444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The China video surveillance market represents one of the most dynamic and rapidly evolving security technology sectors in the global landscape. China’s surveillance infrastructure has experienced unprecedented expansion, driven by urbanization, smart city initiatives, and enhanced security requirements across multiple sectors. The market encompasses a comprehensive range of technologies including IP cameras, analog surveillance systems, video analytics software, and cloud-based monitoring solutions.

Market growth in China’s video surveillance sector has been remarkable, with the industry experiencing a robust CAGR of 12.5% over recent years. This expansion reflects the country’s commitment to developing comprehensive security infrastructure while embracing cutting-edge technologies such as artificial intelligence, facial recognition, and behavioral analytics. The integration of these advanced technologies has positioned China as a global leader in surveillance innovation.

Government initiatives have played a crucial role in market development, with substantial investments in public safety infrastructure and smart city projects. The Safe City program and various municipal security enhancement projects have created significant demand for sophisticated video surveillance solutions. Additionally, private sector adoption has accelerated as businesses recognize the value of comprehensive security monitoring systems.

The China video surveillance market refers to the comprehensive ecosystem of security monitoring technologies, systems, and services deployed across the People’s Republic of China for public safety, commercial security, and residential protection purposes. This market encompasses the design, manufacturing, installation, and maintenance of various surveillance technologies including closed-circuit television systems, network cameras, video management software, and intelligent analytics platforms.

Video surveillance systems in China integrate multiple components including capture devices, transmission infrastructure, storage solutions, and display technologies. The market includes both traditional analog systems and modern digital solutions, with increasing emphasis on IP-based networks and cloud-enabled platforms. These systems serve diverse applications ranging from traffic monitoring and crime prevention to business security and residential safety.

Modern surveillance solutions in China incorporate advanced features such as real-time video analytics, automated threat detection, and intelligent behavioral analysis. The integration of artificial intelligence and machine learning capabilities has transformed traditional monitoring into proactive security management, enabling predictive analysis and automated response mechanisms.

China’s video surveillance market stands as a testament to the country’s technological advancement and security infrastructure development. The market has evolved from basic monitoring systems to sophisticated AI-powered surveillance networks that integrate seamlessly with smart city initiatives and public safety programs. This transformation has been supported by significant government investment and rapid technological innovation.

Key market characteristics include the dominance of domestic manufacturers, widespread adoption of IP-based systems, and increasing integration of artificial intelligence capabilities. The market benefits from strong government support, with public sector projects accounting for approximately 60% of total demand. Private sector adoption continues to grow, driven by enhanced security awareness and regulatory compliance requirements.

Technological advancement remains a primary market driver, with companies investing heavily in research and development to create next-generation surveillance solutions. The integration of 5G connectivity, edge computing, and cloud-based analytics has opened new possibilities for comprehensive security monitoring. These innovations have positioned Chinese manufacturers as global leaders in surveillance technology development.

Market segmentation reveals diverse applications across transportation, retail, banking, education, and residential sectors. Each segment presents unique requirements and growth opportunities, contributing to the overall market expansion and technological diversification.

Strategic market insights reveal several critical trends shaping China’s video surveillance landscape. The following key observations highlight the market’s current state and future trajectory:

Primary market drivers for China’s video surveillance sector stem from multiple interconnected factors that create sustained demand for advanced security solutions. Urbanization trends continue to accelerate, with millions of people migrating to cities annually, creating increased security challenges and infrastructure requirements.

Government initiatives represent the most significant driver, with comprehensive smart city programs requiring extensive surveillance infrastructure. The Digital China strategy emphasizes the integration of advanced technologies into urban management, creating substantial opportunities for surveillance system deployment. Public safety investments have increased consistently, with local governments prioritizing security infrastructure development.

Technological advancement serves as both a driver and enabler of market growth. The development of AI-powered analytics, facial recognition technology, and behavioral analysis systems has expanded the value proposition of video surveillance beyond basic monitoring. These capabilities enable proactive security management and operational intelligence gathering.

Private sector adoption has accelerated due to increased security awareness and regulatory compliance requirements. Businesses across various industries recognize the importance of comprehensive security monitoring for asset protection, employee safety, and operational efficiency. The retail sector, in particular, has embraced advanced surveillance for both security and customer analytics purposes.

Infrastructure development projects, including transportation networks, commercial complexes, and residential developments, consistently require integrated surveillance solutions. The scale of construction activity in China creates continuous demand for new surveillance system installations.

Market restraints in China’s video surveillance sector present challenges that companies must navigate while pursuing growth opportunities. Privacy concerns have become increasingly prominent as surveillance technology becomes more sophisticated and pervasive. Public awareness of data collection and monitoring practices has led to calls for enhanced privacy protections and regulatory oversight.

Regulatory complexity poses ongoing challenges for market participants, particularly as government policies evolve to address privacy, data security, and technology standards. Companies must invest significant resources in compliance management and regulatory monitoring to ensure their products and services meet changing requirements.

Technology obsolescence represents a significant concern as rapid innovation cycles require continuous investment in research and development. Companies face pressure to regularly update their product offerings while managing the costs associated with maintaining multiple technology platforms and supporting legacy systems.

Market saturation in certain segments, particularly traditional analog surveillance systems, has intensified competition and compressed profit margins. Companies must differentiate their offerings through advanced features and superior service capabilities to maintain competitive positions.

Cybersecurity vulnerabilities in connected surveillance systems create potential risks that could undermine market confidence. As systems become more networked and cloud-enabled, ensuring robust security measures becomes increasingly critical and costly.

Emerging opportunities in China’s video surveillance market reflect the convergence of technological innovation, evolving security requirements, and expanding application areas. Artificial intelligence integration presents substantial growth potential as organizations seek more intelligent and automated security solutions. The development of edge computing capabilities enables real-time processing and reduces bandwidth requirements, creating new deployment possibilities.

Smart city expansion continues to generate significant opportunities as municipal governments invest in comprehensive urban management systems. These projects require integrated surveillance solutions that can support multiple applications including traffic management, public safety, and environmental monitoring. The scale and scope of these initiatives create substantial market potential for innovative companies.

Industry 4.0 adoption in manufacturing and logistics sectors presents opportunities for specialized surveillance solutions that support operational efficiency and safety compliance. Industrial surveillance systems can provide valuable insights into production processes while ensuring worker safety and asset protection.

Export market development offers Chinese surveillance manufacturers opportunities to leverage their technological expertise and cost advantages in international markets. The Belt and Road Initiative has created pathways for Chinese companies to participate in infrastructure projects across multiple countries.

Cloud-based services represent a growing opportunity as organizations seek scalable and cost-effective surveillance solutions. The development of surveillance-as-a-service models can provide recurring revenue streams while reducing customer capital expenditure requirements.

Market dynamics in China’s video surveillance sector reflect the complex interplay between technological innovation, regulatory evolution, and competitive pressures. Supply chain integration has become increasingly important as companies seek to control costs and ensure product quality. Many leading manufacturers have developed comprehensive supply chains that span from component production to system integration.

Competitive intensity has increased significantly as both domestic and international companies compete for market share. Chinese manufacturers have achieved technological parity with international competitors while maintaining cost advantages, leading to intense price competition in certain market segments. This dynamic has accelerated innovation as companies seek differentiation through advanced features and superior performance.

Customer expectations continue to evolve, with increasing demands for integrated solutions that combine surveillance with other security and operational systems. The trend toward platform-based approaches requires companies to develop comprehensive ecosystems rather than standalone products. This shift has implications for product development strategies and partnership arrangements.

Technology convergence is reshaping market boundaries as surveillance systems integrate with access control, alarm systems, and building management platforms. This convergence creates opportunities for companies that can provide comprehensive solutions while challenging those focused on single-product categories.

Investment patterns show increasing focus on research and development, with leading companies allocating approximately 15% of revenue to innovation activities. This investment emphasis reflects the importance of technological leadership in maintaining competitive positions.

Research methodology for analyzing China’s video surveillance market employs a comprehensive approach that combines quantitative analysis with qualitative insights from industry experts and market participants. Primary research involves extensive interviews with manufacturers, system integrators, end users, and government officials to understand market trends, challenges, and opportunities.

Data collection encompasses multiple sources including industry associations, government publications, company financial reports, and trade statistics. This multi-source approach ensures comprehensive coverage of market dynamics and validates findings through cross-referencing. Market sizing utilizes bottom-up analysis based on installation data, pricing information, and adoption rates across different sectors.

Analytical frameworks include competitive analysis, technology assessment, and regulatory impact evaluation. MarkWide Research employs proprietary models to assess market dynamics and forecast future trends based on historical patterns and emerging factors. The methodology incorporates scenario analysis to account for potential market disruptions and policy changes.

Quality assurance measures include peer review processes, data validation procedures, and expert panel discussions to ensure accuracy and reliability of findings. The research process maintains objectivity through structured methodologies and transparent analytical approaches.

Regional analysis of China’s video surveillance market reveals significant variations in adoption patterns, technology preferences, and growth rates across different geographic areas. Eastern China dominates market activity, accounting for approximately 45% of total market share, driven by high urbanization levels, economic development, and government investment in smart city initiatives.

Tier-1 cities including Beijing, Shanghai, Guangzhou, and Shenzhen represent the most mature markets with sophisticated surveillance infrastructure and high adoption of advanced technologies. These cities serve as testing grounds for innovative solutions and drive technology development through demanding requirements and substantial budgets.

Central China represents a growing market opportunity with approximately 25% market share, as regional governments invest in security infrastructure and economic development projects. Cities like Wuhan, Changsha, and Zhengzhou are implementing comprehensive surveillance systems as part of urban modernization efforts.

Western China shows strong growth potential despite currently representing a smaller market share of approximately 20%. Government initiatives to develop western regions include substantial infrastructure investments that incorporate modern surveillance technologies. The unique geographic and security challenges in western regions create demand for specialized surveillance solutions.

Northeastern China faces economic transition challenges but maintains steady demand for surveillance systems, particularly in industrial and transportation applications. The region’s focus on industrial modernization creates opportunities for specialized surveillance solutions that support manufacturing and logistics operations.

Competitive landscape analysis reveals a dynamic market structure with strong domestic players competing alongside international companies. The market has evolved significantly over the past decade, with Chinese manufacturers achieving technological leadership in many product categories.

Market consolidation trends show increasing concentration among leading players, with top companies expanding through acquisitions and strategic partnerships. The competitive dynamics emphasize innovation, cost efficiency, and comprehensive solution capabilities.

Market segmentation analysis provides detailed insights into the diverse components and applications within China’s video surveillance market. Technology-based segmentation reveals the transition from analog to digital systems, with IP-based solutions gaining dominant market position.

By Technology:

By Component:

By Application:

Category-wise analysis reveals distinct characteristics and growth patterns across different surveillance system categories. IP camera systems represent the fastest-growing category, driven by superior image quality, network integration capabilities, and advanced analytics features. This category benefits from continuous technological advancement and decreasing component costs.

AI-enabled surveillance systems constitute an emerging high-growth category with significant potential for market expansion. These systems incorporate machine learning algorithms, facial recognition technology, and behavioral analytics to provide intelligent monitoring capabilities. Adoption rates in this category are accelerating as organizations recognize the value of automated threat detection and operational insights.

Cloud-based surveillance solutions represent a transformative category that is reshaping traditional deployment models. These solutions offer scalability advantages, reduced infrastructure requirements, and enhanced accessibility for remote monitoring. The category appeals particularly to small and medium-sized businesses seeking cost-effective surveillance solutions.

Mobile surveillance systems address specific market needs for temporary or portable monitoring applications. This category includes vehicle-mounted systems, portable cameras, and body-worn devices that provide flexibility for law enforcement and security operations.

Thermal imaging systems represent a specialized category with applications in perimeter security, industrial monitoring, and public safety. While representing a smaller market segment, thermal surveillance systems command premium pricing and serve critical security applications.

Industry participants in China’s video surveillance market enjoy numerous benefits from the sector’s dynamic growth and technological advancement. Manufacturers benefit from substantial market opportunities driven by government investment, urbanization trends, and increasing security awareness. The large domestic market provides a foundation for achieving economies of scale and supporting international expansion efforts.

Technology developers find significant opportunities for innovation and commercialization in the rapidly evolving surveillance landscape. The integration of artificial intelligence, cloud computing, and mobile technologies creates multiple avenues for product development and differentiation. Research and development investments yield competitive advantages in this technology-driven market.

System integrators benefit from growing demand for comprehensive security solutions that combine multiple technologies and applications. The trend toward integrated platforms creates opportunities for companies that can design, implement, and maintain complex surveillance systems. Professional services represent a growing revenue stream with recurring income potential.

End users across various sectors gain enhanced security capabilities, operational insights, and cost efficiencies through advanced surveillance systems. Government agencies improve public safety and urban management capabilities, while businesses enhance asset protection and operational intelligence. The evolution toward intelligent systems provides value beyond traditional security monitoring.

Investors find attractive opportunities in a market characterized by strong growth fundamentals, technological innovation, and expanding applications. The sector’s resilience and essential nature provide stability, while emerging technologies offer growth potential.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key market trends shaping China’s video surveillance landscape reflect the convergence of technological advancement, evolving security requirements, and changing user expectations. Artificial intelligence integration has emerged as the most significant trend, with AI-powered analytics becoming standard features in modern surveillance systems. This trend enables proactive security management and transforms surveillance from reactive monitoring to predictive intelligence.

Cloud migration represents another major trend as organizations seek scalable and cost-effective surveillance solutions. Cloud-based platforms offer enhanced accessibility, reduced infrastructure requirements, and improved collaboration capabilities. This trend is particularly pronounced among small and medium-sized businesses seeking enterprise-grade surveillance capabilities without substantial capital investment.

Mobile integration continues to gain momentum as users demand remote access and real-time monitoring capabilities. Mobile applications and responsive web interfaces enable security personnel to monitor systems from any location, improving response times and operational efficiency. The trend toward mobile-first design influences product development and user interface design.

Edge computing adoption is accelerating as organizations seek to reduce bandwidth requirements and improve system responsiveness. Edge-based analytics enable real-time processing and decision-making while reducing dependence on centralized computing resources. This trend supports the deployment of intelligent surveillance in bandwidth-constrained environments.

Privacy-by-design approaches are becoming increasingly important as organizations address growing privacy concerns. Data protection features, anonymization capabilities, and consent management tools are being integrated into surveillance systems to ensure compliance with evolving regulations.

Recent industry developments highlight the dynamic nature of China’s video surveillance market and the continuous evolution of technology and business models. Strategic partnerships between surveillance manufacturers and technology companies have accelerated the integration of advanced capabilities such as artificial intelligence and cloud computing.

Product innovations continue to drive market evolution, with companies introducing 4K and 8K resolution cameras, advanced night vision capabilities, and multi-sensor platforms that combine video, thermal, and audio monitoring. These innovations address growing demands for higher image quality and comprehensive situational awareness.

Acquisition activities have reshaped the competitive landscape as companies seek to expand their technology portfolios and market reach. Vertical integration strategies have led to companies acquiring component suppliers and software developers to control entire value chains and improve cost competitiveness.

International expansion efforts by Chinese surveillance manufacturers have intensified, with companies establishing regional offices, manufacturing facilities, and partnership networks in key global markets. These developments reflect the maturation of Chinese companies and their ambitions for global leadership.

Regulatory developments including data protection laws and cybersecurity requirements have influenced product development and deployment strategies. Companies are investing in compliance capabilities and security features to address evolving regulatory requirements.

Analyst recommendations for stakeholders in China’s video surveillance market emphasize the importance of strategic positioning and technological innovation. MarkWide Research analysis suggests that companies should prioritize artificial intelligence integration and cloud-based service development to capitalize on emerging market opportunities.

Investment priorities should focus on research and development capabilities, particularly in areas such as machine learning algorithms, edge computing platforms, and cybersecurity technologies. Companies that establish technological leadership in these areas are likely to achieve sustainable competitive advantages and premium market positioning.

Market expansion strategies should consider both domestic and international opportunities, with particular attention to emerging applications in smart cities, industrial automation, and retail analytics. Diversification across multiple application areas can reduce market risk and provide multiple growth vectors.

Partnership development represents a critical success factor, particularly for companies seeking to integrate complementary technologies or access new market segments. Strategic alliances with technology providers, system integrators, and channel partners can accelerate market penetration and capability development.

Regulatory compliance should be treated as a strategic priority rather than a compliance burden. Companies that proactively address privacy and security requirements can differentiate their offerings and build trust with customers and regulators.

Future outlook for China’s video surveillance market indicates continued strong growth driven by technological advancement, expanding applications, and sustained investment in security infrastructure. Market evolution will be characterized by increasing intelligence, connectivity, and integration with broader smart city and IoT ecosystems.

Technology trends suggest that artificial intelligence will become ubiquitous in surveillance systems, with advanced analytics capabilities becoming standard features rather than premium options. The integration of 5G connectivity will enable new applications and deployment models, particularly for mobile and temporary surveillance requirements.

Application expansion will continue beyond traditional security monitoring into areas such as business intelligence, operational optimization, and customer analytics. This evolution will create new market segments and revenue opportunities while expanding the total addressable market for surveillance technologies.

Market structure is expected to evolve toward greater consolidation among leading players, with successful companies achieving scale advantages and technological leadership. The competitive landscape will likely feature fewer but stronger companies with comprehensive solution portfolios and global market presence.

Growth projections indicate that the market will maintain robust expansion with a projected CAGR of 11.8% over the next five years. This growth will be supported by continued urbanization, smart city development, and the ongoing digital transformation of security infrastructure across multiple sectors.

China’s video surveillance market represents one of the most dynamic and innovative sectors in the global security technology landscape. The market has evolved from basic monitoring systems to sophisticated AI-powered platforms that provide comprehensive security intelligence and operational insights. This transformation reflects China’s commitment to technological leadership and infrastructure modernization.

Market fundamentals remain strong, supported by government investment, urbanization trends, and increasing security awareness across all sectors. The integration of advanced technologies such as artificial intelligence, cloud computing, and mobile connectivity has expanded the value proposition of surveillance systems beyond traditional security applications.

Competitive dynamics favor companies that can combine technological innovation with cost efficiency and comprehensive solution capabilities. Chinese manufacturers have achieved global leadership positions while continuing to invest in research and development to maintain their competitive advantages.

Future prospects indicate continued market expansion driven by smart city initiatives, emerging applications, and technological advancement. The China video surveillance market is well-positioned to maintain its growth trajectory while contributing to global security technology development and innovation.

What is Video Surveillance?

Video surveillance refers to the use of video cameras to transmit a signal to a specific place, on a limited set of monitors. It is widely used for security purposes in various sectors, including retail, transportation, and public safety.

What are the key players in the China Video Surveillance Market?

Key players in the China Video Surveillance Market include Hikvision, Dahua Technology, and Uniview, among others. These companies are known for their innovative products and extensive market reach.

What are the main drivers of the China Video Surveillance Market?

The main drivers of the China Video Surveillance Market include the increasing demand for security solutions, advancements in technology such as AI and IoT, and the growing need for surveillance in urban areas and critical infrastructure.

What challenges does the China Video Surveillance Market face?

Challenges in the China Video Surveillance Market include privacy concerns, regulatory compliance issues, and the high costs associated with advanced surveillance technologies. These factors can hinder market growth and adoption.

What opportunities exist in the China Video Surveillance Market?

Opportunities in the China Video Surveillance Market include the integration of smart technologies, the expansion of smart city initiatives, and the increasing adoption of cloud-based surveillance solutions. These trends are expected to drive future growth.

What trends are shaping the China Video Surveillance Market?

Trends shaping the China Video Surveillance Market include the rise of AI-powered analytics, the shift towards IP-based systems, and the growing emphasis on cybersecurity measures. These innovations are transforming how surveillance systems are deployed and managed.

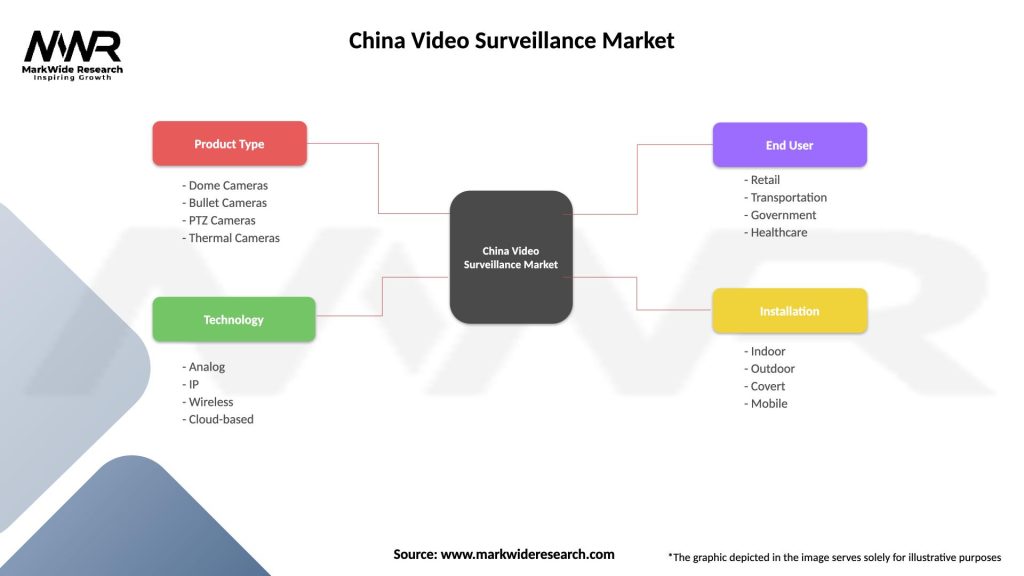

China Video Surveillance Market

| Segmentation Details | Description |

|---|---|

| Product Type | Dome Cameras, Bullet Cameras, PTZ Cameras, Thermal Cameras |

| Technology | Analog, IP, Wireless, Cloud-based |

| End User | Retail, Transportation, Government, Healthcare |

| Installation | Indoor, Outdoor, Covert, Mobile |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the China Video Surveillance Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.