444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Europe District Cooling Pipeline Network Market has witnessed significant growth in recent years due to the increasing demand for energy-efficient cooling systems and the rising focus on sustainable infrastructure. District cooling is a centralized cooling system that uses chilled water or other cooling mediums to cool multiple buildings or areas within a city or district. The cooling is delivered through a network of underground pipelines, making it an efficient and environmentally friendly alternative to individual cooling systems.

Meaning

District cooling pipeline networks consist of a network of pipes that distribute chilled water or refrigerants from a central cooling plant to various connected buildings or facilities. These pipelines form the backbone of the district cooling system, enabling the transfer of cooling energy from the plant to the end-users. The pipelines are typically insulated to minimize heat gain and loss during transportation, ensuring the efficiency of the cooling system.

Executive Summary

The Europe District Cooling Pipeline Network Market is witnessing steady growth due to the rising demand for sustainable cooling solutions. The market is characterized by the presence of several key players offering a wide range of district cooling infrastructure and services. Factors such as increasing urbanization, government initiatives to promote energy efficiency, and the need to reduce carbon emissions are driving the adoption of district cooling systems in Europe. The market is expected to continue its growth trajectory in the coming years.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

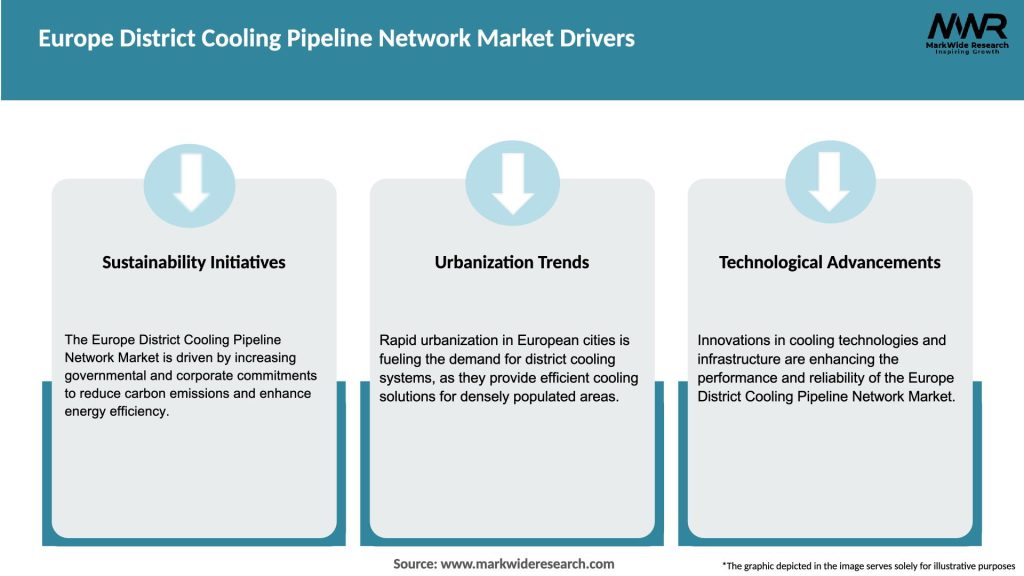

Market Dynamics

The Europe District Cooling Pipeline Network Market is influenced by several dynamics, including technological advancements, regulatory frameworks, market competition, and consumer preferences. The market is characterized by continuous innovation, with key players investing in research and development to enhance the efficiency and sustainability of district cooling systems. The regulatory landscape plays a crucial role in shaping market dynamics, with governments implementing policies and incentives to promote the adoption of district cooling. Market competition is intense, with players focusing on product differentiation, cost-effectiveness, and service quality to gain a competitive edge.

Regional Analysis

The Europe District Cooling Pipeline Network Market can be segmented into several key regions, including Western Europe, Eastern Europe, Northern Europe, Southern Europe, and Central Europe. Each region has its unique market dynamics, influenced by factors such as climate conditions, urbanization rates, government policies, and economic development. Western Europe, including countries like Germany, France, and the United Kingdom, currently dominates the market due to its advanced infrastructure, high urbanization rates, and favorable regulatory environment. However, other regions, such as Eastern Europe and Southern Europe, are also witnessing significant growth potential.

Competitive Landscape

Leading Companies in Europe District Cooling Pipeline Network Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

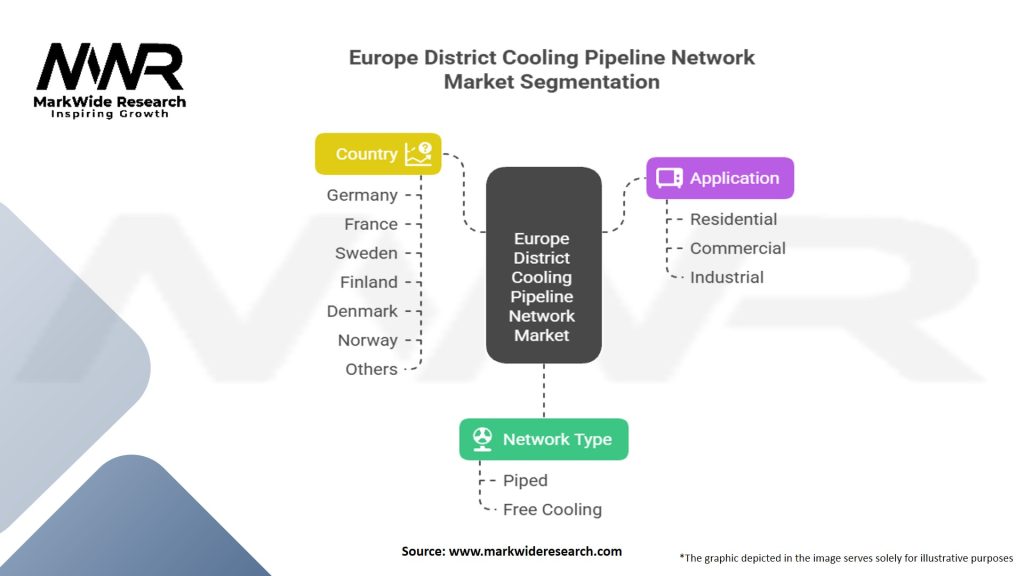

Segmentation

The Europe district cooling pipeline network market can be segmented based on type, application, and region. Each of these segments provides insights into the growth opportunities and key trends in the market.

By Type:

By Application:

By Region:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic has had both short-term and long-term impacts on the Europe District Cooling Pipeline Network Market. During the pandemic, there was a temporary slowdown in construction activities and infrastructure projects, affecting the demand for district cooling systems. However, the pandemic also highlighted the importance of resilient and sustainable cooling solutions, leading to increased awareness and demand for district cooling post-pandemic. The market is expected to rebound as economies recover and infrastructure projects resume.

Key Industry Developments

Analyst Suggestions

Future Outlook

The Europe District Cooling Pipeline Network Market is expected to witness significant growth in the coming years. Factors such as increasing urbanization, the need for sustainable cooling solutions, and supportive government policies will drive market expansion. The integration of renewable energy sources, smart grid technologies, and energy storage solutions will further enhance the efficiency and sustainability of district cooling systems. Market players should focus on innovation, customer-centric approaches, and strategic partnerships to capitalize on the market’s growth potential.

Conclusion

The Europe District Cooling Pipeline Network Market is poised for substantial growth, driven by the demand for energy-efficient and sustainable cooling solutions. District cooling systems offer significant benefits, including energy savings, cost reduction, and environmental sustainability. Although the market faces challenges such as initial investment costs and limited awareness, opportunities lie in the integration of renewable energy sources, smart grid technologies, and energy storage solutions. With continuous innovation, collaboration, and government support, the market is expected to flourish in the future, providing efficient cooling services to residential, commercial, and industrial buildings throughout Europe.

What is District Cooling Pipeline Network?

District Cooling Pipeline Network refers to a centralized cooling system that distributes chilled water through a network of insulated pipes to multiple buildings or facilities. This system is designed to provide efficient cooling solutions, reducing energy consumption and environmental impact.

What are the key players in the Europe District Cooling Pipeline Network Market?

Key players in the Europe District Cooling Pipeline Network Market include Veolia, Engie, and Fortum, which are known for their innovative cooling solutions and extensive infrastructure. These companies focus on enhancing energy efficiency and sustainability in urban environments, among others.

What are the growth factors driving the Europe District Cooling Pipeline Network Market?

The growth of the Europe District Cooling Pipeline Network Market is driven by increasing urbanization, rising energy costs, and a growing emphasis on sustainable building practices. Additionally, government initiatives promoting energy efficiency and reduced carbon emissions contribute to market expansion.

What challenges does the Europe District Cooling Pipeline Network Market face?

Challenges in the Europe District Cooling Pipeline Network Market include high initial investment costs and the need for extensive infrastructure development. Additionally, regulatory hurdles and competition from alternative cooling solutions can hinder market growth.

What opportunities exist in the Europe District Cooling Pipeline Network Market?

Opportunities in the Europe District Cooling Pipeline Network Market include the integration of renewable energy sources and advancements in smart grid technology. These innovations can enhance system efficiency and reliability, making district cooling more attractive to urban planners and developers.

What trends are shaping the Europe District Cooling Pipeline Network Market?

Trends in the Europe District Cooling Pipeline Network Market include the increasing adoption of energy-efficient technologies and the rise of smart city initiatives. Additionally, there is a growing focus on sustainability and reducing greenhouse gas emissions, influencing the design and implementation of cooling systems.

Europe District Cooling Pipeline Network Market

| Segmentation Details | Description |

|---|---|

| Network Type | Piped, Free Cooling |

| Application | Residential, Commercial, Industrial |

| Country | Germany, France, Sweden, Finland, Denmark, Norway, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Europe District Cooling Pipeline Network Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.