444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe discrete semiconductor market represents a critical component of the continent’s electronics and technology infrastructure, encompassing essential electronic components that perform individual functions within electronic circuits. Discrete semiconductors include diodes, transistors, thyristors, and rectifiers that serve as fundamental building blocks for various electronic applications across automotive, industrial, consumer electronics, and telecommunications sectors. The European market demonstrates robust growth trajectory with increasing demand driven by electric vehicle adoption, renewable energy systems, and advanced industrial automation.

Market dynamics in Europe reflect the region’s commitment to technological innovation and sustainable energy solutions. The discrete semiconductor industry benefits from strong automotive sector presence, particularly in Germany, France, and Italy, where major automotive manufacturers drive demand for power management solutions. Additionally, the region’s focus on Industry 4.0 initiatives and smart manufacturing creates substantial opportunities for discrete semiconductor applications in industrial control systems and automation equipment.

Regional leadership in renewable energy adoption significantly influences market growth, with solar and wind energy installations requiring sophisticated power conversion systems utilizing discrete semiconductors. The market experiences steady expansion at approximately 6.2% CAGR, supported by increasing electrification trends and stringent energy efficiency regulations across European Union member states.

The Europe discrete semiconductor market refers to the regional industry segment focused on manufacturing, distributing, and utilizing individual semiconductor components that perform specific electronic functions within larger circuit systems. Discrete semiconductors operate as standalone components, unlike integrated circuits that combine multiple functions on a single chip, providing essential switching, amplification, and power management capabilities across diverse electronic applications.

Key characteristics of discrete semiconductors include their ability to handle high power levels, operate under extreme conditions, and provide precise control over electrical current flow. These components serve as fundamental building blocks in electronic systems, enabling everything from simple switching operations to complex power conversion processes in industrial machinery, automotive systems, and consumer electronics.

Market scope encompasses various product categories including power diodes, small signal transistors, power transistors, thyristors, and specialized components designed for specific applications. The European market particularly emphasizes high-quality standards and advanced manufacturing processes, reflecting the region’s commitment to technological excellence and reliability in semiconductor production.

Europe’s discrete semiconductor market demonstrates exceptional resilience and growth potential, driven by transformative trends in automotive electrification, renewable energy adoption, and industrial digitalization. The market benefits from strong regional manufacturing capabilities and established supply chain networks that support both domestic consumption and global export activities.

Automotive sector transformation represents the primary growth driver, with electric vehicle production requiring approximately 75% more discrete semiconductors compared to traditional internal combustion engine vehicles. This shift creates unprecedented demand for power management components, battery management systems, and charging infrastructure solutions across major European automotive manufacturing hubs.

Industrial automation initiatives further accelerate market expansion, as European manufacturers embrace smart factory concepts and advanced robotics systems. The integration of Internet of Things (IoT) technologies and artificial intelligence in manufacturing processes generates substantial demand for discrete semiconductor components in sensor systems, motor control applications, and power conversion equipment.

Renewable energy sector contributes significantly to market growth, with European Union’s commitment to carbon neutrality by 2050 driving massive investments in solar, wind, and energy storage systems. These applications require sophisticated power electronics utilizing discrete semiconductors for efficient energy conversion and grid integration capabilities.

Strategic market positioning reveals several critical insights that define the European discrete semiconductor landscape and its future trajectory:

Electric vehicle revolution stands as the most significant driver transforming the European discrete semiconductor market. The transition from internal combustion engines to electric powertrains requires sophisticated power management systems, with each electric vehicle containing substantially more discrete semiconductors for battery management, motor control, and charging systems. European automotive manufacturers’ commitment to electrification creates sustained demand growth across multiple semiconductor categories.

Industrial digitalization initiatives drive consistent market expansion as European manufacturers implement Industry 4.0 concepts and smart factory technologies. These advanced manufacturing systems require extensive semiconductor integration for sensor networks, automated control systems, and real-time data processing capabilities. The emphasis on operational efficiency and predictive maintenance creates ongoing demand for discrete components in industrial applications.

Renewable energy expansion generates substantial market opportunities as European Union member states pursue aggressive clean energy targets. Solar photovoltaic installations, wind energy systems, and energy storage solutions require sophisticated power electronics utilizing discrete semiconductors for efficient energy conversion and grid integration. The market benefits from both utility-scale projects and distributed energy resources across residential and commercial sectors.

5G infrastructure deployment creates new demand vectors for discrete semiconductors in telecommunications equipment and base station applications. The rollout of next-generation wireless networks requires advanced power management solutions and high-frequency components that support increased data transmission capabilities and network densification requirements.

Supply chain vulnerabilities present significant challenges for the European discrete semiconductor market, particularly regarding raw material availability and manufacturing capacity constraints. Global semiconductor shortages have highlighted the industry’s dependence on complex international supply networks and the potential for disruptions to impact production schedules and customer deliveries across multiple sectors.

High capital investment requirements create barriers for market entry and expansion, as semiconductor manufacturing facilities require substantial financial commitments for advanced equipment and clean room infrastructure. The need for continuous technology upgrades and process improvements demands ongoing capital allocation that may strain resources for smaller market participants.

Intense price competition from Asian manufacturers challenges European companies’ market positioning, particularly in commodity discrete semiconductor segments. Lower manufacturing costs in other regions create pricing pressures that require European companies to focus on high-value applications and differentiated product offerings to maintain competitive advantages.

Regulatory compliance complexity increases operational costs and development timelines as European manufacturers must navigate stringent environmental regulations, quality standards, and export control requirements. While these regulations ensure high product quality, they also create additional compliance burdens that impact competitiveness in global markets.

Wide bandgap semiconductor adoption presents exceptional growth opportunities as European companies invest in silicon carbide and gallium nitride technologies. These advanced materials offer superior performance characteristics including higher efficiency, faster switching speeds, and improved thermal management capabilities that enable next-generation power electronics applications across automotive and industrial sectors.

Energy storage system expansion creates substantial market potential as European countries implement large-scale battery storage projects to support renewable energy integration and grid stability. These systems require sophisticated power management solutions utilizing discrete semiconductors for battery charging, discharging, and protection functions across utility-scale and distributed storage applications.

Smart grid infrastructure development generates new demand for discrete semiconductors in advanced metering systems, grid automation equipment, and power quality management solutions. The modernization of European electrical grids requires intelligent power electronics that enable bidirectional power flow, real-time monitoring, and automated fault detection capabilities.

Aerospace and defense applications offer high-value market segments where European companies can leverage their technological expertise and quality standards. Military and space applications require radiation-hardened semiconductors and components that meet stringent reliability requirements, creating opportunities for specialized product development and premium pricing strategies.

Technology evolution drives fundamental changes in the European discrete semiconductor market as manufacturers transition toward more efficient and capable component designs. The shift from silicon-based devices to wide bandgap materials enables significant performance improvements, with silicon carbide devices offering up to 30% efficiency gains in power conversion applications compared to traditional silicon alternatives.

Customer demand patterns reflect increasing emphasis on system-level solutions rather than individual component sales. European semiconductor companies respond by developing integrated product portfolios that combine discrete components with supporting technologies, application expertise, and design services to create comprehensive solutions for target markets.

Competitive landscape evolution shows consolidation trends as companies pursue strategic acquisitions to expand technological capabilities and market reach. This consolidation enables enhanced research and development investments and improved economies of scale while creating more comprehensive product offerings for customers across multiple application segments.

Supply chain localization emerges as a critical strategic priority following global disruptions and geopolitical tensions. European companies increasingly focus on regional supply chain development and domestic manufacturing capabilities to reduce dependency on international suppliers and ensure supply security for critical applications.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the European discrete semiconductor market. The research approach combines primary data collection through industry expert interviews, customer surveys, and supplier assessments with extensive secondary research utilizing industry reports, company financial statements, and regulatory filings.

Primary research activities include structured interviews with key market participants including semiconductor manufacturers, distributors, system integrators, and end-user companies across automotive, industrial, and telecommunications sectors. These interviews provide qualitative insights into market trends, competitive dynamics, and future growth opportunities that complement quantitative data analysis.

Secondary research methodology incorporates analysis of industry publications, trade association reports, government statistics, and company annual reports to establish market sizing, growth trends, and competitive positioning. The research team validates findings through cross-reference analysis and triangulation of data sources to ensure accuracy and reliability of market assessments.

Data validation processes include expert review panels, statistical analysis of market trends, and comparison with historical performance data to identify anomalies and ensure consistency. MarkWide Research employs rigorous quality control measures throughout the research process to maintain high standards of accuracy and reliability in market analysis and forecasting.

Germany dominates the European discrete semiconductor market with approximately 35% market share, driven by its strong automotive industry presence and advanced manufacturing capabilities. German companies like Infineon Technologies lead in power semiconductor innovation, while the country’s automotive sector creates substantial demand for discrete components in electric vehicle applications and advanced driver assistance systems.

France maintains significant market presence with focus on aerospace, defense, and industrial applications. French semiconductor companies excel in specialized discrete components for high-reliability applications, while the country’s nuclear energy infrastructure creates demand for radiation-hardened semiconductors and power management solutions.

United Kingdom contributes to market growth through its strengths in telecommunications and consumer electronics sectors. Despite Brexit-related challenges, UK companies maintain important positions in RF discrete semiconductors and specialized components for wireless communication applications, supported by ongoing 5G infrastructure investments.

Italy and Netherlands represent emerging growth markets with increasing focus on renewable energy and industrial automation applications. These countries benefit from strategic geographic positioning and growing investments in solar energy systems and smart manufacturing technologies that drive discrete semiconductor demand.

Nordic countries including Sweden, Denmark, and Norway contribute to market growth through their leadership in renewable energy adoption and environmental sustainability initiatives. These markets demonstrate strong demand for power electronics in wind energy systems and electric vehicle charging infrastructure applications.

Market leadership in the European discrete semiconductor industry reflects a combination of established multinational corporations and specialized regional players that compete across different technology segments and application markets:

Competitive strategies emphasize technological innovation, manufacturing excellence, and customer-specific solution development. Leading companies invest heavily in research and development to advance wide bandgap semiconductor technologies and develop next-generation power devices that meet evolving market requirements.

Product-based segmentation reveals distinct market categories with varying growth trajectories and application focus areas:

By Product Type:

By Application:

Power semiconductor category demonstrates the strongest growth potential within the European discrete semiconductor market, driven by increasing demand for energy-efficient solutions across automotive and industrial applications. Silicon carbide power devices show particularly impressive adoption rates, with market penetration increasing by approximately 25% annually in electric vehicle applications due to their superior efficiency and thermal performance characteristics.

Automotive-specific components represent the most dynamic market segment, with specialized discrete semiconductors designed for harsh automotive environments experiencing rapid growth. These components must meet stringent AEC-Q101 qualification standards and operate reliably across extreme temperature ranges, creating premium pricing opportunities for qualified suppliers.

RF and microwave discrete semiconductors benefit from 5G infrastructure deployment and increasing wireless communication requirements. European companies maintain competitive advantages in specialized RF applications through advanced packaging technologies and custom design capabilities that address specific customer requirements in telecommunications and aerospace sectors.

Industrial automation components show consistent demand growth as European manufacturers implement smart factory concepts and advanced robotics systems. These applications require high-reliability discrete semiconductors that can operate continuously in industrial environments while providing precise control over motor drives and power conversion systems.

Manufacturers benefit from expanding market opportunities across multiple high-growth application segments, particularly in automotive electrification and renewable energy systems. The European market offers premium pricing potential for advanced discrete semiconductors that meet stringent quality and performance requirements, enabling improved profit margins compared to commodity product segments.

System integrators gain access to comprehensive discrete semiconductor portfolios that enable innovative system designs and improved performance characteristics. European suppliers provide extensive technical support and application expertise that facilitates faster time-to-market for new product developments and system optimizations.

End-user companies benefit from reliable supply chains and high-quality components that ensure system reliability and performance consistency. European discrete semiconductor suppliers offer long-term supply commitments and product lifecycle management that support multi-year product development cycles and manufacturing planning requirements.

Investors find attractive opportunities in the European discrete semiconductor market through exposure to transformative trends in automotive electrification, industrial automation, and renewable energy adoption. The market offers stable growth prospects supported by fundamental technology transitions and regulatory drivers that create sustained demand for advanced semiconductor solutions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Wide bandgap semiconductor adoption represents the most significant technological trend transforming the European discrete semiconductor market. Silicon carbide devices demonstrate superior performance in high-power applications, offering reduced switching losses and improved thermal management that enable more compact and efficient system designs across automotive and industrial applications.

System-level integration emerges as a key trend as customers seek comprehensive solutions rather than individual components. European suppliers respond by developing integrated power modules that combine multiple discrete semiconductors with supporting components and thermal management solutions to simplify system design and improve overall performance.

Sustainability focus drives demand for energy-efficient discrete semiconductors that reduce power consumption and environmental impact. European regulations and customer requirements increasingly emphasize lifecycle environmental impact, creating opportunities for companies that develop eco-friendly manufacturing processes and recyclable product designs.

Digitalization and connectivity influence discrete semiconductor design as components integrate smart features and communication capabilities. Intelligent power devices incorporate diagnostic functions and real-time monitoring capabilities that enable predictive maintenance and system optimization across industrial and automotive applications.

Strategic acquisitions reshape the competitive landscape as companies pursue complementary technologies and expanded market access. Recent consolidation activities focus on wide bandgap semiconductor capabilities and specialized application expertise that strengthen competitive positioning in high-growth market segments.

Manufacturing capacity expansion addresses growing demand across key application markets, with European companies investing in new production facilities and equipment upgrades. These investments emphasize advanced packaging technologies and automated manufacturing processes that improve efficiency and product quality while reducing production costs.

Research and development partnerships between semiconductor companies, automotive manufacturers, and research institutions accelerate innovation in next-generation discrete semiconductor technologies. These collaborations focus on application-specific solutions that address unique requirements in electric vehicles, renewable energy systems, and industrial automation applications.

Supply chain localization initiatives gain momentum as European companies seek to reduce dependency on global supply networks and ensure supply security. MWR analysis indicates increasing investment in European-based supply chain development and strategic partnerships with regional suppliers to enhance supply chain resilience.

Technology investment priorities should focus on wide bandgap semiconductor development and advanced packaging technologies that enable superior performance in high-growth applications. Companies should allocate resources toward silicon carbide and gallium nitride device development while building manufacturing capabilities that support volume production requirements.

Market positioning strategies should emphasize differentiation through application-specific solutions and comprehensive technical support rather than competing solely on price. European companies should leverage their quality advantages and customer relationships to develop premium market positions in automotive, industrial, and aerospace applications.

Supply chain development requires immediate attention to build resilient sourcing networks and reduce dependency on global supply chains. Companies should invest in regional supplier relationships and consider vertical integration opportunities that provide greater control over critical manufacturing processes and materials.

Customer engagement approaches should evolve toward system-level partnerships and collaborative development programs that create deeper customer relationships and higher switching costs. Technical support capabilities and application expertise become increasingly important competitive differentiators in complex application markets.

Long-term growth prospects for the European discrete semiconductor market remain highly positive, supported by fundamental technology transitions and regulatory drivers that create sustained demand growth. MarkWide Research projects continued market expansion driven by automotive electrification, renewable energy adoption, and industrial digitalization trends that show no signs of slowing.

Technology evolution will accelerate toward wide bandgap semiconductors and intelligent power devices that offer superior performance and integrated functionality. The market expects silicon carbide adoption to reach approximately 40% penetration in automotive power electronics applications within the next five years, driven by efficiency requirements and cost reductions through volume production.

Application market development will create new opportunities in emerging sectors including energy storage systems, electric aircraft, and advanced robotics applications. These markets require specialized discrete semiconductors with unique performance characteristics that offer premium pricing opportunities for innovative suppliers.

Competitive landscape evolution will continue toward consolidation and specialization as companies focus on core competencies and strategic market segments. The market expects increased collaboration between semiconductor suppliers and system manufacturers to develop integrated solutions that address complex application requirements and create sustainable competitive advantages.

The Europe discrete semiconductor market stands at a pivotal transformation point, driven by revolutionary changes in automotive electrification, renewable energy adoption, and industrial automation technologies. Market fundamentals remain exceptionally strong, with diverse application segments creating multiple growth vectors that support sustained expansion and innovation opportunities across the semiconductor value chain.

Technology leadership in wide bandgap semiconductors and specialized discrete components positions European companies advantageously for future market developments. The emphasis on quality, reliability, and application-specific solutions creates sustainable competitive advantages that differentiate European suppliers from low-cost global competitors while enabling premium pricing strategies in high-value market segments.

Strategic opportunities abound across automotive electrification, renewable energy systems, and industrial digitalization applications that require advanced discrete semiconductor solutions. Companies that successfully navigate supply chain challenges while investing in next-generation technologies will capture disproportionate market share and establish leadership positions in emerging high-growth segments that define the industry’s future trajectory.

What is Discrete Semiconductor?

Discrete semiconductors are individual semiconductor devices that perform specific functions, such as rectification, amplification, or switching. They are commonly used in various applications, including consumer electronics, automotive systems, and industrial equipment.

What are the key players in the Europe Discrete Semiconductor Market?

Key players in the Europe Discrete Semiconductor Market include STMicroelectronics, Infineon Technologies, NXP Semiconductors, and ON Semiconductor, among others.

What are the main drivers of the Europe Discrete Semiconductor Market?

The main drivers of the Europe Discrete Semiconductor Market include the increasing demand for energy-efficient devices, the growth of electric vehicles, and advancements in renewable energy technologies.

What challenges does the Europe Discrete Semiconductor Market face?

The Europe Discrete Semiconductor Market faces challenges such as supply chain disruptions, fluctuating raw material prices, and the need for continuous innovation to meet evolving consumer demands.

What opportunities exist in the Europe Discrete Semiconductor Market?

Opportunities in the Europe Discrete Semiconductor Market include the expansion of the Internet of Things (IoT), the rise of smart home technologies, and increasing investments in automation and robotics.

What trends are shaping the Europe Discrete Semiconductor Market?

Trends shaping the Europe Discrete Semiconductor Market include the shift towards wide bandgap semiconductors, the integration of artificial intelligence in semiconductor design, and the growing focus on sustainability and eco-friendly manufacturing processes.

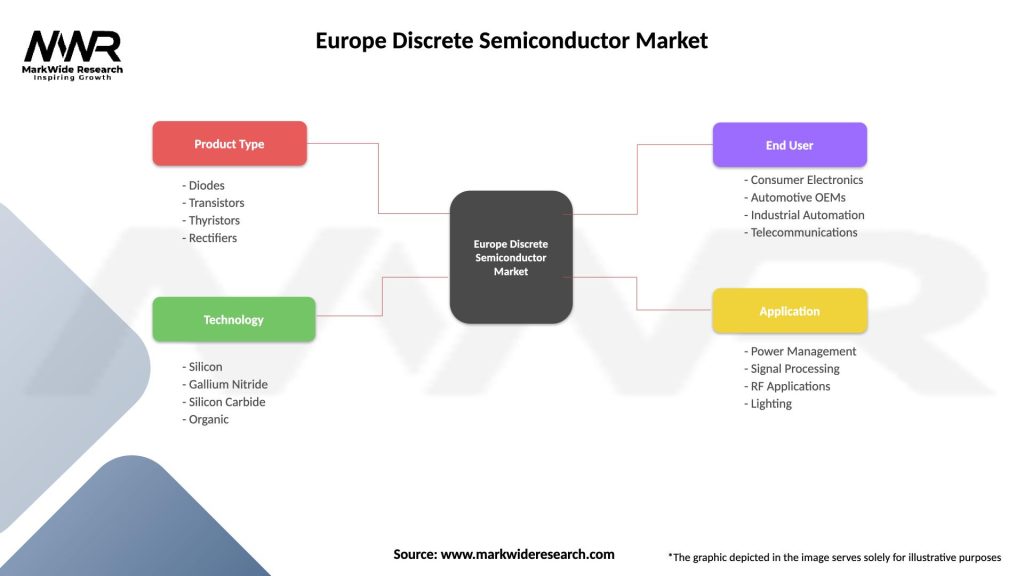

Europe Discrete Semiconductor Market

| Segmentation Details | Description |

|---|---|

| Product Type | Diodes, Transistors, Thyristors, Rectifiers |

| Technology | Silicon, Gallium Nitride, Silicon Carbide, Organic |

| End User | Consumer Electronics, Automotive OEMs, Industrial Automation, Telecommunications |

| Application | Power Management, Signal Processing, RF Applications, Lighting |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Discrete Semiconductor Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.