementation timelines, and the need for extensive staff training create obstacles for healthcare organizations considering IT system upgrades or replacements.

Cybersecurity concerns represent a major restraint as healthcare organizations face increasing cyber threats targeting sensitive patient data. High-profile data breaches and ransomware attacks on healthcare systems create hesitation among providers considering cloud-based solutions or increased digital connectivity. Regulatory compliance complexity adds additional layers of requirements that healthcare IT solutions must address, potentially increasing costs and implementation complexity.

Interoperability challenges between different healthcare IT systems limit the effectiveness of digital health initiatives. Legacy system integration difficulties and varying data standards across different vendors create technical barriers that healthcare organizations must overcome. Change management resistance from healthcare professionals accustomed to traditional workflows can slow adoption of new healthcare IT solutions.

Artificial intelligence integration presents substantial opportunities for healthcare IT vendors to develop advanced clinical decision support systems, predictive analytics platforms, and automated administrative processes. AI adoption rates in European healthcare are projected to reach 45% by 2027, creating significant market potential for innovative AI-powered healthcare solutions.

Telemedicine expansion offers opportunities for comprehensive virtual care platforms that integrate with existing healthcare IT infrastructure. Rural healthcare delivery, specialist consultations, and chronic disease management represent key application areas for telemedicine solutions. Mobile health applications present opportunities for patient engagement platforms that connect with healthcare provider systems.

Data analytics services represent growing opportunities as healthcare organizations seek insights from their digital health data. Population health management, clinical outcome improvement, and operational optimization create demand for advanced analytics capabilities. Cybersecurity solutions specifically designed for healthcare environments offer opportunities for specialized security vendors to address unique healthcare IT protection requirements.

Competitive intensity in the European healthcare IT market continues increasing as established technology companies expand their healthcare portfolios while specialized healthcare IT vendors enhance their solution capabilities. Market fragmentation creates opportunities for both large integrated solution providers and niche specialists focusing on specific healthcare IT segments.

Technology convergence drives market dynamics as traditional healthcare IT boundaries blur with the integration of artificial intelligence, Internet of Things devices, and advanced analytics capabilities. Cloud adoption acceleration reshapes vendor strategies and customer procurement approaches, with hybrid cloud implementations representing 52% of new healthcare IT deployments.

Partnership strategies become increasingly important as healthcare IT vendors collaborate with healthcare providers, technology companies, and research institutions to develop innovative solutions. Merger and acquisition activity continues consolidating the market as larger vendors acquire specialized capabilities and expand their geographic presence across European markets.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the European healthcare IT market. Primary research includes extensive interviews with healthcare IT executives, healthcare provider decision-makers, and industry experts across major European countries to gather firsthand insights into market trends, challenges, and opportunities.

Secondary research encompasses analysis of government healthcare digitization reports, industry publications, company financial statements, and regulatory documentation to understand market structure and competitive dynamics. Quantitative analysis utilizes statistical modeling and trend analysis to project market growth patterns and identify key performance indicators.

Market segmentation analysis examines healthcare IT adoption patterns across different healthcare provider types, geographic regions, and technology categories. Competitive landscape assessment evaluates vendor market positioning, solution capabilities, and strategic initiatives to provide comprehensive market intelligence for stakeholders seeking to understand the European healthcare IT market dynamics.

Western Europe dominates the healthcare IT market with advanced digital health infrastructure, substantial government investment, and high healthcare IT adoption rates. Germany leads regional healthcare IT spending, representing approximately 28% of total European healthcare IT investments, driven by comprehensive electronic health record mandates and digital health strategy implementation.

United Kingdom maintains strong healthcare IT market presence despite Brexit implications, with the National Health Service driving significant digital transformation initiatives. France demonstrates robust growth in healthcare IT adoption, particularly in hospital information systems and telemedicine platforms. Nordic countries including Sweden, Denmark, and Norway showcase advanced healthcare digitization with high electronic health record adoption rates exceeding 85% among healthcare providers.

Southern Europe shows accelerating healthcare IT adoption with Italy and Spain implementing comprehensive digital health strategies supported by European Union funding. Eastern Europe represents emerging opportunities with countries like Poland and Czech Republic investing heavily in healthcare IT infrastructure modernization. Regional market share distribution shows Western Europe accounting for 72% of healthcare IT adoption, while Eastern Europe demonstrates the highest growth rates in new healthcare IT implementations.

Market leadership features a diverse ecosystem of global technology companies, specialized healthcare IT vendors, and emerging innovative startups. Leading market participants include:

Competitive strategies emphasize solution integration, interoperability capabilities, and specialized healthcare vertical expertise. Innovation focus centers on artificial intelligence integration, cloud-native architectures, and patient engagement platforms that differentiate vendor offerings in the competitive European healthcare IT market.

By Solution Type:

By Deployment Model:

By End User:

Electronic Health Records represent the largest healthcare IT segment, driven by regulatory mandates and clinical workflow optimization requirements. EHR adoption rates across European healthcare providers have reached 82% for basic systems and 67% for comprehensive EHR implementations. Advanced EHR features including clinical decision support, patient portals, and mobile access drive continued market growth.

Telemedicine platforms demonstrate exceptional growth following pandemic-driven adoption acceleration. Virtual care utilization maintains elevated levels with permanent adoption rates of approximately 58% among European healthcare providers. Integration with existing healthcare IT systems and regulatory compliance for cross-border telemedicine consultations create opportunities for specialized platform providers.

Healthcare analytics emerges as a high-growth segment with healthcare organizations leveraging data insights for population health management, clinical outcome improvement, and operational efficiency. Analytics adoption shows strong momentum with implementation rates increasing by 35% annually among European healthcare systems seeking data-driven decision-making capabilities.

Healthcare Providers benefit from improved clinical workflows, enhanced patient safety through clinical decision support systems, and reduced administrative burden through automated processes. Operational efficiency gains of up to 25% in administrative tasks enable healthcare professionals to focus more time on direct patient care activities.

Patients experience enhanced healthcare access through patient portals, telemedicine consultations, and mobile health applications. Improved care coordination between healthcare providers and better access to personal health information empower patients to actively participate in their healthcare management. Patient satisfaction scores increase by an average of 18% following healthcare IT implementation.

Healthcare IT Vendors access substantial market opportunities driven by ongoing digital transformation initiatives and government healthcare IT investments. Recurring revenue models from software-as-a-service offerings provide stable income streams while creating long-term customer relationships. Innovation partnerships with healthcare providers enable vendors to develop solutions addressing specific European healthcare market needs.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial Intelligence Integration represents the most significant trend reshaping European healthcare IT, with AI-powered clinical decision support, diagnostic assistance, and predictive analytics becoming standard features in advanced healthcare IT platforms. Machine learning algorithms enhance clinical outcomes while reducing healthcare costs through improved diagnostic accuracy and treatment optimization.

Interoperability Standardization gains momentum as European healthcare systems implement common data exchange protocols enabling seamless information sharing between different healthcare IT systems. FHIR (Fast Healthcare Interoperability Resources) adoption accelerates across European healthcare providers seeking improved care coordination and data accessibility.

Patient-Centric Design influences healthcare IT solution development with emphasis on user-friendly interfaces, mobile accessibility, and patient engagement features. Consumer health applications integrate with professional healthcare IT systems, creating comprehensive digital health ecosystems that support both clinical care and patient self-management.

Cloud-Native Architecture becomes the preferred deployment model for new healthcare IT implementations, offering scalability, cost-effectiveness, and enhanced security features. Microservices architecture enables modular healthcare IT solutions that can be customized and upgraded independently, providing flexibility for evolving healthcare requirements.

Strategic partnerships between healthcare IT vendors and European healthcare systems accelerate innovation and solution development. MarkWide Research analysis indicates increasing collaboration between technology companies and healthcare providers to develop specialized solutions addressing specific European healthcare challenges and regulatory requirements.

Regulatory initiatives including the European Health Data Space proposal create frameworks for secure healthcare data sharing across EU member states. These developments drive demand for healthcare IT solutions supporting cross-border healthcare delivery and research collaboration while maintaining strict data protection standards.

Investment activity in European healthcare IT startups reaches record levels as venture capital firms and strategic investors recognize the market potential for innovative digital health solutions. Funding rounds focus on artificial intelligence applications, telemedicine platforms, and patient engagement technologies that address specific European healthcare market needs.

Acquisition strategies among major healthcare IT vendors involve acquiring specialized European companies to expand solution portfolios and enhance local market presence. These transactions consolidate market leadership while bringing innovative technologies and regional expertise to larger healthcare IT platforms.

Healthcare IT vendors should prioritize interoperability capabilities and European regulatory compliance in solution development to address market requirements for seamless data exchange and data protection standards. Investment focus on artificial intelligence integration and cloud-native architectures positions vendors for long-term market success in the evolving European healthcare landscape.

Healthcare providers should develop comprehensive digital transformation strategies that align with national healthcare digitization initiatives while addressing specific organizational needs. Phased implementation approaches enable manageable healthcare IT adoption while minimizing disruption to clinical operations and patient care delivery.

Government policymakers should continue supporting healthcare IT adoption through funding programs, regulatory frameworks, and standardization initiatives that facilitate market development. Public-private partnerships can accelerate healthcare digitization while ensuring solutions meet public healthcare system requirements and patient needs.

Investment considerations should focus on healthcare IT companies demonstrating strong European market presence, regulatory compliance capabilities, and innovative solution portfolios addressing key healthcare challenges. MWR analysis suggests particular opportunities in AI-powered healthcare solutions and interoperability platforms supporting cross-border healthcare delivery.

Market trajectory indicates continued robust growth driven by ongoing digital transformation initiatives, artificial intelligence integration, and expanding telemedicine adoption across European healthcare systems. Technology evolution will focus on advanced analytics, predictive healthcare, and personalized medicine applications that leverage comprehensive healthcare data for improved patient outcomes.

Regulatory developments including the European Health Data Space implementation will create new opportunities for healthcare IT solutions supporting secure data sharing and cross-border healthcare collaboration. Standardization efforts will enhance interoperability while maintaining strict data protection and patient privacy requirements.

Innovation focus will emphasize patient-centric solutions, mobile health integration, and artificial intelligence applications that transform healthcare delivery models. Emerging technologies including blockchain for healthcare data security, Internet of Things for patient monitoring, and virtual reality for medical training will create additional market opportunities.

Market consolidation will continue as larger healthcare IT vendors acquire specialized capabilities while new entrants focus on innovative niche solutions. Partnership strategies between technology companies, healthcare providers, and research institutions will drive collaborative innovation addressing specific European healthcare challenges and opportunities.

The Europe Healthcare Information Technology (IT) market represents a dynamic and rapidly evolving landscape characterized by strong government support, comprehensive digital transformation initiatives, and increasing adoption of advanced healthcare technologies. Market fundamentals remain robust with substantial growth opportunities driven by demographic pressures, regulatory mandates, and evolving patient expectations for digital health services.

Key success factors for market participants include interoperability capabilities, regulatory compliance expertise, and innovative solution development addressing specific European healthcare requirements. The integration of artificial intelligence, cloud computing, and mobile health technologies creates significant opportunities for healthcare IT vendors while enhancing patient care quality and operational efficiency for healthcare providers.

Strategic positioning requires understanding of diverse European healthcare systems, regulatory environments, and cultural preferences that influence healthcare IT adoption patterns. MarkWide Research projects continued market expansion supported by sustained government investment, technological innovation, and the ongoing digital transformation of European healthcare delivery models, positioning the market for sustained growth and innovation in the coming years.

What is Healthcare Information Technology (IT)?

Healthcare Information Technology (IT) refers to the use of technology to manage healthcare data and improve the delivery of healthcare services. This includes electronic health records, telemedicine, and health information exchanges, which enhance patient care and operational efficiency.

What are the key players in the Europe Healthcare Information Technology (IT) Market?

Key players in the Europe Healthcare Information Technology (IT) Market include Siemens Healthineers, Cerner Corporation, Philips Healthcare, and Allscripts Healthcare Solutions, among others. These companies are known for their innovative solutions in electronic health records and healthcare analytics.

What are the main drivers of growth in the Europe Healthcare Information Technology (IT) Market?

The main drivers of growth in the Europe Healthcare Information Technology (IT) Market include the increasing demand for digital health solutions, the need for improved patient care, and government initiatives promoting healthcare digitization. Additionally, the rise of telehealth services has significantly contributed to market expansion.

What challenges does the Europe Healthcare Information Technology (IT) Market face?

The Europe Healthcare Information Technology (IT) Market faces challenges such as data privacy concerns, high implementation costs, and resistance to change among healthcare professionals. These factors can hinder the adoption of new technologies and systems.

What opportunities exist in the Europe Healthcare Information Technology (IT) Market?

Opportunities in the Europe Healthcare Information Technology (IT) Market include the growing trend of personalized medicine, advancements in artificial intelligence for healthcare applications, and the increasing integration of IoT devices in patient monitoring. These trends are expected to drive innovation and investment in the sector.

What trends are shaping the Europe Healthcare Information Technology (IT) Market?

Trends shaping the Europe Healthcare Information Technology (IT) Market include the rise of telemedicine, the adoption of cloud-based solutions, and the focus on interoperability among healthcare systems. These trends are enhancing the efficiency and effectiveness of healthcare delivery.

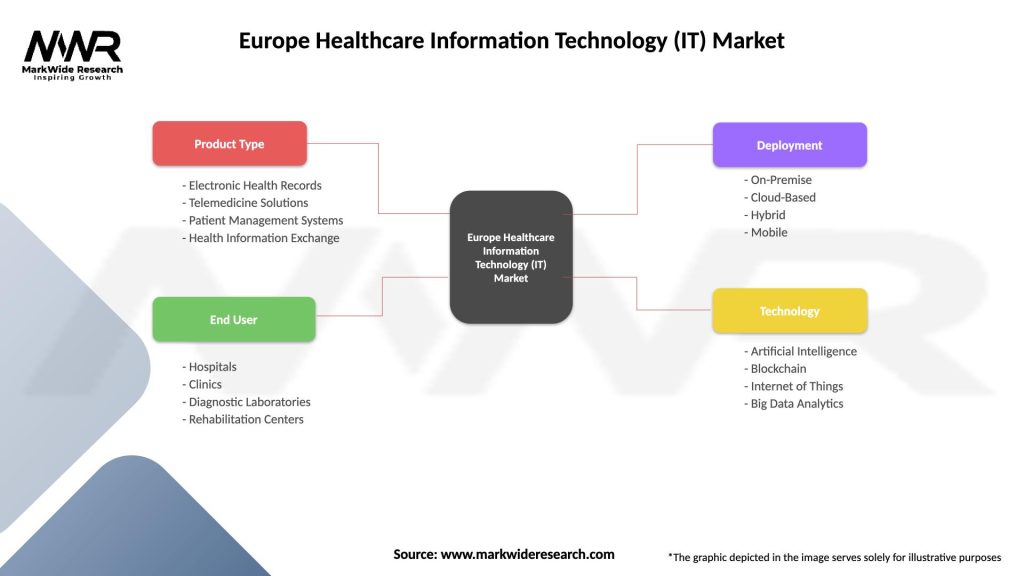

Europe Healthcare Information Technology (IT) Market

| Segmentation Details | Description |

|---|---|

| Product Type | Electronic Health Records, Telemedicine Solutions, Patient Management Systems, Health Information Exchange |

| End User | Hospitals, Clinics, Diagnostic Laboratories, Rehabilitation Centers |

| Deployment | On-Premise, Cloud-Based, Hybrid, Mobile |

| Technology | Artificial Intelligence, Blockchain, Internet of Things, Big Data Analytics |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Healthcare Information Technology (IT) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.