The commercial vehicle aluminum casting market plays a crucial role in the automotive industry, particularly in the manufacturing of trucks, buses, and other heavy-duty vehicles. Aluminum casting involves the process of melting aluminum and pouring it into molds to create complex shapes and components used in vehicle construction. This market segment is driven by the demand for lightweight, durable, and fuel-efficient vehicle components, which are essential for improving vehicle performance and meeting stringent regulatory standards.

Meaning

Commercial vehicle aluminum casting refers to the manufacturing process of shaping aluminum into specific components used in commercial vehicles. These components include engine parts, transmission housings, wheels, chassis parts, and structural components. Aluminum casting offers advantages such as weight reduction, corrosion resistance, and design flexibility, making it a preferred choice for vehicle manufacturers aiming to enhance vehicle efficiency and performance.

Executive Summary

The commercial vehicle aluminum casting market has experienced significant growth due to advancements in automotive technology, increasing demand for fuel-efficient vehicles, and regulatory pressures to reduce emissions. This market provides lucrative opportunities for industry players involved in aluminum casting processes, although it faces challenges such as fluctuating raw material costs and competitive pressures. Understanding key market insights, technological trends, and regulatory dynamics is crucial for stakeholders aiming to capitalize on market growth.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Demand for Lightweight Materials: The shift towards lightweight materials in commercial vehicles is driven by the need to improve fuel efficiency and reduce carbon emissions. Aluminum casting enables manufacturers to achieve weight savings while maintaining structural integrity and safety standards.

Technological Advancements: Innovations in aluminum casting technologies, such as high-pressure die casting (HPDC) and squeeze casting, have enhanced production efficiency and product quality in the commercial vehicle sector. These advancements support the development of complex, lightweight aluminum components.

Regulatory Requirements: Stringent environmental regulations mandating lower vehicle emissions and higher fuel efficiency standards have propelled the adoption of aluminum components in commercial vehicles. Aluminum’s recyclability and lower carbon footprint further align with sustainability goals.

Market Growth Drivers: Increasing investments in infrastructure development, rising demand for logistics and transportation services, and expansion in the construction and mining sectors are driving the demand for commercial vehicles, thereby boosting the market for aluminum castings.

Market Drivers

Fuel Efficiency and Emission Regulations: Regulatory mandates for reducing vehicle emissions and improving fuel efficiency drive the demand for lightweight materials like aluminum in commercial vehicles. Aluminum casting helps manufacturers meet these stringent standards without compromising vehicle performance.

Cost Efficiency: Aluminum casting offers cost advantages over traditional materials like steel, as it requires less energy for production and offers superior corrosion resistance, reducing maintenance costs over the vehicle’s lifespan.

Design Flexibility: The ability of aluminum casting to create complex shapes and intricate designs allows for innovative vehicle architectures and improved aerodynamics, contributing to enhanced vehicle performance and fuel economy.

End-Use Applications: Growing applications of aluminum castings in engine blocks, transmission components, structural parts, and chassis systems in commercial vehicles drive market expansion. These components contribute to vehicle durability, safety, and operational efficiency.

Market Restraints

Raw Material Price Volatility: Fluctuations in aluminum prices impact production costs and profit margins for manufacturers. Economic factors and global supply chain disruptions can lead to unpredictable raw material costs, affecting market stability.

High Initial Investment: The capital-intensive nature of aluminum casting facilities and equipment requires significant upfront investments. This barrier to entry limits the market entry of small and medium-sized enterprises (SMEs) and new players, restricting market competitiveness.

Competitive Pressure: Intense competition among aluminum casting suppliers and manufacturers in the commercial vehicle sector necessitates continuous innovation, quality improvement, and cost optimization to maintain market share and profitability.

Technological Challenges: Despite advancements, challenges such as casting defects, process variability, and quality control issues persist in aluminum casting. Overcoming these technological barriers is essential for ensuring consistent product quality and reliability.

Market Opportunities

Electric and Hybrid Vehicles: The shift towards electric and hybrid commercial vehicles presents opportunities for aluminum casting manufacturers. Lightweight aluminum components contribute to extended vehicle range and battery life, supporting the electrification trend.

Emerging Markets: Expansion opportunities in emerging economies with growing industrialization, infrastructure development, and transportation needs offer a fertile ground for commercial vehicle aluminum casting. Market penetration in regions like Asia-Pacific and Latin America presents untapped growth potential.

Recycling Initiatives: Increasing focus on sustainable practices and circular economy principles drives the demand for recycled aluminum in casting applications. Recycling reduces environmental impact, enhances resource efficiency, and supports green manufacturing practices.

Supply Chain Integration: Strategic collaborations and partnerships along the supply chain enable aluminum casting manufacturers to optimize logistics, enhance product distribution, and offer comprehensive solutions to commercial vehicle OEMs.

Market Dynamics

The commercial vehicle aluminum casting market operates in a dynamic environment influenced by technological advancements, regulatory developments, economic conditions, and shifting consumer preferences. These dynamics shape market trends, demand patterns, and competitive strategies, requiring stakeholders to adapt and innovate to maintain market relevance and profitability.

Regional Analysis

North America: The mature automotive industry and stringent emissions regulations in North America drive the adoption of aluminum casting in commercial vehicles. Market growth is supported by investments in lightweight materials and sustainable manufacturing practices.

Europe: Europe leads in automotive innovation and environmental sustainability, driving demand for aluminum casting in commercial vehicle applications. The region’s focus on reducing CO2 emissions and enhancing vehicle efficiency accelerates market expansion.

Asia-Pacific: Rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Japan fuel the demand for commercial vehicles and aluminum casting. Asia-Pacific emerges as a lucrative market due to expanding logistics networks and increasing transportation needs.

Latin America: The growing construction and mining sectors in Latin America create opportunities for aluminum casting in heavy-duty commercial vehicles. Economic growth, coupled with infrastructure investments, stimulates market growth in the region.

Middle East and Africa: Infrastructure development projects and investments in transportation infrastructure drive demand for commercial vehicles and associated aluminum casting components. Strategic location as a transit hub enhances market prospects in the Middle East and Africa.

Competitive Landscape

Leading Companies in the Commercial Vehicle Aluminum Casting Market

Nemak

Ryobi Limited

Martinrea Hitech

Alcoa Corporation

Bühler Group

LINAMAR Corporation

Inteva Products

GF Automotive

Castrol Limited

ZF Friedrichshafen AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

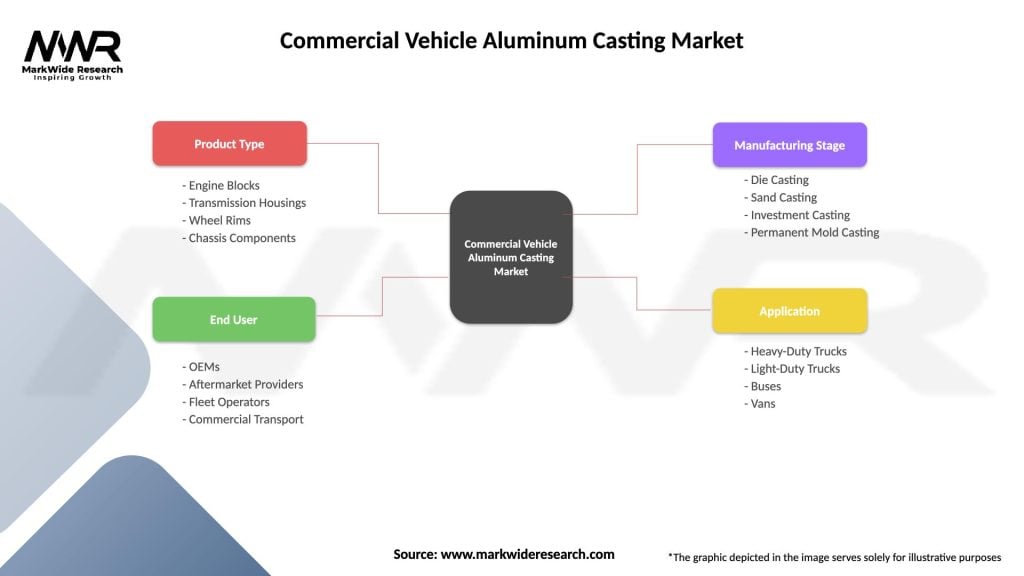

Segmentation

The commercial vehicle aluminum casting market can be segmented based on:

Vehicle Type: Trucks, buses, trailers, and other heavy-duty vehicles.

Process Type: High-pressure die casting (HPDC), low-pressure die casting (LPDC), and gravity die casting.

Application: OEMs and aftermarket.

Region: North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa.

Segmentation provides insights into market dynamics, customer preferences, and growth opportunities tailored to specific market segments.

Category-wise Insights

Engine Components: Aluminum casting enhances engine performance by reducing weight and improving thermal management. Components include cylinder heads, pistons, and engine blocks, contributing to fuel efficiency and emission reduction.

Transmission Systems: Lightweight aluminum transmission housings and components optimize vehicle powertrain performance, ensuring smooth gear shifting and operational reliability in commercial vehicles.

Chassis and Suspension: Aluminum chassis components and suspension parts improve vehicle handling, stability, and ride comfort. Enhanced durability and corrosion resistance extend component lifespan in challenging operating conditions.

Wheels and Brakes: Aluminum wheels offer weight savings and aesthetic appeal, enhancing vehicle aesthetics and fuel efficiency. Aluminum brake components provide heat dissipation and braking performance in heavy-duty applications.

Key Benefits for Industry Participants and Stakeholders

Performance Enhancement: Aluminum casting enhances vehicle performance through weight reduction, improved fuel efficiency, and optimized component design, meeting the performance demands of commercial vehicle OEMs and end-users.

Cost Efficiency: Reduced material and manufacturing costs associated with aluminum casting offer cost advantages over conventional materials, supporting OEMs in achieving cost-effective vehicle production and competitive pricing strategies.

Sustainability: Aluminum’s recyclability and lower carbon footprint align with industry sustainability goals, promoting environmentally responsible manufacturing practices and enhancing corporate social responsibility (CSR) initiatives.

Innovation and Customization: Advanced casting technologies enable innovation in component design and customization, meeting diverse customer requirements for performance, durability, and regulatory compliance in commercial vehicle applications.

SWOT Analysis

Strengths:

Lightweight and durable material properties.

Enhanced vehicle performance and fuel efficiency.

Design flexibility and complex geometry capabilities.

Recyclability and sustainability advantages.

Weaknesses:

Vulnerability to raw material price fluctuations.

High initial investment in casting equipment.

Technical challenges in process optimization.

Opportunities:

Expansion in electric and hybrid vehicle markets.

Growing demand for lightweight materials in commercial vehicles.

Strategic alliances and partnerships for market expansion.

Economic volatility and global supply chain disruptions.

Market Key Trends

Electrification and Lightweighting: Increasing adoption of electric and hybrid commercial vehicles necessitates lightweight materials like aluminum casting to optimize vehicle efficiency and range, driving market growth for aluminum casting manufacturers.

Advanced Casting Technologies: Technological advancements in high-pressure die casting (HPDC), low-pressure die casting (LPDC), and squeeze casting techniques enhance production efficiency, product quality, and design capabilities. These innovations cater to the growing demand for complex, lightweight aluminum components in commercial vehicles.

Sustainable Practices: Industry focus on sustainable manufacturing practices, including aluminum recycling and waste reduction initiatives, supports environmental stewardship and regulatory compliance. Sustainability-driven consumer preferences and corporate sustainability goals drive the adoption of aluminum casting in commercial vehicle applications.

Digitalization and Industry 4.0: Integration of digital technologies, automation, and data analytics in aluminum casting processes enhances operational efficiency, quality control, and predictive maintenance capabilities. Industry 4.0 initiatives enable real-time monitoring, process optimization, and cost management in commercial vehicle manufacturing.

Supply Chain Resilience: Strategic supply chain management, including localization of production facilities and raw material sourcing diversification, strengthens resilience against global disruptions, geopolitical uncertainties, and supply chain risks affecting aluminum casting operations.

COVID-19 Impact

The COVID-19 pandemic significantly impacted the commercial vehicle aluminum casting market, disrupting supply chains, reducing vehicle production volumes, and delaying new product launches. Lockdown measures, economic downturns, and fluctuating consumer demand affected market dynamics, requiring adaptive strategies, remote working protocols, and enhanced safety measures to mitigate operational challenges and maintain business continuity.

Key Industry Developments

Collaborative Partnerships: Collaborations between aluminum casting manufacturers, commercial vehicle OEMs, and technology providers foster innovation, product development, and market expansion strategies. Joint ventures, strategic alliances, and research partnerships strengthen industry competitiveness and technological leadership in the commercial vehicle sector.

Investment in R&D: Continued investments in research and development (R&D) initiatives, including material science advancements, process innovations, and product design enhancements, drive technological breakthroughs and market differentiation in aluminum casting applications for commercial vehicles.

Market Expansion Strategies: Geographic expansion into emerging markets, capacity expansions, and facility modernizations enhance production capabilities, supply chain efficiencies, and market presence for aluminum casting manufacturers targeting global commercial vehicle markets.

Analyst Suggestions

Diversification Strategies: Aluminum casting manufacturers should diversify their product portfolios, customer base, and geographic reach to mitigate risks associated with market volatility, economic uncertainties, and competitive pressures in the commercial vehicle sector.

Technological Innovation: Continuous investment in advanced casting technologies, automation solutions, and digital transformation initiatives improves manufacturing efficiency, product quality, and operational agility. Embracing Industry 4.0 principles and digitalization enhances competitiveness and resilience in a rapidly evolving market landscape.

Sustainability Initiatives: Prioritizing sustainability practices, including aluminum recycling, energy-efficient production processes, and carbon footprint reduction strategies, aligns with regulatory requirements, customer expectations, and corporate sustainability goals. Sustainable manufacturing practices enhance brand reputation, mitigate environmental impacts, and foster long-term industry leadership.

Market Intelligence and Forecasting: Leveraging market intelligence, data analytics, and predictive modeling techniques enables aluminum casting manufacturers to anticipate market trends, customer preferences, and competitive dynamics. Real-time insights support informed decision-making, strategic planning, and proactive response to market challenges and opportunities.

Future Outlook

The commercial vehicle aluminum casting market is poised for steady growth driven by increasing demand for lightweight, fuel-efficient vehicles, technological advancements in casting processes, and expanding applications in electric and hybrid vehicle platforms. Continued emphasis on sustainability, innovation in material science, and strategic partnerships will shape the industry’s evolution, positioning aluminum casting manufacturers as key contributors to the global automotive supply chain.

Conclusion

The commercial vehicle aluminum casting market represents a critical segment of the automotive industry, characterized by technological innovation, regulatory compliance, and sustainability-driven manufacturing practices. As demand for lightweight materials and energy-efficient vehicles accelerates, aluminum casting manufacturers are poised to capitalize on growth opportunities through advanced technologies, market diversification, and strategic investments. By embracing digitalization, sustainable practices, and collaborative partnerships, industry stakeholders can navigate evolving market dynamics, enhance operational resilience, and drive sustainable growth in the competitive global marketplace.

What is Commercial Vehicle Aluminum Casting?

Commercial Vehicle Aluminum Casting refers to the process of creating components for commercial vehicles using aluminum alloys. This method is favored for its lightweight properties, corrosion resistance, and ability to produce complex shapes, making it ideal for parts like engine blocks and transmission housings.

What are the key players in the Commercial Vehicle Aluminum Casting Market?

Key players in the Commercial Vehicle Aluminum Casting Market include companies like Nemak, Alcoa Corporation, and Ryobi Limited, which specialize in manufacturing aluminum castings for various commercial vehicle applications, among others.

What are the main drivers of the Commercial Vehicle Aluminum Casting Market?

The main drivers of the Commercial Vehicle Aluminum Casting Market include the increasing demand for lightweight materials to improve fuel efficiency, the growing trend of electric vehicles requiring specialized components, and advancements in casting technologies that enhance production efficiency.

What challenges does the Commercial Vehicle Aluminum Casting Market face?

Challenges in the Commercial Vehicle Aluminum Casting Market include the high initial costs of aluminum compared to traditional materials, potential supply chain disruptions for raw materials, and the need for skilled labor to handle advanced casting techniques.

What opportunities exist in the Commercial Vehicle Aluminum Casting Market?

Opportunities in the Commercial Vehicle Aluminum Casting Market include the rising adoption of electric and hybrid vehicles, which require lightweight components, and the potential for innovation in recycling aluminum, which can reduce costs and environmental impact.

What trends are shaping the Commercial Vehicle Aluminum Casting Market?

Trends shaping the Commercial Vehicle Aluminum Casting Market include the increasing use of advanced manufacturing techniques like 3D printing for prototypes, the integration of smart technologies in vehicle components, and a growing focus on sustainability and reducing carbon footprints in production processes.

Leading Companies in the Commercial Vehicle Aluminum Casting Market

Nemak

Ryobi Limited

Martinrea Hitech

Alcoa Corporation

Bühler Group

LINAMAR Corporation

Inteva Products

GF Automotive

Castrol Limited

ZF Friedrichshafen AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.