The Direct Reduced Iron (DRI) market is a vital component of the steel industry, providing an alternative iron source to traditional blast furnaces. Direct Reduced Iron, also known as sponge iron, is produced through the reduction of iron ore using natural gas or coal-based processes. DRI serves as a high-quality feedstock for electric arc furnaces (EAFs) in steelmaking, offering several advantages such as lower greenhouse gas emissions, reduced energy consumption, and enhanced steel quality.

Meaning

Direct Reduced Iron (DRI) refers to a form of iron produced by the reduction of iron ore using a reducing gas generated from natural gas or coal. This process occurs outside the traditional blast furnace route and is characterized by its simplicity and environmental benefits. DRI is typically used as a feedstock in electric arc furnaces (EAFs) for steelmaking, contributing to the production of high-quality steel with lower energy consumption and greenhouse gas emissions compared to conventional methods.

Executive Summary

The Direct Reduced Iron (DRI) market has witnessed significant growth driven by factors such as increasing steel production, growing demand for cleaner steelmaking technologies, and rising environmental concerns. The market offers lucrative opportunities for industry participants, but it also faces challenges related to raw material availability, energy costs, and regulatory compliance. Understanding key market insights, technological advancements, and competitive dynamics is crucial for stakeholders to capitalize on emerging trends and sustain growth in the DRI sector.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

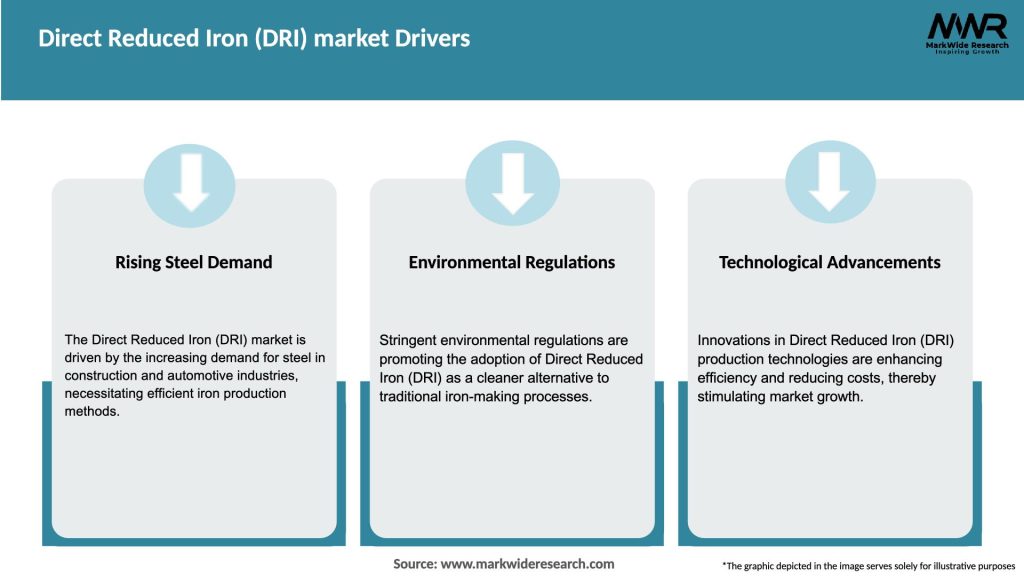

Growing Steel Production: The global demand for steel continues to rise, driving the need for alternative ironmaking processes like Direct Reduced Iron (DRI) to meet steelmakers’ requirements.

Environmental Regulations: Stringent environmental regulations and carbon emission reduction targets have prompted steel producers to adopt cleaner and more sustainable production methods, including DRI technology.

Raw Material Availability: Access to iron ore reserves and natural gas resources plays a critical role in the development and expansion of the DRI market. Regions with abundant natural gas reserves have a competitive advantage in DRI production.

Technological Advancements: Ongoing research and development efforts are focused on enhancing DRI production efficiency, reducing energy consumption, and minimizing environmental impact through process innovations and technology upgrades.

Market Drivers

Environmental Sustainability: The environmental benefits of DRI, such as lower carbon footprint and reduced greenhouse gas emissions, drive its adoption as a preferred ironmaking method among steel producers committed to sustainability goals.

Energy Efficiency: DRI production consumes less energy compared to traditional blast furnace routes, making it a cost-effective and energy-efficient alternative for steelmakers, especially in regions with high electricity costs.

Steel Quality: DRI offers superior steel quality with low levels of impurities and residual elements, making it suitable for manufacturing high-grade steel products used in automotive, construction, and infrastructure sectors.

Operational Flexibility: DRI plants are modular and scalable, allowing steelmakers to adjust production levels according to market demand and operational requirements, enhancing flexibility and responsiveness to changing market dynamics.

Market Restraints

Capital Intensive: The establishment of DRI plants requires substantial capital investment due to the high costs associated with equipment procurement, infrastructure development, and technology implementation, posing barriers to market entry for new players.

Raw Material Price Volatility: Fluctuations in iron ore and natural gas prices can impact the profitability of DRI production, affecting operating margins and investment decisions for steelmakers and DRI producers.

Technological Challenges: DRI technology involves complex chemical reactions and process controls, requiring specialized expertise and operational know-how to optimize plant performance and ensure product quality, posing technical challenges for industry stakeholders.

Market Competition: The DRI market faces competition from alternative ironmaking technologies, such as the blast furnace-basic oxygen furnace (BF-BOF) route and direct smelting processes, which offer their unique advantages and market positioning, intensifying competition and market rivalry.

Market Opportunities

Technological Innovation: Continued investments in research and development (R&D) aimed at improving DRI process efficiency, enhancing product quality, and reducing environmental footprint present opportunities for technological innovation and product differentiation in the market.

Expansion in Emerging Markets: Emerging economies with growing steel industries, such as India, China, and Southeast Asian countries, offer significant growth opportunities for DRI producers and steelmakers looking to expand their market presence and tap into new demand sources.

Strategic Partnerships and Alliances: Collaborations between DRI producers, steel manufacturers, technology providers, and government agencies can facilitate knowledge exchange, technology transfer, and market access, fostering growth and market expansion opportunities.

Diversification of Product Portfolio: DRI producers can explore diversification strategies such as product differentiation, value-added services, and customized solutions to meet evolving customer needs, expand market reach, and enhance competitive positioning in the global marketplace.

Market Dynamics

The Direct Reduced Iron (DRI) market operates in a dynamic environment shaped by factors such as technological advancements, regulatory changes, market competition, and macroeconomic trends. Understanding market dynamics is essential for industry participants to navigate challenges, leverage opportunities, and formulate strategic responses to emerging trends and disruptions in the DRI sector.

Regional Analysis

The Direct Reduced Iron (DRI) market exhibits regional variations influenced by factors such as resource availability, market demand, infrastructure development, and regulatory frameworks. Key regions contributing to the global DRI market include:

Middle East: Abundant natural gas reserves and strategic geographic location position Middle Eastern countries as key players in the DRI market, with significant investments in DRI capacity expansion and export-oriented production.

North America: Technological advancements and regulatory support for cleaner steelmaking technologies drive DRI adoption in North America, with investments in DRI plants and production facilities aimed at reducing carbon emissions and enhancing energy efficiency.

Asia Pacific: Rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Southeast Asian nations fuel demand for steel and DRI, creating opportunities for market expansion and investment in the region.

Europe: Stringent environmental regulations, carbon pricing mechanisms, and sustainability initiatives promote DRI adoption in Europe, with emphasis on resource efficiency, circular economy principles, and low-carbon steel production.

Competitive Landscape

Leading Companies in the Direct Reduced Iron (DRI) Market:

Nucor Corporation

POSCO

Jindal Steel & Power Ltd.

Bahrain Steel B.S.C.C.

Vale S.A.

Cliffs Natural Resources Inc.

Essar Steel

ArcelorMittal S.A.

Tata Steel

Kobe Steel, Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

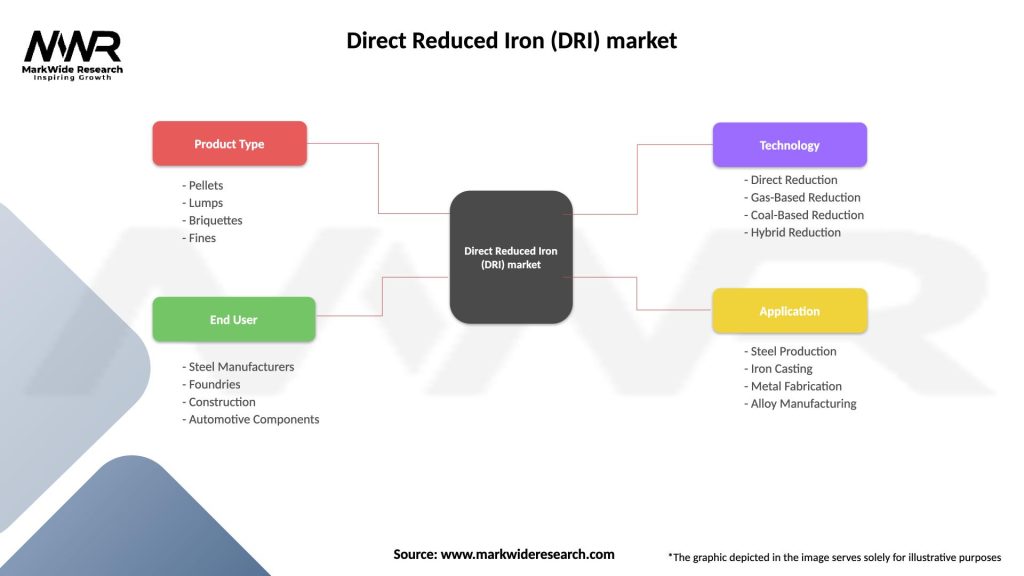

The Direct Reduced Iron (DRI) market can be segmented based on several factors, including:

Production Process: Midrex Process, HYL Process, SL/RN Process, and Other DRI Processes.

End-Use Industry: Steelmaking, Foundry, and Other Industrial Applications.

Raw Material Type: Natural Gas-based DRI and Coal-based DRI.

Application: Long Steel Production, Flat Steel Production, and Other Steel Applications.

Segmentation enhances market granularity, facilitates targeted marketing strategies, and provides insights into customer preferences, industry trends, and growth opportunities within specific market segments.

Category-wise Insights

Long Steel Production: DRI serves as a preferred feedstock for long steel production processes, including rebar, wire rod, and structural steel manufacturing, offering superior product quality, process efficiency, and environmental performance compared to traditional ironmaking routes.

Flat Steel Production: The use of DRI in flat steel production applications, such as hot-rolled coils, cold-rolled sheets, and coated steel products, enables steelmakers to meet stringent quality standards, reduce production costs, and enhance product competitiveness in domestic and export markets.

Foundry Applications: DRI finds applications in foundry operations for producing ductile iron, gray iron, and specialty castings, offering advantages such as consistent chemical composition, low impurities, and improved casting properties for automotive, machinery, and construction industries.

Other Industrial Uses: DRI is utilized in various industrial applications beyond steelmaking, including direct reduced iron-based alloys, iron powder production, and chemical synthesis processes, catering to diverse end-user requirements and market demands.

Key Benefits for Industry Participants and Stakeholders

The Direct Reduced Iron (DRI) market offers several benefits for industry participants and stakeholders, including:

Environmental Sustainability: DRI production reduces carbon emissions, energy consumption, and environmental footprint compared to traditional ironmaking methods, aligning with sustainability goals and regulatory requirements.

Energy Efficiency: DRI technology enables efficient utilization of natural gas or coal resources, minimizing energy consumption and operating costs for steelmakers, and enhancing process efficiency and resource utilization.

Product Quality: DRI provides high-quality iron feedstock with low levels of impurities, enabling steelmakers to produce premium-grade steel products meeting stringent quality specifications and customer requirements.

Process Flexibility: DRI plants offer flexibility in production output, raw material selection, and process control, allowing steelmakers to adapt to market demand fluctuations, operational constraints, and technological advancements.

Market Competitiveness: DRI enhances steelmakers’ competitiveness by offering cost-effective, environmentally friendly, and technologically advanced ironmaking solutions, enabling them to differentiate their products, expand market reach, and achieve sustainable growth.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the Direct Reduced Iron (DRI) market:

Strengths:

Energy-efficient ironmaking process

Superior product quality and purity

Environmental sustainability and regulatory compliance

Technological innovation and process optimization

Weaknesses:

Capital-intensive investment requirements

Dependency on natural gas or coal resources

Process complexity and operational challenges

Market volatility and pricing uncertainties

Opportunities:

Technological advancements and innovation

Expansion in emerging markets and growth regions

Strategic partnerships and alliances

Diversification of product portfolio and end-user applications

Threats:

Fluctuations in raw material prices and availability

Regulatory changes and environmental compliance

Competition from alternative ironmaking technologies

Economic downturns and market uncertainties

Understanding these factors helps stakeholders identify strategic priorities, mitigate risks, capitalize on opportunities, and formulate effective business strategies in the dynamic and competitive DRI market landscape.

Market Key Trends

Technological Advancements: Continuous innovation and R&D efforts focus on enhancing DRI process efficiency, reducing production costs, and improving product quality through advanced process control systems, reactor design improvements, and catalyst development.

Carbon Capture and Utilization (CCU): Integration of carbon capture technologies, carbon sequestration methods, and carbon utilization strategies into DRI plants enables steelmakers to mitigate greenhouse gas emissions, comply with regulatory requirements, and achieve carbon neutrality goals.

Circular Economy Initiatives: Adoption of circular economy principles, resource recovery techniques, and waste valorization strategies in DRI production promotes resource efficiency, waste minimization, and sustainable materials management across the value chain.

Industry 4.0 Integration: The convergence of digitalization, automation, and data analytics in DRI plants facilitates real-time monitoring, predictive maintenance, and process optimization, enabling steelmakers to enhance operational performance, maximize uptime, and improve asset utilization.

Supply Chain Resilience: Strengthening supply chain resilience, diversifying raw material sources, and implementing risk management strategies help steelmakers mitigate supply chain disruptions, secure critical inputs, and maintain production continuity amid global uncertainties and geopolitical risks.

Covid-19 Impact

The Covid-19 pandemic has had mixed effects on the Direct Reduced Iron (DRI) market, with short-term disruptions and long-term implications for industry stakeholders:

Supply Chain Disruptions: The pandemic disrupted global supply chains, impacting raw material availability, logistics operations, and production schedules for DRI producers and steelmakers.

Demand Fluctuations: Economic slowdowns, trade disruptions, and reduced industrial activity during lockdowns and containment measures led to fluctuations in steel demand, affecting DRI consumption and market dynamics.

Operational Challenges: DRI plants faced operational challenges related to workforce safety, plant shutdowns, and supply chain disruptions, requiring adaptation to new health and safety protocols and remote work arrangements.

Resilience and Adaptation: The pandemic underscored the importance of resilience, agility, and adaptation in the DRI industry, prompting stakeholders to diversify supply chains, invest in digital technologies, and explore new business models to navigate uncertainties and mitigate risks.

Key Industry Developments

Market Consolidation: The Direct Reduced Iron (DRI) market witnessed consolidation through mergers, acquisitions, and strategic alliances aimed at enhancing market positioning, expanding geographic presence, and achieving economies of scale.

Technological Collaboration: Collaboration among DRI technology providers, steelmakers, and research institutions facilitated knowledge sharing, technology transfer, and innovation diffusion, driving process improvements and product development in the industry.

Sustainable Practices: Increasing emphasis on sustainability, corporate social responsibility (CSR), and environmental stewardship prompted DRI producers to adopt sustainable practices, reduce carbon emissions, and promote circular economy initiatives across the value chain.

Market Expansion: Expansion into new markets, diversification of product offerings, and vertical integration strategies enabled DRI companies to capture emerging growth opportunities, penetrate new customer segments, and strengthen market competitiveness.

Analyst Suggestions

Strategic Partnerships: Forge strategic partnerships and collaborations with technology providers, raw material suppliers, and end-users to leverage complementary strengths, share risks, and capitalize on market opportunities in the Direct Reduced Iron (DRI) sector.

Operational Excellence: Embrace operational excellence principles, lean manufacturing practices, and continuous improvement methodologies to optimize plant performance, enhance production efficiency, and reduce operating costs across the value chain.

Sustainability Integration: Integrate sustainability considerations, environmental impact assessments, and carbon management strategies into business operations, product development, and supply chain management to meet regulatory requirements and address stakeholder expectations.

Digital Transformation: Embrace digital transformation initiatives, Industry 4.0 technologies, and data-driven decision-making processes to streamline operations, improve asset performance, and unlock value creation opportunities in DRI production and steelmaking.

Market Diversification: Explore opportunities for market diversification, product differentiation, and vertical integration across the value chain to mitigate risks, enhance resilience, and capture value in evolving market landscapes.

Future Outlook

The Direct Reduced Iron (DRI) market is poised for steady growth and innovation driven by factors such as increasing steel demand, technological advancements, regulatory mandates, and sustainability imperatives. While challenges related to raw material availability, energy costs, and market competition persist, opportunities for expansion, diversification, and differentiation abound for industry stakeholders. The future outlook for the DRI market hinges on proactive adaptation to evolving market dynamics, strategic alignment with sustainability goals, and continuous pursuit of operational excellence and innovation across the value chain.

Conclusion

The Direct Reduced Iron (DRI) market plays a pivotal role in the global steel industry, offering a sustainable, energy-efficient, and environmentally friendly ironmaking solution for steelmakers worldwide. Despite challenges posed by raw material constraints, market volatility, and regulatory pressures, the DRI sector continues to evolve and innovate, driven by a commitment to technological advancement, operational excellence, and sustainability. By embracing collaboration, innovation, and resilience, stakeholders in the DRI market can navigate uncertainties, capitalize on emerging opportunities, and contribute to a more sustainable and prosperous future for the steel industry and society at large.

What is Direct Reduced Iron (DRI)?

Direct Reduced Iron (DRI) is a form of iron produced by the direct reduction of iron ore using natural gas or coal. It is used primarily in steelmaking as a substitute for scrap iron, providing a cleaner and more efficient alternative in the production process.

What are the key companies in the Direct Reduced Iron (DRI) market?

Key companies in the Direct Reduced Iron (DRI) market include Nucor Corporation, Tenaris, and Vale S.A., among others. These companies are involved in the production and supply of DRI for various steelmaking applications.

What are the growth factors driving the Direct Reduced Iron (DRI) market?

The growth of the Direct Reduced Iron (DRI) market is driven by the increasing demand for high-quality steel, the shift towards cleaner production methods, and the rising use of DRI in electric arc furnaces. Additionally, the growing focus on sustainability in steel production is boosting DRI adoption.

What challenges does the Direct Reduced Iron (DRI) market face?

The Direct Reduced Iron (DRI) market faces challenges such as fluctuating raw material prices, competition from scrap steel, and the need for significant capital investment in production facilities. These factors can impact the profitability and growth of DRI producers.

What opportunities exist in the Direct Reduced Iron (DRI) market?

Opportunities in the Direct Reduced Iron (DRI) market include the expansion of production capacities in emerging economies, advancements in DRI production technologies, and increasing investments in renewable energy sources for DRI production. These factors can enhance market growth and sustainability.

What trends are shaping the Direct Reduced Iron (DRI) market?

Trends shaping the Direct Reduced Iron (DRI) market include the growing emphasis on carbon-neutral steel production, innovations in DRI technology, and the increasing integration of DRI in hybrid steelmaking processes. These trends are influencing how steel is produced and consumed globally.

Leading Companies in the Direct Reduced Iron (DRI) Market:

Nucor Corporation

POSCO

Jindal Steel & Power Ltd.

Bahrain Steel B.S.C.C.

Vale S.A.

Cliffs Natural Resources Inc.

Essar Steel

ArcelorMittal S.A.

Tata Steel

Kobe Steel, Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

market")