The factoring services market in China is witnessing rapid growth and transformation, driven by factors such as economic development, urbanization, and the increasing demand for working capital solutions among businesses. Factoring services play a crucial role in facilitating trade, supporting SMEs, and optimizing cash flow management in China’s dynamic business environment. With the government’s support for financial innovation and the expansion of digital platforms, the factoring industry in China presents significant opportunities for factors and businesses to collaborate and thrive.

Meaning

Factoring services in China involve the purchase of accounts receivable by specialized financial institutions known as factors. Businesses, particularly SMEs, utilize factoring to convert unpaid invoices into immediate cash, improve liquidity, and mitigate credit risk. Factors provide funding against invoices, assume credit risk, and manage collections, enabling businesses to optimize cash flow, enhance working capital management, and focus on core operations.

Executive Summary

The factoring services market in China is experiencing robust growth, supported by factors such as increasing demand for working capital solutions, technological innovation, and government initiatives to promote financial inclusion and SME financing. Despite challenges such as regulatory complexity, credit risk management, and market competition, the factoring industry in China offers vast opportunities for factors and businesses to capitalize on the country’s economic development, digital transformation, and expanding market dynamics.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Economic Development: China’s rapid economic growth, urbanization, and industrialization drive the demand for factoring services, as businesses seek efficient working capital solutions to support growth, expansion, and trade activities.

Financial Innovation: The Chinese government’s support for financial innovation and the expansion of digital platforms has fostered the growth of the factoring industry, enabling factors to leverage technology, data analytics, and online platforms to streamline operations and reach a wider customer base.

SME Financing: Factoring services cater to the financing needs of SMEs in China, providing them with access to working capital, credit risk protection, and financial stability to support growth, innovation, and entrepreneurship.

Trade Facilitation: Factoring plays a crucial role in facilitating domestic and international trade in China, providing exporters and importers with access to financing, credit risk mitigation, and supply chain support to facilitate cross-border transactions and business expansion.

Market Drivers

Working Capital Optimization: Factoring services enable businesses to optimize working capital by accelerating the conversion of accounts receivable into liquid assets, improving liquidity ratios, and reducing reliance on traditional bank financing sources.

Financial Inclusion: Factors in China support financial inclusion by providing working capital solutions to SMEs and underserved businesses that may have limited access to traditional bank financing due to credit constraints or regulatory requirements.

Digital Transformation: The adoption of digital technologies such as AI, blockchain, and mobile payment platforms has transformed the factoring industry in China, enabling factors to streamline operations, enhance customer experience, and mitigate credit risk through real-time data analytics and online platforms.

Government Support: The Chinese government’s initiatives to promote financial inclusion, SME financing, and trade facilitation support the growth of the factoring industry, creating a conducive regulatory environment and policy framework for factors and businesses to operate and thrive.

Market Restraints

Regulatory Complexity: The factoring industry in China is subject to regulatory oversight and compliance requirements from various government agencies, including the People’s Bank of China (PBOC), China Banking and Insurance Regulatory Commission (CBIRC), and local financial regulators, adding complexity and operational costs to factors’ operations.

Credit Risk Management: Factors face credit risk exposure from non-payment or late payment by customers, requiring robust credit risk management practices, stringent underwriting criteria, and proactive collections strategies to mitigate risk and maintain financial stability in China’s dynamic business environment.

Market Competition: The factoring services market in China is highly competitive, with factors competing based on factors such as pricing, service quality, industry expertise, and geographic coverage, driving innovation, differentiation, and consolidation in the marketplace.

Technological Risks: The reliance on digital technologies and online platforms exposes factors to cybersecurity risks, data breaches, and operational disruptions, necessitating investments in cybersecurity measures, data protection, and business continuity planning to safeguard against potential threats and vulnerabilities.

Market Opportunities

SME Financing: Factoring services offer a lifeline to SMEs in China, providing them with access to working capital, credit risk protection, and financial stability to support growth, innovation, and entrepreneurship in a rapidly evolving business landscape.

Supply Chain Finance: Factoring plays a crucial role in supply chain finance, providing financing, credit risk mitigation, and supply chain support to businesses across various industries, including manufacturing, retail, logistics, and e-commerce, to optimize cash flow, enhance liquidity, and improve operational efficiency.

Technology Integration: Embracing digital technologies such as AI, blockchain, and mobile payment platforms can enhance operational efficiency, streamline customer interactions, and mitigate credit risk through real-time data analytics, automated underwriting processes, and online platforms.

Trade Facilitation: Factoring services support domestic and international trade in China by providing exporters and importers with access to financing, credit risk mitigation, and supply chain support to facilitate cross-border transactions, mitigate trade-related risks, and expand market reach.

Market Dynamics

The factoring services market in China operates within a dynamic and evolving ecosystem influenced by factors such as economic conditions, technological advancements, regulatory developments, and market competition. These dynamics shape the demand for factoring services, the competitive landscape, and the overall market outlook, requiring factors to adapt and innovate to stay competitive and relevant in the marketplace.

Regional Analysis

The factoring services market in China exhibits regional variations in terms of market demand, industry composition, and regulatory environment. Major cities such as Shanghai, Beijing, Shenzhen, and Guangzhou serve as hubs for financial services and attract factors seeking to tap into local markets, industries, and business opportunities. Factors must consider regional factors and market dynamics when developing strategies and targeting clients in specific geographic regions.

Competitive Landscape

Leading Companies in China Factoring Services Market:

Industrial and Commercial Bank of China Limited (ICBC)

China Construction Bank Corporation

Bank of China Limited

Agricultural Bank of China Limited

China Merchants Bank Co., Ltd.

China Minsheng Banking Corp., Ltd.

Bank of Communications Co., Ltd.

Postal Savings Bank of China Co., Ltd.

China Everbright Bank Co., Ltd.

Industrial Bank Co., Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

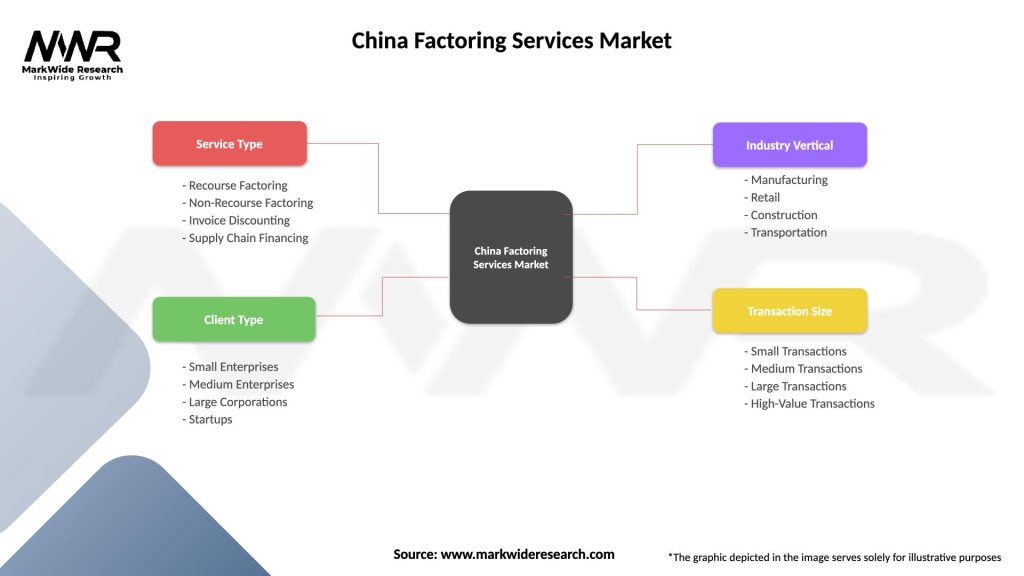

Segmentation

The factoring services market in China can be segmented based on various factors such as:

Industry Vertical: Segmentation by industry vertical includes sectors such as manufacturing, retail, healthcare, construction, and transportation, with factors offering tailored solutions to meet the unique financing needs and challenges of each industry.

Invoice Volume: Segmentation by invoice volume includes businesses with varying levels of invoice turnover, from low-volume SMEs to high-volume corporates, with factors customizing financing arrangements and pricing structures based on invoice volume and frequency.

Geographic Reach: Segmentation by geographic reach includes factors operating at the local, regional, national, or international level, with factors leveraging their network and infrastructure to serve clients across different geographic regions and markets.

Segmentation enables factors to tailor their offerings, pricing structures, and marketing strategies to specific customer segments, enhancing relevance, targeting, and customer satisfaction.

Category-wise Insights

Recourse Factoring: Recourse factoring involves the sale of accounts receivable with recourse, meaning the factor has the right to recourse to the seller in case of non-payment by the customer. It is suitable for businesses with established creditworthiness and low credit risk exposure.

Non-Recourse Factoring: Non-recourse factoring offers credit risk protection to the seller, with the factor assuming responsibility for bad debt losses in case of customer default. It provides peace of mind to businesses concerned about credit risk and offers predictable cash flow without recourse to the seller.

Spot Factoring: Spot factoring allows businesses to selectively finance individual invoices or batches of invoices on a case-by-case basis, providing flexibility and control over the financing process. It is ideal for businesses with occasional cash flow needs or seasonal fluctuations in invoice volume.

Construction Factoring: Construction factoring caters to the unique financing needs of construction companies, subcontractors, and suppliers by providing advances against construction-related invoices, progress billings, and accounts receivable. It helps address cash flow challenges associated with project-based invoicing and long payment cycles in the construction industry.

Key Benefits for Industry Participants and Stakeholders

Improved Cash Flow: Factoring services provide immediate access to cash, enabling businesses to meet operational expenses, fund growth initiatives, and seize business opportunities without waiting for customer payments.

Credit Risk Protection: Factors assume credit risk for the invoices they purchase, protecting businesses from bad debt losses and providing peace of mind to sellers concerned about customer default or insolvency.

Working Capital Optimization: Factoring helps optimize working capital by converting accounts receivable into liquid assets, improving liquidity ratios, and reducing reliance on traditional lending sources such as bank loans or lines of credit.

Streamlined Operations: Factors handle collections, credit analysis, and accounts receivable management, freeing up time and resources for businesses to focus on core operations, sales, and customer relationships.

Business Growth: Factoring services support business growth by providing access to flexible and scalable financing solutions that adapt to changing business needs, market conditions, and growth opportunities.

SWOT Analysis

Strengths:

Liquidity: Factoring services provide immediate cash flow without adding debt to the balance sheet, improving liquidity and financial flexibility for businesses.

Risk Mitigation: Factors assume credit risk for the invoices they purchase, protecting businesses from bad debt losses and providing peace of mind to sellers concerned about customer default or insolvency.

Flexibility: Factoring arrangements are flexible and scalable, allowing businesses to finance individual invoices or entire accounts receivable portfolios based on their cash flow needs and growth objectives.

Speed: Factoring offers quick access to cash, with funding typically available within 24 to 48 hours of invoice verification, enabling businesses to address urgent cash flow needs and capitalize on time-sensitive opportunities.

Weaknesses:

Cost: Factoring services can be more expensive than traditional bank financing, with factors charging fees based on factors such as the volume of invoices, the creditworthiness of customers, and the risk profile of the industry.

Customer Relationships: Factors interact directly with customers during the collections process, which can potentially strain customer relationships or damage the seller’s reputation if not handled professionally and diplomatically.

Dependency: Businesses that rely heavily on factoring may become dependent on this form of financing, limiting their ability to access alternative financing sources or negotiate better terms with suppliers and customers.

Opportunities:

Market Expansion: The factoring services market in China is poised for expansion, driven by factors such as increased awareness, changing attitudes towards alternative financing, and the emergence of innovative factoring solutions tailored to the needs of SMEs and startups.

Technology Integration: Embracing digital technologies such as AI, blockchain, and mobile payment platforms can enhance operational efficiency, improve risk management, and unlock new opportunities for innovation and growth in the factoring industry in China.

Industry Specialization: Factors can differentiate themselves by specializing in specific industries or niche markets, such as healthcare, construction, or transportation, and offering tailored factoring solutions that meet the unique needs and challenges of those industries.

Threats:

Regulatory Compliance: Compliance with regulatory requirements, including federal and EU regulations governing disclosure, consumer protection, and AML compliance, is critical for factors to build trust, credibility, and legitimacy in the factoring industry.

Competition: The factoring services market in China is highly competitive, with factors competing based on factors such as pricing, service quality, industry expertise, and geographic coverage, driving innovation, differentiation, and consolidation in the marketplace.

Credit Risk: Factors face credit risk exposure from non-payment or late payment by customers, requiring robust credit risk management practices, stringent underwriting criteria, and proactive collections strategies to mitigate risk and maintain financial stability in China’s dynamic business environment.

Market Key Trends

Digital Transformation: The factoring industry in China is undergoing digital transformation, with factors embracing technology, automation, and online platforms to streamline operations, enhance customer experience, and mitigate credit risk through real-time data analytics and online platforms.

Fintech Integration: The integration of fintech solutions such as AI, blockchain, and mobile payment platforms is reshaping the factoring landscape in China, enabling factors to offer innovative, efficient, and customer-centric factoring solutions tailored to the needs of SMEs and startups.

Platform Economy: Online platforms and marketplaces are emerging as key players in the factoring ecosystem, connecting factors with businesses seeking working capital solutions and providing access to a wide range of factoring services, financing options, and risk management tools.

Supply Chain Finance: Factoring services are evolving beyond traditional accounts receivable financing to encompass supply chain finance solutions, providing financing, credit risk mitigation, and supply chain support to businesses across various industries, including manufacturing, retail, and e-commerce.

Covid-19 Impact

The COVID-19 pandemic had a significant impact on the factoring services market in China, with both challenges and opportunities arising from the crisis:

Challenges:

Economic Uncertainty: The pandemic led to economic uncertainty, supply chain disruptions, and decreased demand for goods and services, impacting business operations, cash flow, and credit risk in the factoring industry.

Credit Risk: Factors faced increased credit risk exposure from customers affected by the pandemic, requiring stringent credit risk management practices, proactive collections strategies, and adjustments to underwriting criteria to mitigate risk and maintain financial stability.

Regulatory Changes: The pandemic prompted regulatory changes and government interventions to support businesses, stabilize financial markets, and mitigate the economic impact of the crisis, affecting factors’ operations, compliance requirements, and risk management practices.

Opportunities:

Digital Adoption: The pandemic accelerated the adoption of digital technologies in the factoring industry, with factors embracing online platforms, automation, and remote collaboration tools to streamline operations, enhance customer experience, and adapt to the new normal of remote work and digital transactions.

Government Support: The Chinese government implemented measures to support businesses, stabilize financial markets, and stimulate economic recovery, providing factors with opportunities to collaborate with government agencies, financial institutions, and industry stakeholders to address challenges and unlock new growth opportunities.

Market Expansion: Despite challenges posed by the pandemic, the factoring services market in China remained resilient, with factors adapting to changing market dynamics, leveraging technology, and exploring new business models to expand market reach, meet customer needs, and drive industry growth.

Key Industry Developments

Digital Innovation: The pandemic accelerated the adoption of digital technologies in the factoring industry, with factors investing in AI, machine learning, and blockchain to enhance operational efficiency, improve risk management, and meet evolving customer expectations.

Customer-Centric Solutions: Factors are prioritizing customer-centricity, transparency, and trust in their interactions with clients, fostering long-term relationships, loyalty, and referrals through exceptional service, communication, and responsiveness.

Regulatory Compliance: Compliance with regulatory requirements, including federal and EU regulations governing disclosure, consumer protection, and AML compliance, remains a top priority for factors to build trust, credibility, and legitimacy in the factoring industry.

Market Consolidation: The pandemic has sparked consolidation in the factoring industry, with larger factors acquiring smaller competitors, expanding market share, and diversifying service offerings to meet evolving customer needs and market demands.

Analyst Suggestions

Risk Management: Factors should prioritize credit risk management, collections, and underwriting practices to mitigate risk, protect against bad debt losses, and maintain financial stability in the face of economic uncertainty and market volatility.

Digital Innovation: Embracing digital technologies such as AI, machine learning, and blockchain can enhance operational efficiency, improve risk management, and unlock new opportunities for innovation and growth in the factoring industry in China.

Customer-Centricity: Factors should prioritize customer-centricity, transparency, and trust in their interactions with clients, fostering long-term relationships, loyalty, and referrals through exceptional service, communication, and responsiveness.

Compliance: Compliance with regulatory requirements, including federal and EU regulations governing disclosure, consumer protection, and AML compliance, is critical for factors to build trust, credibility, and legitimacy in the factoring industry.

Future Outlook

The factoring services market in China is expected to rebound and resume growth trajectory as businesses recover from the impacts of the pandemic, economic activity resumes, and demand for working capital solutions rebounds. Factors such as technological innovation, regulatory evolution, and industry collaboration will continue to shape the future of the factoring industry in China, driving innovation, expansion, and sustainability.

Conclusion

The factoring services market in China plays a crucial role in supporting businesses’ working capital needs, enhancing cash flow management, and fueling economic growth. Despite challenges posed by regulatory compliance, credit risk management, and market competition, the factoring industry in China remains resilient, adaptable, and well-positioned for future growth and innovation. By embracing technology, collaboration, and customer-centricity, factors can navigate uncertainty, seize opportunities, and contribute to a vibrant and dynamic factoring ecosystem that benefits businesses, industries, and the Chinese economy as a whole.

What is Factoring Services?

Factoring services involve the sale of accounts receivable to a third party, known as a factor, to improve cash flow. This financial service is commonly used by businesses to manage their working capital and reduce the risk of bad debts.

What are the key players in the China Factoring Services Market?

Key players in the China Factoring Services Market include China Minmetals Corporation, Bank of China, and China Construction Bank, among others. These companies provide various factoring solutions tailored to different industries, enhancing liquidity for businesses.

What are the growth factors driving the China Factoring Services Market?

The growth of the China Factoring Services Market is driven by increasing demand for working capital, the expansion of small and medium-sized enterprises, and the need for efficient cash flow management. Additionally, the rise of e-commerce has further fueled the need for factoring services.

What challenges does the China Factoring Services Market face?

Challenges in the China Factoring Services Market include regulatory hurdles, the risk of default on receivables, and competition from alternative financing options. These factors can impact the growth and stability of factoring services in the region.

What opportunities exist in the China Factoring Services Market?

Opportunities in the China Factoring Services Market include the potential for digital transformation, the introduction of innovative financial products, and the growing acceptance of factoring among various industries. These trends can enhance service offerings and attract new clients.

What trends are shaping the China Factoring Services Market?

Trends in the China Factoring Services Market include the increasing use of technology for risk assessment and client onboarding, the rise of online factoring platforms, and a focus on sustainability in financial practices. These trends are reshaping how factoring services are delivered and utilized.

Leading Companies in China Factoring Services Market:

Industrial and Commercial Bank of China Limited (ICBC)

China Construction Bank Corporation

Bank of China Limited

Agricultural Bank of China Limited

China Merchants Bank Co., Ltd.

China Minsheng Banking Corp., Ltd.

Bank of Communications Co., Ltd.

Postal Savings Bank of China Co., Ltd.

China Everbright Bank Co., Ltd.

Industrial Bank Co., Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.