The consumer credit market plays a crucial role in the global economy, enabling individuals to access funds for various purposes, such as purchasing homes, cars, or funding their education. Consumer credit refers to the provision of funds by financial institutions or lenders to individuals for personal, non-business purposes. This market encompasses a wide range of financial products, including credit cards, personal loans, auto loans, mortgages, and more.

Consumer credit has become an integral part of modern-day living, as it allows individuals to fulfill their immediate financial needs without requiring substantial upfront capital. It provides people with the flexibility to make purchases and pay back the borrowed amount over time, either in installments or as a revolving credit line.

Meaning

Consumer credit is a financial arrangement in which individuals borrow money from financial institutions or lenders to meet their personal expenses. This type of credit includes various products and services, such as credit cards, personal loans, payday loans, installment loans, and lines of credit.

The primary purpose of consumer credit is to provide individuals with convenient access to funds, allowing them to make purchases or cover expenses when they do not have the required cash immediately available. Consumer credit also enables people to build their credit history and improve their credit scores, which can have long-term benefits in terms of accessing better financial opportunities.

Executive Summary

The consumer credit market has witnessed significant growth and transformation in recent years. With the rise of digital platforms and advancements in financial technology, the process of obtaining and managing consumer credit has become more efficient and accessible. This market offers numerous opportunities for financial institutions, lenders, and borrowers alike.

In this report, we will provide key insights into the consumer credit market, including its drivers, restraints, opportunities, and dynamics. We will also analyze the market on a regional basis, examine the competitive landscape, and discuss the key trends and developments shaping the industry. Additionally, we will explore the impact of the COVID-19 pandemic and provide future outlook and recommendations.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The consumer credit market has experienced steady growth over the years, driven by increasing consumer demand for financing options and the expanding availability of credit products.

Technological advancements and the emergence of online lending platforms have revolutionized the consumer credit landscape, making it more convenient and accessible for borrowers.

Changing consumer preferences and lifestyles have led to a shift in credit utilization patterns, with a greater emphasis on digital payments and alternative lending models.

Regulatory frameworks and consumer protection measures play a crucial role in shaping the consumer credit market, ensuring fair practices and preventing predatory lending.

The rising importance of credit scores and creditworthiness has driven the need for individuals to manage their debts responsibly and maintain a good credit history.

Economic factors, such as interest rates, inflation, and employment levels, have a significant impact on the consumer credit market, influencing borrowing behavior and repayment capabilities.

Collaboration between financial institutions and technology companies has resulted in innovative credit products and enhanced risk assessment techniques, improving the overall efficiency of the consumer credit market.

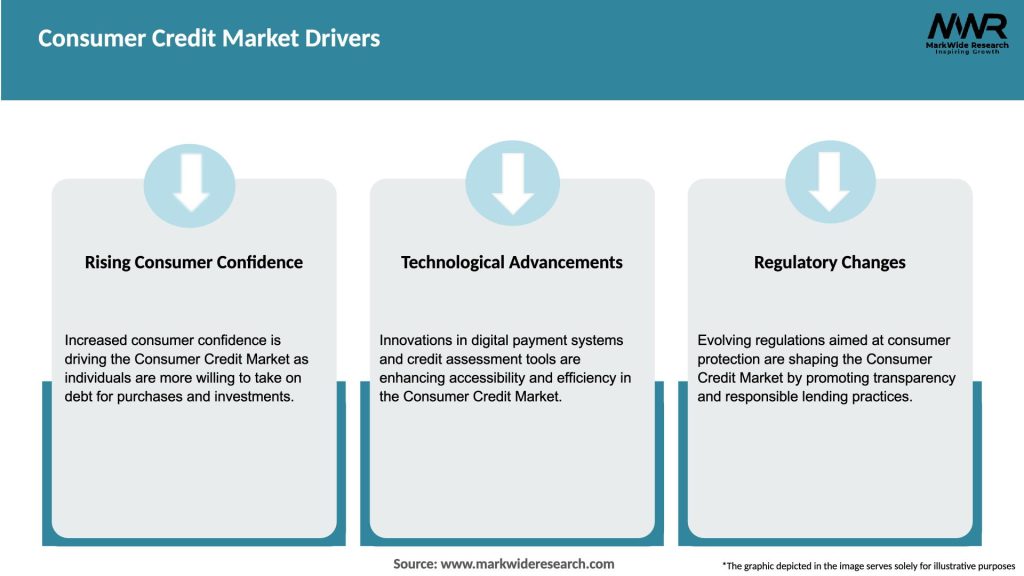

Market Drivers

Increasing consumer purchasing power: Rising income levels and economic growth have enabled individuals to have greater disposable income, driving the demand for consumer credit.

Ease of access and convenience: The advent of online lending platforms and digital banking services has made it easier for individuals to apply for and manage consumer credit, reducing the time and effort required.

Emergence of alternative lending models: Peer-to-peer lending, crowdfunding, and other alternative financing options have gained popularity, providing borrowers with more choices and competitive interest rates.

Technological advancements: Fintech innovations, such as mobile banking apps, digital wallets, and automated underwriting processes, have transformed the consumer credit market, making it more efficient and user-friendly.

Changing consumer behavior: The shift towards a cashless society and the increasing reliance on digital transactions have contributed to the growth of consumer credit, as individuals prefer the convenience and security offered by credit cards and digital payment methods.

Market Restraints

Increasing debt burden: Excessive borrowing and lack of financial discipline among consumers can lead to high debt levels and potential defaults, posing risks to both borrowers and lenders.

Stringent regulatory environment: Consumer credit markets are subject to strict regulations and compliance requirements, which can limit the profitability and flexibility of financial institutions.

Economic volatility: Fluctuations in interest rates, inflation, and unemployment rates can impact borrowers’ ability to repay their loans, leading to higher default rates and credit risks.

Cybersecurity concerns: As consumer credit transactions increasingly shift to online platforms, the risk of data breaches, identity theft, and fraud becomes a significant challenge for both consumers and lenders.

Limited access to credit: Certain demographic groups, such as individuals with low credit scores or limited credit history, may face difficulties in obtaining affordable consumer credit options.

Market Opportunities

Growing demand for personalized lending solutions: Tailored credit products and services, such as microloans, peer-to-peer lending, and point-of-sale financing, present opportunities for financial institutions to cater to specific consumer needs.

Expansion in emerging markets: The rising middle class and increasing urbanization in developing economies provide a fertile ground for the expansion of consumer credit markets, as individuals seek access to financing for their aspirations and needs.

Integration of artificial intelligence and big data analytics: Leveraging advanced technologies can enhance credit scoring models, risk assessment, and fraud detection, enabling lenders to make more informed decisions and offer competitive interest rates.

Collaborative partnerships: Financial institutions partnering with technology companies, e-commerce platforms, or retailers can create synergies that benefit both parties and provide consumers with seamless credit options at the point of purchase.

Focus on financial education: Promoting financial literacy and educating consumers about responsible credit usage can lead to a more informed and responsible borrowing behavior, reducing default rates and credit risks.

Market Dynamics

The consumer credit market is highly dynamic, influenced by various factors that shape its growth and development. Economic conditions, regulatory policies, technological advancements, and changing consumer preferences interact to determine the market dynamics. Understanding these dynamics is crucial for industry participants to adapt and thrive in a rapidly evolving environment.

As the market becomes increasingly digitalized, the demand for efficient and user-friendly credit solutions continues to rise. Consumers expect quick loan approval processes, seamless digital experiences, and competitive interest rates. Financial institutions and lenders must embrace technology and leverage data analytics to streamline operations, improve risk assessment, and offer personalized credit options.

Moreover, the regulatory landscape plays a significant role in shaping the consumer credit market. Governments and regulatory bodies have implemented measures to protect consumers, ensure fair lending practices, and manage systemic risks. Compliance with these regulations is essential for industry players to build trust with consumers and maintain a sustainable business model.

Additionally, macroeconomic factors, such as interest rates, inflation, and employment levels, impact borrowing behavior and repayment capabilities. A stable economy with favorable economic conditions encourages borrowing and stimulates credit market growth. Conversely, economic downturns or financial crises can lead to decreased consumer confidence and tighter credit availability.

Furthermore, the ongoing digitization and integration of financial services have created opportunities for collaboration between traditional financial institutions and technology companies. Partnerships and strategic alliances enable incumbents to leverage technological expertise, enhance customer experiences, and expand their reach in the consumer credit market.

Regional Analysis

The consumer credit market exhibits regional variations due to differences in economic conditions, cultural norms, regulatory frameworks, and financial infrastructures. Understanding the regional dynamics is crucial for industry participants to identify growth opportunities, tailor their products and services, and navigate specific market challenges.

North America: The consumer credit market in North America is characterized by the dominance of credit card usage and a well-developed banking system. The United States, in particular, is a significant player in the global consumer credit market, driven by a culture of consumerism and a strong emphasis on credit scores. The market is highly regulated, with strict consumer protection measures in place.

Europe: European countries have a diverse consumer credit landscape, with variations in credit culture and lending practices. Countries like the United Kingdom and Germany have mature consumer credit markets, while emerging economies in Eastern Europe offer growth potential. Regulatory frameworks, such as the European Union’s General Data Protection Regulation (GDPR), impact credit data sharing and consumer rights.

Asia-Pacific: The Asia-Pacific region presents immense opportunities for consumer credit market growth, fueled by rapid urbanization, rising disposable incomes, and the adoption of digital payment solutions. Countries like China and India have witnessed significant expansion in their consumer credit markets, driven by a growing middle class and increasing consumer aspirations. However, regulatory challenges and cultural differences shape the market dynamics in each country.

Latin America: Latin American countries have a developing consumer credit market, with varying degrees of credit penetration and regulatory frameworks. Brazil, Mexico, and Chile are among the key markets in the region, characterized by the increasing adoption of credit cards and the emergence of fintech lending platforms. Access to credit and financial inclusion remain key challenges in some parts of Latin America.

Middle East and Africa: The consumer credit market in the Middle East and Africa is still nascent, but growing steadily. Countries like the United Arab Emirates and South Africa have relatively mature markets, while other nations are witnessing increasing consumer credit demand. Islamic banking principles and cultural factors influence lending practices in the region.

Understanding the regional nuances and adapting strategies accordingly is vital for industry participants to capitalize on the unique opportunities and address the specific challenges in each market.

Competitive Landscape

Leading Companies in the Consumer Credit Market:

JPMorgan Chase & Co.

Bank of America Corporation

Citigroup Inc.

Wells Fargo & Company

Discover Financial Services

Capital One Financial Corporation

American Express Company

Barclays PLC

HSBC Holdings plc

Santander Group

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The consumer credit market can be segmented based on various factors, including loan type, borrower profile, and purpose of credit. Understanding the different segments helps industry participants tailor their offerings, target specific customer groups, and develop effective marketing strategies.

Loan Type:

Credit Cards: Revolving credit lines with varying credit limits, allowing cardholders to make purchases and pay back the borrowed amount over time.

Personal Loans: Unsecured loans provided for personal use, typically used for purposes such as debt consolidation, home improvement, or medical expenses.

Auto Loans: Loans specifically designed for financing the purchase of vehicles, with the vehicle serving as collateral for the loan.

Mortgages: Loans provided for purchasing residential properties, with the property serving as collateral.

Borrower Profile:

Prime Borrowers: Individuals with good credit scores and a strong credit history, who qualify for the most favorable interest rates and credit terms.

Subprime Borrowers: Individuals with lower credit scores or limited credit history, who may face challenges in obtaining credit and often pay higher interest rates.

Near-prime Borrowers: Individuals who fall between prime and subprime categories in terms of creditworthiness and credit scores.

Purpose of Credit:

Education Loans: Loans specifically designed for funding educational expenses, such as tuition fees, books, and living costs.

Medical Loans: Loans used to cover medical expenses not covered by insurance, including elective procedures or cosmetic treatments.

Home Improvement Loans: Loans provided for renovating or improving residential properties, such as remodeling kitchens, adding extensions, or installing energy-efficient systems.

Debt Consolidation Loans: Loans used to combine multiple debts into a single loan, typically with the aim of obtaining a lower interest rate and simplifying repayment.

Segmentation allows industry participants to target their marketing efforts, customize credit products, and develop tailored strategies to meet the specific needs and preferences of different customer segments.

Category-wise Insights

Credit Cards:

Credit cards have become a ubiquitous financial tool, providing consumers with convenience and flexibility in making purchases and managing their finances.

Rewards programs and cashback incentives have become crucial factors in consumers’ choice of credit cards, as they seek to maximize the benefits of their spending.

Co-branded credit cards, tied to specific retailers, travel companies, or organizations, offer targeted rewards and discounts, enhancing customer loyalty.

Personal Loans:

Personal loans have gained popularity as a means of financing various personal expenses, from weddings and vacations to medical emergencies and debt consolidation.

Online lenders and fintech startups have simplified the personal loan application process, providing quick approvals and competitive interest rates.

Peer-to-peer lending platforms have emerged as alternative sources of personal loans, connecting borrowers directly with individual lenders.

Auto Loans:

Auto loans enable individuals to purchase vehicles without requiring a substantial upfront payment, spreading the cost over a specified period.

Low-interest rates and extended loan terms have made auto loans attractive to consumers, driving vehicle sales and stimulating the automotive industry.

Balloon payment options and leasing arrangements have provided consumers with more flexibility in managing their auto loan obligations.

Mortgages:

Mortgages represent a significant portion of consumer credit, enabling individuals to fulfill their dream of homeownership.

Fixed-rate and adjustable-rate mortgages are the two primary types, offering borrowers different options based on their risk tolerance and financial goals.

Mortgage refinancing has gained popularity, allowing homeowners to take advantage of lower interest rates or access equity for other purposes.

Understanding the specific dynamics and trends within each category of consumer credit helps industry participants identify opportunities for innovation, product differentiation, and market expansion.

Key Benefits for Industry Participants and Stakeholders

Financial Institutions:

Access to a diverse customer base and revenue streams through consumer credit offerings.

Opportunities to cross-sell other financial products and services, such as insurance, investment products, and wealth management services.

Enhanced customer loyalty and long-term relationships through personalized credit solutions and superior customer experiences.

Lenders:

Potential for higher interest income and profitability through interest charges and fees associated with consumer credit products.

Mitigation of credit risk through comprehensive risk assessment processes, credit scoring models, and collateral evaluation.

Expansion of lending portfolios and diversification of risk through offering a variety of consumer credit options.

Borrowers:

Convenient access to funds for personal expenses and financial needs without requiring immediate upfront payment.

Flexibility in repayment terms, allowing borrowers to choose installment plans or revolving credit lines based on their preferences and financial situations.

Opportunities to build credit history, improve credit scores, and gain access to better credit options and interest rates in the future.

Retailers and Merchants:

Increased sales and revenue through offering point-of-sale financing options, attracting customers who prefer to pay in installments.

Collaboration with credit card issuers or financing providers to offer co-branded cards, loyalty programs, and exclusive discounts.

Improved customer satisfaction and loyalty through seamless and integrated credit options at the point of purchase.

Investors:

Potential for attractive returns through investing in consumer credit-backed securities or participating in peer-to-peer lending platforms.

Portfolio diversification by including consumer credit as an asset class, balancing risk exposure across different financial instruments.

Access to a broad range of investment opportunities across various segments of the consumer credit market.

The consumer credit market benefits various stakeholders, creating opportunities for financial institutions, lenders, borrowers, retailers, and investors to meet their respective objectives and contribute to economic growth.

SWOT Analysis

A SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis provides an overview of the internal and external factors influencing the consumer credit market.

Strengths:

Strong demand for consumer credit, driven by increasing consumer purchasing power and changing lifestyles.

Advancements in financial technology, enabling faster and more convenient loan application processes and risk assessment.

Established banking infrastructure and regulatory frameworks supporting responsible lending practices and consumer protection.

Weaknesses:

Potential for high default rates and credit risks, especially during economic downturns or in subprime lending segments.

Compliance with stringent regulatory requirements, which may limit flexibility and increase operational costs for financial institutions.

Cybersecurity vulnerabilities and the risk of data breaches, which can erode consumer trust and lead to financial losses.

Opportunities:

Growing demand for personalized credit solutions, such as microloans, point-of-sale financing, and alternative lending models.

Expansion in emerging markets, driven by rising middle-class populations and increasing access to financial services.

Integration of artificial intelligence and big data analytics to enhance credit scoring models and risk assessment processes.

Threats:

Economic volatility and fluctuating interest rates, impacting borrowers’ repayment capabilities and credit quality.

Increasing regulatory scrutiny and potential changes in consumer credit regulations, requiring financial institutions to adapt their practices.

Intense competition among traditional banks, online lenders, and fintech startups, leading to margin pressures and the need for differentiation.

Understanding the SWOT analysis helps industry participants identify their strengths, address weaknesses, capitalize on opportunities, and mitigate threats in the consumer credit market.

Market Key Trends

Digital Transformation: The consumer credit market is witnessing a rapid digital transformation, with the adoption of online lending platforms, mobile banking apps, and digital payment solutions. This trend provides convenience, speed, and accessibility to borrowers, streamlines the loan approval process, and enables financial institutions to leverage data for better risk assessment.

Personalized and Alternative Credit Models: Consumers are increasingly seeking personalized credit solutions tailored to their specific needs. Alternative lending models, such as peer-to-peer lending and point-of-sale financing, are gaining traction, offering borrowers more choices and competitive interest rates.

Credit Scoring Innovation: Advancements in data analytics and artificial intelligence are revolutionizing credit scoring models. Traditional credit scores are being supplemented or replaced by alternative data sources, such as utility payments, rental history, and social media profiles, enabling a more holistic assessment of creditworthiness.

ESG Considerations: Environmental, Social, and Governance (ESG) factors are becoming more important in the consumer credit market. Lenders are incorporating ESG criteria into their risk assessment processes and offering sustainable financing options, aligning with the growing demand for responsible and ethical lending.

Open Banking and Data Sharing: Open banking initiatives and data-sharing agreements are emerging, allowing consumers to securely share their financial information with authorized third parties. This trend fosters innovation, competition, and the development of personalized financial services in the consumer credit market.

Rise of Buy Now, Pay Later: The buy now, pay later (BNPL) model is gaining popularity, particularly in e-commerce and retail sectors. BNPL platforms allow consumers to make purchases and pay in installments, often interest-free, providing an alternative to traditional credit cards and increasing affordability.

Focus on Financial Inclusion: Efforts to promote financial inclusion are shaping the consumer credit market. Technology-driven solutions, such as digital wallets and mobile banking, are extending access to credit to underserved populations, empowering them to participate in the formal financial system.

These key trends highlight the evolving nature of the consumer credit market and the need for industry participants to adapt their strategies and offerings to meet changing consumer preferences and market dynamics.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the consumer credit market, creating both challenges and opportunities for industry participants.

Economic Contraction: The pandemic caused a global economic downturn, with many individuals facing reduced incomes, job losses, and financial instability. This led to a decrease in consumer spending and a higher risk of loan defaults.

Increased Loan Delinquencies: As borrowers faced financial hardships, loan delinquencies and default rates rose across various segments of consumer credit. Financial institutions had to increase provisions for bad debts, impacting profitability.

Government Support and Stimulus Packages: Governments implemented fiscal stimulus measures, including loan repayment moratoriums, grants, and loan guarantees, to support individuals and businesses. These measures provided temporary relief to borrowers and prevented a more severe impact on the consumer credit market.

Digital Transformation Acceleration: The pandemic accelerated the shift towards digital channels and online transactions. Financial institutions and lenders had to quickly adapt their processes to facilitate contactless loan applications, electronic signatures, and remote customer verification.

Changing Credit Risk Assessment: The pandemic highlighted the importance of assessing credit risks accurately. Lenders had to factor in new variables, such as the industry-specific impact of lockdowns and the stability of borrowers’ income sources, to make informed lending decisions.

Increased Demand for Liquidity: Some borrowers sought additional credit to cover immediate expenses or bridge income gaps caused by the pandemic. This increased demand for liquidity in the consumer credit market, particularly for personal loans and credit card facilities.

Potential Opportunities: The crisis created opportunities for lenders to develop innovative credit products and services, such as emergency loans, debt consolidation options, and tailored repayment plans, to assist borrowers facing financial difficulties.

The long-term impact of the COVID-19 pandemic on the consumer credit market will depend on the speed of economic recovery, employment levels, and the ability of borrowers to regain financial stability.

Key Industry Developments

Expansion of Fintech Lending Platforms: Fintech companies have witnessed significant growth in the consumer credit market, offering innovative loan products, streamlined processes, and quick approvals. These platforms leverage technology to reach underserved segments, provide competitive interest rates, and improve the customer experience.

Integration of AI and Machine Learning: Artificial intelligence and machine learning algorithms are being increasingly used in the consumer credit market. These technologies enable lenders to automate credit scoring, improve risk assessment models, and detect fraudulent activities, leading to more efficient lending processes and enhanced decision-making.

Regulatory Reforms: Governments and regulatory bodies are implementing reforms to promote responsible lending practices and protect consumers. This includes measures to ensure transparency, prevent predatory lending, and enhance data privacy and security.

Collaboration between Traditional Banks and Fintech Startups: Traditional banks are forming partnerships and collaborations with fintech startups to harness technology and innovation. These collaborations allow banks to enhance their digital capabilities, offer seamless customer experiences, and expand their reach in the consumer credit market.

Sustainable Financing Initiatives: There is a growing emphasis on sustainable financing and ESG considerations in the consumer credit market. Financial institutions are incorporating environmental and social factors into their lending decisions, supporting initiatives such as green loans and financing for renewable energy projects.

Digital Identity Verification: With the rise of digital lending platforms, the need for secure and efficient identity verification processes has become crucial. Digital identity solutions leveraging technologies such as biometrics and blockchain are being developed to streamline and enhance customer verification in the consumer credit market.

These industry developments reflect the ongoing transformation of the consumer credit market, driven by technology advancements, regulatory changes, and evolving consumer expectations.

Analyst Suggestions

Embrace Digital Transformation: Financial institutions and lenders should invest in technology infrastructure, digitize processes, and enhance online customer experiences to meet the evolving demands of consumers in the digital age.

Enhance Risk Management Practices: Given the potential credit risks associated with economic volatility and borrower financial hardships, lenders should strengthen their risk management frameworks, refine credit scoring models, and incorporate alternative data sources to assess creditworthiness accurately.

Foster Financial Inclusion: Efforts to promote financial inclusion should be prioritized, particularly in underserved segments. This can be achieved through collaborations with technology companies, innovative credit products, and financial education programs.

Focus on Customer Experience: Providing exceptional customer experiences is crucial for building customer loyalty and retention. Lenders should strive to offer personalized credit solutions, seamless digital interfaces, and proactive customer support to enhance borrower satisfaction.

Embrace Sustainable Financing: Financial institutions should integrate ESG considerations into their lending practices and explore sustainable financing options. This can help align with evolving consumer preferences and contribute to environmental and social goals.

Monitor Changing Regulatory Landscape: Compliance with evolving regulations is essential to maintain market credibility and meet consumer protection requirements. Financial institutions should stay updated on regulatory changes and adapt their processes and practices accordingly.

Data Security and Privacy: In an increasingly digital landscape, protecting customer data and ensuring data privacy should be a top priority. Robust cybersecurity measures, data encryption, and compliance with data protection regulations are critical for maintaining customer trust.

Future Outlook

The consumer credit market is expected to continue evolving in the coming years, driven by technological advancements, changing consumer preferences, and regulatory developments. Key trends and factors that are likely to shape the future outlook of the market include:

Continued Digital Transformation: The consumer credit market will further embrace digital channels, automation, and artificial intelligence. Online lending platforms, digital wallets, and seamless customer experiences will become the norm.

Greater Personalization: Consumer credit products will become more tailored to individual needs and preferences, leveraging advanced data analytics and alternative credit scoring models.

Focus on Responsible Lending: Regulatory scrutiny and consumer demand for ethical practices will drive the adoption of responsible lending principles, sustainable financing options, and enhanced credit risk management.

Enhanced Financial Inclusion: Efforts to bridge the financial inclusion gap will continue, with technology-driven solutions and partnerships facilitating access to credit for underserved populations.

Integration of Open Banking: Open banking initiatives will gain momentum, allowing consumers to securely share their financial data and benefit from a wider range of personalized financial services.

Evolving Regulatory Landscape: Regulatory frameworks governing the consumer credit market will continue to evolve, focusing on consumer protection, data privacy, and responsible lending practices.

ESG Integration: Environmental and social considerations will play an increasingly important role in the consumer credit market, with financial institutions incorporating ESG factors into their lending decisions and offering sustainable financing options.

Overall, the consumer credit market is poised for growth and transformation, driven by technology-driven innovations, changing consumer expectations, and evolving regulatory requirements.

Conclusion

The consumer credit market serves as a critical component of the global economy, providing individuals with access to funds for various personal expenses. The market continues to evolve, driven by technological advancements, changing consumer preferences, and regulatory developments.

What is consumer credit?

Consumer credit refers to the borrowing of funds by individuals to purchase goods and services, typically through credit cards, personal loans, or installment loans. It plays a crucial role in enabling consumers to manage their finances and make significant purchases without immediate cash availability.

Who are the major players in the consumer credit market?

Major players in the consumer credit market include companies like American Express, Discover Financial Services, and Capital One, which offer various credit products. Additionally, fintech companies such as Affirm and Klarna are increasingly influencing the landscape with innovative lending solutions, among others.

What are the key drivers of growth in the consumer credit market?

Key drivers of growth in the consumer credit market include increasing consumer spending, the rise of e-commerce, and the expansion of credit options available to consumers. Additionally, favorable economic conditions and low-interest rates contribute to higher borrowing levels.

What challenges does the consumer credit market face?

The consumer credit market faces challenges such as rising levels of consumer debt, regulatory scrutiny, and potential economic downturns that can affect repayment rates. Additionally, competition from alternative lending sources can pressure traditional credit providers.

What opportunities exist in the consumer credit market?

Opportunities in the consumer credit market include the growth of digital lending platforms, the increasing demand for flexible payment options, and the potential for personalized credit products based on consumer data. These trends can lead to enhanced customer experiences and greater market penetration.

What trends are shaping the consumer credit market?

Trends shaping the consumer credit market include the rise of buy now, pay later services, increased use of mobile payment solutions, and a focus on responsible lending practices. Additionally, advancements in technology are enabling more efficient credit assessments and personalized offerings.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.