444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The China plastic packaging film market represents one of the most dynamic and rapidly evolving segments within the global packaging industry. China’s position as the world’s manufacturing hub has created unprecedented demand for innovative plastic packaging solutions across diverse sectors including food and beverage, pharmaceuticals, consumer goods, and industrial applications. The market demonstrates robust growth potential driven by urbanization, changing consumer preferences, and technological advancements in film manufacturing processes.

Market dynamics in China reflect the country’s transition toward sustainable packaging solutions while maintaining cost-effectiveness and performance standards. The plastic packaging film sector encompasses various product categories including polyethylene films, polypropylene films, polyester films, and specialty barrier films. Growth projections indicate the market is expanding at a compound annual growth rate of 6.2%, supported by increasing demand from e-commerce, food delivery services, and pharmaceutical packaging applications.

Regional distribution shows significant concentration in eastern coastal provinces, with Guangdong province accounting for approximately 28% of total production capacity. The market benefits from China’s well-established petrochemical infrastructure, advanced manufacturing capabilities, and proximity to major consumer markets across Asia-Pacific region.

The China plastic packaging film market refers to the comprehensive ecosystem of manufacturing, distribution, and consumption of thin plastic materials used for packaging applications within Chinese territory. These films serve as protective barriers, preservation mediums, and branding platforms for countless products ranging from food items to industrial components.

Plastic packaging films encompass various polymer-based materials engineered to provide specific functional properties including moisture resistance, oxygen barrier capabilities, heat sealability, and printability. The market includes both commodity films for general packaging applications and specialty films designed for specific industry requirements such as pharmaceutical blister packaging, food preservation, and electronic component protection.

Market scope extends beyond traditional packaging applications to include emerging segments such as biodegradable films, smart packaging solutions with embedded sensors, and high-performance barrier films for extended shelf-life applications. The definition encompasses the entire value chain from raw material procurement through film production, conversion, and end-use applications.

China’s plastic packaging film market stands at the forefront of global packaging innovation, driven by technological advancement and evolving consumer demands. The market demonstrates exceptional resilience and adaptability, with manufacturers increasingly focusing on sustainable solutions and advanced functional properties. Key growth drivers include the rapid expansion of e-commerce platforms, increasing demand for convenient food packaging, and stringent quality requirements in pharmaceutical applications.

Market segmentation reveals diverse opportunities across multiple application areas, with food packaging representing the largest segment at approximately 45% market share. The pharmaceutical and healthcare segment shows the highest growth potential, expanding at 8.1% annually due to aging population demographics and increased healthcare spending. Technology adoption trends indicate growing preference for multi-layer films, biodegradable alternatives, and smart packaging solutions.

Competitive landscape features both international players and domestic manufacturers, with Chinese companies gaining significant market share through cost advantages and localized production capabilities. The market benefits from government support for packaging industry development and environmental sustainability initiatives promoting recyclable and biodegradable film solutions.

Strategic insights reveal several critical factors shaping the China plastic packaging film market landscape:

Primary market drivers propelling the China plastic packaging film market include fundamental economic and social trends reshaping consumer behavior and industrial requirements. Urbanization acceleration continues driving demand for packaged foods, convenience products, and consumer goods requiring protective packaging solutions.

E-commerce expansion represents a transformative force, with online retail sales growth creating unprecedented demand for shipping and protective packaging films. The sector benefits from increasing consumer preference for home delivery services and the corresponding need for durable, lightweight packaging materials that ensure product integrity during transportation.

Food industry evolution toward processed and packaged products drives substantial film demand, particularly for barrier films that extend shelf life and maintain product quality. Pharmaceutical sector growth contributes significantly through requirements for specialized packaging films meeting stringent regulatory standards for drug safety and efficacy preservation.

Manufacturing cost advantages position Chinese producers competitively in both domestic and international markets, supported by established petrochemical infrastructure and economies of scale. Government initiatives promoting packaging industry development through favorable policies and infrastructure investment further accelerate market growth.

Environmental concerns represent the most significant challenge facing the China plastic packaging film market, with increasing scrutiny over plastic waste and its environmental impact. Regulatory pressure for sustainable packaging solutions creates compliance costs and necessitates investment in alternative materials and recycling technologies.

Raw material price volatility affects production costs and profit margins, particularly for petroleum-based polymers subject to crude oil price fluctuations. Supply chain disruptions can impact production schedules and increase operational costs, especially for manufacturers dependent on imported raw materials or specialized additives.

Quality control challenges emerge as manufacturers balance cost reduction with performance requirements, particularly in applications requiring consistent barrier properties and mechanical strength. Competition intensity from both domestic and international players pressures pricing strategies and profit margins across all market segments.

Technology transition costs associated with upgrading production equipment for advanced film manufacturing processes represent significant capital investments that may strain smaller manufacturers’ financial resources.

Sustainable packaging solutions present the most promising growth opportunity, with increasing demand for biodegradable, compostable, and recyclable films driven by environmental awareness and regulatory requirements. Innovation potential in bio-based polymers and advanced recycling technologies offers competitive advantages for early adopters.

Smart packaging integration represents an emerging opportunity through incorporation of sensors, indicators, and interactive elements that enhance product functionality and consumer engagement. Pharmaceutical packaging expansion offers high-value applications requiring specialized barrier properties and regulatory compliance.

Export market development provides growth avenues for Chinese manufacturers leveraging cost advantages and improving quality standards to compete in international markets. Premium segment growth in high-performance films for specialized applications offers improved profit margins compared to commodity products.

Digital printing compatibility creates opportunities for customized packaging solutions supporting brand differentiation and marketing initiatives. Automation integration in packaging processes drives demand for films optimized for high-speed packaging equipment and automated handling systems.

Market dynamics in China’s plastic packaging film sector reflect complex interactions between supply-side capabilities and demand-side requirements across multiple end-use industries. Production capacity expansion continues at a measured pace, with manufacturers focusing on efficiency improvements and technology upgrades rather than pure volume increases.

Demand patterns show seasonal variations particularly in food packaging applications, with peak requirements during harvest seasons and holiday periods. Price dynamics demonstrate sensitivity to raw material costs, with manufacturers implementing various strategies including long-term supply contracts and vertical integration to manage cost volatility.

Technology adoption rates vary significantly across different market segments, with high-value applications driving faster implementation of advanced manufacturing processes. Market consolidation trends indicate ongoing merger and acquisition activity as companies seek to achieve economies of scale and expand product portfolios.

Regulatory influences increasingly shape market dynamics through environmental standards, food safety requirements, and quality specifications that drive innovation and investment in compliance capabilities. Consumer behavior evolution toward sustainability and convenience continues reshaping demand patterns and product development priorities.

Comprehensive research methodology employed for analyzing the China plastic packaging film market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability. Primary research includes extensive interviews with industry executives, manufacturers, suppliers, and end-users across various market segments and geographic regions.

Secondary research encompasses analysis of government statistics, industry reports, trade publications, and company financial statements to establish market baselines and trend identification. Market sizing methodology utilizes bottom-up and top-down approaches to validate findings and ensure consistency across different analytical perspectives.

Data validation processes include cross-referencing multiple sources, expert consultations, and statistical analysis to identify and resolve discrepancies. Forecasting models incorporate historical trends, economic indicators, and industry-specific factors to project future market developments and growth trajectories.

Regional analysis methodology examines provincial-level data and local market conditions to provide granular insights into geographic variations and opportunities. Competitive intelligence gathering includes analysis of company strategies, product portfolios, and market positioning to understand competitive dynamics and strategic implications.

Regional distribution of China’s plastic packaging film market reveals significant geographic concentration in economically developed coastal provinces. Guangdong Province maintains market leadership with approximately 28% of national production capacity, benefiting from proximity to Hong Kong, established manufacturing infrastructure, and access to international markets.

Jiangsu Province represents the second-largest market with 22% market share, supported by strong petrochemical industry presence and proximity to major consumer markets in the Yangtze River Delta region. Zhejiang Province contributes significantly through specialized film production and strong export orientation, particularly in high-value applications.

Northern regions including Beijing, Tianjin, and Hebei provinces focus primarily on serving local markets and benefit from proximity to raw material sources. Western provinces show emerging growth potential driven by government development initiatives and increasing local demand from expanding manufacturing sectors.

Market characteristics vary significantly across regions, with coastal areas emphasizing export-oriented production and advanced technology adoption, while inland regions focus on cost-effective solutions for domestic markets. Infrastructure development continues supporting market expansion in previously underserved regions through improved transportation and logistics capabilities.

Competitive landscape in China’s plastic packaging film market features a diverse mix of international corporations, domestic leaders, and specialized manufacturers competing across different market segments and applications. Market structure shows moderate concentration with the top ten players accounting for approximately 35% of total market share.

Leading companies in the market include:

Competitive strategies focus on technology innovation, cost optimization, and market expansion through both organic growth and strategic acquisitions. Domestic players increasingly challenge international competitors through improved quality standards and competitive pricing strategies.

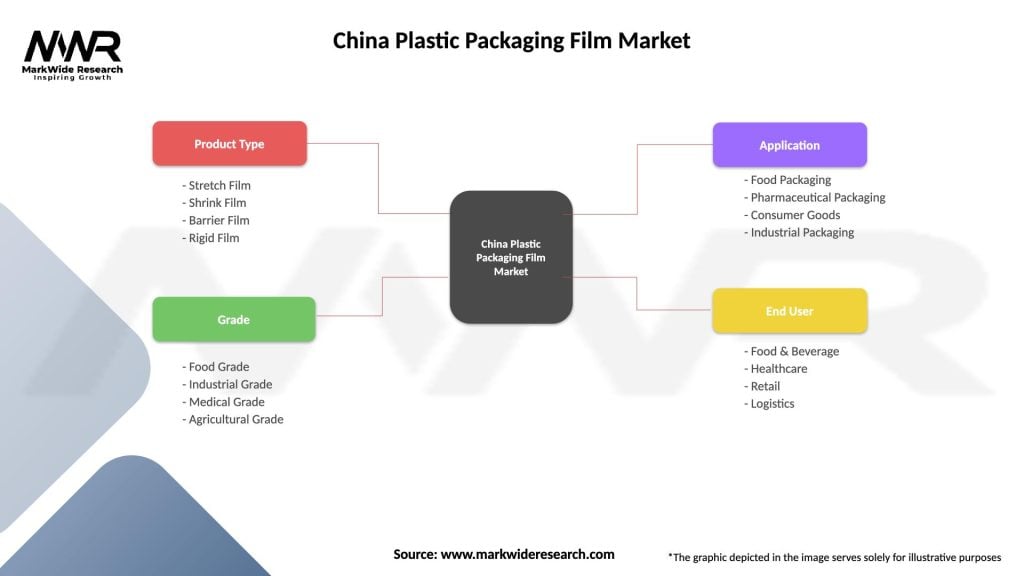

Market segmentation analysis reveals diverse opportunities across multiple dimensions including product type, application, end-use industry, and technology platform. Product-based segmentation encompasses various polymer types and film configurations designed for specific performance requirements.

By Material Type:

By Application:

By Technology:

Food packaging category dominates the China plastic packaging film market through diverse applications ranging from fresh produce packaging to processed food preservation. Barrier film demand shows particular strength in dairy products, meat packaging, and snack food applications where extended shelf life and product protection are critical requirements.

Pharmaceutical packaging represents the highest growth category, driven by China’s aging population and expanding healthcare infrastructure. Blister packaging films show exceptional demand growth at 9.3% annually due to increased pharmaceutical production and stricter packaging regulations ensuring drug safety and efficacy.

Industrial packaging applications demonstrate steady growth through electronics manufacturing, automotive components, and chemical products requiring specialized protective films. Anti-static films and moisture barrier films serve critical roles in protecting sensitive electronic components during manufacturing and transportation processes.

Consumer goods packaging benefits from premiumization trends and brand differentiation requirements driving demand for high-quality printing substrates and decorative films. Personal care packaging shows particular strength in cosmetics and hygiene products requiring attractive appearance and functional performance.

E-commerce packaging emerges as a distinct category with unique requirements for tamper-evident features, branding opportunities, and sustainable materials addressing environmental concerns while maintaining cost-effectiveness for high-volume applications.

Manufacturers benefit from China’s plastic packaging film market through access to cost-effective production capabilities, established supply chains, and proximity to major consumer markets. Economies of scale enable competitive pricing strategies while maintaining quality standards required for both domestic and export applications.

Brand owners gain advantages through diverse packaging solutions supporting product differentiation, shelf appeal, and functional performance requirements. Customization capabilities allow for tailored packaging solutions addressing specific product requirements and marketing objectives while maintaining cost-effectiveness.

Converters and processors benefit from reliable film supply, technical support, and innovation partnerships enabling development of value-added packaging solutions. Processing efficiency improvements through advanced film technologies reduce waste and increase productivity in packaging operations.

End consumers benefit from improved product protection, extended shelf life, and enhanced convenience features enabled by advanced packaging film technologies. Sustainability initiatives provide environmentally conscious consumers with recyclable and biodegradable packaging options addressing environmental concerns.

Investors find attractive opportunities in a growing market supported by fundamental demand drivers and technological innovation potential. Market diversification across multiple end-use segments provides risk mitigation and growth opportunities in various economic conditions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping China’s plastic packaging film market, with manufacturers investing heavily in biodegradable alternatives and recycling technologies. Circular economy principles drive development of films designed for recyclability and reduced environmental impact while maintaining performance standards.

Smart packaging integration gains momentum through incorporation of sensors, QR codes, and interactive elements that enhance consumer engagement and provide supply chain visibility. Digital printing compatibility enables customized packaging solutions supporting brand differentiation and marketing campaigns with shorter production runs and faster turnaround times.

Multi-layer film technology advancement continues improving barrier properties and functional performance while reducing material usage through optimized layer structures. Nanotechnology applications enhance film properties including antimicrobial characteristics, improved barrier performance, and enhanced mechanical strength.

E-commerce optimization drives development of films specifically designed for shipping and handling requirements including tamper-evident features, easy-open characteristics, and enhanced protection during transportation. Automation compatibility becomes increasingly important as packaging operations adopt high-speed automated equipment requiring films with consistent properties and reliable performance.

Regional specialization trends show different provinces developing expertise in specific film types and applications based on local industrial clusters and market requirements. MarkWide Research indicates that premium segment growth outpaces commodity products at 7.4% annually as manufacturers focus on value-added solutions.

Technology advancement initiatives continue transforming China’s plastic packaging film industry through significant investments in research and development. Major manufacturers are establishing innovation centers focused on sustainable packaging solutions and advanced barrier technologies addressing evolving market requirements.

Capacity expansion projects emphasize efficiency improvements and technology upgrades rather than pure volume increases, with companies investing in advanced extrusion equipment and quality control systems. Strategic partnerships between Chinese manufacturers and international technology providers accelerate knowledge transfer and capability development.

Regulatory developments include implementation of stricter environmental standards and food safety requirements driving industry compliance investments and technology adoption. Government support programs promote packaging industry development through favorable policies, infrastructure investment, and research funding initiatives.

Merger and acquisition activity increases as companies seek to achieve economies of scale, expand product portfolios, and enhance market positioning. International expansion by Chinese manufacturers accelerates through establishment of overseas production facilities and distribution networks.

Sustainability initiatives gain prominence with multiple companies announcing commitments to recyclable packaging solutions and carbon footprint reduction targets. Digital transformation adoption improves operational efficiency and customer service capabilities through advanced manufacturing execution systems and supply chain optimization technologies.

Strategic recommendations for market participants emphasize the critical importance of sustainability integration and technology advancement to maintain competitive positioning. Investment priorities should focus on developing biodegradable film alternatives and advanced recycling capabilities to address environmental concerns and regulatory requirements.

Market positioning strategies should emphasize value-added solutions and specialized applications rather than competing solely on price in commodity segments. Innovation investment in smart packaging technologies and multi-functional films offers opportunities for differentiation and premium pricing in growing market segments.

Geographic expansion recommendations include targeting underserved inland regions with cost-effective solutions while maintaining focus on export market development through quality improvements and certification achievements. Partnership strategies with technology providers and end-use customers can accelerate innovation and market penetration.

Operational excellence initiatives should prioritize automation adoption, quality consistency, and supply chain optimization to maintain cost competitiveness while improving service levels. Talent development programs focusing on technical expertise and innovation capabilities are essential for long-term success in an evolving market landscape.

Risk management strategies should address raw material price volatility through diversified sourcing, long-term contracts, and vertical integration opportunities where economically viable. Regulatory compliance preparation for evolving environmental standards requires proactive investment in sustainable technologies and processes.

Future prospects for China’s plastic packaging film market remain highly positive, supported by fundamental demand drivers and ongoing technological innovation. Market evolution toward sustainable solutions and advanced functionality positions the industry for continued growth despite environmental challenges and regulatory pressures.

Growth projections indicate sustained expansion at 6.2% compound annual growth rate through the forecast period, driven by e-commerce growth, food industry development, and pharmaceutical sector expansion. MarkWide Research analysis suggests that premium segment growth will significantly outpace commodity products as manufacturers focus on value-added solutions.

Technology advancement will continue reshaping market dynamics through development of biodegradable alternatives, smart packaging solutions, and enhanced barrier technologies. Automation integration in both manufacturing and packaging operations will drive demand for films optimized for high-speed processing and consistent performance.

International expansion opportunities for Chinese manufacturers will grow through quality improvements, certification achievements, and competitive cost structures. Domestic market development in underserved regions will provide additional growth avenues as infrastructure development and economic growth continue.

Sustainability transformation will accelerate through regulatory requirements, consumer preferences, and corporate responsibility initiatives, creating opportunities for innovative companies while challenging traditional approaches. Market consolidation trends will continue as companies seek economies of scale and enhanced competitive positioning through strategic combinations and partnerships.

China’s plastic packaging film market stands at a pivotal transformation point, balancing traditional growth drivers with emerging sustainability requirements and technological innovation opportunities. The market demonstrates remarkable resilience and adaptability, with manufacturers successfully navigating environmental challenges while maintaining competitive advantages in cost-effectiveness and production capabilities.

Strategic positioning for future success requires comprehensive approaches encompassing sustainability integration, technology advancement, and market diversification across both domestic and international opportunities. Companies that successfully balance innovation investment with operational excellence will capture the most significant growth opportunities in this dynamic market environment.

Market fundamentals remain strong, supported by China’s manufacturing leadership, expanding consumer markets, and ongoing economic development. The industry’s ability to address environmental concerns while maintaining performance standards and cost competitiveness will determine long-term success and market leadership positions in the evolving global packaging landscape.

What is Plastic Packaging Film?

Plastic packaging film refers to thin, flexible sheets made from various types of plastic materials, used primarily for packaging products to protect them from damage, contamination, and spoilage. These films are widely utilized in food packaging, consumer goods, and industrial applications.

What are the key players in the China Plastic Packaging Film Market?

Key players in the China Plastic Packaging Film Market include companies such as Amcor, Sealed Air Corporation, and Berry Global, among others. These companies are known for their innovative packaging solutions and extensive product offerings in the plastic film sector.

What are the growth factors driving the China Plastic Packaging Film Market?

The growth of the China Plastic Packaging Film Market is driven by increasing demand for convenient packaging solutions, the rise of e-commerce, and the need for sustainable packaging options. Additionally, the food and beverage industry significantly contributes to the market’s expansion.

What challenges does the China Plastic Packaging Film Market face?

The China Plastic Packaging Film Market faces challenges such as environmental concerns regarding plastic waste and stringent regulations on plastic usage. These factors may hinder market growth as companies seek to adopt more sustainable practices.

What opportunities exist in the China Plastic Packaging Film Market?

Opportunities in the China Plastic Packaging Film Market include the development of biodegradable films and the integration of smart packaging technologies. These innovations can enhance product shelf life and improve consumer engagement.

What trends are shaping the China Plastic Packaging Film Market?

Trends shaping the China Plastic Packaging Film Market include the increasing focus on sustainability, the adoption of advanced manufacturing technologies, and the growing popularity of flexible packaging solutions. These trends reflect changing consumer preferences and regulatory pressures.

China Plastic Packaging Film Market

| Segmentation Details | Description |

|---|---|

| Product Type | Stretch Film, Shrink Film, Barrier Film, Rigid Film |

| Grade | Food Grade, Industrial Grade, Medical Grade, Agricultural Grade |

| Application | Food Packaging, Pharmaceutical Packaging, Consumer Goods, Industrial Packaging |

| End User | Food & Beverage, Healthcare, Retail, Logistics |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the China Plastic Packaging Film Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.