444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe Container Load Market represents a critical component of the continent’s logistics and transportation infrastructure, encompassing the comprehensive handling, loading, and management of containerized cargo across European ports, terminals, and inland facilities. This dynamic market serves as the backbone of international trade, facilitating the movement of goods through sophisticated container handling systems, automated loading equipment, and integrated logistics solutions that connect European markets to global supply chains.

Market dynamics indicate robust growth driven by increasing international trade volumes, port modernization initiatives, and the adoption of advanced container handling technologies. The market experiences significant demand from major European ports including Rotterdam, Hamburg, Antwerp, and Valencia, which collectively handle substantial portions of the continent’s containerized cargo. Growth projections suggest the market will expand at a 6.2% CAGR through the forecast period, supported by infrastructure investments and technological innovations.

Regional distribution shows Western European countries maintaining dominant positions, with Germany accounting for 24% market share, followed by the Netherlands at 18%, and the United Kingdom at 15%. The market encompasses various container types, loading methodologies, and specialized equipment designed to optimize cargo handling efficiency while reducing operational costs and environmental impact.

The Europe Container Load Market refers to the comprehensive ecosystem of services, technologies, and infrastructure dedicated to the efficient loading, unloading, handling, and management of containerized cargo across European logistics networks. This market encompasses container terminals, port facilities, inland container depots, specialized loading equipment, and integrated software solutions that facilitate seamless cargo movement from origin to destination.

Container loading operations involve sophisticated processes including container positioning, cargo securing, weight distribution optimization, and documentation management. The market includes various stakeholders such as port operators, terminal management companies, container handling equipment manufacturers, logistics service providers, and technology solution developers who collectively ensure efficient cargo flow throughout European trade corridors.

Strategic analysis reveals the Europe Container Load Market as a rapidly evolving sector characterized by technological advancement, infrastructure modernization, and increasing automation adoption. The market benefits from Europe’s strategic geographic position as a gateway between global markets, with major ports serving as critical transshipment hubs for international trade.

Key market drivers include growing e-commerce volumes, which have increased container throughput by 12% annually, expanding manufacturing activities, and enhanced port connectivity through improved rail and road networks. The market demonstrates resilience through diversified service offerings, ranging from traditional container handling to specialized solutions for temperature-controlled cargo, hazardous materials, and oversized containers.

Technological integration plays a pivotal role, with automated container handling systems, IoT-enabled tracking solutions, and artificial intelligence-driven optimization platforms transforming operational efficiency. Market participants are investing heavily in digital transformation initiatives to enhance cargo visibility, reduce handling times, and improve overall supply chain performance.

Market intelligence reveals several critical insights shaping the Europe Container Load Market landscape:

International trade growth serves as the primary catalyst for Europe Container Load Market expansion, with increasing import and export volumes driving demand for efficient container handling solutions. The market benefits from Europe’s position as a major trading bloc, with containerized cargo volumes showing consistent growth across key trade routes connecting European markets to Asia, North America, and emerging economies.

E-commerce expansion significantly impacts market dynamics, as online retail growth necessitates sophisticated container handling capabilities to manage diverse cargo types, varying shipment sizes, and accelerated delivery requirements. The rise of omnichannel distribution strategies requires flexible container loading solutions that can accommodate both bulk shipments and smaller, more frequent deliveries.

Port modernization initiatives across Europe are driving substantial investments in container handling infrastructure, with governments and private operators collaborating to enhance port capacity, efficiency, and competitiveness. These initiatives include terminal expansion projects, equipment upgrades, and technology integration programs that collectively strengthen the container load market foundation.

Technological advancement continues to transform container handling operations through automation, digitalization, and intelligent systems integration. Advanced container handling equipment, real-time tracking solutions, and predictive maintenance technologies are improving operational efficiency while reducing costs and environmental impact.

Infrastructure limitations present significant challenges for market growth, particularly in older European ports where space constraints and aging facilities limit expansion opportunities. The high capital requirements for port modernization and container handling equipment upgrades can strain financial resources and delay necessary improvements.

Regulatory complexity across different European jurisdictions creates operational challenges for container handling companies operating in multiple markets. Varying safety standards, environmental regulations, and customs procedures can complicate cross-border container movements and increase compliance costs.

Labor market dynamics pose ongoing challenges, as the transition toward automated container handling systems requires significant workforce retraining while potentially reducing traditional employment opportunities. Skilled labor shortages in technical and operational roles can limit the implementation of advanced container handling technologies.

Environmental pressures are intensifying, with stricter emissions regulations and sustainability requirements increasing operational costs and necessitating investments in cleaner technologies. The need to balance operational efficiency with environmental responsibility creates complex decision-making scenarios for market participants.

Digital transformation presents substantial opportunities for market expansion through the development and implementation of advanced container management systems, IoT-enabled tracking solutions, and artificial intelligence-driven optimization platforms. These technologies can significantly improve operational efficiency, reduce costs, and enhance customer service capabilities.

Sustainable solutions offer promising growth avenues as European markets increasingly prioritize environmental responsibility. Opportunities exist for developing electric container handling equipment, renewable energy integration, and carbon-neutral container operations that align with European Union sustainability objectives.

Emerging markets integration provides expansion opportunities as European container handling companies can leverage their expertise to support infrastructure development in growing economies. Technical consulting, equipment supply, and operational management services represent significant revenue potential in international markets.

Specialized cargo handling creates niche opportunities for companies developing expertise in temperature-controlled containers, hazardous materials handling, and oversized cargo management. These specialized services typically command premium pricing and offer higher profit margins than standard container handling operations.

Competitive intensity within the Europe Container Load Market continues to increase as established players expand their service offerings while new entrants introduce innovative technologies and business models. Market dynamics are characterized by ongoing consolidation among terminal operators, strategic partnerships between technology providers and port operators, and increasing collaboration between public and private sector stakeholders.

Technology adoption rates vary significantly across European markets, with Northern European ports generally leading in automation and digitalization while Southern and Eastern European facilities are rapidly modernizing their operations. This technological disparity creates both challenges and opportunities for market participants seeking to standardize operations across multiple locations.

Supply chain integration is becoming increasingly important as container handling operations must seamlessly connect with broader logistics networks. The market is evolving toward more integrated service offerings that combine container handling with warehousing, distribution, and value-added services to provide comprehensive supply chain solutions.

Customer expectations are rising, with shippers demanding greater visibility, faster processing times, and more flexible service options. These evolving requirements are driving innovation in container handling processes and technology solutions while creating pressure for continuous operational improvement.

Comprehensive market analysis employs a multi-faceted research approach combining primary and secondary data sources to provide accurate and actionable insights into the Europe Container Load Market. The methodology encompasses quantitative analysis of market trends, qualitative assessment of industry dynamics, and strategic evaluation of competitive landscapes.

Primary research activities include structured interviews with industry executives, port operators, terminal managers, and technology providers to gather firsthand insights into market conditions, challenges, and opportunities. Survey data collection from market participants provides quantitative validation of market trends and performance indicators.

Secondary research incorporates analysis of industry publications, government statistics, trade association reports, and company financial statements to establish market baselines and validate primary research findings. MarkWide Research analysts utilize proprietary databases and analytical tools to process and interpret complex market data.

Data validation processes ensure research accuracy through cross-referencing multiple sources, statistical analysis of data consistency, and expert review of findings. The methodology includes scenario analysis and sensitivity testing to account for market uncertainties and provide robust forecasting capabilities.

Western Europe dominates the container load market, with major ports in the Netherlands, Germany, and Belgium handling significant portions of European container traffic. The Netherlands maintains 22% market share, driven by Rotterdam’s position as Europe’s largest port and its advanced container handling capabilities. German ports, particularly Hamburg and Bremen, contribute substantially to market volumes through their strategic locations and excellent inland connectivity.

Southern Europe represents a growing market segment, with Spanish and Italian ports expanding their container handling capacities to serve Mediterranean trade routes. Valencia, Barcelona, and Genoa are investing heavily in modernization projects to enhance their competitive positions and capture increasing trade volumes with North Africa and the Middle East.

Northern Europe maintains strong market positions through the ports of Gothenburg, Copenhagen, and Helsinki, which serve as important gateways for Scandinavian and Baltic trade. These ports are pioneering sustainable container handling practices and advanced automation technologies that set industry standards for environmental responsibility.

Eastern Europe presents significant growth opportunities as ports in Poland, Romania, and the Baltic states modernize their facilities and expand container handling capabilities. Market growth in this region exceeds 8% annually, driven by increasing trade volumes and infrastructure investments supported by European Union development programs.

Market leadership is distributed among several categories of companies, including global terminal operators, specialized equipment manufacturers, and technology solution providers. The competitive landscape is characterized by ongoing consolidation, strategic partnerships, and continuous innovation in container handling technologies and services.

Major terminal operators include:

Equipment manufacturers play crucial roles in market development through the supply of advanced container handling equipment, including ship-to-shore cranes, rubber-tired gantry cranes, and automated guided vehicles. Leading manufacturers are investing heavily in electric and hybrid technologies to meet environmental requirements while improving operational efficiency.

Technology providers are increasingly important as container handling operations become more digitalized and automated. Companies specializing in terminal operating systems, container tracking solutions, and optimization software are experiencing strong demand as ports seek to enhance their operational capabilities.

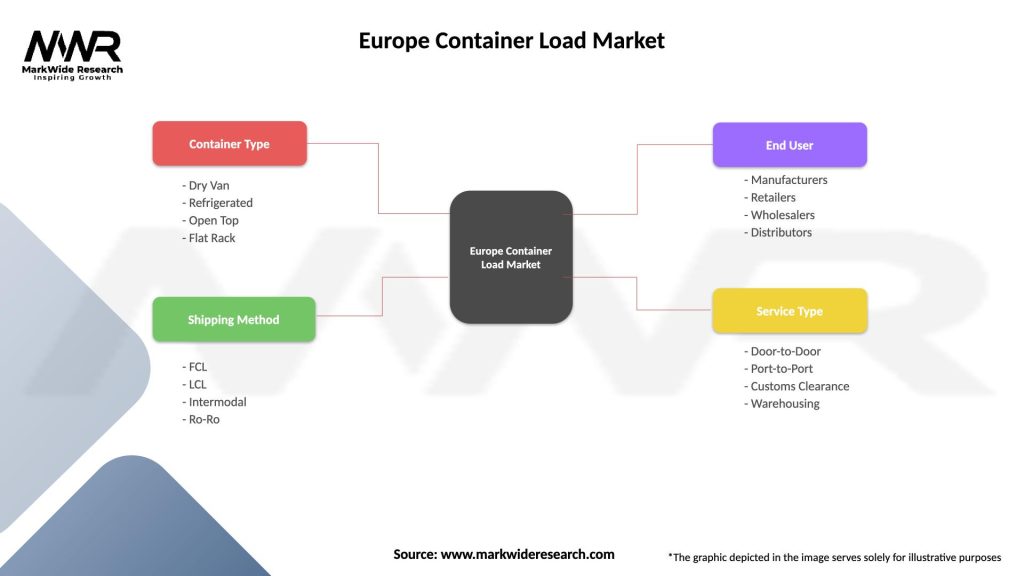

By Container Type:

By Equipment Type:

By End-User:

Dry container handling represents the largest market segment, accounting for approximately 78% of total container volumes across European ports. This category benefits from standardized handling procedures, established infrastructure, and economies of scale that enable efficient operations. Market growth is driven by increasing general cargo volumes and the expansion of manufacturing activities across Europe.

Refrigerated container operations constitute a high-value market segment with specialized requirements for temperature monitoring, power supply management, and rapid processing to maintain cargo integrity. European ports are investing in dedicated reefer facilities and advanced monitoring systems to capture growing demand from food, pharmaceutical, and chemical industries.

Automated container handling is experiencing rapid adoption as European ports seek to improve efficiency, reduce labor costs, and enhance safety performance. Automation implementation rates have increased by 28% over recent years, with major terminals investing in automated stacking cranes, guided vehicles, and integrated control systems.

Specialized cargo handling presents premium opportunities for ports and terminal operators capable of managing complex container types, including tank containers, open-top units, and oversized cargo. These services typically command higher rates and provide differentiation opportunities in competitive markets.

Operational efficiency gains represent primary benefits for industry participants, with modern container handling systems delivering significant improvements in processing speed, accuracy, and resource utilization. Advanced equipment and technology integration enable ports to handle larger volumes with reduced labor requirements while maintaining high service quality standards.

Cost optimization opportunities emerge through economies of scale, automated operations, and integrated service offerings that reduce per-container handling costs. Participants can achieve better asset utilization, lower maintenance expenses, and improved energy efficiency through modern container handling solutions.

Competitive advantages accrue to companies investing in advanced container handling capabilities, including faster vessel turnaround times, enhanced cargo security, and superior customer service. These advantages translate into market share growth, premium pricing opportunities, and stronger customer relationships.

Sustainability benefits include reduced environmental impact through electric equipment adoption, optimized operations that minimize energy consumption, and improved air quality around port facilities. These benefits support regulatory compliance while enhancing corporate social responsibility profiles.

Stakeholder value creation extends beyond direct participants to include shipping lines benefiting from efficient port operations, importers and exporters enjoying reliable cargo handling, and regional economies gaining from enhanced trade facilitation capabilities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Automation acceleration continues as a dominant trend, with European ports implementing increasingly sophisticated automated container handling systems. This trend encompasses automated stacking cranes, autonomous vehicle systems, and integrated terminal operating systems that optimize container movements while reducing labor requirements and improving safety performance.

Sustainability integration is becoming central to container handling operations, with ports investing in electric equipment, renewable energy systems, and carbon-neutral operational practices. This trend responds to regulatory requirements and customer demands for environmentally responsible logistics solutions.

Digital connectivity enhancement involves implementing IoT sensors, real-time tracking systems, and blockchain-based documentation to improve cargo visibility and streamline administrative processes. These technologies enable better coordination between stakeholders and enhance overall supply chain efficiency.

Mega-ship accommodation drives infrastructure investments as ports modify facilities to handle increasingly large container vessels. This trend requires deeper berths, taller cranes, and enhanced inland connectivity to manage the concentrated cargo volumes from ultra-large container ships.

Service integration sees container handling companies expanding their offerings to include warehousing, distribution, and value-added services. This trend creates comprehensive logistics solutions that provide greater customer value while generating additional revenue streams.

Infrastructure investments across European ports are reaching unprecedented levels, with major expansion projects underway at Rotterdam, Hamburg, Antwerp, and other key facilities. These investments focus on increasing capacity, improving efficiency, and accommodating larger vessels while incorporating advanced automation technologies.

Technology partnerships between port operators and technology companies are accelerating innovation in container handling solutions. Recent collaborations have produced advanced terminal operating systems, predictive maintenance platforms, and autonomous equipment that significantly improve operational performance.

Regulatory developments include new environmental standards, safety requirements, and digitalization mandates that are reshaping container handling operations. MWR analysis indicates these regulations are driving substantial investments in cleaner technologies and digital systems across the industry.

Market consolidation continues as larger operators acquire smaller terminals and specialized service providers to expand their geographic coverage and service capabilities. This consolidation trend is creating more integrated and efficient container handling networks across Europe.

Sustainability initiatives are expanding beyond equipment electrification to include comprehensive carbon reduction programs, circular economy practices, and biodiversity protection measures. These initiatives demonstrate the industry’s commitment to environmental responsibility while meeting stakeholder expectations.

Strategic positioning recommendations emphasize the importance of investing in automation and digitalization to maintain competitive advantages in the evolving container handling landscape. Companies should prioritize technology adoption while ensuring adequate workforce training and change management support.

Market expansion strategies should focus on developing specialized capabilities in high-value segments such as refrigerated cargo handling, hazardous materials management, and oversized container operations. These segments offer premium pricing opportunities and reduced competitive pressure.

Sustainability integration should be approached as a strategic imperative rather than a compliance requirement, with companies developing comprehensive environmental programs that create competitive advantages while meeting regulatory requirements. Early adoption of sustainable practices can provide market differentiation and cost advantages.

Partnership development recommendations include forming strategic alliances with technology providers, logistics companies, and other stakeholders to create integrated service offerings and share investment risks. Collaborative approaches can accelerate innovation while reducing individual company exposure.

Investment prioritization should focus on technologies and capabilities that provide measurable returns on investment while supporting long-term strategic objectives. Companies should carefully evaluate automation investments to ensure they align with operational requirements and market conditions.

Market evolution projections indicate continued growth driven by increasing trade volumes, technological advancement, and infrastructure modernization across European container handling facilities. The market is expected to maintain robust expansion with projected growth rates of 6.5% annually through the next decade, supported by ongoing investments and operational improvements.

Technology transformation will accelerate, with artificial intelligence, machine learning, and advanced automation becoming standard components of container handling operations. These technologies will enable predictive maintenance, optimized resource allocation, and enhanced decision-making capabilities that significantly improve operational performance.

Sustainability requirements will intensify, driving further investments in clean technologies, renewable energy integration, and carbon-neutral operations. MarkWide Research projects that environmental considerations will become primary factors in equipment selection and operational planning decisions.

Market consolidation is likely to continue as companies seek economies of scale, expanded geographic coverage, and enhanced service capabilities. This consolidation will create larger, more integrated container handling networks capable of serving complex customer requirements across multiple markets.

Service innovation will expand beyond traditional container handling to include comprehensive logistics solutions, real-time cargo monitoring, and predictive analytics services. These value-added offerings will become increasingly important for maintaining competitive positions and generating premium revenues.

The Europe Container Load Market represents a dynamic and essential component of the continent’s logistics infrastructure, characterized by ongoing technological advancement, sustainability integration, and operational optimization. Market participants are successfully adapting to evolving customer requirements, regulatory changes, and competitive pressures through strategic investments in automation, digitalization, and service enhancement.

Growth prospects remain positive, supported by increasing trade volumes, infrastructure modernization, and the adoption of advanced container handling technologies. The market’s resilience and adaptability have been demonstrated through recent global challenges, positioning it well for continued expansion and development.

Strategic success in this market requires balanced approaches that combine operational excellence, technological innovation, and environmental responsibility. Companies that effectively integrate these elements while maintaining focus on customer service and cost efficiency will be best positioned to capitalize on emerging opportunities and navigate future challenges in the evolving European container load market landscape.

What is Container Load?

Container Load refers to the transportation of goods in large containers, typically used in shipping and logistics. This method is efficient for moving bulk items across various industries, including retail, manufacturing, and agriculture.

What are the key players in the Europe Container Load Market?

Key players in the Europe Container Load Market include Maersk, MSC, and Hapag-Lloyd, which are known for their extensive shipping networks and container services. These companies play a significant role in facilitating international trade and logistics, among others.

What are the main drivers of the Europe Container Load Market?

The main drivers of the Europe Container Load Market include the growth of e-commerce, increasing demand for efficient supply chain solutions, and the expansion of global trade. These factors contribute to a higher volume of goods being transported via container shipping.

What challenges does the Europe Container Load Market face?

The Europe Container Load Market faces challenges such as port congestion, fluctuating fuel prices, and regulatory compliance issues. These factors can impact shipping schedules and operational costs for logistics companies.

What opportunities exist in the Europe Container Load Market?

Opportunities in the Europe Container Load Market include advancements in digital logistics technologies, increased sustainability initiatives, and the potential for expanding trade routes. These developments can enhance efficiency and reduce environmental impact.

What trends are shaping the Europe Container Load Market?

Trends shaping the Europe Container Load Market include the adoption of automation in shipping processes, the rise of green logistics practices, and the integration of data analytics for better decision-making. These trends are transforming how goods are transported and managed.

Europe Container Load Market

| Segmentation Details | Description |

|---|---|

| Container Type | Dry Van, Refrigerated, Open Top, Flat Rack |

| Shipping Method | FCL, LCL, Intermodal, Ro-Ro |

| End User | Manufacturers, Retailers, Wholesalers, Distributors |

| Service Type | Door-to-Door, Port-to-Port, Customs Clearance, Warehousing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Container Load Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.