Compression therapy devices are medical devices designed to improve circulation and promote healing in patients suffering from conditions such as deep vein thrombosis (DVT), lymphedema, varicose veins, and venous leg ulcers. These devices apply controlled pressure to the affected areas, assisting blood flow and reducing swelling. In recent years, the compression therapy devices market has witnessed significant growth due to the rising prevalence of chronic diseases and an aging population.

Compression therapy involves the use of external pressure through specially designed garments or devices to improve blood circulation. By applying compression to the limbs or affected areas, these devices help reduce edema, minimize pain, and enhance overall vascular function. Compression therapy can be categorized into static compression (where pressure remains constant) and dynamic compression (where pressure is periodically adjusted).

Executive Summary

The compression therapy devices market has experienced robust growth in recent years, driven by the increasing incidence of venous disorders, obesity, and sports-related injuries. The market is characterized by a wide range of products, including compression stockings, sleeves, bandages, and pumps. Hospitals, clinics, and home healthcare settings are the primary end-users of these devices. With advancements in technology, the market has witnessed the introduction of innovative and user-friendly compression therapy devices.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Elastic stockings account for over 50% of market volume, favored for long-term management of chronic venous insufficiency.

Intermittent pneumatic compression systems are projected to grow at a CAGR of 7–8% over the next five years, driven by improved portability and digital monitoring features.

Compression bandages remain essential in wound care clinics, particularly for venous leg ulcer management, representing a stable, albeit mature, market segment.

Home care adoption is rising, with over 40% of IPC devices now sold directly to patients under tele-health programs.

Regulatory approvals of class II medical devices and updated clinical guidelines by vascular societies are accelerating clinician adoption.

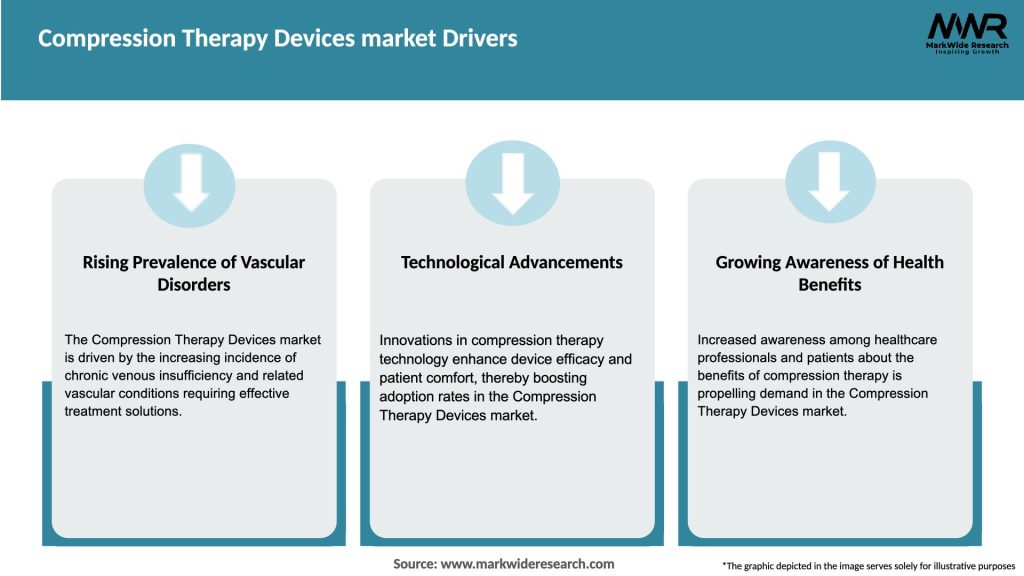

Market Drivers

Rising Prevalence of Vascular Disorders: An estimated 40% of adults suffer from some form of venous insufficiency, creating a large addressable population.

Aging Population: Global geriatric demographics, projected to double by 2050, are more susceptible to lymphedema and chronic edema.

Home-Care Shift: Telemedicine and remote monitoring programs favor at-home compression devices that reduce hospital readmissions.

Technological Innovation: Development of smart compression garments with embedded pressure sensors enhances therapy personalization and compliance.

Preventive Applications: Growing use of IPC for DVT prophylaxis in surgical wards and during long-haul flights expands market use cases.

Market Restraints

Patient Compliance Issues: Discomfort and difficulty donning tight compression garments can hinder long-term adherence.

Reimbursement Variability: Inconsistent insurance coverage across regions may limit access, especially for premium IPC systems.

Device Costs: High initial cost of motorized IPC pumps can deter healthcare providers and patients in cost-sensitive markets.

Clinical Training Requirements: Proper fitting and parameter adjustment necessitate trained personnel, slowing widespread use.

Skin Irritation Risks: Prolonged use of tight stockings or bandages can cause dermatitis or pressure injuries if not monitored.

Market Opportunities

Smart Textiles: Integration of wireless connectivity and apps for real-time pressure monitoring can improve adherence and outcomes.

Tele-Rehabilitation Platforms: Bundling compression devices with remote therapy protocols addresses post-surgical and chronic care needs.

Emerging Markets: Expansion into Asia Pacific and Latin America where rising healthcare spending and aging populations drive demand.

Custom-Fit Solutions: 3D scanning and on-demand manufacturing of personalized compression garments can enhance patient comfort.

Combination Therapies: Integrating compression with electrical muscle stimulation or infrared therapy presents novel treatment modalities.

Market Dynamics

Private-Label vs. Branded: Retail chains and e-commerce players are introducing private-label compression stockings, intensifying price competition.

Service-Based Models: Rental and subscription services for IPC devices lower upfront costs and encourage ongoing engagement.

Clinical Guidelines: Updated consensus statements from vascular societies are standardizing compression protocols, boosting device utilization.

Multi-Chamber Systems: IPC pumps with sequential chamber inflation improve hemodynamic response compared to single-chamber designs.

Cross-Channel Distribution: Growth of online direct-to-consumer sales complements traditional medical supply and pharmacy channels.

Regional Analysis

North America: Largest revenue share, driven by high awareness, strong reimbursement, and advanced home-care programs.

Europe: Mature market with established compression hosiery adoption; Germany, France, and the UK lead volume sales.

Asia Pacific: Fastest growth region, propelled by expanding geriatric care, growing middle class, and increasing physician awareness in China and India.

Latin America: Emerging opportunities in surgical prophylaxis and chronic care as healthcare access improves.

Middle East & Africa: Nascent market with growth tied to private-sector hospital expansion and expatriate health programs.

Competitive Landscape

Leading Companies in the Compression Therapy Devices Market:

3M Company

BSN medical GmbH (Essity AB)

Sigvaris Group

Cardinal Health, Inc.

Medtronic plc

Tactile Medical

ArjoHuntleigh (Getinge AB)

DJO Global, Inc.

Bio Compression Systems, Inc.

PAUL HARTMANN AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

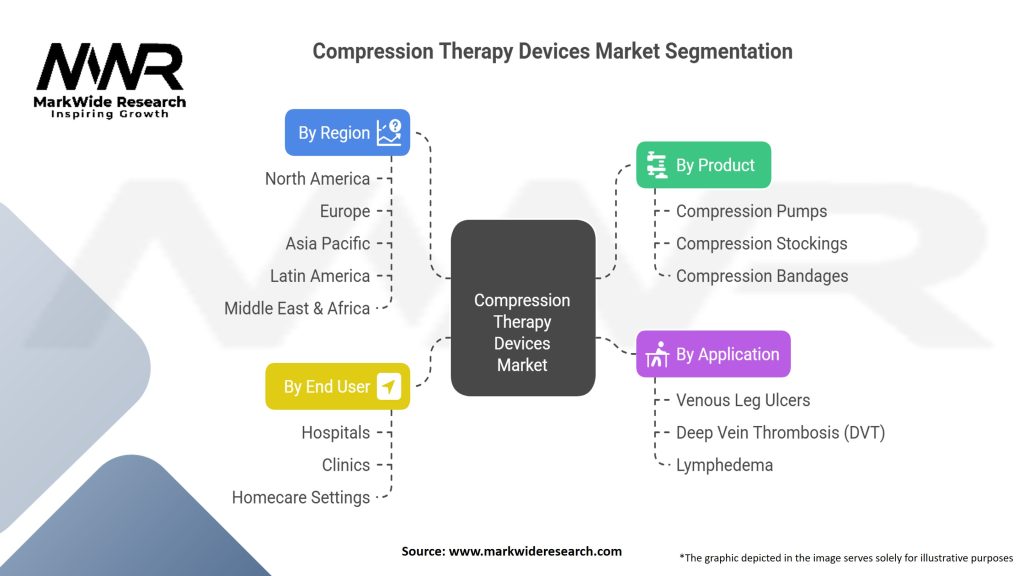

Segmentation

The compression therapy devices market can be segmented based on product type, application, end-user, and geography.

By Product Type:

Compression Stockings

Compression Sleeves

Compression Bandages

Compression Pumps

Others

By Application:

Deep Vein Thrombosis (DVT)

Lymphedema

Varicose Veins

Wound Care

Others

By End-User:

Hospitals

Clinics

Home Healthcare Settings

By Geography:

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Category-wise Insights

Compression Stockings: Available in Classes I–IV, provide continuous pressure; Class II (20–30 mmHg) is most commonly prescribed for chronic venous disease.

IPC Systems: Portable pumps with single or multi-chamber garments; used for DVT prophylaxis and lymphedema management in both hospital and home settings.

Compression Bandages: Short-stretch and long-stretch bandages used primarily in wound care clinics for venous leg ulcers and lymphedema decongestion.

Compression Wraps: Multi-panel adjustable garments offering customizable pressure, popular in home therapy for ease of application.

Key Benefits for Industry Participants and Stakeholders

Improved Clinical Outcomes: Enhanced venous and lymphatic circulation leads to faster ulcer healing and reduced edema.

Reduced Healthcare Costs: Preventing DVT and managing chronic edema can lower hospitalization rates and long-term care expenses.

Patient Empowerment: Home-use systems and tele-rehabilitation models promote self-management and quality of life.

Product Differentiation: Smart-device integration and custom-fit offerings allow manufacturers to capture premium segments.

Regulatory Alignment: Compliance with FDA (510(k)) and CE marking ensures global market access and clinician trust.

SWOT Analysis Strengths:

Proven efficacy backed by clinical guidelines.

Diverse product range addressing acute and chronic care.

Growing home-care and telehealth integration.

Weaknesses:

Patient discomfort and adherence challenges.

High upfront costs for motorized IPC devices.

Dependence on trained personnel for proper fitting.

Opportunities:

Smart textile and IoT integration to boost compliance.

Expansion in emerging markets with rising chronic-disease prevalence.

Development of eco-friendly, recyclable compression garments.

Threats:

Competition from pharmacological DVT prophylaxis and advanced wound dressings.

Reimbursement cuts or changing insurance policies.

Eco-Friendly Materials: Biodegradable elastomers and recycled fibers respond to sustainability demands.

Digital Therapeutics Bundles: Compression devices paired with guided exercise apps and tele-consultation platforms to enhance rehabilitation.

Covid-19 Impact The pandemic accelerated home-care adoption of IPC systems as hospitals deferred elective procedures and prioritized DVT prophylaxis in bedridden COVID-19 patients. Supply-chain disruptions in 2020 led to shortages of premium stockings and pumps, prompting manufacturers to localize production. Virtual fitting services and online sales channels expanded rapidly as in-person clinic visits declined.

Key Industry Developments

BSN Medical launched the JOBST SmartCompression™ line in 2023, featuring embedded pressure sensors and smartphone integration.

3M introduced a portable, battery-powered IPC pump with customizable inflation profiles, approved for home use in 2024.

ArjoHuntleigh expanded its clinical-grade IPC portfolio with multi-chamber garments optimized for lower-limb and upper-limb therapy.

Sigvaris partnered with a telehealth platform to offer remote fitting and compliance monitoring services for compression stockings.

Analyst Suggestions

Invest in Patient Education: Provide digital tutorials and virtual fitting sessions to improve adherence and outcomes.

Expand Service Models: Develop rental and subscription options for IPC pumps to lower access barriers.

Leverage Data Analytics: Use usage data from smart devices to refine therapy protocols and demonstrate value to payers.

Localize Manufacturing: Establish regional assembly or manufacturing to mitigate supply-chain disruptions and reduce costs.

Pursue Sustainable Innovations: Adopt eco-friendly materials and recyclable packaging to meet emerging regulatory and consumer expectations.

Future Outlook The Compression Therapy Devices market is expected to grow at a healthy CAGR of 5–6% through 2030, driven by technological innovations, expanding home-care models, and increasing prevalence of chronic vascular and lymphatic disorders. Smart, connected devices and personalized compression solutions will redefine therapy paradigms, while emerging markets in APAC and Latin America offer significant untapped potential. Partnerships between device manufacturers, tele-health providers, and clinical specialists will be critical in delivering integrated care pathways that improve patient outcomes and reduce healthcare costs.

Conclusion In conclusion, the Compression Therapy Devices market stands at the intersection of clinical efficacy, technological innovation, and patient-centric care. Stakeholders who focus on smart device integration, service-oriented models, and sustainable product development will lead market transformation. As healthcare systems continue to shift toward value-based and home-centered care, compression therapy devices will play an increasingly vital role in vascular and lymphatic disease management, offering both clinical and economic benefits.

What is Compression Therapy Devices?

Compression therapy devices are medical tools designed to apply controlled pressure to specific areas of the body, primarily used to improve blood circulation, reduce swelling, and aid in the recovery of various conditions such as venous insufficiency and lymphedema.

What are the key players in the Compression Therapy Devices market?

Key players in the Compression Therapy Devices market include DJO Global, Inc., Medtronic, and Tactile Medical, which are known for their innovative products and solutions in the field of compression therapy, among others.

What are the main drivers of growth in the Compression Therapy Devices market?

The growth of the Compression Therapy Devices market is driven by an increasing prevalence of chronic venous diseases, a rising aging population, and growing awareness about the benefits of compression therapy in post-surgical recovery and sports medicine.

What challenges does the Compression Therapy Devices market face?

Challenges in the Compression Therapy Devices market include the high cost of advanced devices, the need for proper training for healthcare professionals, and potential patient discomfort during use, which can hinder adoption rates.

What opportunities exist in the Compression Therapy Devices market?

Opportunities in the Compression Therapy Devices market include the development of smart compression devices with integrated monitoring technology, expansion into emerging markets, and increasing applications in sports medicine and rehabilitation.

What trends are shaping the Compression Therapy Devices market?

Trends in the Compression Therapy Devices market include the integration of wearable technology, advancements in materials for better comfort and effectiveness, and a growing focus on personalized therapy solutions tailored to individual patient needs.

Leading Companies in the Compression Therapy Devices Market:

3M Company

BSN medical GmbH (Essity AB)

Sigvaris Group

Cardinal Health, Inc.

Medtronic plc

Tactile Medical

ArjoHuntleigh (Getinge AB)

DJO Global, Inc.

Bio Compression Systems, Inc.

PAUL HARTMANN AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.