444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Genetic Testing Market")

Market Overview

Direct-to-Consumer (DTC) genetic testing has emerged as a prominent industry in recent years, revolutionizing the way people access and understand their genetic information. This market offers individuals the opportunity to explore their genetic makeup and gain insights into their ancestry, health traits, and potential genetic predispositions. DTC genetic testing enables consumers to bypass traditional healthcare providers and directly engage with genetic testing companies, making it a convenient and accessible option for many individuals.

Meaning

Direct-to-Consumer (DTC) genetic testing refers to the process of individuals ordering and accessing genetic tests without the involvement of healthcare professionals or medical intermediaries. These tests typically involve collecting a DNA sample, either through a saliva or cheek swab, and sending it to a laboratory for analysis. The results are then made available directly to the consumer through an online platform or application. DTC genetic testing provides individuals with personalized information about their genetic traits, health risks, and ancestral origins.

Executive Summary

The DTC genetic testing market has witnessed significant growth in recent years, driven by increasing consumer interest in understanding their genetic information. The ease of access, affordability, and privacy offered by DTC genetic testing have fueled its adoption worldwide. Consumers are increasingly seeking personalized healthcare solutions, and DTC genetic testing provides them with valuable insights that can guide their lifestyle choices and healthcare decisions. However, the market also faces certain challenges and regulatory considerations that need to be addressed to ensure its responsible and ethical use.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

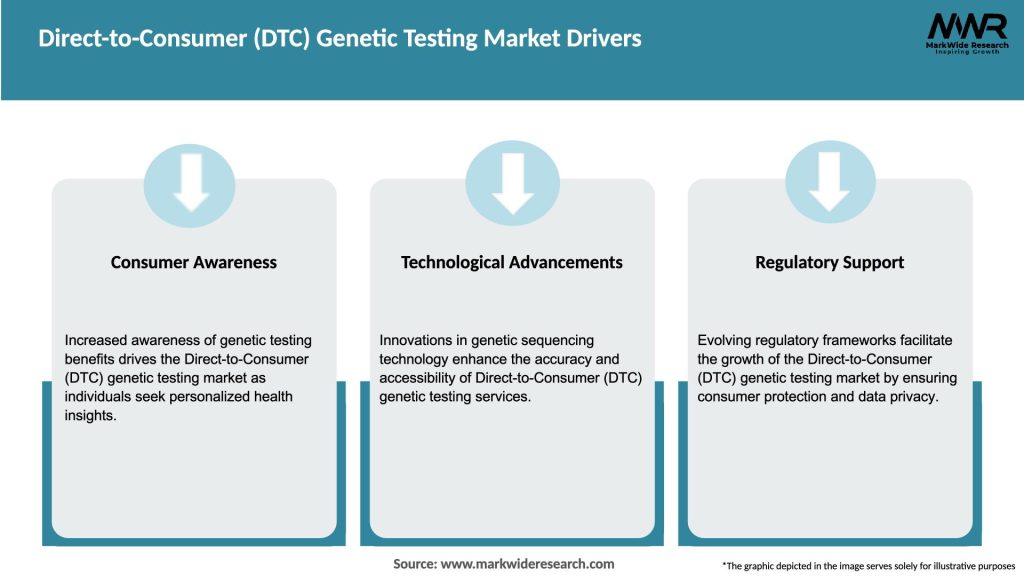

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The DTC genetic testing market is dynamic and evolving, influenced by various factors, including technological advancements, consumer preferences, regulatory changes, and competitive dynamics. It is essential for market players to stay abreast of these dynamics and adapt their strategies to maintain a competitive edge. Continuous innovation, responsible marketing practices, and building consumer trust are crucial for long-term success in this rapidly evolving market.

Regional Analysis

The DTC genetic testing market is experiencing robust growth across various regions, including North America, Europe, Asia Pacific, and Latin America. North America currently holds a significant market share, driven by the presence of key market players, high consumer awareness, and favorable regulatory frameworks. Europe is also witnessing substantial growth, with increasing adoption of DTC genetic testing in countries such as the United Kingdom, Germany, and France. The Asia Pacific region is emerging as a lucrative market, driven by a large consumer base, rising disposable incomes, and increasing healthcare awareness.

Competitive Landscape

Leading Companies in Direct-to-Consumer (DTC) Genetic Testing Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

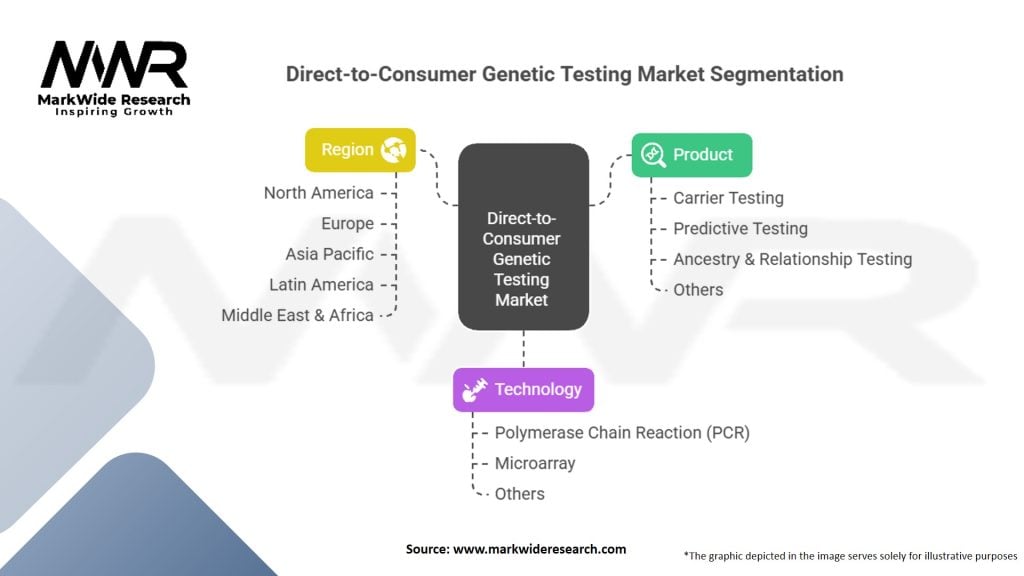

Segmentation

The DTC genetic testing market can be segmented based on test type, application, and region.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Consumer Empowerment: Personalized ancestry, health risk, and trait insights drive engagement.

Scalable Business Model: High volumes of mail-in kits and digital reporting reduce marginal costs.

Data Assets: Large genomic databases fuel R&D and targeted service expansions.

Weaknesses:

Privacy Concerns: Potential misuse or data breaches erode consumer trust.

Regulatory Scrutiny: Varying oversight on health claims and laboratory standards.

Interpretation Limitations: Genetic risk does not guarantee disease, leading to misinterpretation.

Opportunities:

Preventive Healthcare Partnerships: Integration with telehealth and wellness platforms for actionable follow-through.

Expansion into Pharmacogenomics: Drug-response testing for personalized medicine adoption.

International Growth: Emerging markets with growing health-awareness populations.

Threats:

Tightening Regulations: Stricter FDA/EMA rules on health-related tests may limit offerings.

Competitive Pressure: Traditional labs and tech giants entering the DTC space.

Ethical Debates: Concerns over genetic discrimination and informed consent.

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic has had both positive and negative impacts on the DTC genetic testing market. On one hand, the pandemic has heightened public awareness of the importance of health and well-being, leading to increased interest in genetic testing. Consumers are seeking information about potential genetic factors influencing susceptibility to the virus or other health conditions. On the other hand, the pandemic has disrupted supply chains, delayed testing processes, and affected consumer purchasing power, impacting the market’s growth.

Key Industry Developments

Analyst Suggestions

Future Outlook

The DTC genetic testing market is expected to continue its growth trajectory in the coming years. Advances in genetic technology, increasing consumer awareness, and the rising demand for personalized healthcare solutions are driving market expansion. However, regulatory considerations, ethical implications, and the responsible use of genetic information will remain key challenges that need to be addressed. Collaboration with healthcare providers, integration of AI technologies, and a focus on data privacy and security will shape the future of the DTC genetic testing market.

Conclusion

The Direct-to-Consumer (DTC) genetic testing market has transformed the way individuals access and interpret their genetic information. It offers convenience, affordability, and personalized insights that empower consumers to make informed decisions about their health and well-being. While the market presents significant opportunities for industry participants, it also faces regulatory challenges and ethical considerations. The future of the DTC genetic testing market lies in continuous innovation, responsible integration of genetic information into healthcare systems, and building consumer trust through data privacy and security measures.

What is Direct-to-Consumer (DTC) Genetic Testing?

Direct-to-Consumer (DTC) Genetic Testing refers to genetic tests that are marketed directly to consumers, allowing individuals to access their genetic information without the need for a healthcare provider. These tests can provide insights into ancestry, health risks, and traits based on genetic data.

What are the key companies in the Direct-to-Consumer (DTC) Genetic Testing Market?

Key companies in the Direct-to-Consumer (DTC) Genetic Testing Market include 23andMe, AncestryDNA, MyHeritage, and Invitae, among others.

What are the growth factors driving the Direct-to-Consumer (DTC) Genetic Testing Market?

The growth of the Direct-to-Consumer (DTC) Genetic Testing Market is driven by increasing consumer interest in personalized health, advancements in genetic technology, and the rising demand for ancestry-related services. Additionally, the convenience of at-home testing kits contributes to market expansion.

What challenges does the Direct-to-Consumer (DTC) Genetic Testing Market face?

Challenges in the Direct-to-Consumer (DTC) Genetic Testing Market include concerns over data privacy, the accuracy of test results, and the potential for misinterpretation of genetic information. Regulatory uncertainties also pose challenges for companies operating in this space.

What opportunities exist in the Direct-to-Consumer (DTC) Genetic Testing Market?

Opportunities in the Direct-to-Consumer (DTC) Genetic Testing Market include the potential for expanding into new health-related testing areas, partnerships with healthcare providers, and the development of more comprehensive testing services. Additionally, increasing consumer awareness presents growth potential.

What trends are shaping the Direct-to-Consumer (DTC) Genetic Testing Market?

Trends in the Direct-to-Consumer (DTC) Genetic Testing Market include the integration of artificial intelligence for data analysis, the rise of subscription-based models for ongoing genetic insights, and a growing focus on health and wellness applications. These trends are influencing how consumers engage with genetic testing services.

Direct-to-Consumer (DTC) Genetic Testing Market

| Segmentation Details | Description |

|---|---|

| Product | Carrier Testing, Predictive Testing, Ancestry & Relationship Testing, Others |

| Technology | Polymerase Chain Reaction (PCR), Microarray, Others |

| Region | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Direct-to-Consumer (DTC) Genetic Testing Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA