444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The China electric vehicle battery materials market represents one of the most dynamic and rapidly evolving sectors within the global automotive industry. As the world’s largest electric vehicle market, China has established itself as a dominant force in the production and consumption of critical battery materials including lithium, cobalt, nickel, graphite, and rare earth elements. The market encompasses a comprehensive ecosystem of raw material extraction, processing, manufacturing, and recycling operations that support the country’s ambitious electrification goals.

Market dynamics indicate that China controls approximately 60% of global lithium processing capacity and maintains significant influence over the supply chains of other essential battery materials. The country’s strategic focus on achieving carbon neutrality by 2060 has accelerated investments in battery material technologies, with particular emphasis on developing sustainable and cost-effective solutions for next-generation electric vehicles.

Key market characteristics include vertical integration strategies adopted by major Chinese companies, substantial government support through policy incentives, and continuous technological innovations in material processing and battery chemistry. The market benefits from China’s established manufacturing infrastructure, skilled workforce, and proximity to key raw material sources across Asia-Pacific regions.

The China electric vehicle battery materials market refers to the comprehensive ecosystem of raw materials, processed components, and specialized chemicals required for manufacturing lithium-ion batteries used in electric vehicles within China’s automotive sector. This market encompasses the entire value chain from mineral extraction and processing to advanced material synthesis and recycling operations.

Battery materials include critical components such as lithium compounds for electrolytes, cathode materials containing nickel, cobalt, and manganese, anode materials primarily based on graphite, separator materials, and various additives that enhance battery performance, safety, and longevity. The market also covers emerging materials for next-generation battery technologies including solid-state electrolytes and silicon-based anodes.

Strategic importance of this market extends beyond automotive applications, as these materials are essential for energy storage systems, consumer electronics, and industrial applications. China’s dominance in this sector reflects its comprehensive approach to securing supply chain control and technological leadership in the global transition to electric mobility.

China’s electric vehicle battery materials market continues to demonstrate exceptional growth momentum, driven by the country’s leadership in electric vehicle adoption and manufacturing. The market benefits from comprehensive government support, substantial private sector investments, and China’s strategic positioning as a global hub for battery material processing and production.

Key growth drivers include the rapid expansion of domestic electric vehicle production, increasing demand for energy storage systems, and China’s commitment to developing a complete domestic supply chain for critical battery materials. The market is experiencing significant technological advancement with 15% annual improvement in material processing efficiency and cost reduction initiatives.

Market structure reflects high concentration among leading Chinese companies that have achieved vertical integration across the battery materials value chain. These companies are expanding their global footprint through strategic acquisitions, joint ventures, and direct investments in overseas mining and processing operations.

Competitive landscape features both established chemical companies and specialized battery material manufacturers, with increasing collaboration between automotive OEMs and material suppliers to secure long-term supply agreements and develop customized solutions for specific vehicle platforms.

Strategic market insights reveal several critical trends shaping the China electric vehicle battery materials landscape:

Primary market drivers propelling the China electric vehicle battery materials sector include the country’s aggressive electric vehicle adoption targets and comprehensive policy support framework. The Chinese government’s commitment to achieving 25% electric vehicle market share by 2025 creates substantial demand for battery materials across all vehicle segments.

Technological advancement serves as a crucial driver, with continuous improvements in battery chemistry, energy density, and charging capabilities requiring sophisticated material solutions. Chinese companies are investing heavily in research and development to maintain technological leadership and develop next-generation materials for solid-state batteries and other advanced technologies.

Cost competitiveness remains a fundamental driver, as China’s integrated supply chains, manufacturing scale, and process optimization enable significant cost advantages compared to other regions. The country’s ability to produce high-quality materials at competitive prices supports both domestic market growth and global export opportunities.

Infrastructure development including charging networks, manufacturing facilities, and logistics systems creates additional demand for battery materials while supporting market expansion. The circular economy initiatives focusing on battery recycling and material recovery are generating new revenue streams and reducing dependence on primary raw materials.

Market restraints affecting the China electric vehicle battery materials sector include increasing environmental regulations and sustainability requirements that necessitate substantial investments in cleaner production technologies and waste management systems. These regulatory pressures create compliance costs and operational challenges for material producers.

Raw material supply constraints pose significant challenges, particularly for critical materials like lithium and cobalt where China depends heavily on imports from politically sensitive regions. Price volatility in raw material markets creates uncertainty and affects long-term planning and investment decisions.

International trade tensions and geopolitical considerations impact global supply chains and market access, potentially limiting export opportunities and creating barriers to technology transfer and international collaboration. These factors may affect the competitiveness of Chinese battery material companies in certain markets.

Technical challenges related to material performance, safety requirements, and quality consistency continue to require substantial research and development investments. The complexity of battery chemistry and the need for precise material specifications create ongoing technical and commercial risks for market participants.

Significant market opportunities exist in the development of next-generation battery materials including solid-state electrolytes, silicon-based anodes, and advanced cathode materials that offer improved performance characteristics. These emerging technologies represent substantial growth potential for innovative Chinese companies.

Global expansion opportunities are emerging as international markets accelerate electric vehicle adoption and seek reliable suppliers of high-quality battery materials. Chinese companies can leverage their cost advantages and technical expertise to capture market share in Europe, North America, and other regions.

Recycling and circular economy initiatives present new business opportunities as the volume of end-of-life batteries increases. Companies developing efficient recycling technologies and processes can create sustainable revenue streams while addressing environmental concerns and resource scarcity issues.

Energy storage applications beyond automotive markets, including grid-scale storage, residential systems, and industrial applications, offer additional growth opportunities for battery material suppliers. The expanding renewable energy sector creates substantial demand for energy storage solutions and associated materials.

Market dynamics in China’s electric vehicle battery materials sector reflect the complex interplay between supply chain control, technological innovation, and government policy support. The market demonstrates strong growth momentum with 12% annual capacity expansion across key material categories, driven by increasing domestic demand and export opportunities.

Competitive dynamics feature intense competition among domestic players, with companies pursuing differentiation strategies through technological innovation, vertical integration, and customer relationship development. The market is experiencing consolidation as larger companies acquire smaller specialized firms to enhance their capabilities and market position.

Supply chain dynamics emphasize the importance of securing reliable access to raw materials while developing domestic processing capabilities. Chinese companies are implementing comprehensive supply chain strategies including overseas investments, long-term supply agreements, and strategic partnerships with mining companies.

Innovation dynamics focus on developing advanced materials with improved performance characteristics, reduced environmental impact, and lower production costs. The market benefits from substantial research and development investments and collaboration between industry, academia, and government research institutions.

Research methodology for analyzing the China electric vehicle battery materials market employs a comprehensive approach combining primary and secondary research techniques to ensure accurate and reliable market insights. The methodology incorporates quantitative analysis of market data, qualitative assessment of industry trends, and expert interviews with key market participants.

Primary research includes structured interviews with industry executives, technical experts, and government officials involved in policy development and implementation. Survey data collection from material suppliers, battery manufacturers, and automotive companies provides insights into market dynamics, competitive positioning, and future growth expectations.

Secondary research encompasses analysis of industry reports, government publications, company financial statements, and technical literature to understand market structure, technological developments, and regulatory frameworks. Data validation through multiple sources ensures accuracy and reliability of market assessments.

Analytical framework incorporates market sizing methodologies, competitive analysis techniques, and trend identification processes to develop comprehensive market insights. The research approach considers both quantitative metrics and qualitative factors that influence market development and competitive dynamics.

Regional analysis reveals that China’s electric vehicle battery materials market demonstrates significant geographic concentration in key industrial regions, with Eastern China accounting for 45% of production capacity due to established manufacturing infrastructure and proximity to major automotive production centers.

Yangtze River Delta region, including Shanghai, Jiangsu, and Zhejiang provinces, serves as a major hub for battery material production and research activities. The region benefits from advanced manufacturing capabilities, skilled workforce, and strong government support for new energy industries.

Pearl River Delta region in Guangdong province represents another significant cluster for battery materials, particularly for companies serving the consumer electronics and automotive markets. The region’s proximity to Hong Kong and established export infrastructure supports international market access.

Central and Western regions are experiencing increased investment in battery material production facilities, driven by lower operating costs, government incentives, and proximity to raw material sources. These regions account for approximately 30% of total production capacity and are expected to grow rapidly.

Northeastern China maintains importance in certain specialized materials and benefits from established chemical industry infrastructure. The region is focusing on upgrading existing facilities and developing advanced material processing capabilities.

Competitive landscape in China’s electric vehicle battery materials market features a diverse mix of established chemical companies, specialized material suppliers, and vertically integrated battery manufacturers. The market demonstrates high concentration among leading players who have achieved significant scale and technological capabilities.

Strategic positioning among competitors emphasizes technological differentiation, supply chain control, and customer relationship development. Companies are pursuing various growth strategies including capacity expansion, international acquisitions, and research and development investments.

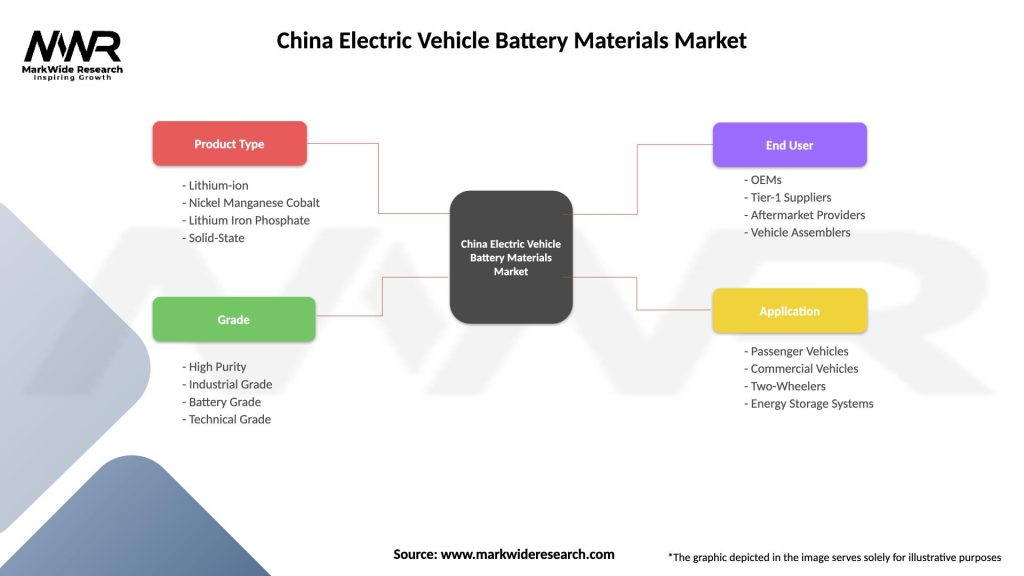

Market segmentation analysis reveals distinct categories based on material type, application, and end-user requirements within China’s electric vehicle battery materials sector.

By Material Type:

By Application:

By End-User:

Cathode materials represent the largest segment within China’s electric vehicle battery materials market, with lithium iron phosphate accounting for 55% of domestic production due to its cost-effectiveness and safety characteristics. NCM materials are gaining market share in premium applications requiring higher energy density.

Anode materials demonstrate steady demand growth, with natural graphite maintaining dominance while synthetic graphite and silicon-based alternatives gain traction in high-performance applications. Chinese companies are investing in advanced processing technologies to improve material purity and performance characteristics.

Electrolyte materials show strong growth potential as battery manufacturers focus on improving safety, performance, and temperature stability. The development of solid-state electrolytes represents a significant opportunity for technological advancement and market differentiation.

Separator materials benefit from increasing quality requirements and safety standards in battery applications. Chinese manufacturers are developing advanced coating technologies and specialized membrane structures to enhance battery performance and safety.

Recycling materials emerge as an important category as the volume of end-of-life batteries increases. Companies developing efficient recovery processes for lithium, cobalt, and nickel are creating new revenue streams while addressing sustainability concerns.

Industry participants in China’s electric vehicle battery materials market benefit from substantial growth opportunities driven by the country’s leadership in electric vehicle adoption and manufacturing. Companies can leverage China’s integrated supply chains, manufacturing scale, and cost advantages to achieve competitive positioning in global markets.

Material suppliers benefit from long-term demand visibility and stable customer relationships as automotive OEMs and battery manufacturers seek reliable supply partners. The market offers opportunities for premium pricing through technological differentiation and quality enhancement initiatives.

Technology developers can access substantial research and development resources, government support programs, and collaboration opportunities with leading industry players. The market provides platforms for commercializing innovative materials and processing technologies.

Investors benefit from exposure to high-growth market segments with strong government policy support and increasing global demand. The market offers diverse investment opportunities across the value chain from raw materials to advanced processing technologies.

End-users including automotive manufacturers benefit from access to high-quality materials at competitive prices, enabling the development of cost-effective electric vehicle solutions. The market provides supply chain security and technological advancement opportunities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key market trends shaping China’s electric vehicle battery materials sector include the accelerating shift toward lithium iron phosphate (LFP) chemistry in cost-sensitive applications, with LFP adoption increasing by 35% annually in domestic electric vehicle production due to improved safety characteristics and cost advantages.

Vertical integration represents a dominant trend as companies seek to control entire value chains from raw material processing to battery cell production. This strategy enables better quality control, cost optimization, and supply chain security while reducing dependence on external suppliers.

Sustainability focus is driving investments in cleaner production technologies, renewable energy adoption, and circular economy solutions. Companies are developing comprehensive environmental strategies to address regulatory requirements and customer expectations for sustainable materials.

Technological advancement continues with emphasis on developing high-performance materials for next-generation batteries including solid-state electrolytes, silicon-based anodes, and advanced cathode chemistries. Research and development investments are accelerating to maintain technological leadership.

Global supply chain diversification efforts are expanding as Chinese companies establish international operations, secure overseas raw material sources, and develop regional production capabilities to serve global markets and reduce geopolitical risks.

Recent industry developments highlight the dynamic nature of China’s electric vehicle battery materials market, with major companies announcing substantial capacity expansion projects and strategic partnerships to meet growing demand and enhance competitive positioning.

Capacity expansion initiatives include significant investments in new production facilities for cathode materials, with several leading companies announcing plans to double their manufacturing capacity over the next three years. These expansions focus on both domestic market growth and export opportunities.

Technology partnerships between Chinese companies and international automotive manufacturers are accelerating, with joint development programs focusing on customized material solutions for specific vehicle platforms and performance requirements. These collaborations enhance market access and technological capabilities.

Recycling infrastructure development represents a major industry focus, with MarkWide Research indicating that leading companies are establishing comprehensive battery recycling networks to recover valuable materials and support circular economy objectives.

International acquisitions by Chinese companies continue to expand, with strategic investments in overseas mining operations, processing facilities, and technology companies to secure supply chain control and enhance global market presence.

Analyst recommendations for stakeholders in China’s electric vehicle battery materials market emphasize the importance of developing comprehensive supply chain strategies that balance cost optimization with supply security and sustainability requirements.

Investment priorities should focus on technological innovation, particularly in next-generation materials and processing technologies that offer competitive advantages and market differentiation opportunities. Companies should allocate resources to research and development programs that address emerging market needs.

Strategic partnerships with international companies, research institutions, and government agencies can enhance market access, technological capabilities, and regulatory compliance. These collaborations are essential for companies seeking to expand globally and maintain competitive positioning.

Sustainability initiatives require immediate attention as environmental regulations tighten and customer expectations evolve. Companies should implement comprehensive environmental management systems and invest in cleaner production technologies to ensure long-term viability.

Market diversification strategies should consider applications beyond automotive markets, including energy storage systems, consumer electronics, and industrial applications. This diversification can reduce market concentration risks and create additional revenue streams.

Future outlook for China’s electric vehicle battery materials market remains highly positive, with continued strong growth expected across all major material categories. The market is projected to maintain robust expansion with annual growth rates exceeding 18% through 2030, driven by accelerating electric vehicle adoption and expanding energy storage applications.

Technological evolution will continue to drive market development, with next-generation materials including solid-state electrolytes and advanced cathode chemistries expected to gain commercial traction within the next five years. These technologies will create new market opportunities and competitive dynamics.

Global market integration is expected to accelerate as Chinese companies establish international operations and serve growing global demand for battery materials. According to MWR projections, Chinese companies will maintain their dominant position while expanding their global market presence significantly.

Sustainability requirements will become increasingly important, with circular economy solutions and environmental performance becoming key competitive differentiators. Companies investing in sustainable technologies and practices will be best positioned for long-term success.

Market consolidation is likely to continue as larger companies acquire specialized firms and smaller players to enhance their capabilities and market position. This consolidation will create stronger, more integrated companies capable of competing effectively in global markets.

China’s electric vehicle battery materials market represents a critical component of the global transition to electric mobility, with the country maintaining dominant positions across key material categories and supply chain segments. The market benefits from comprehensive government support, substantial private sector investments, and China’s strategic focus on achieving leadership in new energy technologies.

Market fundamentals remain strong, with robust demand growth driven by accelerating electric vehicle adoption, expanding energy storage applications, and increasing global recognition of Chinese companies’ technological capabilities and cost competitiveness. The market’s integrated supply chains and manufacturing scale provide sustainable competitive advantages.

Future success in this market will depend on companies’ ability to balance growth opportunities with sustainability requirements, technological innovation with cost optimization, and domestic market leadership with global expansion strategies. Companies that can effectively navigate these challenges while maintaining quality and reliability standards will be best positioned for long-term success in China’s dynamic electric vehicle battery materials market.

What is Electric Vehicle Battery Materials?

Electric Vehicle Battery Materials refer to the various components and substances used in the production of batteries for electric vehicles, including lithium, cobalt, nickel, and graphite. These materials are essential for enhancing battery performance, energy density, and longevity.

What are the key players in the China Electric Vehicle Battery Materials Market?

Key players in the China Electric Vehicle Battery Materials Market include CATL, BYD, and LG Chem, which are known for their significant contributions to battery technology and production. These companies focus on innovation and supply chain efficiency to meet the growing demand for electric vehicles.

What are the growth factors driving the China Electric Vehicle Battery Materials Market?

The growth of the China Electric Vehicle Battery Materials Market is driven by increasing government support for electric vehicles, rising consumer demand for sustainable transportation, and advancements in battery technology. Additionally, the push for reduced carbon emissions is propelling investments in battery materials.

What challenges does the China Electric Vehicle Battery Materials Market face?

The China Electric Vehicle Battery Materials Market faces challenges such as supply chain disruptions, fluctuating raw material prices, and environmental concerns related to mining and processing. These factors can impact the availability and cost of essential battery materials.

What opportunities exist in the China Electric Vehicle Battery Materials Market?

Opportunities in the China Electric Vehicle Battery Materials Market include the development of new recycling technologies for battery materials, the exploration of alternative materials to reduce reliance on scarce resources, and the expansion of partnerships between manufacturers and technology firms to enhance battery performance.

What trends are shaping the China Electric Vehicle Battery Materials Market?

Trends shaping the China Electric Vehicle Battery Materials Market include the increasing adoption of solid-state batteries, advancements in battery management systems, and a growing focus on sustainability and circular economy practices. These trends are influencing how materials are sourced, used, and recycled.

China Electric Vehicle Battery Materials Market

| Segmentation Details | Description |

|---|---|

| Product Type | Lithium-ion, Nickel Manganese Cobalt, Lithium Iron Phosphate, Solid-State |

| Grade | High Purity, Industrial Grade, Battery Grade, Technical Grade |

| End User | OEMs, Tier-1 Suppliers, Aftermarket Providers, Vehicle Assemblers |

| Application | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Energy Storage Systems |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the China Electric Vehicle Battery Materials Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.