The Europe EVA (Ethylene Vinyl Acetate) adhesives market has been witnessing significant growth in recent years. EVA adhesives are widely used in various industries due to their excellent bonding properties, flexibility, and low-temperature resistance. This market overview provides insights into the key factors driving the market, the challenges faced, and the opportunities for growth in the European region.

Meaning

EVA adhesives are a type of thermoplastic adhesive made from a copolymer of ethylene and vinyl acetate. They are widely used in industries such as packaging, automotive, construction, electronics, and footwear. EVA adhesives offer advantages such as strong bonding, flexibility, and resistance to UV radiation and chemicals. These properties make them suitable for a wide range of applications, including bonding different substrates and materials.

Executive Summary

The Europe EVA adhesives market has experienced steady growth over the past few years, driven by increasing demand from various end-use industries. The market has witnessed advancements in technology and product innovation, leading to improved adhesive performance and expanded application areas. This executive summary provides a concise overview of the market trends, key insights, and future growth prospects.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Solar Encapsulation: Over 35% of market volume derives from photovoltaic module lamination, as EVA adhesives ensure long‑term panel durability.

Packaging Growth: Single‑serve and flexible packaging segments account for nearly 25% of demand, driven by food safety regulations and consumer convenience trends.

Woodworking Sector: Engineered wood flooring and furniture manufacturing represent 20% of EVA adhesive consumption, owing to strong European construction activity.

Low‑Temp Formulations: Rapid adoption of grades melting below 130 °C reduces energy usage, aligning with corporate sustainability targets.

Water‑Based Transition: Water-based EVA emulsions are gaining share, comprising 15% of the market by 2023, due to stringent VOC regulations.

Market Drivers

Renewable Energy Expansion: Europe’s ambitious solar capacity targets are driving EVA encapsulant demand for module lamination.

Sustainable Packaging Initiatives: Regulatory bans on single‑use plastics and focus on recyclability boost flexible packaging adhesives.

Construction Boom: Growth in engineered wood products for green buildings increases the use of EVA adhesives in lamination and bonding.

Automotive Lightweighting: EVA adhesives in interior trim and composite bonding contribute to vehicle weight reduction and fuel efficiency.

Technological Innovation: Development of reactive EVA grades with improved peel strength and UV resistance opens new application avenues.

Market Restraints

Feedstock Price Volatility: Fluctuating ethylene and vinyl acetate costs can compress profit margins for adhesive manufacturers.

Competition from Alternatives: Polyurethane and acrylic adhesives offer specialized properties, challenging EVA usage in certain niches.

Temperature Sensitivity: Standard EVA adhesives may degrade at high service temperatures, limiting some industrial applications.

Recycling Challenges: EVA‑bonded laminates can complicate recycling streams, prompting calls for more easily separable adhesive systems.

Market Opportunities

Bio‑Based EVA Polymers: Incorporating renewable feedstocks (e.g., bio‑ethylene) can reduce carbon footprints and appeal to sustainability‑focused customers.

Smart Packaging: Integration of functional additives (e.g., antimicrobial agents) into EVA adhesives for active packaging solutions.

Flexible Electronics: EVA formulations with enhanced electrical insulation are suitable for wearable device lamination.

Cross‑Sector Innovation: Collaborations with solar glass manufacturers and wood panel producers enable co‑development of optimized adhesive systems.

Circular Economy Models: Development of adhesives that allow easier delamination for substrate recycling supports EU circularity goals.

Market Dynamics

Supply Side: Major chemical producers are retrofitting existing polymer lines to produce higher‑Vinyl Acetate Content (VAC) EVA grades, improving tack and flexibility. Strategic acquisitions among specialty adhesive firms are consolidating technology portfolios.

Demand Side: End‑users are demanding multi‑functional adhesives with reduced processing temperatures, faster set times, and enhanced environmental profiles. OEM partnerships and just‑in‑time supply models are becoming standard.

Economic Factors: Energy costs significantly impact hot‑melt adhesive production; EU energy subsidies and carbon pricing mechanisms influence operating expenses.

Regional Analysis

Western Europe: Germany, France, and the UK dominate consumption, driven by large solar installations, robust packaging industries, and advanced wood processing sectors.

Northern Europe: Scandinavia shows strong uptake of low‑temperature EVA adhesives in cold‑chain packaging and automotive applications.

Southern Europe: Spain and Italy lead in photovoltaic projects and flexible packaging, fueling EVA demand.

Eastern Europe: Poland and the Czech Republic exhibit growing woodworking and furniture manufacturing, adopting EVA adhesives in laminates and veneer bonding.

Competitive Landscape

Leading Companies in the Europe EVA Adhesives Market:

H.B. Fuller Company

Arkema S.A.

3M Company

Henkel AG & Co. KGaA

Sika AG

Bostik SA (a subsidiary of Arkema S.A.)

Avery Dennison Corporation

Huntsman Corporation

Dymax Corporation

Permabond LLC (an Ellsworth Adhesives company)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

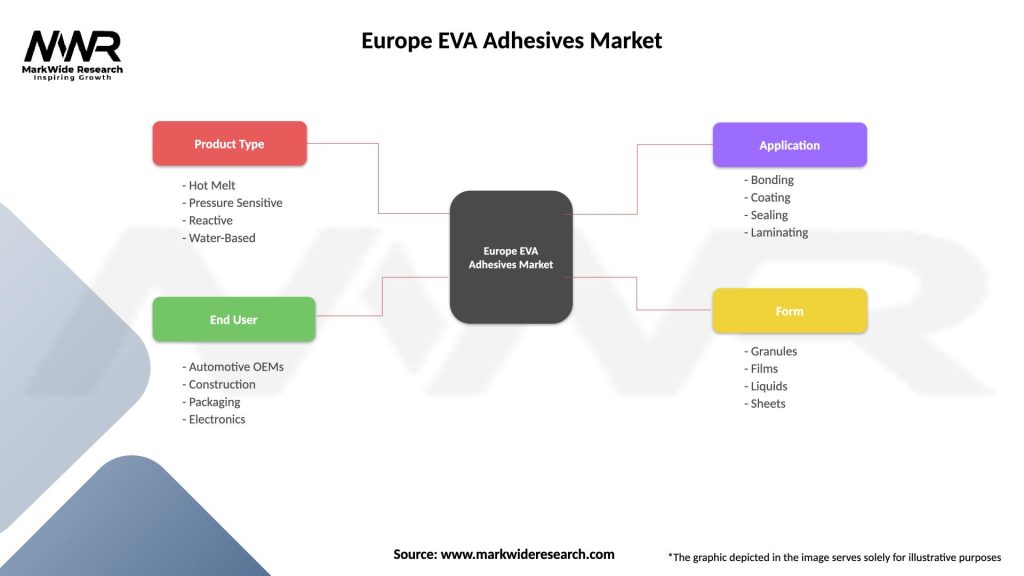

The Europe EVA adhesives market can be segmented based on application, end-use industry, and geography. Segmentation helps in understanding the specific needs of different industries and regions, enabling market players to customize their strategies accordingly. The segmentation also assists in identifying growth opportunities in niche markets and optimizing product offerings.

Category-wise Insights

Understanding the market trends and opportunities in specific categories within the Europe EVA adhesives market is essential. Category-wise insights provide detailed information about the growth prospects, demand-supply dynamics, and technological advancements in each category. This knowledge helps market participants make informed decisions and tap into lucrative market segments.

Key Benefits for Industry Participants and Stakeholders

Industry participants and stakeholders in the Europe EVA adhesives market can benefit from:

Opportunities for market expansion and diversification.

Insights into customer preferences and industry trends.

Strategic partnerships and collaborations to enhance product offerings.

Understanding the competitive landscape and benchmarking against industry leaders.

Identification of emerging market trends and future growth prospects.

SWOT Analysis

Strengths:

Strong demand in packaging, automotive, and construction industries.

High versatility in bonding different materials, including plastics, metals, and wood.

Environmentally friendly and non-toxic options available.

Weaknesses:

Vulnerability to fluctuations in raw material costs, such as ethylene and vinyl acetate.

Limited adoption in niche applications requiring more specialized adhesives.

Challenges with heat resistance in certain EVA adhesive formulations.

Opportunities:

Increasing demand for eco-friendly and sustainable adhesive products.

Expanding applications in the electric vehicle and renewable energy sectors.

Growth in the e-commerce and packaging industries driving adhesive needs.

Threats:

Competition from other adhesive technologies like polyurethane and pressure-sensitive adhesives.

Rising raw material prices affecting production costs.

Stringent environmental regulations affecting production processes.

Market Key Trends

Crosslinkable EVA Grades: Formulations enabling post‑application crosslinking for enhanced thermal and UV resistance.

Hybrid Adhesive Systems: Blends of EVA with polyolefin or styrenic block copolymers to tailor adhesion profiles.

Digital Printing Integration: Development of UV‑curable EVA adhesives compatible with digital label printing processes.

Energy‑Efficient Processing: Low‑temperature melt grades reducing energy consumption in high‑volume production lines.

Additive‑Enhanced Formulations: Inclusion of nanoparticles and bio‑additives to impart antimicrobial and conductivity functionalities.

Covid-19 Impact

Supply‑Chain Disruptions: Temporary shortages of vinyl acetate monomer and packaging line shutdowns impacted EVA adhesive availability in early 2020.

Surge in Packaging Demand: Spike in e‑commerce and food‑delivery packaging accelerated hot‑melt adhesive consumption.

Delayed Construction Projects: Slowdown in non‑essential construction reduced demand for woodworking and flooring adhesives temporarily.

Solar Installation Recovery: Renewable energy projects deemed essential continued, sustaining EVA encapsulant usage.

Key Industry Developments

Eastman’s Bio‑EVA Launch: Introduction of partially bio‑based EVA grades with 30% renewable content for sustainable packaging.

Bostik’s Low‑Temp Tech: Rollout of EVA hot‑melts curing at temperatures as low as 100 °C, enabling bonding of heat‑sensitive substrates.

Arkema’s Water‑Based Expansion: Commissioning of a new EVA emulsion line in France to meet rising demand for low‑VOC adhesives.

H.B. Fuller–SolarCo Partnership: Co‑development of advanced encapsulants for higher module efficiency and longer service life.

Avery Dennison’s Smart Labels: Collaboration to embed RFID and antimicrobial agents into EVA‑based label adhesive systems.

Analyst Suggestions

Diversify Feedstock Sourcing: Secure multiple ethylene and VAC suppliers to mitigate supply and price volatility.

Invest in Bio‑Based R&D: Accelerate development of fully renewable EVA formulations to stay ahead of regulatory curves.

Enhance Recycling Solutions: Collaborate with recyclers to develop adhesives that enable easier delamination of laminated materials.

Expand Technical Service: Offer in‑line monitoring and on‑site trials to optimize adhesive performance and reduce waste.

Target Niche Verticals: Explore high‑growth applications such as flexible electronics and medical device bonding.

Future Outlook The Europe EVA Adhesives Market is poised for steady growth, driven by renewable energy projects, sustainable packaging mandates, and advanced construction materials. Continued innovation in bio‑based chemistries, low‑temperature processing, and functional additives will unlock new applications and value‑added opportunities. Eastern Europe’s emerging industrial sectors and Western Europe’s push for green technologies will create a balanced demand landscape. EVA adhesive suppliers that combine technical excellence with sustainable product portfolios will lead the market’s next phase of expansion.

Conclusion EVA adhesives remain a cornerstone of Europe’s industrial and renewable energy sectors, offering unmatched versatility and performance. As market dynamics evolve—shaped by regulatory pressures, sustainability goals, and technological advancements—the ability to deliver eco‑friendly, high‑performance adhesive solutions will determine competitive success. Stakeholders who embrace innovation, strengthen supply‑chain resilience, and deepen customer partnerships will capitalize on the robust growth trajectory of the Europe EVA Adhesives Market.

What is EVA Adhesives?

EVA Adhesives, or Ethylene Vinyl Acetate Adhesives, are thermoplastic adhesives known for their excellent bonding properties, flexibility, and resistance to moisture. They are widely used in various applications, including packaging, automotive, and construction.

What are the key players in the Europe EVA Adhesives Market?

Key players in the Europe EVA Adhesives Market include companies like Henkel AG, Bostik, and 3M, which are known for their innovative adhesive solutions and strong market presence. These companies focus on developing high-performance adhesives for diverse applications, among others.

What are the growth factors driving the Europe EVA Adhesives Market?

The Europe EVA Adhesives Market is driven by increasing demand in the packaging industry, growth in the automotive sector, and the rising need for durable and flexible bonding solutions. Additionally, the trend towards lightweight materials in manufacturing is boosting the adoption of EVA adhesives.

What challenges does the Europe EVA Adhesives Market face?

Challenges in the Europe EVA Adhesives Market include fluctuating raw material prices and stringent environmental regulations. These factors can impact production costs and limit the availability of certain adhesive formulations.

What opportunities exist in the Europe EVA Adhesives Market?

Opportunities in the Europe EVA Adhesives Market include the growing demand for eco-friendly adhesives and advancements in adhesive technology. The increasing focus on sustainability is prompting manufacturers to develop bio-based EVA adhesives for various applications.

What trends are shaping the Europe EVA Adhesives Market?

Trends in the Europe EVA Adhesives Market include the rise of automation in manufacturing processes and the development of specialized adhesives for specific applications. Additionally, there is a growing emphasis on product innovation to meet the evolving needs of end-users.

Leading Companies in the Europe EVA Adhesives Market:

H.B. Fuller Company

Arkema S.A.

3M Company

Henkel AG & Co. KGaA

Sika AG

Bostik SA (a subsidiary of Arkema S.A.)

Avery Dennison Corporation

Huntsman Corporation

Dymax Corporation

Permabond LLC (an Ellsworth Adhesives company)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.