The China oil and gas downstream market refers to the sector of the oil and gas industry responsible for the processing, refining, and distribution of petroleum products. It plays a crucial role in meeting the energy demands of China’s rapidly growing economy. The downstream sector is vital for converting crude oil into various valuable products such as gasoline, diesel, jet fuel, lubricants, and petrochemicals.

Meaning

The China oil and gas downstream market encompasses all activities involved in the refining and distribution of petroleum products. It includes processes such as refining, petrochemical manufacturing, distribution, marketing, and retailing. The sector plays a significant role in meeting China’s energy needs and contributes to the country’s economic development.

Executive Summary

The China oil and gas downstream market is a crucial component of the country’s energy industry. It has witnessed steady growth over the years due to increasing energy consumption, rapid urbanization, and industrialization. The sector has attracted significant investments and is characterized by both domestic and international players competing to meet the growing demand for petroleum products in China.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rising Energy Consumption: China’s growing population, expanding middle class, and industrial development have led to an increase in energy consumption. This trend has driven the demand for petroleum products and stimulated the growth of the oil and gas downstream market.

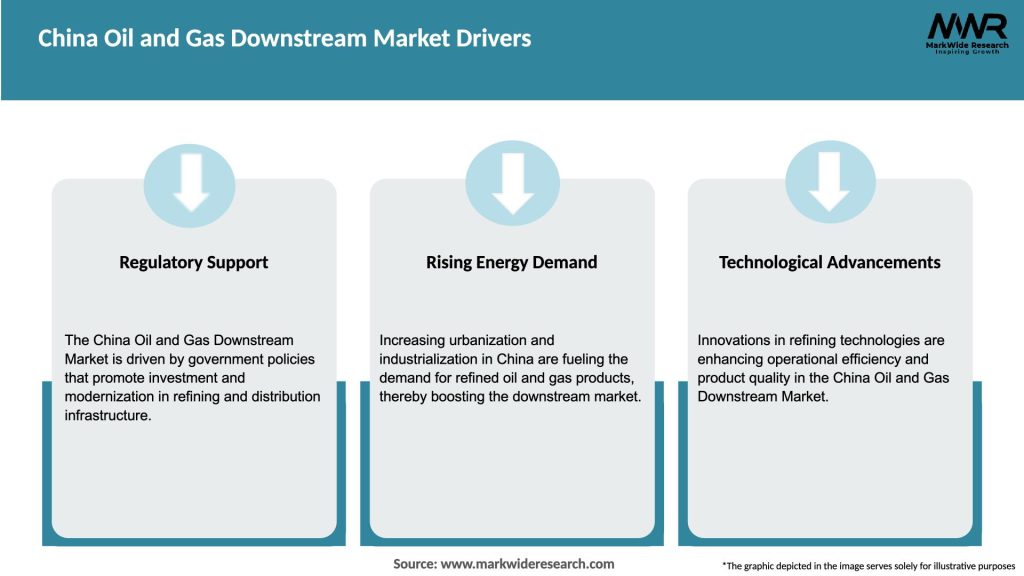

Government Initiatives: The Chinese government has implemented policies and initiatives to promote the development of the downstream sector. These include investments in refining capacity, infrastructure expansion, and the adoption of cleaner and more efficient technologies.

Environmental Concerns: With increasing environmental awareness, there is a growing emphasis on cleaner and more sustainable energy sources. The downstream market is witnessing a shift towards cleaner fuels and the development of eco-friendly technologies to reduce emissions.

Technological Advancements: The sector has seen advancements in refining technologies, process optimization, and digitalization. These innovations have improved operational efficiency, reduced costs, and enhanced product quality.

Market Drivers

Growing Energy Demand: China’s rapid economic growth and urbanization have resulted in a surge in energy consumption. The increasing demand for transportation fuels, electricity, and petrochemicals is a major driver for the oil and gas downstream market.

Infrastructure Development: Infrastructure investments, including the construction of refineries, storage facilities, and distribution networks, are driving the expansion of the downstream market. These developments aim to enhance supply capabilities and meet the rising demand for petroleum products.

Favorable Government Policies: The Chinese government has implemented policies to encourage investments in the downstream sector. These policies include tax incentives, subsidies, and favorable regulatory frameworks, which attract both domestic and foreign companies to invest in the market.

Rising Vehicle Ownership: The growing middle class and increasing disposable income have led to a rise in vehicle ownership. This has propelled the demand for gasoline and diesel, driving the growth of the downstream market.

Market Restraints

Volatile crude Oil Prices: Fluctuating crude oil prices impact the profitability of the downstream market. Sharp price fluctuations can affect margins and profitability, making it challenging for downstream companies to plan and make long-term investment decisions.

Environmental Concerns and Regulations: Stringent environmental regulations and the need to reduce carbon emissions pose challenges for the downstream market. Companies must invest in cleaner technologies and comply with strict emission standards, which can increase operational costs.

Competition from Electric Vehicles: The growing popularity of electric vehicles poses a long-term threat to the downstream market. As electric vehicles become more affordable and charging infrastructure improves, the demand for traditional petroleum products could decline.

Infrastructure Limitations: In certain regions, the lack of adequate infrastructure, including pipelines, storage facilities, and transportation networks, can hinder the efficient distribution of petroleum products, limiting market growth.

Market Opportunities

Petrochemical Sector Expansion: China’s growing petrochemical industry presents significant opportunities for the downstream market. The demand for petrochemical products, such as plastics, polymers, and synthetic fibers, is increasing, driving the need for feedstocks produced by the downstream sector.

International Cooperation: China’s Belt and Road Initiative (BRI) encourages international cooperation in energy projects. This provides opportunities for foreign companies to collaborate with Chinese counterparts in refining, distribution, and infrastructure development.

Renewable Fuels and Clean Technologies: The transition towards cleaner and renewable energy sources presents opportunities for the downstream market. Investments in biofuels, hydrogen, and other alternative energy technologies can diversify product portfolios and meet evolving consumer preferences.

Digital Transformation: The adoption of digital technologies, such as advanced analytics, artificial intelligence, and automation, can optimize operations, improve productivity, and reduce costs in the downstream sector. Embracing digital transformation presents opportunities for companies to gain a competitive edge.

Market Dynamics

The China oil and gas downstream market is dynamic and influenced by various factors, including economic growth, energy policies, technological advancements, and environmental considerations. It is characterized by intense competition, evolving consumer preferences, and changing regulatory frameworks. Companies in the sector must continuously adapt to market dynamics, invest in innovation, and maintain strong partnerships to thrive in this rapidly changing landscape.

Regional Analysis

The China oil and gas downstream market is geographically diverse, with refining and distribution facilities located throughout the country. Key regions include:

Eastern China: This region, including major cities like Shanghai and Guangzhou, is a significant hub for the oil and gas downstream industry. It has a well-developed infrastructure and houses several major refineries and petrochemical complexes.

Northern China: The northern region, including cities such as Beijing and Tianjin, is a major consumer of petroleum products. It is characterized by a high concentration of industrial activities and transportation networks, driving the demand for fuels and petrochemicals.

Coastal Areas: China’s coastal areas, including provinces like Shandong and Zhejiang, have significant refining and petrochemical capacities. These regions benefit from proximity to major ports, facilitating export and import activities.

Western and Central China: These regions are experiencing rapid industrialization and urbanization, leading to increased energy consumption. The development of refining and distribution infrastructure in these areas aims to meet the growing demand for petroleum products.

Competitive Landscape

Leading companies in the China Oil and Gas Downstream Market:

PetroChina Company Limited

Sinopec Corporation

China National Offshore Oil Corporation (CNOOC)

China Petroleum & Chemical Corporation (Sinopec)

China National Aviation Fuel Group Corporation

Sinochem Group

China Huaneng Group

China Huadian Corporation Ltd.

China Resources (Holdings) Co., Ltd.

China State Construction Engineering Corporation (CSCEC)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

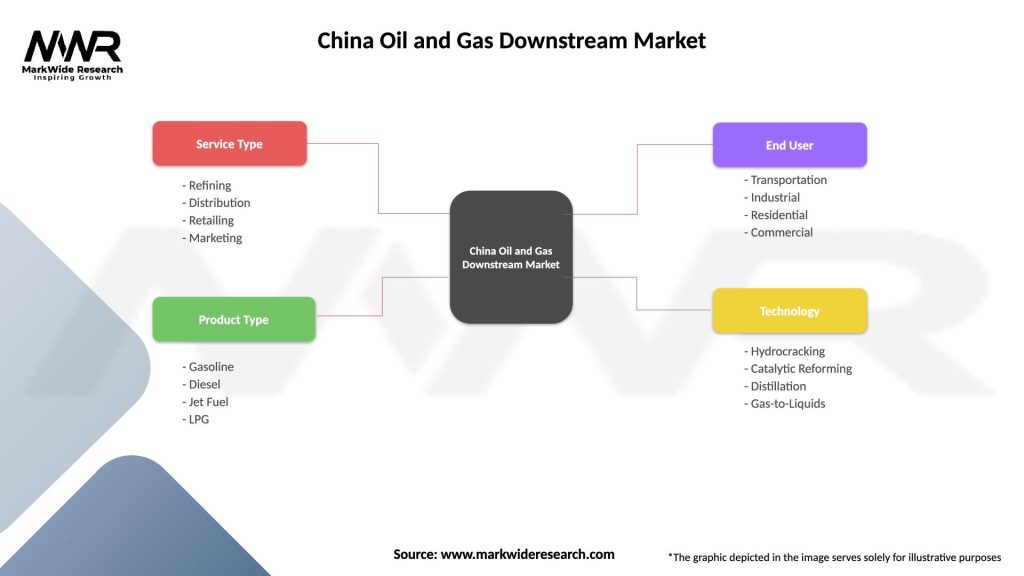

Segmentation

The China oil and gas downstream market can be segmented based on the following factors:

Product Type: The market can be segmented by product types, including gasoline, diesel, jet fuel, lubricants, and petrochemicals. Each product category has its unique demand drivers and market dynamics.

Distribution Channel: The downstream market can be segmented based on distribution channels, including wholesale, retail, and direct sales. Retail channels involve fuel stations and convenience stores, while wholesale channels supply to industrial and commercial customers.

End-User Industries: The market can also be segmented based on end-user industries, such as transportation, manufacturing, power generation, and chemicals. Each industry segment has specific requirements and demand patterns for petroleum products.

Category-wise Insights

Gasoline: Gasoline is a vital fuel for the transportation sector, especially passenger vehicles. The demand for gasoline in China is driven by the increasing number of vehicles on the road and changing consumer preferences.

Diesel: Diesel is predominantly used in heavy-duty vehicles, trucks, and industrial machinery. The growth of the logistics sector and industrial activities in China contributes to the demand for diesel.

Jet Fuel: China’s booming aviation industry drives the demand for jet fuel. The growth of air travel, both domestically and internationally, stimulates the demand for jet fuel in airports across the country.

Lubricants: Lubricants are essential for ensuring smooth operation and maintenance of machinery and equipment. The expanding industrial and manufacturing sectors in China drive the demand for lubricants.

Petrochemicals: China’s petrochemical industry is witnessing significant growth, driven by the increasing demand for plastics, polymers, and chemicals. The downstream sector plays a critical role in providing feedstocks for petrochemical production.

Key Benefits for Industry Participants and Stakeholders

Revenue Generation: The oil and gas downstream market offers substantial revenue opportunities for industry participants. Companies involved in refining, distribution, and marketing can benefit from the growing demand for petroleum products in China.

Market Expansion: The downstream sector provides avenues for market expansion, both domestically and internationally. Companies can leverage partnerships, investments, and technological advancements to expand their operations and customer base.

Employment Generation: The oil and gas downstream market creates employment opportunities across various segments, including refinery operations, logistics, marketing, and retail. It contributes to job creation and economic development in the country.

Technology Adoption: The downstream market encourages the adoption of advanced technologies and innovation. Companies can benefit from increased operational efficiency, reduced costs, and improved product quality by embracing digitalization and process optimization.

SWOT Analysis

Strengths:

Vast Market Potential: China’s huge population and growing energy needs create a substantial market for petroleum products, providing opportunities for growth and profitability.

Extensive Infrastructure: The country has a well-developed infrastructure for refining, storage, and distribution, facilitating efficient supply chains and market reach.

Government Support: The Chinese government’s support through policies, investments, and favorable regulations encourages the development of the downstream sector.

Weaknesses:

Environmental Concerns: The downstream market faces challenges related to emissions and environmental impact. Companies must invest in cleaner technologies to comply with strict regulations.

Volatile Crude Oil Prices: The market’s vulnerability to fluctuating crude oil prices can impact profit margins and financial stability.

Opportunities:

Shift towards Cleaner Energy: The transition to cleaner and renewable energy sources presents opportunities for the downstream market to diversify its product portfolio and meet evolving consumer preferences.

International Cooperation: Collaboration with international partners and participation in global energy projects, such as the Belt and Road Initiative, can open new avenues for growth and expansion.

Threats:

Electric Vehicles: The increasing popularity of electric vehicles poses a long-term threat to the demand for traditional petroleum products. Downstream companies must adapt to the changing landscape and explore opportunities in the electric vehicle market.

Market Competition: The downstream sector is highly competitive, with both domestic and international players vying for market share. Intense competition can impact pricing and profitability.

Market Key Trends

Digitalization and Automation: The adoption of digital technologies, such as advanced analytics, artificial intelligence, and automation, is transforming the downstream sector. Companies are leveraging data-driven insights to optimize operations and enhance efficiency.

Sustainable Practices: Environmental concerns and the need for sustainable practices are driving the adoption of cleaner technologies, renewable fuels, and eco-friendly processes in the downstream market.

Integration and Diversification: Companies are focusing on integrating their operations and diversifying their product portfolios to enhance competitiveness and capture a larger market share.

Refinery Upgrades: Refinery upgrades and capacity expansions are being undertaken to meet the increasing demand for petroleum products and comply with stricter environmental regulations.

Covid-19 Impact

The Covid-19 pandemic had a significant impact on the China oil and gas downstream market. The measures implemented to control the spread of the virus, such as lockdowns, travel restrictions, and reduced economic activity, led to a decline in energy demand. The transportation sector, including aviation and road transportation, experienced a sharp decrease in fuel consumption.

However, China’s effective management of the pandemic and subsequent economic recovery resulted in a rebound in energy demand. As the country reopened and industrial activities resumed, the downstream market witnessed a gradual recovery. The Chinese government’s stimulus measures and infrastructure investments also helped stimulate energy consumption and support market recovery.

The pandemic highlighted the importance of resilient supply chains and the need for contingency planning. It accelerated digitalization efforts in the downstream sector, with companies adopting remote monitoring, automation, and other digital solutions to enhance operational efficiency and minimize disruptions.

Key Industry Developments

Refinery Expansions: Several refineries in China have undergone capacity expansions and upgrades to meet the growing demand for petroleum products. These developments aim to enhance efficiency, reduce emissions, and increase product quality.

Petrochemical Investments: The petrochemical sector has witnessed significant investments in China, driven by the increasing demand for plastics and chemicals. Companies are expanding their petrochemical capacities to cater to domestic and international markets.

Cleaner Fuel Initiatives: The Chinese government has implemented initiatives to promote the use of cleaner fuels, such as Euro VI emission standards for vehicles. This has led to the development and adoption of advanced refining technologies and the production of low-sulfur fuels.

International Collaborations: Chinese companies have been forging partnerships and collaborations with international counterparts to gain access to advanced technologies, market expertise, and global distribution networks. These collaborations aim to enhance competitiveness and accelerate innovation in the downstream sector.

Analyst Suggestions

Embrace Sustainability: Downstream companies should focus on adopting sustainable practices, reducing emissions, and investing in cleaner technologies. This will help meet regulatory requirements and address environmental concerns.

Diversify Product Portfolio: Companies should explore opportunities to diversify their product portfolios, including the production of biofuels, hydrogen, and other alternative energy sources. Diversification can help mitigate risks associated with changing market dynamics and consumer preferences.

Invest in Digital Transformation: The adoption of digital technologies can enhance operational efficiency, optimize supply chains, and improve customer experiences. Companies should invest in digital transformation initiatives to remain competitive in the evolving market.

Collaboration and Partnerships: Collaboration with international partners and technology providers can bring new perspectives, expertise, and market access. Companies should seek strategic partnerships to enhance their capabilities and expand their presence in the downstream sector.

Future Outlook

The future outlook for the China oil and gas downstream market remains promising. Despite challenges posed by environmental regulations, market competition, and the transition to cleaner energy, the growing energy demand, government support, and infrastructure development provide a solid foundation for market growth.

The sector will witness continued investments in refinery expansions, petrochemical capacities, and infrastructure development. The adoption of digital technologies, sustainable practices, and cleaner fuels will shape the industry’s future.

China’s focus on energy security, economic growth, and sustainable development will drive the demand for petroleum products. Downstream companies that adapt to market dynamics, embrace innovation, and prioritize sustainability will be well-positioned to thrive in this evolving landscape.

Conclusion

The China oil and gas downstream market plays a vital role in meeting the country’s energy needs and supporting economic development. The sector faces both challenges and opportunities, driven by factors such as energy demand, environmental concerns, technological advancements, and government policies.

The market’s future outlook remains positive, with opportunities arising from petrochemical expansion, international cooperation, renewable fuels, and digital transformation. Companies that embrace sustainability, diversify their product portfolios, invest in technology, and seek strategic collaborations will be well-prepared to navigate the evolving market dynamics and drive future growth in the China oil and gas downstream market.

What is Oil and Gas Downstream?

Oil and Gas Downstream refers to the processes involved in refining crude oil and distributing petroleum products. This includes the production of fuels, lubricants, and petrochemicals, as well as the marketing and sale of these products to consumers and industries.

What are the key players in the China Oil and Gas Downstream Market?

Key players in the China Oil and Gas Downstream Market include Sinopec, PetroChina, and CNOOC. These companies dominate the refining and distribution sectors, providing a wide range of petroleum products and services, among others.

What are the growth factors driving the China Oil and Gas Downstream Market?

The growth of the China Oil and Gas Downstream Market is driven by increasing energy demand, urbanization, and the expansion of the transportation sector. Additionally, advancements in refining technologies and the rise of petrochemical production contribute to market growth.

What challenges does the China Oil and Gas Downstream Market face?

The China Oil and Gas Downstream Market faces challenges such as regulatory pressures, environmental concerns, and fluctuating crude oil prices. These factors can impact profitability and operational efficiency for companies in the sector.

What opportunities exist in the China Oil and Gas Downstream Market?

Opportunities in the China Oil and Gas Downstream Market include the development of cleaner fuels, investment in renewable energy sources, and the expansion of infrastructure for distribution. These trends can enhance sustainability and meet changing consumer preferences.

What trends are shaping the China Oil and Gas Downstream Market?

Trends shaping the China Oil and Gas Downstream Market include the shift towards digitalization, the adoption of advanced refining technologies, and increasing focus on sustainability. Companies are also exploring alternative energy sources to adapt to market changes.

Leading companies in the China Oil and Gas Downstream Market:

PetroChina Company Limited

Sinopec Corporation

China National Offshore Oil Corporation (CNOOC)

China Petroleum & Chemical Corporation (Sinopec)

China National Aviation Fuel Group Corporation

Sinochem Group

China Huaneng Group

China Huadian Corporation Ltd.

China Resources (Holdings) Co., Ltd.

China State Construction Engineering Corporation (CSCEC)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.