The defense contracting service market encompasses a wide array of services provided to government agencies, military branches, and defense contractors involved in the procurement, development, and maintenance of defense systems, equipment, and infrastructure. These services range from engineering and technical support to logistics, maintenance, and program management, playing a critical role in ensuring the readiness, effectiveness, and efficiency of defense operations worldwide.

Meaning

Defense contracting services involve the provision of specialized expertise, resources, and capabilities to support defense organizations and contractors in meeting their mission-critical requirements. These services cover various domains, including defense procurement, research and development, testing and evaluation, training, sustainment, and lifecycle support, contributing to national security, military readiness, and technological superiority.

Executive Summary

The defense contracting service market is driven by increasing defense spending, evolving security threats, and the growing complexity of defense systems and operations. As defense organizations seek to modernize their capabilities, improve operational efficiency, and enhance readiness, the demand for specialized contracting services continues to grow. To succeed in this dynamic market, defense contractors must adapt to changing customer needs, technological advancements, and regulatory requirements while delivering innovative, cost-effective solutions.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Defense Budget Trends: Fluctuations in defense budgets and procurement priorities influence market dynamics, driving demand for specific contracting services aligned with defense modernization programs, platform upgrades, and operational requirements.

Technology Innovation: Advancements in defense technologies, including artificial intelligence, unmanned systems, cybersecurity, and space-based capabilities, create opportunities for defense contractors to provide specialized services in areas such as research and development, system integration, and technology insertion.

Global Security Challenges: Evolving security threats, including terrorism, cyber attacks, geopolitical tensions, and unconventional warfare, shape defense contracting priorities, driving investments in capabilities such as intelligence, surveillance, reconnaissance (ISR), counterterrorism, and homeland security.

Public-Private Partnerships: Collaboration between government agencies, defense contractors, and industry partners fosters innovation, efficiency, and cost savings in defense contracting, enabling the delivery of integrated solutions, shared resources, and joint capabilities.

Market Drivers

Defense Modernization: Increasing focus on defense modernization programs, platform upgrades, and force modernization initiatives drives demand for specialized contracting services in areas such as systems engineering, integration, testing, and sustainment to support the development and fielding of advanced defense capabilities.

Cybersecurity Threats: Growing cybersecurity threats and vulnerabilities across defense networks, platforms, and systems drive investments in cybersecurity services, including risk assessment, vulnerability analysis, threat intelligence, and security operations, to safeguard critical assets and information.

Global Threat Landscape: Evolving security threats, including terrorism, insurgency, geopolitical tensions, and regional conflicts, drive demand for contracting services in areas such as intelligence, surveillance, reconnaissance (ISR), counterterrorism, and crisis response to address emerging threats and challenges.

Interoperability Requirements: Increasing emphasis on interoperability and coalition operations among allied nations drives demand for contracting services in areas such as interoperable communications, command and control (C2), information sharing, and coalition interoperability to enhance military cooperation and joint mission effectiveness.

Market Restraints

Budget Constraints: Fluctuations in defense budgets, sequestration, and fiscal constraints limit government spending on contracting services, impacting procurement, program funding, and contract awards, particularly for non-essential or low-priority programs and initiatives.

Regulatory Compliance: Stringent regulatory requirements, including defense acquisition regulations (DAR), Federal Acquisition Regulation (FAR), and Defense Federal Acquisition Regulation Supplement (DFARS), impose compliance burdens, administrative overhead, and contractual obligations on defense contractors, affecting cost, schedule, and performance.

Procurement Delays: Lengthy procurement cycles, contract negotiations, and bureaucratic processes delay contract awards, program initiation, and project execution, impacting revenue generation, cash flow, and profitability for defense contracting firms, particularly small and medium-sized businesses (SMBs).

Market Competition: Intense competition among defense contractors, prime contractors, and subcontractors for limited contract opportunities, task orders, and procurement dollars drives price competition, margin pressure, and bid protests, affecting market share, profitability, and business sustainability.

Market Opportunities

Emerging Technologies: Opportunities exist for defense contractors to leverage emerging technologies, such as artificial intelligence, machine learning, unmanned systems, and advanced materials, to develop innovative solutions, enhance operational effectiveness, and address emerging mission requirements.

Cybersecurity Services: Growing demand for cybersecurity services presents opportunities for defense contractors to provide cybersecurity assessments, risk management, incident response, and managed security services to government agencies, military branches, and defense industry partners.

Training and Simulation: Demand for training and simulation services continues to grow as defense organizations seek to enhance readiness, proficiency, and effectiveness through virtual, augmented, and mixed-reality training environments, offering opportunities for contractors to provide simulation hardware, software, and support services.

Logistics and Sustainment: The need for logistics support, sustainment services, and supply chain management remains critical to defense operations, creating opportunities for contractors to provide logistics planning, transportation, maintenance, and depot-level support for military equipment and systems.

Market Dynamics

The defense contracting service market operates within a dynamic environment influenced by factors such as defense budgets, technological advancements, geopolitical trends, regulatory requirements, and market competition. These dynamics shape market trends, business strategies, and industry partnerships, driving innovation, collaboration, and adaptation among defense contractors and industry stakeholders.

Regional Analysis

The defense contracting service market exhibits regional variations driven by factors such as defense spending, geopolitical tensions, military modernization efforts, and industry capabilities. Key regions include:

North America: The United States dominates the defense contracting market, accounting for the largest share of defense spending, contract awards, and procurement opportunities, supported by a robust defense industrial base, advanced technology expertise, and strategic alliances with allied nations.

Europe: European countries, including the United Kingdom, France, Germany, and Italy, represent significant markets for defense contracting services, driven by defense modernization initiatives, NATO requirements, and collaborative defense projects among European Union (EU) member states.

Asia Pacific: Asia Pacific nations, including China, India, Japan, South Korea, and Australia, are investing in defense capabilities, driving demand for contracting services in areas such as military modernization, technology acquisition, and regional security cooperation to address evolving security challenges and geopolitical tensions.

Middle East and Africa: Middle Eastern countries, such as Saudi Arabia, United Arab Emirates (UAE), and Israel, invest heavily in defense procurement, security cooperation, and military modernization, creating opportunities for defense contractors to provide specialized services in areas such as aerospace, cybersecurity, and defense logistics.

Competitive Landscape

Leading Companies in the Defense Contracting Service Market:

Lockheed Martin Corporation

BAE Systems plc

Northrop Grumman Corporation

General Dynamics Corporation

Raytheon Technologies Corporation

Boeing Company

Airbus SE

L3Harris Technologies, Inc.

Leonardo S.p.A.

SAIC (Science Applications International Corporation)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

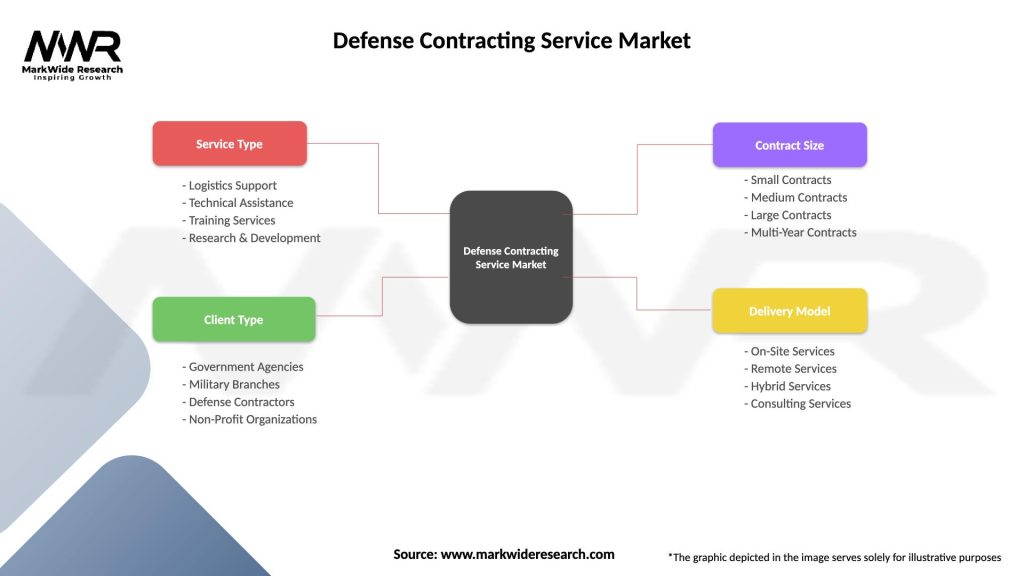

The defense contracting service market can be segmented based on various factors, including:

Service Type: Engineering and technical services, logistics and sustainment, training and simulation, cybersecurity, program management, and professional services.

End-User: Government agencies, military branches, defense contractors, and industry partners.

Application Area: Aerospace, land systems, maritime systems, information technology (IT), cybersecurity, intelligence, and homeland security.

Geography: Regional markets, including North America, Europe, Asia Pacific, Middle East, and Africa.

Segmentation provides insights into market dynamics, customer requirements, and business opportunities, enabling defense contractors to tailor their strategies, offerings, and capabilities to specific market segments and customer needs.

Category-wise Insights

Engineering and Technical Services: Defense contractors provide engineering and technical services, including systems engineering, integration, testing, and validation, to support defense acquisition programs, platform upgrades, and technology insertion initiatives.

Logistics and Sustainment: Logistics and sustainment services encompass a wide range of activities, including maintenance, repair, overhaul (MRO), supply chain management, and depot-level support, ensuring the operational readiness and availability of military equipment and systems.

Training and Simulation: Training and simulation services enable military personnel to enhance their skills, proficiency, and readiness through virtual, augmented, and mixed-reality training environments, offering realistic scenarios, mission rehearsals, and skill development exercises.

Cybersecurity Services: Cybersecurity services focus on protecting defense networks, platforms, and systems from cyber threats, vulnerabilities, and attacks through risk assessment, vulnerability management, incident response, and security operations, ensuring the integrity, confidentiality, and availability of critical information and assets.

Key Benefits for Industry Participants and Stakeholders

Mission Support: Defense contracting services provide critical support to government agencies, military branches, and defense contractors in fulfilling their mission requirements, including system development, procurement, sustainment, and operational support.

Expertise and Capabilities: Defense contractors offer specialized expertise, resources, and capabilities in areas such as engineering, logistics, cybersecurity, and program management, augmenting customer capabilities and enhancing mission effectiveness.

Innovation and Technology: Defense contracting services drive innovation, technology development, and research advancements in defense systems, platforms, and capabilities, enabling the adoption of cutting-edge technologies and solutions to address emerging threats and challenges.

Operational Readiness: By providing logistics support, maintenance services, and training solutions, defense contractors contribute to the operational readiness, efficiency, and effectiveness of military forces, ensuring their preparedness for a wide range of missions and contingencies.

SWOT Analysis

A SWOT analysis provides insights into the defense contracting service market’s strengths, weaknesses, opportunities, and threats:

Strengths:

Specialized Expertise: Defense contractors possess specialized expertise, resources, and capabilities in defense systems, technologies, and operations, enabling them to deliver tailored solutions and support to government and military customers.

Mission-Critical Support: Defense contracting services provide mission-critical support to government agencies, military branches, and defense contractors, ensuring the readiness, effectiveness, and efficiency of defense operations and capabilities.

Innovation and Technology: Defense contractors drive innovation, technology development, and research advancements in defense systems, platforms, and capabilities, delivering cutting-edge solutions to address evolving threats and challenges.

Partnership and Collaboration: Collaboration among government agencies, military branches, prime contractors, and subcontractors fosters partnership, teamwork, and synergy in defense contracting, enabling integrated solutions, shared resources, and joint capabilities.

Weaknesses:

Dependency on Government Funding: Defense contractors are highly dependent on government funding, contract awards, and procurement opportunities, making them vulnerable to fluctuations in defense budgets, procurement priorities, and political dynamics.

Regulatory Compliance: Stringent regulatory requirements, including defense acquisition regulations (DAR), Federal Acquisition Regulation (FAR), and Defense Federal Acquisition Regulation Supplement (DFARS), impose compliance burdens, administrative overhead, and contractual obligations on defense contractors, affecting cost, schedule, and performance.

Market Competition: Intense competition among defense contractors, prime contractors, and subcontractors for limited contract opportunities, task orders, and procurement dollars drives price competition, margin pressure, and bid protests, affecting market share, profitability, and business sustainability.

Opportunities:

Emerging Technologies: Opportunities exist for defense contractors to leverage emerging technologies, such as artificial intelligence, unmanned systems, cybersecurity, and space-based capabilities, to develop innovative solutions, enhance operational effectiveness, and address emerging mission requirements.

Cybersecurity Services: Growing demand for cybersecurity services presents opportunities for defense contractors to provide cybersecurity assessments, risk management, incident response, and managed security services to government agencies, military branches, and defense industry partners.

Global Security Challenges: Evolving security threats, including terrorism, insurgency, geopolitical tensions, and regional conflicts, drive demand for contracting services in areas such as intelligence, surveillance, reconnaissance (ISR), counterterrorism, and crisis response to address emerging threats and challenges.

Threats:

Budget Constraints: Fluctuations in defense budgets, sequestration, and fiscal constraints limit government spending on contracting services, impacting procurement, program funding, and contract awards, particularly for non-essential or low-priority programs and initiatives.

Regulatory Compliance: Stringent regulatory requirements, including defense acquisition regulations (DAR), Federal Acquisition Regulation (FAR), and Defense Federal Acquisition Regulation Supplement (DFARS), impose compliance burdens, administrative overhead, and contractual obligations on defense contractors, affecting cost, schedule, and performance.

Market Competition: Intense competition among defense contractors, prime contractors, and subcontractors for limited contract opportunities, task orders, and procurement dollars drives price competition, margin pressure, and bid protests, affecting market share, profitability, and business sustainability.

Understanding these factors through a SWOT analysis helps defense contractors identify their competitive advantages, address weaknesses, capitalize on opportunities, and mitigate potential threats.

Market Key Trends

Digital Transformation: Digital transformation initiatives, including digital twin technology, artificial intelligence (AI), machine learning (ML), and big data analytics, are transforming defense operations, logistics, and contracting, enabling data-driven decision-making, automation, and efficiency improvements.

Remote Operations: The COVID-19 pandemic accelerated the adoption of remote operations, telework, and virtual collaboration in defense contracting, driving investments in remote access, secure communications, and remote support capabilities to ensure business continuity and operational resilience.

Supply Chain Resilience: Supply chain resilience and risk management have become critical priorities for defense contractors, leading to efforts to diversify supply chains, identify alternative sources of supply, and enhance visibility, traceability, and agility in supply chain operations.

Space Domain Awareness: Growing emphasis on space domain awareness, satellite communications, and space-based capabilities drives demand for contracting services in areas such as satellite launch, satellite operations, space situational awareness (SSA), and space traffic management.

Covid-19 Impact

The COVID-19 pandemic had a significant impact on the defense contracting service market, disrupting supply chains, operations, and program execution while accelerating trends such as remote work, digital transformation, and supply chain resilience. Some key impacts include:

Operational Disruptions: The pandemic caused operational disruptions, delays, and cancellations in defense contracting activities, including contract negotiations, program execution, and supply chain operations, impacting project timelines, deliverables, and customer satisfaction.

Remote Workforce: Defense contractors transitioned to remote work and telework arrangements to comply with social distancing guidelines and mitigate the risk of COVID-19 transmission, requiring investments in remote access, virtual collaboration, and cybersecurity to support distributed workforces.

Supply Chain Challenges: Supply chain disruptions, shortages, and logistics challenges affected defense contractors’ ability to source materials, components, and subsystems, leading to delays, cost increases, and program uncertainties in defense procurement and production.

Business Continuity: Defense contractors implemented business continuity plans, contingency measures, and risk mitigation strategies to ensure operational resilience and continuity of critical services, including remote support, virtual training, and secure communications.

Key Industry Developments

Digital Transformation: Acceleration of digital transformation initiatives, including cloud computing, remote collaboration, and cybersecurity enhancements, to support remote operations, virtual contracting, and digital delivery of defense services and solutions.

Supply Chain Resilience: Investments in supply chain resilience, risk management, and diversification to mitigate the impact of disruptions, shortages, and geopolitical risks on defense procurement, production, and sustainment activities.

Cybersecurity Enhancements: Strengthening of cybersecurity defenses, incident response capabilities, and threat intelligence sharing to protect defense networks, systems, and information from cyber threats, vulnerabilities, and attacks.

Remote Support: Expansion of remote support capabilities, virtual training solutions, and telework infrastructure to facilitate remote operations, workforce collaboration, and customer support in response to the COVID-19 pandemic and future contingencies.

Analyst Suggestions

Invest in Digital Transformation: Defense contractors should invest in digital transformation initiatives, including cloud computing, remote collaboration, and cybersecurity enhancements, to support remote operations, virtual contracting, and digital delivery of defense services and solutions.

Enhance Supply Chain Resilience: Develop resilient supply chain strategies, partnerships, and sourcing options to mitigate risks of supply chain disruptions, shortages, and logistics challenges, ensuring continuity of critical materials, components, and subsystems for defense production and sustainment.

Strengthen Cybersecurity Defenses: Strengthen cybersecurity defenses, incident response capabilities, and threat intelligence sharing to protect defense networks, systems, and information from cyber threats, vulnerabilities, and attacks, ensuring the integrity, confidentiality, and availability of critical assets and data.

Adapt to Remote Operations: Adapt to remote operations, telework arrangements, and virtual collaboration by investing in remote access, secure communications, and remote support capabilities to ensure business continuity, operational resilience, and customer satisfaction.

Future Outlook

The defense contracting service market is poised for growth and innovation in the coming years, driven by increasing defense spending, evolving security threats, and technological advancements in defense systems and capabilities. However, challenges such as budget constraints, regulatory compliance, and market competition require defense contractors to innovate, collaborate, and adapt to changing market dynamics, customer needs, and industry trends to succeed in this dynamic and competitive market landscape.

Conclusion

In conclusion, the defense contracting service market continues to play a crucial role in supporting government agencies, military branches, and defense contractors worldwide. Despite challenges such as budget constraints, regulatory compliance, and market competition, the market is poised for growth fueled by increasing defense spending, technological advancements, and evolving security threats. With a focus on innovation, supply chain resilience, and cybersecurity enhancements, defense contractors are well-positioned to navigate the dynamic market landscape and capitalize on emerging opportunities. Collaboration, adaptation to remote operations, and investments in digital transformation are key strategies for success in this ever-evolving market.

What is Defense Contracting Service?

Defense Contracting Service refers to the provision of services and support to government defense agencies by private contractors. This includes logistics, maintenance, research and development, and operational support for military operations.

What are the key players in the Defense Contracting Service Market?

Key players in the Defense Contracting Service Market include Lockheed Martin, Northrop Grumman, Raytheon Technologies, and BAE Systems, among others. These companies provide a range of services from advanced technology solutions to logistical support.

What are the growth factors driving the Defense Contracting Service Market?

The growth of the Defense Contracting Service Market is driven by increasing defense budgets, the need for advanced military technology, and the rising complexity of defense operations. Additionally, geopolitical tensions and the demand for modernization of defense systems contribute to market expansion.

What challenges does the Defense Contracting Service Market face?

The Defense Contracting Service Market faces challenges such as stringent regulations, budget constraints, and the need for compliance with government standards. Additionally, competition among contractors can lead to pricing pressures and reduced profit margins.

What opportunities exist in the Defense Contracting Service Market?

Opportunities in the Defense Contracting Service Market include the increasing adoption of artificial intelligence and cybersecurity solutions, as well as the potential for partnerships with government agencies for innovative defense technologies. The shift towards modernization and digital transformation also presents new avenues for growth.

What trends are shaping the Defense Contracting Service Market?

Trends shaping the Defense Contracting Service Market include the integration of advanced technologies such as drones and autonomous systems, a focus on sustainability in defense operations, and the growing importance of cybersecurity measures. These trends are influencing how contractors develop and deliver their services.

Leading Companies in the Defense Contracting Service Market:

Lockheed Martin Corporation

BAE Systems plc

Northrop Grumman Corporation

General Dynamics Corporation

Raytheon Technologies Corporation

Boeing Company

Airbus SE

L3Harris Technologies, Inc.

Leonardo S.p.A.

SAIC (Science Applications International Corporation)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.