The commercial banking market plays a crucial role in the global economy by providing a wide range of financial services to businesses, corporations, and individuals. Commercial banks serve as intermediaries between depositors and borrowers, facilitating the flow of capital and supporting economic growth. This comprehensive article provides insights into the commercial banking market, including its meaning, executive summary, key market insights, market drivers, market restraints, market opportunities, market dynamics, regional analysis, competitive landscape, segmentation, category-wise insights, key benefits for industry participants and stakeholders, SWOT analysis, market key trends, Covid-19 impact, key industry developments, analyst suggestions, future outlook, and conclusion.

Commercial banking refers to the activities and services provided by banks to businesses, corporations, and various financial institutions. These services include accepting deposits, granting loans, offering credit facilities, facilitating international trade transactions, providing treasury and cash management solutions, investment banking services, and more. Commercial banks act as financial intermediaries, mobilizing funds from depositors and channeling them towards productive economic activities. They play a pivotal role in facilitating economic growth, managing risks, and providing financial stability.

Executive Summary

The commercial banking market has witnessed significant growth and transformation over the years, driven by globalization, technological advancements, regulatory changes, and evolving customer demands. This executive summary provides a concise overview of the commercial banking market, highlighting key trends, market dynamics, and future prospects. It serves as a quick reference point for industry professionals, investors, and stakeholders seeking an overview of the market landscape and its key drivers.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Increasing Globalization: Globalization has expanded business horizons, leading to increased cross-border trade and investment activities. Commercial banks play a vital role in facilitating international transactions, providing trade finance solutions, foreign exchange services, and advisory support to businesses engaged in global trade.

Technological Advancements: Rapid advancements in technology have transformed the commercial banking landscape. Digitalization, automation, and the emergence of fintech companies have disrupted traditional banking models, enabling banks to provide innovative services such as mobile banking, online payments, and personalized financial solutions.

Regulatory Environment: Commercial banks operate within a complex regulatory framework aimed at maintaining financial stability, consumer protection, and preventing money laundering and fraud. Stricter regulations, including capital adequacy requirements and enhanced risk management practices, have compelled banks to adapt their business models and invest in compliance measures.

Evolving Customer Expectations: Customers’ expectations and preferences have evolved in the digital age. They demand convenience, personalized experiences, and seamless integration of banking services into their daily lives. Commercial banks need to embrace customer-centric approaches and leverage technology to meet these changing demands effectively.

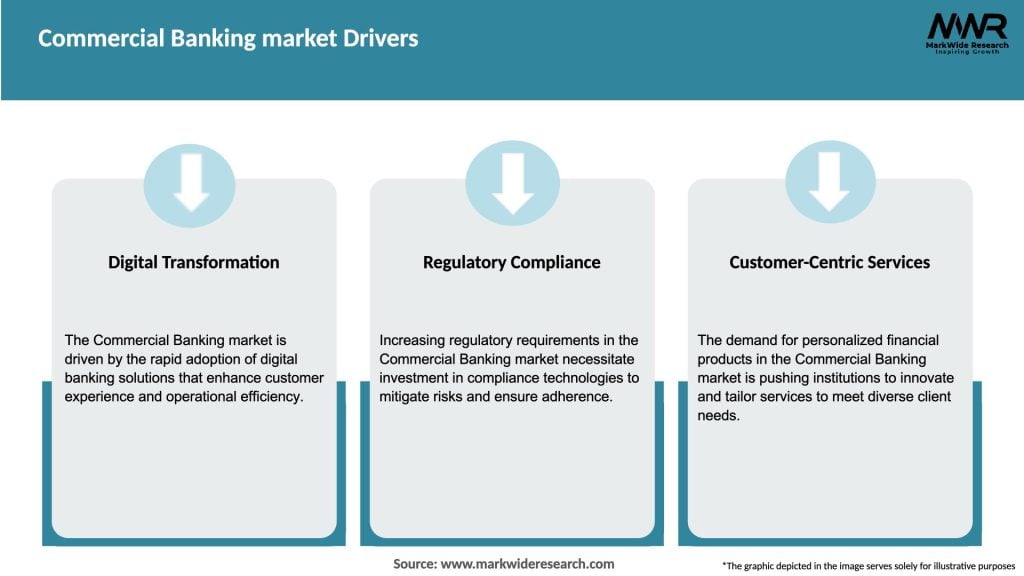

Market Drivers

Economic Growth and Business Expansion: As economies grow and businesses expand, the demand for banking services increases. Commercial banks play a critical role in providing businesses with capital for investment, financing working capital requirements, and supporting entrepreneurial ventures, thereby driving market growth.

Increasing Financial Inclusion: Governments and regulatory bodies worldwide are promoting financial inclusion, aiming to provide banking services to underserved populations. Commercial banks are actively expanding their reach and developing innovative solutions to cater to the unbanked and underbanked segments, fostering market growth.

Technological Advancements: Technological innovations, such as artificial intelligence, blockchain, and data analytics, have enabled commercial banks to enhance operational efficiency, streamline processes, and deliver superior customer experiences. Embracing digital transformation is crucial for banks to remain competitive and meet evolving customer expectations.

Mergers and Acquisitions: Consolidation within the commercial banking sector has been a significant driver of market growth. Mergers and acquisitions enable banks to expand their geographical presence, diversify their service offerings, and achieve economies of scale, leading to enhanced competitiveness and market dominance.

Market Restraints

Regulatory Compliance Challenges: The regulatory landscape for commercial banks is becoming increasingly complex. Adhering to stringent regulations and compliance requirements can be costly and time-consuming, posing challenges for banks, particularly smaller institutions with limited resources.

Cybersecurity Risks: With the increasing reliance on technology and digitization, commercial banks face heightened cybersecurity risks. Cyberattacks, data breaches, and identity theft pose significant threats to the integrity and trustworthiness of banks, requiring robust security measures and continuous investment in cybersecurity infrastructure.

Economic Volatility: Commercial banks are vulnerable to economic fluctuations and financial crises. A slowdown in economic growth, recessionary periods, or unstable financial markets can adversely affect the banking sector, leading to reduced lending, increased credit risk, and decreased profitability.

Fierce Competition: The commercial banking market is highly competitive, with both traditional banks and emerging fintech players vying for market share. Established banks face the challenge of maintaining customer loyalty and retaining market dominance in the face of innovative disruptions and evolving customer preferences.

Market Opportunities

Emerging Markets: The commercial banking sector in emerging markets presents significant growth opportunities due to increasing financial literacy, rising middle-class populations, and economic development. Banks can capitalize on these opportunities by expanding their presence, offering tailored solutions, and leveraging technological advancements to reach untapped customer segments.

Fintech Collaboration: Collaboration between commercial banks and fintech companies can lead to mutually beneficial partnerships. By harnessing the innovative capabilities of fintech firms, banks can enhance their service offerings, improve customer experiences, and drive operational efficiencies.

Sustainable Finance: The growing emphasis on sustainability and environmental responsibility opens up avenues for commercial banks to offer sustainable finance solutions. Investing in renewable energy projects, promoting green lending, and integrating Environmental, Social, and Governance (ESG) principles into their operations can attract environmentally conscious customers and drive market growth.

Digital Transformation: The ongoing digital transformation presents numerous opportunities for commercial banks to improve operational efficiency, streamline processes, and deliver personalized services. Embracing advanced technologies, such as artificial intelligence, machine learning, and robotic process automation, can enable banks to offer innovative solutions and gain a competitive edge.

Market Dynamics

The commercial banking market is dynamic and influenced by various factors, including economic conditions, technological advancements, regulatory changes, and customer behavior. Understanding the market dynamics is essential for banks and industry participants to adapt to changing trends and seize growth opportunities. Key market dynamics include:

Changing Customer Preferences: Customers increasingly prefer digital banking solutions and personalized experiences. Banks need to adapt their service delivery models, invest in digital channels, and utilize data analytics to gain insights into customer behavior and preferences.

Regulatory Environment: The regulatory landscape continues to evolve, impacting banks’ operations, risk management practices, and compliance requirements. Banks need to stay abreast of regulatory changes and proactively adopt measures to ensure compliance while delivering seamless customer experiences.

Technological Advancements: Technology plays a pivotal role in shaping the commercial banking landscape. Banks must embrace emerging technologies, such as artificial intelligence, blockchain, and cloud computing, to enhance operational efficiency, improve risk management, and provide innovative services.

Industry Consolidation: Mergers and acquisitions remain prevalent in the commercial banking sector as banks seek to achieve economies of scale, expand their geographic presence, and enhance service offerings. Industry consolidation reshapes the competitive landscape and presents opportunities for banks to strengthen their market positions.

Regional Analysis

The commercial banking market exhibits regional variations influenced by economic, cultural, and regulatory factors. A regional analysis provides insights into market trends, growth rates, competitive landscapes, and opportunities specific to different geographical regions. The following regions are key players in the global commercial banking market:

North America: The commercial banking sector in North America is well-established, characterized by large national and regional banks. The region’s mature economy, technological advancements, and regulatory environment contribute to its market dominance.

Europe: Europe has a diverse commercial banking landscape, comprising multinational banks, regional banks, and cooperative banks. The region’s regulatory framework, including the Basel III standards, shapes banking operations and risk management practices.

Asia Pacific: The Asia Pacific region is witnessing rapid economic growth and urbanization, driving the demand for commercial banking services. The market is highly competitive, with both domestic and international banks vying for market share.

Latin America: The commercial banking market in Latin America is experiencing growth, driven by increasing financial inclusion initiatives, economic reforms, and infrastructure development. Regional banks and foreign players compete for market share in this dynamic environment.

Middle East and Africa: The Middle East and Africa present unique opportunities and challenges for commercial banks. The region’s diverse economies, oil-dependent economies, and emerging markets offer potential for growth, while geopolitical factors and regulatory frameworks influence market dynamics.

Competitive Landscape

Leading Companies in the Commercial Banking Market:

JPMorgan Chase & Co.

Bank of America Corporation

Industrial and Commercial Bank of China Limited (ICBC)

Wells Fargo & Company

Citigroup Inc.

HSBC Holdings plc

Agricultural Bank of China Limited

Bank of China Limited

Mitsubishi UFJ Financial Group, Inc.

BNP Paribas

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

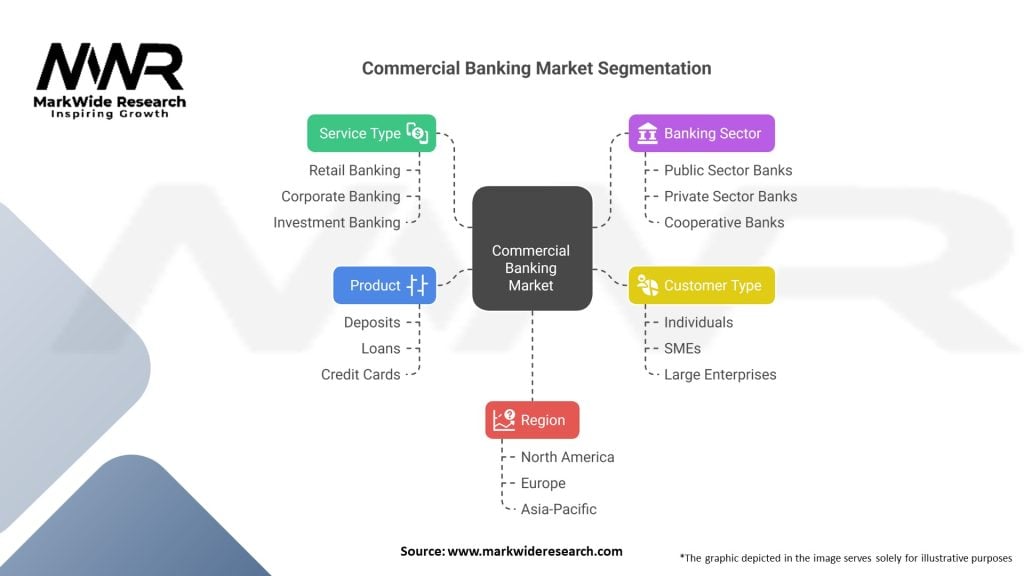

Segmentation

The commercial banking market can be segmented based on various criteria, including banking services, customer segments, and geographical regions. The following segmentation provides a comprehensive understanding of the market landscape:

By Banking Services: a. Deposits and Savings Accounts b. Loans and Credit Facilities c. Trade Finance and International Banking d. Treasury and Cash Management Services e. Investment Banking and Capital Markets f. Wealth Management and Private Banking

By Customer Segments: a. Small and Medium Enterprises (SMEs) b. Corporate and Commercial Clients c. Retail Customers d. Government and Public Sector

By Geographical Regions: a. North America b. Europe c. Asia Pacific d. Latin America e. Middle East and Africa

Category-wise Insights

Deposits and Savings Accounts:

Deposits and savings accounts are essential banking services that provide customers with a secure place to hold their funds and earn interest.

Banks offer a range of deposit products, including current accounts, savings accounts, fixed deposits, and certificates of deposit.

Deposits and savings accounts serve as a stable funding source for banks, allowing them to lend to businesses and individuals.

Loans and Credit Facilities:

Commercial banks play a crucial role in providing loans and credit facilities to businesses and individuals, supporting economic growth and development.

Banks offer various types of loans, including business loans, mortgages, personal loans, and credit cards.

Loan underwriting, risk assessment, and interest rate determination are critical aspects of the lending process.

Trade Finance and International Banking:

Commercial banks facilitate international trade transactions through trade finance services.

Services include letters of credit, documentary collections, trade guarantees, export financing, and foreign exchange services.

Trade finance enables businesses to mitigate risks, finance imports and exports, and ensure smooth cross-border transactions.

Treasury and Cash Management Services:

Treasury and cash management services help businesses efficiently manage their liquidity, cash flow, and financial risks.

Services include cash pooling, payment and collection services, liquidity management, foreign exchange risk management, and interest rate hedging.

Banks leverage technology and digital solutions to provide real-time cash visibility, streamline payment processes, and enhance treasury operations.

Investment Banking and Capital Markets:

Investment banking services involve assisting corporations, governments, and institutional clients in raising capital, mergers and acquisitions, and securities trading.

Services include underwriting securities, initial public offerings (IPOs), debt and equity financing, financial advisory, and asset management.

Investment banks play a vital role in capital market activities, supporting the efficient allocation of capital and facilitating corporate growth.

Wealth Management and Private Banking:

Wealth management and private banking cater to high-net-worth individuals and families, providing tailored financial solutions and personalized services.

Services include investment advisory, portfolio management, estate planning, tax optimization, philanthropy, and family office services.

Private banks offer exclusive services, personalized relationship management, and access to a range of investment opportunities and specialized products.

Key Benefits for Industry Participants and Stakeholders

The commercial banking market offers several key benefits for industry participants and stakeholders:

Revenue Generation: Commercial banks generate revenue through various avenues, including interest income from loans and credit facilities, fees from banking services, investment banking activities, and wealth management services.

Market Expansion: Banks have the opportunity to expand their market presence by reaching untapped customer segments, expanding into new geographical regions, and diversifying their service offerings.

Customer Relationships: Commercial banks build long-term relationships with their customers, becoming trusted financial partners. Strong customer relationships lead to customer loyalty, increased cross-selling opportunities, and enhanced brand reputation.

Financial Intermediation: Banks play a critical role in mobilizing savings and channeling them towards productive investments. By providing loans and credit facilities, they facilitate economic growth and development.

Risk Management: Commercial banks offer risk management services, such as hedging, insurance, and derivatives, to help clients mitigate financial risks and uncertainties.

Job Creation: The commercial banking sector contributes to job creation by employing a wide range of professionals, including bankers, financial advisors, risk managers, IT specialists, and customer service representatives.

SWOT Analysis

A SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis provides a comprehensive assessment of the commercial banking market:

Strengths:

Established infrastructure and distribution networks

Regulatory framework ensuring stability and consumer protection

Extensive product and service offerings catering to diverse customer needs

Strong customer relationships and brand reputation

Weaknesses:

Dependency on economic conditions and interest rate fluctuations

Regulatory compliance challenges and associated costs

Legacy systems and resistance to digital transformation

Customer perception of banks as bureaucratic and slow to innovate

Opportunities:

Emerging markets with untapped customer segments

Technological advancements enabling digital transformation and innovation

Collaboration with fintech companies to enhance service offerings

Sustainable finance and ESG-focused opportunities

Threats:

Increased competition from fintech disruptors and non-bank financial institutions

Cybersecurity threats and data breaches

Economic downturns impacting credit quality and profitability

Stringent regulatory requirements and compliance risks

Market Key Trends

Digital Transformation: The commercial banking sector is witnessing a rapid digital transformation, driven by technological advancements and changing customer expectations. Banks are investing in digital channels, mobile banking apps, AI-powered chatbots, and personalized digital experiences to meet customer demands for convenience and accessibility.

Open Banking and APIs: Open banking initiatives are reshaping the commercial banking landscape, allowing customers to share their financial data securely with third-party providers. Application Programming Interfaces (APIs) enable seamless integration of banking services with third-party platforms and facilitate the development of innovative banking solutions.

Data Analytics and AI: Banks are leveraging data analytics and artificial intelligence to gain insights into customer behavior, enhance risk management practices, and improve operational efficiency. Predictive analytics and machine learning algorithms help banks make data-driven decisions and deliver personalized services to customers.

Focus on Customer Experience: Customer experience has become a top priority for commercial banks. Banks are adopting customer-centric strategies, leveraging technology to provide seamless, personalized experiences, and investing in customer relationship management tools to enhance customer satisfaction and loyalty.

Sustainable Finance and ESG Integration: There is an increasing focus on sustainable finance and the integration of Environmental, Social, and Governance (ESG) principles into banking operations. Banks are offering green financing, investing in renewable energy projects, and aligning their business practices with sustainability goals.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the commercial banking market:

Economic Disruption: The pandemic led to a global economic downturn, impacting businesses and individuals’ financial stability. Commercial banks faced challenges in managing loan defaults, credit risks, and reduced profitability due to lower economic activity.

Acceleration of Digital Transformation: The pandemic accelerated the adoption of digital banking services as customers shifted to online and mobile banking due to lockdowns and social distancing measures. Banks had to rapidly enhance their digital capabilities to meet the increased demand for remote banking services.

Regulatory Measures: Governments and regulatory authorities introduced measures to mitigate the impact of the pandemic on the banking sector. These included loan moratoriums, regulatory relief measures, and capital adequacy requirements adjustments to ensure financial stability.

Increased Focus on Risk Management: The pandemic highlighted the importance of robust risk management practices for banks. Banks strengthened their risk management frameworks, increased provisions for potential loan losses, and adopted stress testing models to assess their resilience to future crises.

Market Consolidation: The pandemic accelerated the trend of market consolidation, with larger banks acquiring smaller banks struggling due to the economic impact of the pandemic. This consolidation aimed to strengthen banks’ balance sheets, achieve economies of scale, and enhance market competitiveness.

Key Industry Developments

Rise of Neobanks: Neobanks, also known as digital banks or challenger banks, have emerged as disruptive players in the commercial banking market. These fully digital banks operate without physical branches, offering streamlined, user-friendly banking experiences to tech-savvy customers.

Integration of AI and Automation: Commercial banks are increasingly incorporating artificial intelligence and automation technologies into their operations. AI-powered chatbots handle customer inquiries, machine learning algorithms assist in credit risk assessment, and robotic process automation streamlines back-office processes.

Regulatory Compliance Focus: Regulatory compliance remains a key focus for commercial banks. Regulators are implementing stricter requirements to ensure financial stability, combat money laundering, and protect consumer interests. Banks are investing in compliance measures, including enhanced Know Your Customer (KYC) processes and anti-money laundering frameworks.

ESG Integration: Environmental, Social, and Governance (ESG) factors are gaining prominence in the commercial banking sector. Banks are aligning their strategies with sustainability goals, integrating ESG criteria into risk assessment processes, and offering green financing options to support environmentally responsible initiatives.

Collaboration with Fintech Startups: Traditional banks are increasingly collaborating with fintech startups to leverage their innovative technologies and enhance their service offerings. Partnerships focus on areas such as digital payments, lending platforms, data analytics, and cybersecurity.

Analyst Suggestions

Embrace Digital Transformation: Commercial banks should continue investing in digital transformation initiatives to meet evolving customer expectations and stay competitive. This includes enhancing online and mobile banking experiences, adopting AI and automation technologies, and leveraging data analytics for personalized services.

Strengthen Risk Management Practices: Given the increased focus on risk management, banks should prioritize enhancing their risk management frameworks, including credit risk assessment, stress testing, and operational risk management. This will ensure resilience to future economic uncertainties and regulatory changes.

Explore Sustainable Finance Opportunities: Banks should seize the opportunities presented by sustainable finance and ESG integration. This involves offering green financing options, aligning business practices with sustainability goals, and integrating ESG criteria into risk assessment and investment decision-making processes.

Foster Collaboration with Fintech Startups: Collaboration with fintech startups can drive innovation and enhance service offerings. Banks should actively seek partnerships with fintech companies to leverage their expertise, tap into emerging technologies, and deliver cutting-edge solutions to customers.

Enhance Customer Experience: Customer experience should remain a top priority for commercial banks. Banks should invest in customer-centric strategies, leverage data analytics for personalized services, and provide seamless, omnichannel experiences to meet and exceed customer expectations.

Future Outlook

The commercial banking market is poised for continued growth and transformation in the future. Key trends and factors shaping the future outlook include:

Continued Digital Transformation: The digital transformation of the commercial banking sector will persist, driven by evolving customer expectations, technological advancements, and regulatory changes. Banks will increasingly leverage data analytics, AI, and automation to provide seamless, personalized experiences.

Regulatory Compliance Focus: Regulatory requirements will continue to evolve, necessitating ongoing investments in compliance measures. Banks must stay updated with regulatory changes and adapt their operations and risk management practices accordingly.

Sustainable Finance and ESG Integration: The focus on sustainable finance and ESG integration will intensify. Banks will play a crucial role in financing green initiatives, supporting renewable energy projects, and aligning their business practices with sustainability goals.

Increased Collaboration: Collaboration between traditional banks and fintech startups will increase, leading to innovative solutions, enhanced service offerings, and improved customer experiences. Banks will explore partnerships and investments in fintech companies to foster innovation and remain competitive.

Emphasis on Cybersecurity: With the increasing reliance on technology and digital channels, cybersecurity will remain a top priority. Banks will continue to invest in robust cybersecurity infrastructure and practices to protect customer data and maintain trust.

Conclusion

The commercial banking market is undergoing significant changes driven by technological advancements, evolving customer expectations, regulatory requirements, and economic conditions. While challenges such as regulatory compliance and cybersecurity risks persist, numerous opportunities exist, including digital transformation, sustainable finance, and collaboration with fintech startups. To thrive in the competitive landscape, commercial banks should prioritize customer experience, strengthen risk management practices, embrace digital innovation, and adapt to evolving market trends. By doing so, banks can position themselves for future success and continue to support economic growth and financial stability.

What is Commercial Banking?

Commercial banking refers to the services provided by banks to businesses and corporations, including loans, credit, treasury management, and deposit accounts. These banks play a crucial role in the economy by facilitating financial transactions and providing essential funding to various sectors.

What are the key players in the Commercial Banking market?

Key players in the Commercial Banking market include JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo, among others. These institutions offer a wide range of financial services tailored to meet the needs of businesses and corporate clients.

What are the main drivers of growth in the Commercial Banking market?

The main drivers of growth in the Commercial Banking market include increasing demand for business loans, the expansion of small and medium-sized enterprises, and advancements in digital banking technologies. Additionally, economic growth and rising consumer spending contribute to the demand for commercial banking services.

What challenges does the Commercial Banking market face?

The Commercial Banking market faces challenges such as regulatory compliance, cybersecurity threats, and competition from fintech companies. These factors can impact profitability and operational efficiency for traditional banks.

What opportunities exist in the Commercial Banking market?

Opportunities in the Commercial Banking market include the adoption of innovative financial technologies, expansion into emerging markets, and the development of tailored financial products for niche sectors. These trends can enhance customer engagement and drive growth.

What trends are shaping the future of the Commercial Banking market?

Trends shaping the future of the Commercial Banking market include the rise of digital banking, increased focus on sustainability and ESG practices, and the integration of artificial intelligence in customer service. These trends are transforming how banks operate and interact with clients.

Leading Companies in the Commercial Banking Market:

JPMorgan Chase & Co.

Bank of America Corporation

Industrial and Commercial Bank of China Limited (ICBC)

Wells Fargo & Company

Citigroup Inc.

HSBC Holdings plc

Agricultural Bank of China Limited

Bank of China Limited

Mitsubishi UFJ Financial Group, Inc.

BNP Paribas

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.