The construction grade cellulose ether market is an integral component of the construction industry, providing essential additives for various construction materials. Cellulose ether, derived from natural cellulose sources, is widely used to enhance the performance and durability of construction products such as mortars, plasters, and tile adhesives. Its properties, including water retention, thickening, and improved workability, make it indispensable in modern construction practices.

Similarly, the industrial film blade market caters to the manufacturing sector, providing precision cutting solutions for industrial films used in packaging, printing, and other applications. Industrial film blades are crucial for achieving clean, accurate cuts in a wide range of film materials, ensuring optimal performance and efficiency in industrial processes.

Meaning

Construction grade cellulose ether refers to a group of water-soluble polymers derived from cellulose, a natural polymer found in plants. These ethers are widely used as additives in construction materials to improve their performance characteristics. Industrial film blades, on the other hand, are specialized cutting tools designed for precise and efficient cutting of industrial films used in manufacturing processes.

Executive Summary

The construction grade cellulose ether market has witnessed significant growth owing to the booming construction industry and the increasing demand for high-performance construction materials. Similarly, the industrial film blade market has experienced steady expansion driven by the growing manufacturing sector and the need for precision cutting solutions. Both markets offer lucrative opportunities for industry participants but are also characterized by stiff competition and evolving customer demands.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The construction grade cellulose ether market is characterized by increasing adoption in the production of cement-based materials, including mortars, plasters, and tile adhesives, due to their ability to improve workability and durability.

Rising investments in infrastructure development and urbanization projects across emerging economies contribute to the market growth, driving demand for high-quality construction additives like cellulose ethers.

Technological advancements in manufacturing processes and sustainable production practices are enhancing the efficiency and eco-friendliness of cellulose ethers, meeting regulatory requirements and consumer preferences for green building materials.

Market segmentation includes various types of cellulose ethers such as methyl cellulose (MC), hydroxyethyl cellulose (HEC), hydroxypropyl methyl cellulose (HPMC), and carboxymethyl cellulose (CMC), each offering unique properties and benefits for specific construction applications.

Market Drivers

Several factors are driving the growth of the construction grade cellulose ether market:

Increased Construction Activities: Global infrastructure development, residential housing projects, and commercial construction activities are boosting the demand for cellulose ethers to improve the performance and durability of construction materials.

Regulatory Emphasis on Sustainability: Stringent regulations promoting sustainable building practices and the use of environmentally friendly construction materials drive the adoption of cellulose ethers, known for their biodegradability and minimal environmental impact.

Advancements in Construction Technology: Innovations in construction methods and materials require additives like cellulose ethers to enhance workability, reduce water consumption, and improve the overall quality of finished structures.

Growing Urbanization and Infrastructure Investments: Rapid urbanization, population growth, and increasing investments in infrastructure projects stimulate the demand for high-performance construction additives, including cellulose ethers, across residential, commercial, and industrial sectors.

Consumer Demand for Enhanced Building Materials: Increasing consumer awareness regarding the benefits of cellulose ethers in improving construction material properties, such as crack resistance, thermal insulation, and fire resistance, fuels market growth.

Market Restraints

Despite the positive growth outlook, the construction grade cellulose ether market faces several challenges:

High Raw Material Costs: Fluctuations in raw material prices, particularly cellulose derivatives, can impact production costs and profit margins for manufacturers, posing challenges for market expansion.

Technical Limitations and Compatibility Issues: Variations in product performance and compatibility with different cement formulations and construction materials may restrict widespread adoption of cellulose ethers in certain applications.

Competitive Alternatives: Availability of alternative additives and construction materials that offer comparable performance characteristics at lower costs may present competitive challenges to cellulose ethers in the market.

Regulatory Compliance and Certification: Meeting stringent regulatory standards and obtaining certifications for cellulose ether products across different regions and applications requires significant investments in research, testing, and compliance.

Impact of Economic Uncertainty: Economic downturns, fluctuating construction budgets, and geopolitical factors affecting global trade can influence market demand and investment decisions in the construction sector.

Market Opportunities

The construction grade cellulose ether market presents several opportunities for growth and innovation:

Product Development and Innovation: Continued research and development efforts to enhance the performance, versatility, and sustainability of cellulose ethers for emerging applications in construction, such as self-healing concrete and 3D printing.

Expansion in Emerging Markets: Penetration into untapped markets in Asia-Pacific, Latin America, and Middle East & Africa, driven by rapid urbanization, infrastructure development, and increasing construction activities.

Collaboration and Partnerships: Strategic collaborations between manufacturers, construction firms, and research institutions to develop customized solutions, address technical challenges, and explore new market opportunities.

Focus on Sustainable Solutions: Investing in eco-friendly production processes, recycling initiatives for cellulose waste, and promoting green building certifications to align with sustainable construction trends and regulatory requirements.

Digitalization and Industry 4.0 Integration: Adoption of digital technologies, IoT-enabled sensors, and data analytics to optimize production processes, improve supply chain efficiency, and offer real-time insights into construction material performance.

Market Dynamics

The construction grade cellulose ether market is dynamic and influenced by trends such as technological advancements, regulatory developments, shifting consumer preferences, and competitive landscape dynamics. Industry stakeholders must adapt strategies to capitalize on emerging opportunities, mitigate risks, and maintain competitive advantage in a rapidly evolving market environment.

Regional Analysis

North America: Mature market with stringent regulatory standards promoting sustainable construction practices and high demand for cellulose ethers in residential and commercial construction sectors.

Europe: Growing adoption of cellulose ethers in renovation and restoration projects, driven by preservation of historical buildings and regulatory emphasis on energy efficiency and environmental sustainability.

Asia-Pacific: Fastest-growing market due to rapid urbanization, infrastructure investments, and increasing construction activities in countries like China, India, and Southeast Asia, fueling demand for high-performance construction additives.

Latin America: Expanding construction industry, government investments in infrastructure development, and rising urban population driving the adoption of cellulose ethers for improved construction material performance.

Middle East & Africa: Infrastructure projects, urban development initiatives, and construction boom in Gulf Cooperation Council (GCC) countries stimulating demand for cellulose ethers to enhance building material quality and durability.

Competitive Landscape

Leading Companies in the Construction Grade Cellulose Ether Market:

Dow Chemical Company

Ashland Global Holdings Inc.

Shin-Etsu Chemical Co., Ltd.

LOTTE Fine Chemical

Samsung Fine Chemicals Co., Ltd.

Daicel Corporation

Shandong Head Co., Ltd.

CP Kelco

J. Rettenmaier & Söhne GmbH + Co. KG

Dairen Chemical Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

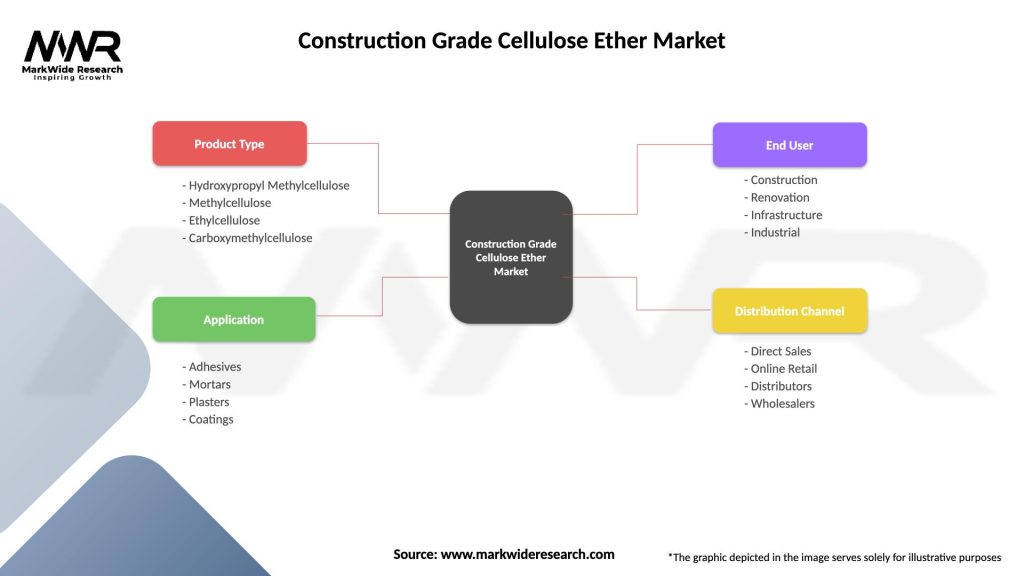

Segmentation

The construction grade cellulose ether market can be segmented based on:

End-Use Sector: Residential Construction, Commercial Construction, Industrial Construction, and Infrastructure.

Region: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa.

Category-wise Insights

Each category of construction grade cellulose ethers offers unique benefits and applications:

Methyl Cellulose (MC): Enhances water retention and improves adhesion in mortars and plasters, ideal for interior wall applications and tile adhesives.

Hydroxyethyl Cellulose (HEC): Provides thickening and rheological control in construction formulations, suitable for exterior renders, cement grouts, and self-leveling compounds.

Hydroxypropyl Methyl Cellulose (HPMC): Offers versatile performance in various construction materials, including cement-based mortars, grouts, and stuccos, balancing water retention and workability.

Carboxymethyl Cellulose (CMC): Enhances viscosity and stability in water-based formulations, used in specialty applications such as decorative plasters, skim coats, and joint compounds.

Key Benefits for Industry Participants and Stakeholders

The construction grade cellulose ether market offers several benefits for manufacturers, contractors, and consumers:

Enhanced Construction Material Performance: Improves workability, adhesion, water retention, and durability of cement-based materials, ensuring high-quality construction finishes and long-term structural integrity.

Regulatory Compliance and Sustainability: Meets regulatory standards for eco-friendly construction materials, reduces environmental impact, and supports green building certifications such as LEED (Leadership in Energy and Environmental Design).

Innovation and Customization: Facilitates product innovation and customization to meet specific construction requirements, offering tailored solutions for different climates, building designs, and application methods.

Operational Efficiency and Cost Savings: Optimizes construction processes, reduces material waste, and enhances productivity on-site through improved material handling, mixing, and application characteristics.

Market Differentiation and Brand Value: Differentiates brands in a competitive market landscape by offering high-performance construction additives that enhance customer satisfaction, project outcomes, and long-term reliability.

SWOT Analysis

Strengths:

Enhanced material properties and performance characteristics, improving construction quality and durability.

Versatile application across diverse construction sectors, including residential, commercial, and infrastructure projects.

Sustainable and eco-friendly additives meeting regulatory requirements and consumer preferences for green building materials.

Weaknesses:

High dependency on cellulose derivatives as raw materials, subject to price fluctuations and supply chain disruptions.

Technical challenges in product formulation and compatibility with varying construction materials and additives.

Opportunities:

Expansion into emerging markets with rising construction activities and infrastructure development.

Innovation in cellulose ether technologies, including bio-based alternatives and advanced formulations for specialized applications.

Strategic partnerships and collaborations to drive research, development, and market penetration in untapped regions and sectors.

Threats:

Competitive pressure from alternative additives and substitutes offering comparable performance benefits at lower costs.

Economic volatility, currency fluctuations, and geopolitical factors impacting global supply chains and market demand.

Stringent regulatory changes and compliance requirements affecting production, distribution, and market access.

Market Key Trends

Several key trends are shaping the construction grade cellulose ether market:

Technological Advancements: Continued R&D efforts to enhance cellulose ether functionalities, develop bio-based alternatives, and integrate smart technologies for improved construction material performance.

Sustainability and Environmental Focus: Growing demand for eco-friendly construction additives, promoting recycling, waste reduction, and carbon footprint mitigation in building practices.

Digitalization and Industry 4.0 Integration: Adoption of digital tools, IoT devices, and data analytics to optimize construction processes, enhance product quality control, and improve project management efficiency.

Urbanization and Infrastructure Investments: Rapid urban development, smart city initiatives, and government investments in sustainable infrastructure driving demand for high-performance construction materials.

Consumer Demand for Quality and Durability: Increasing awareness among consumers, architects, and contractors regarding the benefits of cellulose ethers in ensuring long-lasting, aesthetically pleasing, and structurally sound building designs.

Covid-19 Impact

The Covid-19 pandemic has influenced the construction grade cellulose ether market in various ways:

Disruption in Supply Chain: Temporary disruptions in raw material supply chains, logistics, and manufacturing operations affecting production schedules and market availability.

Construction Activity Slowdown: Temporary halts or delays in construction projects, leading to reduced demand for construction additives including cellulose ethers during lockdowns and economic uncertainties.

Shift in Consumer Behavior: Increased focus on health, safety, and sustainability influencing construction material preferences and specifications post-pandemic recovery phases.

Accelerated Digital Transformation: Adoption of remote work practices, digital tools, and virtual collaboration platforms to manage construction projects, driving digitalization and efficiency improvements in construction processes.

Regulatory and Compliance Adjustments: Adaptation to new health and safety protocols, regulatory changes, and building codes impacting construction practices and material specifications.

Key Industry Developments

Product Innovations: Launch of new cellulose ether formulations, improved functionalities, and sustainable product lines to meet evolving market demands for performance, efficiency, and environmental stewardship.

Technological Advancements: Integration of advanced additives, smart technologies, and digital solutions to optimize cellulose ether performance, production processes, and end-user applications.

Sustainability Initiatives: Investments in eco-friendly manufacturing practices, recycling initiatives, and green certifications to enhance market competitiveness and meet regulatory requirements.

Market Expansion Strategies: Geographic expansion into emerging markets, strategic acquisitions, and partnerships to strengthen market presence, distribution networks, and customer relationships.

Response to Market Challenges: Resilience strategies, operational adjustments, and contingency plans to mitigate risks, manage supply chain disruptions, and maintain business continuity in dynamic market conditions.

Analyst Suggestions

Based on market insights and developments, analysts recommend the following strategies for industry participants:

Innovation and Differentiation: Focus on R&D to innovate cellulose ether products, enhance performance attributes, and differentiate offerings through unique functionalities, sustainability credentials, and value-added solutions.

Market Diversification: Expand product portfolios, target new applications and end-user sectors, and explore untapped geographic markets to capture growth opportunities and mitigate market volatility risks.

Collaboration and Partnerships: Form strategic alliances with construction firms, architects, regulatory bodies, and technology providers to co-develop solutions, address market challenges, and drive innovation leadership.

Sustainability Commitment: Invest in sustainable practices, eco-friendly product lines, and green certifications to align with global sustainability goals, enhance brand reputation, and meet customer expectations.

Digital Transformation: Embrace digital technologies, IoT-enabled solutions, and data analytics to optimize production efficiency, improve supply chain visibility, and deliver enhanced customer value and service.

Future Outlook

The future outlook for the construction grade cellulose ether market is optimistic, with sustained growth expected driven by urbanization trends, infrastructure investments, regulatory support for sustainable construction practices, and advancements in construction technology. As the industry focuses on resilience, innovation, and sustainability, cellulose ethers are poised to play a crucial role in shaping the next generation of high-performance, eco-friendly construction materials.

Conclusion

In conclusion, the construction grade cellulose ether market is poised for significant growth, driven by increasing construction activities, regulatory emphasis on sustainability, technological advancements, and consumer demand for high-performance building materials. Despite challenges such as raw material costs, technical complexities, and competitive pressures, the market offers ample opportunities for innovation, market expansion, and industry collaboration. By prioritizing innovation, sustainability, digitalization, and strategic partnerships, industry stakeholders can navigate market dynamics, capitalize on emerging trends, and contribute to sustainable development in the global construction sector.

What is Construction Grade Cellulose Ether?

Construction Grade Cellulose Ether refers to a group of cellulose derivatives used in construction applications, primarily as thickening agents, binders, and additives in cement, mortar, and plaster formulations.

What are the key players in the Construction Grade Cellulose Ether Market?

Key players in the Construction Grade Cellulose Ether Market include companies like Dow Chemical Company, Ashland Global Holdings, and AkzoNobel, among others.

What are the growth factors driving the Construction Grade Cellulose Ether Market?

The growth of the Construction Grade Cellulose Ether Market is driven by increasing demand for sustainable building materials, the rise in construction activities, and the need for improved performance in construction applications.

What challenges does the Construction Grade Cellulose Ether Market face?

Challenges in the Construction Grade Cellulose Ether Market include fluctuating raw material prices, stringent regulations regarding chemical usage, and competition from alternative materials.

What opportunities exist in the Construction Grade Cellulose Ether Market?

Opportunities in the Construction Grade Cellulose Ether Market include the development of innovative cellulose ether formulations, expansion into emerging markets, and increasing applications in eco-friendly construction practices.

What trends are shaping the Construction Grade Cellulose Ether Market?

Trends in the Construction Grade Cellulose Ether Market include the growing focus on sustainability, advancements in manufacturing technologies, and the increasing use of cellulose ethers in high-performance construction materials.

Leading Companies in the Construction Grade Cellulose Ether Market:

Dow Chemical Company

Ashland Global Holdings Inc.

Shin-Etsu Chemical Co., Ltd.

LOTTE Fine Chemical

Samsung Fine Chemicals Co., Ltd.

Daicel Corporation

Shandong Head Co., Ltd.

CP Kelco

J. Rettenmaier & Söhne GmbH + Co. KG

Dairen Chemical Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.