444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe food contract manufacturing and packaging market represents a dynamic and rapidly evolving sector that serves as the backbone of the continent’s food supply chain. This comprehensive market encompasses specialized companies that provide manufacturing, processing, and packaging services to food brands, retailers, and distributors across European nations. Contract manufacturing has emerged as a strategic solution for food companies seeking to optimize production costs, enhance operational efficiency, and access specialized expertise without substantial capital investments.

Market dynamics indicate robust growth driven by increasing demand for private label products, rising consumer preferences for convenience foods, and the growing complexity of food safety regulations. The sector demonstrates remarkable resilience with annual growth rates exceeding 6.2%, reflecting strong market fundamentals and expanding opportunities across diverse food categories. European food manufacturers are increasingly leveraging contract services to focus on core competencies while outsourcing production and packaging operations to specialized providers.

Regional distribution shows significant concentration in Western European markets, with Germany, France, and the United Kingdom accounting for approximately 58% of total market activity. The sector benefits from advanced manufacturing infrastructure, stringent quality standards, and sophisticated supply chain networks that enable efficient distribution across continental markets. Innovation trends emphasize sustainable packaging solutions, clean label manufacturing processes, and advanced automation technologies that enhance production capabilities.

The Europe food contract manufacturing and packaging market refers to the comprehensive ecosystem of specialized service providers that offer manufacturing, processing, co-packing, and packaging solutions to food companies across European territories. This market encompasses companies that produce food products on behalf of brand owners, retailers, and distributors, providing end-to-end services from ingredient sourcing and recipe development to final packaging and distribution support.

Contract manufacturing in the food industry involves outsourcing production activities to third-party manufacturers who possess specialized equipment, expertise, and regulatory compliance capabilities. These services enable food companies to access production capacity without significant capital investments in manufacturing facilities, equipment, or specialized workforce. Co-packaging services focus specifically on packaging operations, including primary packaging, secondary packaging, labeling, and preparation for retail distribution.

Market participants include dedicated contract manufacturers, co-packers, private label manufacturers, and integrated service providers offering comprehensive solutions across multiple food categories. The sector serves diverse clients ranging from startup food brands and established manufacturers to major retailers developing private label products and international companies seeking European market entry.

Strategic market analysis reveals the Europe food contract manufacturing and packaging market as a critical enabler of food industry growth and innovation. The sector demonstrates exceptional resilience and adaptability, driven by evolving consumer preferences, regulatory requirements, and competitive pressures that encourage outsourcing of non-core manufacturing activities. Market expansion reflects increasing adoption of contract services across traditional and emerging food categories.

Key growth drivers include the rapid expansion of private label products, which now represent over 42% of total food retail sales in several European markets. This trend creates substantial opportunities for contract manufacturers specializing in private label production. Sustainability initiatives are reshaping market dynamics, with 78% of contract manufacturers investing in eco-friendly packaging solutions and sustainable production processes to meet evolving consumer and regulatory expectations.

Technological advancement plays a pivotal role in market evolution, with automation, digitalization, and Industry 4.0 technologies enhancing production efficiency and quality control capabilities. Regulatory compliance remains a fundamental market driver, as food companies increasingly rely on specialized contract manufacturers to navigate complex European food safety regulations and maintain compliance across multiple jurisdictions.

Competitive landscape features a mix of large multinational contract manufacturers, regional specialists, and niche providers focusing on specific food categories or specialized services. Market consolidation trends indicate ongoing merger and acquisition activity as companies seek to expand capabilities, geographic reach, and service offerings to meet evolving client requirements.

Market intelligence reveals several critical insights that define the current state and future trajectory of the Europe food contract manufacturing and packaging market:

Market segmentation analysis indicates strong performance across diverse food categories, with particular strength in convenience foods, snacks, beverages, and frozen products. Service diversification trends show contract manufacturers expanding beyond traditional production to offer comprehensive solutions including product development, regulatory support, and supply chain management.

Primary market drivers propelling growth in the Europe food contract manufacturing and packaging sector reflect fundamental shifts in food industry dynamics and consumer behavior patterns. These drivers create sustained demand for specialized manufacturing and packaging services across diverse market segments.

Private label expansion represents the most significant growth driver, with European retailers increasingly developing proprietary food brands to enhance margins and differentiate their offerings. Retail concentration in major European markets enables large retailers to leverage economies of scale in private label development, creating substantial opportunities for contract manufacturers specializing in private label production.

Cost optimization pressures encourage food companies to outsource manufacturing operations to specialized providers who can achieve greater efficiency through dedicated equipment, expertise, and scale advantages. Capital efficiency considerations drive companies to focus resources on core competencies such as marketing, distribution, and brand development while outsourcing production activities.

Regulatory compliance requirements create demand for specialized expertise in navigating complex European food safety regulations, labeling requirements, and quality standards. Food safety standards continue evolving, requiring ongoing investment in compliance capabilities that many companies prefer to access through specialized contract manufacturers.

Consumer convenience trends drive demand for ready-to-eat products, portion-controlled packaging, and innovative food formats that require specialized manufacturing capabilities. Lifestyle changes emphasizing convenience, health consciousness, and sustainability create opportunities for contract manufacturers offering specialized production and packaging solutions.

Market entry facilitation represents another key driver, as international food companies seek to enter European markets through partnerships with local contract manufacturers who provide market knowledge, regulatory expertise, and established distribution relationships.

Market constraints affecting the Europe food contract manufacturing and packaging sector present challenges that industry participants must navigate to maintain growth momentum and operational effectiveness. These restraints reflect structural, regulatory, and competitive factors that influence market dynamics.

Quality control complexities represent a significant restraint, as food companies must maintain strict oversight of contract manufacturing operations to ensure product quality, safety, and brand consistency. Brand protection concerns create hesitation among some companies regarding outsourcing critical production activities that directly impact product quality and consumer perception.

Supply chain vulnerabilities have become more apparent following recent global disruptions, highlighting risks associated with dependence on third-party manufacturers. Capacity constraints during peak demand periods can create production bottlenecks and limit flexibility in responding to market opportunities or seasonal fluctuations.

Regulatory compliance costs continue increasing as European food safety standards become more stringent and complex. Certification requirements for organic, sustainable, and specialty food categories create additional compliance burdens that can limit market access for smaller contract manufacturers.

Labor shortages in key European manufacturing regions affect production capacity and increase operational costs. Skilled workforce availability remains a persistent challenge, particularly for specialized food processing and packaging operations requiring technical expertise.

Raw material price volatility creates margin pressures and complicates long-term contract negotiations between food companies and contract manufacturers. Energy cost fluctuations particularly impact energy-intensive food processing operations, affecting overall cost competitiveness.

Strategic opportunities within the Europe food contract manufacturing and packaging market reflect emerging trends, technological advances, and evolving consumer preferences that create new avenues for growth and innovation. These opportunities enable market participants to expand services, enter new segments, and enhance competitive positioning.

Sustainable packaging innovation presents substantial opportunities as European consumers and regulators increasingly prioritize environmental sustainability. Circular economy initiatives drive demand for recyclable, biodegradable, and reduced-packaging solutions that require specialized expertise and equipment investments.

Plant-based food production represents a rapidly expanding opportunity segment, with plant-based product sales growing at rates exceeding 23% annually in key European markets. Alternative protein manufacturing requires specialized processing capabilities that create opportunities for contract manufacturers willing to invest in dedicated equipment and expertise.

E-commerce packaging solutions offer growth opportunities as online food retail continues expanding. Direct-to-consumer fulfillment requires specialized packaging solutions that protect products during shipping while meeting sustainability expectations and brand presentation requirements.

Functional food development creates opportunities for contract manufacturers with capabilities in nutraceutical integration, specialized processing techniques, and regulatory compliance for health-focused food products. Personalized nutrition trends may drive demand for flexible manufacturing capabilities supporting customized food products.

Eastern European expansion presents geographic growth opportunities as these markets develop and consumer spending increases. Market penetration in emerging European economies offers potential for establishing manufacturing operations and serving growing local demand.

Technology integration services create opportunities for contract manufacturers to differentiate through advanced capabilities including blockchain traceability, IoT-enabled quality monitoring, and data analytics services that provide additional value to food company clients.

Market dynamics in the Europe food contract manufacturing and packaging sector reflect complex interactions between supply and demand factors, competitive pressures, and external influences that shape market evolution and strategic decision-making. Understanding these dynamics enables stakeholders to navigate market challenges and capitalize on emerging opportunities.

Supply-demand equilibrium demonstrates generally favorable conditions with growing demand for contract services outpacing capacity expansion in several key segments. Capacity utilization rates averaging 82% across major European markets indicate healthy demand levels while suggesting opportunities for strategic capacity investments.

Competitive intensity varies significantly across different food categories and geographic regions, with established players maintaining strong positions in traditional segments while new entrants focus on emerging categories such as plant-based foods and sustainable packaging solutions. Market consolidation trends continue as larger players acquire specialized capabilities and regional presence through strategic acquisitions.

Technology adoption patterns show accelerating investment in automation, digitalization, and advanced manufacturing technologies that enhance efficiency and quality control capabilities. Industry 4.0 integration enables real-time monitoring, predictive maintenance, and data-driven optimization that improve operational performance and client satisfaction.

Regulatory evolution continues influencing market dynamics through evolving food safety standards, environmental regulations, and labeling requirements that create both challenges and opportunities for market participants. Compliance differentiation enables specialized contract manufacturers to command premium pricing for expertise in navigating complex regulatory environments.

Consumer behavior shifts toward health consciousness, sustainability, and convenience continue driving demand for specialized manufacturing and packaging solutions. Trend responsiveness becomes a key competitive advantage for contract manufacturers capable of quickly adapting to evolving consumer preferences and market requirements.

Comprehensive research methodology employed in analyzing the Europe food contract manufacturing and packaging market incorporates multiple data sources, analytical frameworks, and validation techniques to ensure accuracy and reliability of market insights. The methodology combines quantitative analysis with qualitative research to provide holistic market understanding.

Primary research activities include extensive interviews with industry executives, contract manufacturers, food companies, and regulatory experts across major European markets. Survey methodology encompasses structured questionnaires administered to market participants to gather quantitative data on market trends, capacity utilization, pricing dynamics, and future investment plans.

Secondary research incorporates analysis of industry reports, regulatory filings, company financial statements, trade publications, and government statistics to validate primary research findings and provide comprehensive market context. Data triangulation techniques ensure consistency and accuracy across multiple information sources.

Market sizing methodology employs bottom-up and top-down approaches to validate market scope and growth projections. Segmentation analysis utilizes detailed categorization by service type, food category, packaging type, and geographic region to provide granular market insights.

Analytical frameworks include Porter’s Five Forces analysis, SWOT assessment, and competitive positioning analysis to evaluate market structure and competitive dynamics. Trend analysis incorporates historical data review and forward-looking projections to identify market patterns and growth trajectories.

Quality assurance procedures include peer review, expert validation, and cross-referencing with established industry benchmarks to ensure research reliability and credibility. Continuous monitoring processes enable ongoing validation and updating of market insights as new information becomes available.

Regional market analysis reveals significant variations in market development, competitive dynamics, and growth opportunities across different European territories. Understanding regional characteristics enables stakeholders to develop targeted strategies and optimize market positioning.

Western Europe dominates market activity, accounting for approximately 67% of total contract manufacturing capacity across the region. Germany leads in manufacturing sophistication and technological advancement, with particular strength in beverage processing, bakery products, and frozen foods. Advanced automation and strict quality standards characterize German contract manufacturing operations.

France demonstrates strong capabilities in dairy processing, confectionery manufacturing, and premium food packaging solutions. Culinary heritage and emphasis on food quality create opportunities for specialized contract manufacturers serving artisanal and premium food segments. Sustainability initiatives drive innovation in eco-friendly packaging solutions.

United Kingdom maintains significant market presence despite Brexit-related challenges, with particular strength in convenience foods, snacks, and private label manufacturing. Retail concentration creates substantial opportunities for contract manufacturers specializing in private label production for major UK retailers.

Netherlands serves as a strategic hub for European distribution, with contract manufacturers leveraging excellent logistics infrastructure to serve pan-European markets. Port access and transportation networks enable efficient ingredient sourcing and product distribution across continental markets.

Eastern Europe represents the fastest-growing regional segment, with annual growth rates exceeding 8.5% driven by economic development and increasing consumer spending. Poland, Czech Republic, and Hungary lead regional growth, attracting investment in modern manufacturing facilities and packaging capabilities.

Southern Europe demonstrates strength in traditional food categories including olive oil processing, pasta manufacturing, and Mediterranean specialty foods. Export orientation creates opportunities for contract manufacturers serving international markets with authentic European food products.

Competitive landscape analysis reveals a diverse ecosystem of market participants ranging from large multinational contract manufacturers to specialized regional providers and niche service companies. Market structure reflects ongoing consolidation trends alongside continued opportunities for specialized players.

Market positioning strategies vary significantly among competitors, with some focusing on scale and cost efficiency while others emphasize specialization and premium services. Vertical integration trends show leading players expanding capabilities across the value chain from ingredient sourcing to final packaging and distribution.

Innovation leadership becomes increasingly important as companies invest in research and development capabilities, sustainable technologies, and advanced manufacturing processes. Strategic partnerships with food companies, technology providers, and research institutions enable competitive differentiation and market expansion.

Geographic expansion strategies focus on establishing presence in high-growth Eastern European markets while maintaining strong positions in established Western European territories. Acquisition activity continues as companies seek to expand capabilities, market reach, and specialized expertise through strategic acquisitions.

Market segmentation analysis provides detailed insights into different market categories, enabling stakeholders to understand specific opportunities, competitive dynamics, and growth patterns within distinct market segments.

By Service Type:

By Food Category:

By Packaging Type:

Category-specific analysis reveals distinct market dynamics, growth patterns, and competitive characteristics across different food segments within the European contract manufacturing and packaging market.

Bakery Products Segment demonstrates strong growth driven by increasing demand for artisanal breads, gluten-free products, and premium baked goods. Automation adoption in bakery manufacturing enables consistent quality and efficient production while maintaining traditional product characteristics. Clean label trends drive demand for contract manufacturers specializing in natural ingredients and traditional baking processes.

Dairy Products Category benefits from growing demand for plant-based alternatives, functional dairy products, and premium cheese varieties. Processing expertise in dairy alternatives creates opportunities for specialized contract manufacturers with capabilities in plant-based milk production and dairy-free cheese manufacturing. Organic certification becomes increasingly important for premium dairy contract manufacturing.

Beverage Manufacturing shows particular strength in functional beverages, craft beverages, and sustainable packaging solutions. Innovation focus on health-conscious formulations and unique flavor profiles creates opportunities for contract manufacturers with specialized beverage development capabilities. Packaging innovation emphasizes sustainable materials and convenient consumption formats.

Snack Foods Segment experiences robust growth driven by convenience trends and healthy snacking preferences. Portion control packaging and premium snack varieties create opportunities for specialized contract manufacturers. Sustainability initiatives focus on reducing packaging waste and utilizing eco-friendly materials.

Frozen Foods Category benefits from busy lifestyles and demand for convenient meal solutions. Quality preservation technologies and efficient cold chain management become critical competitive advantages for contract manufacturers serving this segment. Premium frozen products create opportunities for specialized manufacturing capabilities.

Strategic benefits derived from participation in the Europe food contract manufacturing and packaging market create value for diverse stakeholders including food companies, retailers, investors, and service providers. Understanding these benefits enables informed decision-making and strategic planning.

For Food Companies:

For Retailers:

For Contract Manufacturers:

For Investors:

Comprehensive SWOT analysis provides strategic insights into the internal strengths and weaknesses of the Europe food contract manufacturing and packaging market, along with external opportunities and threats that influence market dynamics and competitive positioning.

Strengths:

Weaknesses:

Opportunities:

Threats:

Emerging market trends shape the evolution of the Europe food contract manufacturing and packaging sector, influencing strategic decisions, investment priorities, and competitive positioning across the industry. These trends reflect changing consumer preferences, technological advances, and regulatory developments.

Sustainability Integration represents the most significant trend, with environmental considerations becoming central to manufacturing and packaging decisions. Circular economy principles drive innovation in recyclable packaging materials, waste reduction initiatives, and energy-efficient manufacturing processes. Carbon footprint reduction becomes a key competitive differentiator for contract manufacturers.

Digital Transformation accelerates across the industry with Industry 4.0 technologies enhancing operational efficiency and quality control capabilities. IoT integration enables real-time monitoring of production processes, predictive maintenance, and data-driven optimization. Blockchain technology improves traceability and transparency throughout the supply chain.

Clean Label Movement continues gaining momentum, with consumers demanding transparency in ingredient lists and manufacturing processes. Natural ingredients and minimal processing become key requirements for contract manufacturers serving health-conscious consumer segments. Additive reduction drives innovation in natural preservation and flavoring solutions.

Personalization Trends create opportunities for flexible manufacturing capabilities supporting customized food products and specialized dietary requirements. Small batch production becomes increasingly important for serving niche markets and testing new product concepts. Mass customization technologies enable efficient production of personalized food products.

Plant-Based Revolution transforms manufacturing requirements with growing demand for plant-based alternatives across multiple food categories. Alternative protein processing requires specialized equipment and expertise, creating opportunities for contract manufacturers willing to invest in dedicated capabilities.

Convenience Evolution drives demand for innovative packaging formats, portion control solutions, and ready-to-consume products. On-the-go consumption trends influence packaging design and product formulation requirements. Meal kit manufacturing creates new opportunities for specialized contract services.

Recent industry developments highlight significant changes, investments, and strategic initiatives that shape the competitive landscape and market evolution within the Europe food contract manufacturing and packaging sector. These developments reflect industry responses to market opportunities and challenges.

Capacity Expansion Initiatives demonstrate strong market confidence with major contract manufacturers investing in new facilities and equipment upgrades across European markets. Automation investments focus on enhancing efficiency, consistency, and quality control capabilities while addressing labor shortage challenges. Sustainable technology adoption becomes a priority for new facility developments.

Strategic Acquisitions continue reshaping the competitive landscape as larger players acquire specialized capabilities and regional presence. Vertical integration trends show companies expanding across the value chain to offer comprehensive solutions. Technology acquisitions focus on digital capabilities, automation expertise, and sustainable packaging innovations.

Regulatory Compliance Investments reflect ongoing adaptation to evolving European food safety standards and environmental regulations. Certification expansion includes organic, sustainable, and specialty dietary certifications that enable access to premium market segments. Traceability systems become standard requirements for regulatory compliance and consumer transparency.

Sustainability Initiatives encompass comprehensive programs addressing packaging materials, energy efficiency, and waste reduction. Renewable energy adoption accelerates across manufacturing facilities to reduce carbon footprint and operational costs. Circular economy partnerships develop to create closed-loop systems for packaging materials and waste management.

Innovation Partnerships between contract manufacturers, food companies, and technology providers drive development of new products, processes, and packaging solutions. Research collaborations with universities and research institutions focus on sustainable technologies and advanced manufacturing processes. Startup partnerships enable access to innovative technologies and emerging market trends.

Strategic recommendations for stakeholders in the Europe food contract manufacturing and packaging market reflect comprehensive analysis of market dynamics, competitive trends, and future opportunities. These suggestions enable informed decision-making and strategic planning across different market participants.

For Food Companies: MarkWide Research recommends developing long-term partnerships with contract manufacturers that demonstrate strong sustainability credentials and technological capabilities. Due diligence processes should emphasize quality control systems, regulatory compliance track records, and capacity scalability. Geographic diversification of contract manufacturing relationships can enhance supply chain resilience and market access capabilities.

For Contract Manufacturers: Investment priorities should focus on sustainable technologies, automation capabilities, and specialized expertise in high-growth segments such as plant-based foods and functional products. Certification expansion across organic, sustainable, and specialty dietary categories enables access to premium market opportunities. Digital transformation initiatives should emphasize traceability, quality monitoring, and customer service capabilities.

For Retailers: Private label strategies should leverage contract manufacturing partnerships to develop differentiated products that meet evolving consumer preferences for sustainability, health, and convenience. Supply chain optimization through strategic contract manufacturing relationships can enhance efficiency and cost competitiveness. Innovation collaboration with manufacturing partners enables faster product development and market responsiveness.

For Investors: Investment opportunities should prioritize companies with strong sustainability positioning, technological capabilities, and exposure to high-growth market segments. Consolidation opportunities exist in fragmented market segments where scale advantages and operational efficiency can create value. Geographic expansion into Eastern European markets offers attractive growth potential with developing food industries.

Market Entry Strategies for new participants should focus on specialized capabilities, niche market segments, or geographic regions with limited competition. Technology differentiation through advanced automation, sustainability innovations, or specialized processing capabilities can create competitive advantages in established markets.

Future market projections for the Europe food contract manufacturing and packaging sector indicate continued growth driven by fundamental market drivers and emerging opportunities. Long-term growth prospects remain positive despite potential short-term challenges from economic uncertainty and regulatory changes.

Market expansion is projected to continue at annual growth rates exceeding 6.8% over the next five years, driven by sustained demand for private label products, sustainability initiatives, and technological advancement. Eastern European markets are expected to demonstrate the strongest growth rates, with annual expansion exceeding 9.2% as these economies develop and consumer spending increases.

Technology integration will accelerate with Industry 4.0 adoption rates projected to reach 75% of major contract manufacturers within the next three years. Automation investments will focus on enhancing efficiency, quality control, and flexibility while addressing ongoing labor shortage challenges. Digital transformation will enable new service offerings and enhanced customer relationships.

Sustainability requirements will become increasingly stringent, with environmental compliance becoming a fundamental requirement for market participation. Circular economy principles will drive innovation in packaging materials, manufacturing processes, and waste management systems. Carbon neutrality goals will influence facility locations, energy sourcing, and transportation strategies.

Market consolidation trends are expected to continue with larger players acquiring specialized capabilities and regional presence. Vertical integration will expand as companies seek to control more of the value chain and offer comprehensive solutions. Strategic partnerships between manufacturers, technology providers, and food companies will become increasingly important for innovation and market access.

Consumer trends toward health consciousness, sustainability, and convenience will continue driving demand for specialized manufacturing and packaging solutions. Plant-based food production will require significant capacity expansion and specialized expertise. Personalization trends may create opportunities for flexible manufacturing capabilities supporting customized products.

The Europe food contract manufacturing and packaging market stands as a cornerstone of the region’s food industry ecosystem, demonstrating remarkable resilience and adaptability in an increasingly complex global marketplace. Throughout this comprehensive analysis, it has become evident that this sector represents far more than a simple outsourcing solution—it embodies a strategic transformation that is reshaping how food companies approach production, distribution, and market penetration across European territories.

Market dynamics reveal a sector experiencing unprecedented growth driven by evolving consumer preferences, regulatory complexities, and the relentless pursuit of operational efficiency. The shift toward specialized contract manufacturing has enabled food brands to focus on their core competencies while leveraging the expertise, infrastructure, and scalability offered by dedicated manufacturing partners. This strategic alignment has proven particularly valuable as companies navigate the intricate landscape of European food regulations, sustainability requirements, and diverse market demands.

Regional variations across Europe continue to shape market opportunities, with Western European markets leading in terms of sophistication and automation, while Eastern European regions present compelling cost advantages and expanding capabilities. The integration of advanced packaging technologies has emerged as a critical differentiator, with contract manufacturers investing heavily in sustainable packaging solutions, smart packaging innovations, and flexible packaging formats that meet evolving consumer expectations for convenience, freshness, and environmental responsibility.

Technological advancement remains at the forefront of market evolution, with digital transformation initiatives, automation technologies, and data analytics capabilities becoming essential components of competitive contract manufacturing operations. According to MarkWide Research analysis, companies that have embraced these technological innovations are experiencing enhanced operational efficiency and improved client satisfaction rates, positioning themselves advantageously for long-term market success.

Sustainability imperatives have fundamentally altered the competitive landscape, with environmental considerations now influencing every aspect of contract manufacturing operations from raw material sourcing to packaging material selection and waste reduction strategies. The market’s response to these challenges through innovation in eco-friendly packaging solutions and circular economy practices demonstrates the sector’s commitment to responsible growth and long-term viability.

Future market trajectory indicates continued expansion driven by several key factors including the growth of private label products, increasing demand for specialized dietary products, and the ongoing trend toward supply chain optimization. The sector’s ability to provide flexible manufacturing solutions while maintaining stringent quality standards positions it as an indispensable partner for food brands seeking to expand their market presence without significant capital investments.

As the European food contract manufacturing and packaging market continues to evolve, stakeholders must remain vigilant to emerging trends, regulatory developments, and technological innovations that will shape the industry’s future. The successful navigation of challenges such as supply chain disruptions, labor shortages, and evolving consumer preferences will require continued investment in technology, talent development, and strategic partnerships that strengthen the entire value chain ecosystem across Europe’s diverse food manufacturing landscape.

What is Food Contract Manufacturing & Packaging?

Food Contract Manufacturing & Packaging refers to the outsourcing of food production and packaging processes to specialized companies. This allows food brands to focus on marketing and distribution while ensuring high-quality production and compliance with safety standards.

What are the key players in the Europe Food Contract Manufacturing & Packaging Market?

Key players in the Europe Food Contract Manufacturing & Packaging Market include companies like Cargill, Inc., and Kerry Group, which provide a range of services from product development to packaging solutions. Other notable companies include Dole Food Company and Greencore Group, among others.

What are the growth factors driving the Europe Food Contract Manufacturing & Packaging Market?

The growth of the Europe Food Contract Manufacturing & Packaging Market is driven by increasing consumer demand for convenience foods, the rise of e-commerce in food distribution, and the need for compliance with stringent food safety regulations. Additionally, innovations in packaging technology are enhancing product shelf life and appeal.

What challenges does the Europe Food Contract Manufacturing & Packaging Market face?

Challenges in the Europe Food Contract Manufacturing & Packaging Market include rising raw material costs, regulatory compliance complexities, and the need for sustainable packaging solutions. These factors can impact profit margins and operational efficiency for manufacturers.

What opportunities exist in the Europe Food Contract Manufacturing & Packaging Market?

Opportunities in the Europe Food Contract Manufacturing & Packaging Market include the growing trend towards plant-based foods, increased demand for organic products, and advancements in smart packaging technologies. These trends present avenues for innovation and market expansion.

What trends are shaping the Europe Food Contract Manufacturing & Packaging Market?

Trends shaping the Europe Food Contract Manufacturing & Packaging Market include a shift towards sustainable packaging materials, the integration of automation in manufacturing processes, and the increasing popularity of personalized nutrition. These trends are influencing how companies approach product development and consumer engagement.

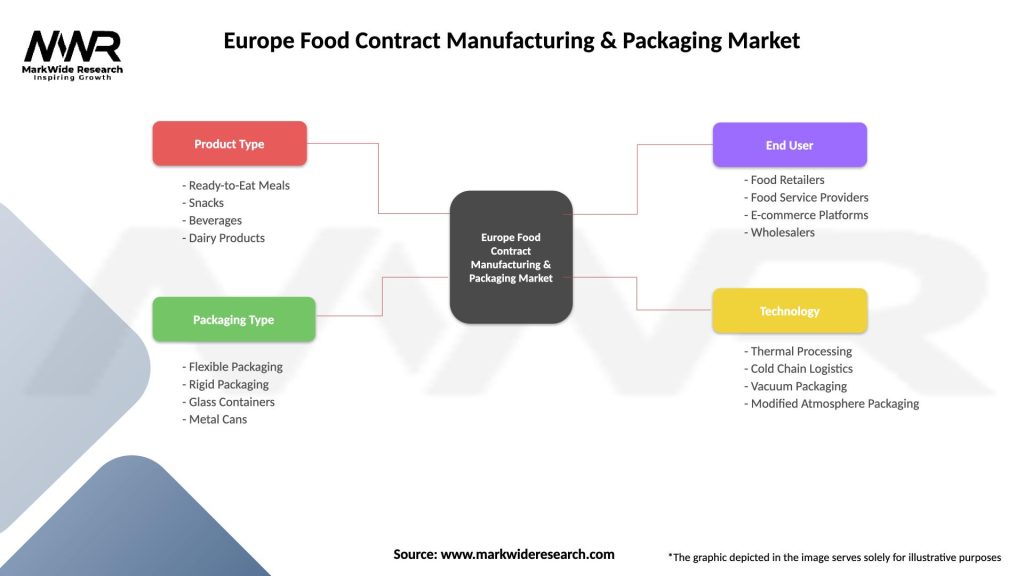

Europe Food Contract Manufacturing & Packaging Market

| Segmentation Details | Description |

|---|---|

| Product Type | Ready-to-Eat Meals, Snacks, Beverages, Dairy Products |

| Packaging Type | Flexible Packaging, Rigid Packaging, Glass Containers, Metal Cans |

| End User | Food Retailers, Food Service Providers, E-commerce Platforms, Wholesalers |

| Technology | Thermal Processing, Cold Chain Logistics, Vacuum Packaging, Modified Atmosphere Packaging |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Food Contract Manufacturing & Packaging Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.