444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The digital health market is experiencing rapid growth and is poised to revolutionize the healthcare industry. Digital health refers to the use of technology and digital solutions to improve healthcare delivery, patient care, and overall health outcomes. It encompasses a wide range of applications, including telemedicine, mobile health (mHealth) apps, wearable devices, electronic health records (EHRs), and health information exchange (HIE) systems.

Meaning

Digital health leverages innovative technologies to transform traditional healthcare practices and address the challenges faced by the industry. It aims to enhance the accessibility, efficiency, and quality of healthcare services. By leveraging digital tools, healthcare providers can remotely monitor patients, deliver personalized care, streamline administrative processes, and enable better collaboration among healthcare professionals.

Executive Summary

The digital health market has experienced significant growth in recent years and is expected to continue its upward trajectory. Factors such as the increasing adoption of smartphones and mobile apps, the rising demand for remote patient monitoring, the need for cost-effective healthcare solutions, and advancements in artificial intelligence (AI) and big data analytics are driving the market’s expansion.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

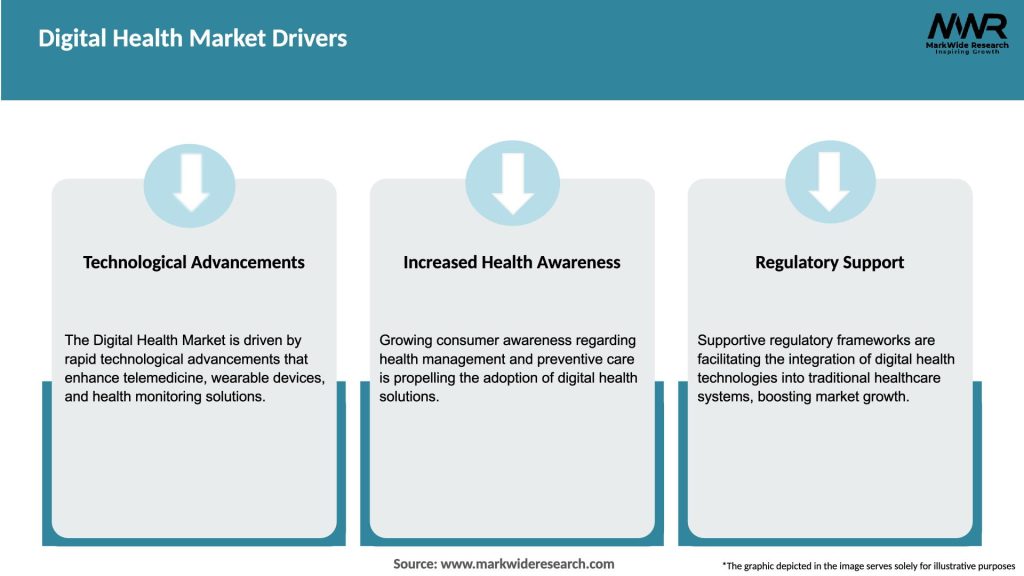

The digital health market is driven by technological advancements, changing consumer preferences, and evolving healthcare needs. Rapid digitization, coupled with the increasing use of smartphones and internet connectivity, has paved the way for the widespread adoption of digital health solutions. Additionally, the COVID-19 pandemic has accelerated the adoption of telemedicine and virtual care, highlighting the need for accessible and remote healthcare services.

Moreover, collaborations and partnerships between digital health companies, healthcare providers, and technology giants are fostering innovation and expanding the market. However, challenges such as data privacy, interoperability, and resistance from traditional healthcare systems need to be addressed to ensure the seamless integration of digital health solutions.

Regional Analysis

The digital health market exhibits significant regional variations, with North America leading in terms of market share. The presence of advanced healthcare infrastructure, favorable government initiatives, and a high level of technology adoption contribute to the region’s dominance. Europe follows closely, driven by robust healthcare systems and supportive regulations.

Asia Pacific is expected to witness substantial growth, fueled by the increasing healthcare expenditure, rising internet penetration, and a growing focus on telemedicine and digital health initiatives in countries like China, India, and Japan. Latin America and the Middle East and Africa are also emerging as promising markets due to the expanding access to mobile technology and the need for affordable healthcare solutions.

Competitive Landscape

Leading Companies in the Digital Health Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

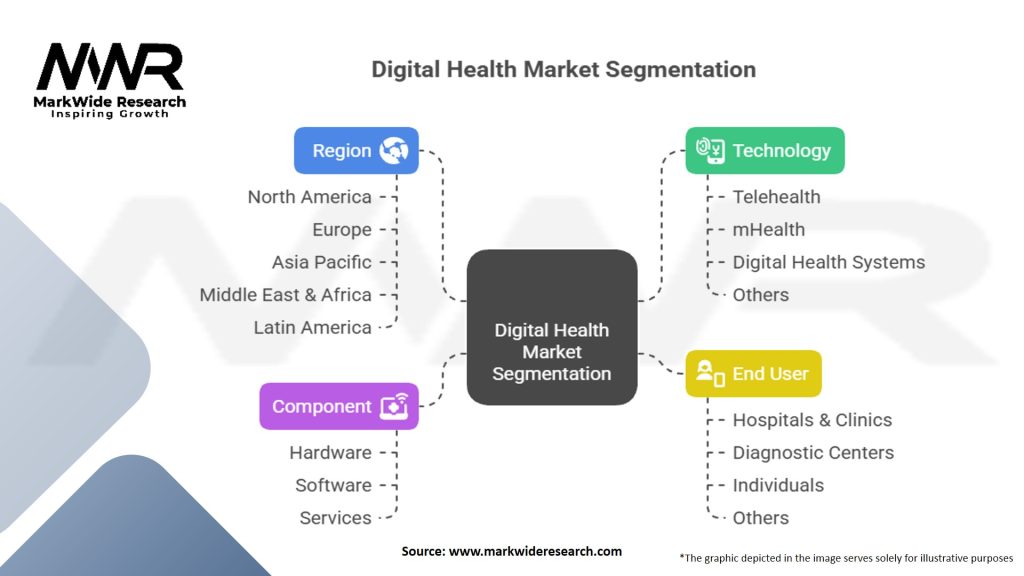

Segmentation

The digital health market can be segmented based on various factors, including product type, component, end-user, and region. The segmentation allows for a deeper understanding of the market dynamics and helps stakeholders identify specific growth opportunities.

Based on product type, the market can be segmented into telemedicine, mHealth apps, EHRs, wearable devices, and health analytics solutions. By component, the market can be categorized into hardware, software, and services. The end-users of digital health solutions include hospitals and clinics, home healthcare, pharmaceutical companies, and individuals.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had a profound impact on the digital health market. With the need for social distancing and reduced in-person interactions, the demand for telemedicine and virtual care skyrocketed. Healthcare providers quickly adopted telehealth solutions to continue providing essential care while minimizing the risk of virus transmission.

Telemedicine allowed patients to consult healthcare professionals remotely, reducing the burden on hospitals and clinics and ensuring access to care. The pandemic also accelerated the development and adoption of mHealth apps, remote patient monitoring devices, and digital therapeutics, as individuals sought ways to manage their health from the safety of their homes.

The COVID-19 crisis underscored the importance of digital health in maintaining continuity of care and highlighted the potential for technology-driven solutions to transform healthcare delivery.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future of the digital health market looks promising, with immense potential for growth and innovation. Advancements in technology, increasing digital literacy among healthcare professionals and consumers, and the need for accessible and efficient healthcare services will continue to drive the market.

The integration of AI, machine learning, and big data analytics will enable more precise diagnostics, personalized treatment plans, and predictive healthcare. Furthermore, the expansion of 5G technology and the Internet of Medical Things (IoMT) will facilitate the seamless connectivity of devices and the exchange of health information.

The digital health market is expected to witness further consolidation, with larger companies acquiring start-ups and smaller players to strengthen their offerings. Collaboration and partnerships among stakeholders will be crucial to address the challenges and capitalize on the opportunities in the digital health landscape.

Conclusion

The digital health market is revolutionizing the healthcare industry by leveraging technology and digital solutions to enhance care delivery, improve patient outcomes, and increase operational efficiency. The adoption of telemedicine, mHealth apps, wearable devices, and health analytics solutions is transforming the way healthcare is delivered and experienced.

While the market offers significant opportunities, challenges related to data security, interoperability, and resistance to change need to be addressed. Through collaboration, investment in infrastructure, and policy reforms, the digital health market can reach its full potential, providing accessible, personalized, and cost-effective healthcare for individuals worldwide.

What is digital health?

Digital health refers to the use of technology to enhance health and healthcare delivery. It encompasses a wide range of applications, including telemedicine, mobile health apps, and electronic health records, aimed at improving patient outcomes and healthcare efficiency.

What are the key companies in the digital health market?

Key companies in the digital health market include Teladoc Health, Cerner Corporation, and Philips Healthcare, among others. These companies are leading the way in providing innovative solutions that enhance patient care and streamline healthcare processes.

What are the main drivers of growth in the digital health market?

The main drivers of growth in the digital health market include the increasing adoption of smartphones, the rising demand for remote patient monitoring, and the need for cost-effective healthcare solutions. Additionally, the growing emphasis on personalized medicine is fueling innovation in this sector.

What challenges does the digital health market face?

The digital health market faces several challenges, including data privacy concerns, regulatory hurdles, and the need for interoperability among different health systems. These issues can hinder the widespread adoption of digital health technologies.

What opportunities exist in the digital health market for the future?

Opportunities in the digital health market include the expansion of telehealth services, the integration of artificial intelligence in diagnostics, and the development of wearable health technologies. These advancements are expected to enhance patient engagement and improve health outcomes.

What trends are shaping the digital health market today?

Current trends in the digital health market include the rise of virtual care platforms, increased focus on mental health apps, and the use of big data analytics to improve patient care. These trends reflect a shift towards more accessible and personalized healthcare solutions.

Digital Health Market

| Segmentation | Details |

|---|---|

| Technology | Telehealth, mHealth, Digital Health Systems, Others |

| Component | Hardware, Software, Services |

| End User | Hospitals & Clinics, Diagnostic Centers, Individuals, Others |

| Region | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Digital Health Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA