444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

Egypt’s oil and gas midstream market plays a critical role in the country’s energy sector. The midstream sector refers to the infrastructure and activities involved in the transportation, storage, and processing of oil and gas products. It serves as a crucial link between the upstream production and downstream distribution of oil and gas resources. The midstream market in Egypt has witnessed significant growth over the years, driven by the country’s strategic location, abundant hydrocarbon reserves, and government initiatives to attract foreign investment.

Meaning

The term “oil and gas midstream” refers to the various stages and processes involved in the transportation, storage, and processing of oil and gas resources. This includes pipelines, terminals, storage facilities, and transportation systems that enable the movement of crude oil, natural gas, and petroleum products from production sites to refineries, petrochemical plants, and end consumers. The midstream sector acts as a bridge between the upstream exploration and production activities and the downstream refining and distribution processes.

Executive Summary

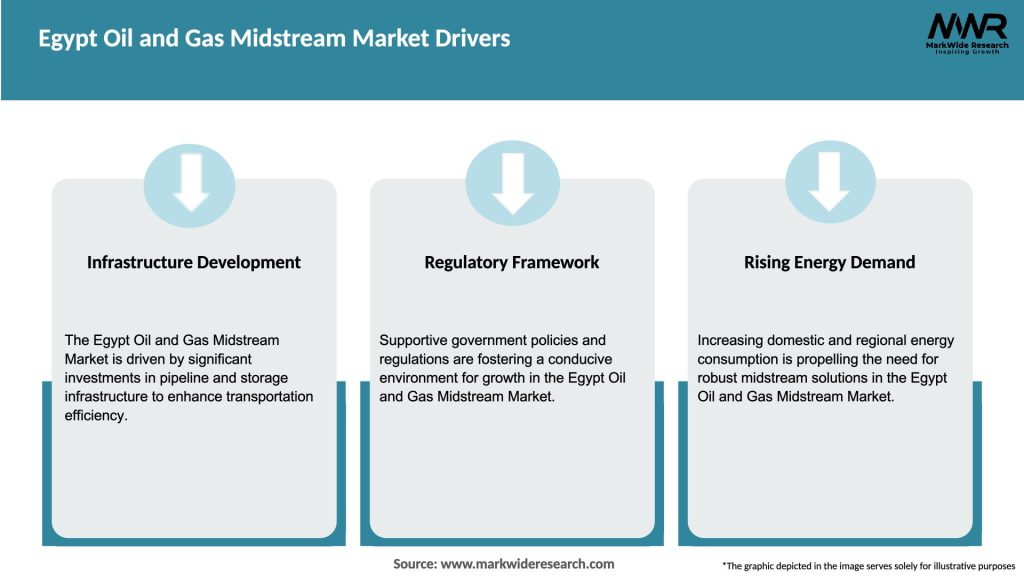

The Egypt oil and gas midstream market is experiencing significant growth, driven by several factors. The country’s strategic location, with access to major shipping routes and proximity to key oil and gas markets, positions it as a hub for energy transportation and storage. Egypt also boasts substantial hydrocarbon reserves, making it an attractive destination for international oil and gas companies. The government has implemented various initiatives to encourage foreign investment and promote the development of the midstream sector. However, challenges such as regulatory complexities, infrastructure constraints, and geopolitical risks need to be addressed to fully unlock the market’s potential.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The Egypt oil and gas midstream market is characterized by intense competition among market players, both domestic and international. The industry is witnessing collaborations and partnerships between local companies and global giants to leverage each other’s expertise and resources. The market dynamics are influenced by factors such as geopolitical developments, changes in energy policies, technological advancements, and market demand. The ongoing shift towards cleaner energy sources and the need for sustainability are also shaping the market dynamics, driving investments in renewable energy infrastructure and cleaner midstream operations.

Regional Analysis

The Egypt oil and gas midstream market is concentrated in key regions with significant hydrocarbon reserves and infrastructure. The Nile Delta region and the Western Desert are the primary areas of oil and gas production. The Mediterranean coast serves as a critical location for LNG terminals and export facilities. Cairo, the capital city, acts as a hub for administrative functions and hosts several major players in the midstream sector. The Suez Canal and the Red Sea coast are vital routes for oil and gas transportation, connecting the Mediterranean with the Indian Ocean and the Arabian Sea.

Competitive Landscape

Leading Companies in the Egypt Oil and Gas Midstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

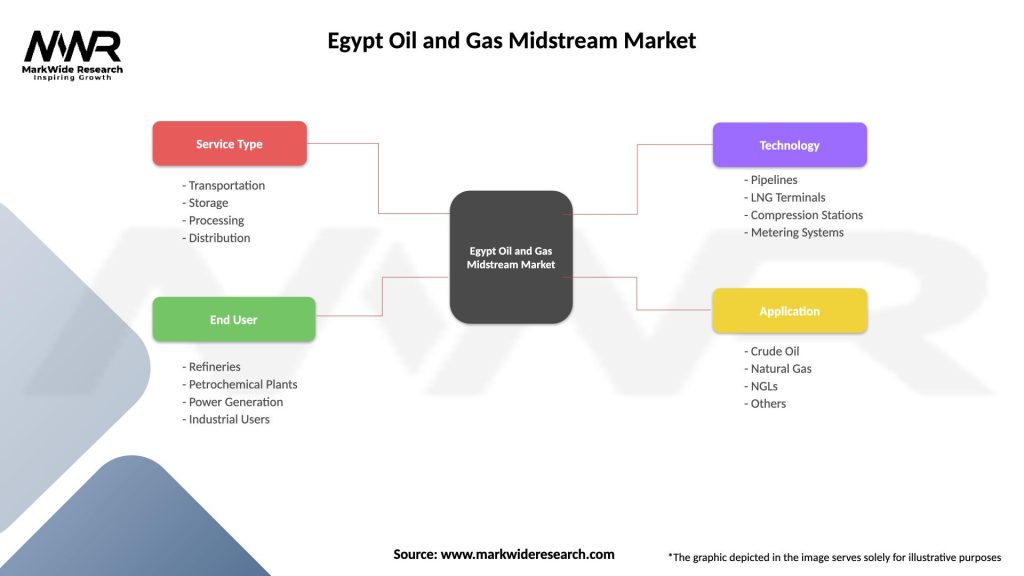

The Egypt oil and gas midstream market can be segmented based on various factors, including infrastructure type, product type, and end-use industry. Infrastructure types include pipelines, storage facilities, LNG terminals, and transportation systems. Product types encompass crude oil, natural gas, petroleum products, and liquefied natural gas. End-use industries that rely on midstream infrastructure include power generation, petrochemicals, transportation, and residential and commercial sectors.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic had a significant impact on the global oil and gas industry, including the midstream sector in Egypt. The pandemic led to a decline in oil and gas demand, disruptions in supply chains, and economic uncertainties. However, the midstream sector demonstrated resilience and adapted to the changing market dynamics. The pandemic accelerated digitalization efforts, highlighted the importance of sustainability, and prompted companies to reassess their operational strategies. As the world recovers from the pandemic, the midstream sector is expected to rebound, driven by increasing energy demand and the gradual restoration of global economic activities.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future outlook for the Egypt oil and gas midstream market is promising. The country’s strategic location, abundant hydrocarbon reserves, and government initiatives to attract investment create a conducive environment for market growth. The expansion of midstream infrastructure, including pipelines, storage facilities, and LNG terminals, will facilitate the efficient transportation and export of oil and gas resources. The integration of renewable energy sources and the adoption of sustainable practices will drive the industry towards a cleaner and more resilient future. However, challenges such as regulatory complexities, infrastructure constraints, and geopolitical risks need to be addressed to unlock the market’s full potential.

Conclusion

The Egypt oil and gas midstream market is witnessing significant growth and offers lucrative opportunities for industry participants and stakeholders. The market is driven by abundant hydrocarbon reserves, government support, and growing energy demand. However, challenges such as regulatory complexities, infrastructure constraints, and geopolitical risks need to be overcome. Investment in infrastructure expansion, technological advancements, and sustainability measures will shape the future of the midstream sector in Egypt. With strategic initiatives and collaborations, Egypt is poised to strengthen its position as a regional hub for oil and gas transportation, storage, and processing, contributing to the country’s economic growth and energy security.

What is Oil and Gas Midstream?

Oil and Gas Midstream refers to the sector involved in the transportation, storage, and processing of oil and gas products. This includes pipelines, storage facilities, and processing plants that connect upstream production with downstream distribution.

What are the key players in the Egypt Oil and Gas Midstream Market?

Key players in the Egypt Oil and Gas Midstream Market include Egyptian Natural Gas Holding Company (EGAS), Petrojet, and the Suez Canal Authority, among others. These companies play significant roles in the transportation and storage of oil and gas resources in the region.

What are the growth factors driving the Egypt Oil and Gas Midstream Market?

The growth of the Egypt Oil and Gas Midstream Market is driven by increasing energy demand, investments in infrastructure, and the discovery of new oil and gas reserves. Additionally, government initiatives to enhance energy security contribute to market expansion.

What challenges does the Egypt Oil and Gas Midstream Market face?

The Egypt Oil and Gas Midstream Market faces challenges such as regulatory hurdles, geopolitical instability, and aging infrastructure. These factors can hinder investment and operational efficiency in the sector.

What opportunities exist in the Egypt Oil and Gas Midstream Market?

Opportunities in the Egypt Oil and Gas Midstream Market include the potential for new pipeline projects, advancements in technology for more efficient transportation, and increased foreign investment. These factors can enhance the overall capacity and reliability of the midstream sector.

What trends are shaping the Egypt Oil and Gas Midstream Market?

Trends in the Egypt Oil and Gas Midstream Market include the adoption of digital technologies for monitoring and management, a focus on sustainability practices, and the integration of renewable energy sources. These trends aim to improve efficiency and reduce environmental impact.

Egypt Oil and Gas Midstream Market

| Segmentation Details | Description |

|---|---|

| Service Type | Transportation, Storage, Processing, Distribution |

| End User | Refineries, Petrochemical Plants, Power Generation, Industrial Users |

| Technology | Pipelines, LNG Terminals, Compression Stations, Metering Systems |

| Application | Crude Oil, Natural Gas, NGLs, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Egypt Oil and Gas Midstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.