444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The China discrete semiconductors market represents one of the most dynamic and rapidly evolving segments within the global semiconductor industry. Discrete semiconductors, including diodes, transistors, thyristors, and rectifiers, serve as fundamental building blocks for electronic devices and systems across numerous applications. China’s position as a manufacturing powerhouse and technology innovation hub has positioned the country at the forefront of discrete semiconductor development and consumption.

Market dynamics in China reflect the nation’s strategic emphasis on semiconductor self-sufficiency and technological advancement. The market demonstrates robust growth driven by expanding applications in automotive electronics, consumer devices, industrial automation, and renewable energy systems. With the government’s strong support for domestic semiconductor manufacturing and the “Made in China 2025” initiative, the discrete semiconductors sector continues to experience significant expansion at a compound annual growth rate (CAGR) of 8.2% through the forecast period.

Manufacturing capabilities within China have evolved substantially, with domestic companies increasingly competing with international players in terms of quality, innovation, and cost-effectiveness. The market encompasses both high-volume commodity products and specialized discrete semiconductors for emerging applications such as electric vehicles, 5G infrastructure, and Internet of Things (IoT) devices.

The China discrete semiconductors market refers to the comprehensive ecosystem encompassing the design, manufacturing, distribution, and application of individual semiconductor components within the Chinese territory. Discrete semiconductors are single-function electronic components that perform specific electrical functions, contrasting with integrated circuits that combine multiple functions on a single chip.

Key components within this market include power diodes for rectification applications, bipolar junction transistors (BJTs) for amplification, field-effect transistors (FETs) for switching operations, and specialized devices such as insulated-gate bipolar transistors (IGBTs) for high-power applications. These components serve as essential elements in virtually every electronic system, from simple consumer gadgets to complex industrial machinery.

Market scope extends beyond mere component supply to encompass research and development activities, manufacturing infrastructure, supply chain management, and end-user applications across diverse industries. The Chinese market’s significance stems from its dual role as both a major consumer and increasingly important producer of discrete semiconductor devices.

Strategic positioning of China’s discrete semiconductors market reflects the country’s broader semiconductor industry ambitions and technological sovereignty goals. The market demonstrates exceptional resilience and growth potential, supported by strong domestic demand and expanding manufacturing capabilities. Government initiatives continue to provide substantial support for industry development through funding, policy incentives, and infrastructure investments.

Market leaders include both established international companies with significant Chinese operations and emerging domestic players gaining market share through innovation and competitive pricing. The competitive landscape shows increasing consolidation as companies seek to achieve economies of scale and technological differentiation. Technology advancement remains a critical success factor, with companies investing heavily in next-generation discrete semiconductor technologies.

Application diversity across automotive, industrial, consumer electronics, and telecommunications sectors provides market stability and growth opportunities. The automotive segment, particularly electric vehicles, represents the fastest-growing application area with adoption rates increasing by 35% annually. MarkWide Research analysis indicates that power management applications account for the largest market segment, driven by increasing energy efficiency requirements across industries.

Fundamental market drivers shaping China’s discrete semiconductors landscape include technological innovation, regulatory support, and evolving end-user requirements. The following insights highlight critical market dynamics:

Primary growth drivers propelling China’s discrete semiconductors market include both macroeconomic factors and industry-specific developments. Government policy support through the National Integrated Circuit Industry Development Guidelines provides substantial financial incentives and strategic direction for industry growth.

Automotive electrification represents the most significant demand driver, with electric vehicle production requiring substantially more discrete semiconductors than traditional internal combustion engine vehicles. Power electronics for battery management, motor control, and charging systems create substantial opportunities for discrete semiconductor suppliers. The automotive segment demonstrates growth rates exceeding 25% annually.

Industrial automation and Industry 4.0 initiatives drive demand for discrete semiconductors in motor drives, power supplies, and control systems. Smart manufacturing implementations require sophisticated power management and signal processing capabilities, creating opportunities for advanced discrete semiconductor solutions.

Consumer electronics continue to represent a substantial market driver, with smartphones, tablets, and smart home devices requiring various discrete semiconductors for power management, signal processing, and connectivity functions. 5G technology deployment creates additional demand for radio frequency (RF) discrete semiconductors and power amplifiers.

Renewable energy infrastructure development, including solar and wind power systems, requires specialized discrete semiconductors for power conversion and grid integration applications. Energy storage systems represent another growing application area requiring advanced power management semiconductors.

Significant challenges facing China’s discrete semiconductors market include technological gaps, supply chain vulnerabilities, and competitive pressures. Technology limitations in certain advanced discrete semiconductor categories continue to create dependencies on international suppliers, particularly for high-performance applications.

Supply chain disruptions have highlighted vulnerabilities in raw material sourcing and equipment availability. Semiconductor manufacturing equipment remains heavily dependent on international suppliers, creating potential bottlenecks for capacity expansion. Material sourcing challenges, particularly for specialized substrates and chemicals, can impact production continuity.

Intellectual property concerns and technology transfer restrictions limit access to certain advanced technologies and manufacturing processes. International trade tensions create uncertainty and potential barriers to technology acquisition and market access.

Quality perception challenges persist for some Chinese discrete semiconductor manufacturers, particularly in high-reliability applications such as aerospace and medical devices. Certification requirements and lengthy qualification processes can delay market entry for new products and suppliers.

Price competition intensifies as more manufacturers enter the market, potentially impacting profitability and investment capacity for research and development activities. Overcapacity concerns in certain discrete semiconductor categories may lead to pricing pressures and industry consolidation.

Substantial opportunities exist within China’s discrete semiconductors market, driven by emerging technologies and evolving application requirements. Wide bandgap semiconductors represent a significant growth opportunity, with silicon carbide and gallium nitride devices enabling higher efficiency and performance in power electronics applications.

Electric vehicle market expansion creates substantial opportunities for power discrete semiconductors, including IGBTs, MOSFETs, and specialized automotive-grade devices. Charging infrastructure development requires high-power discrete semiconductors for fast-charging systems and grid integration.

Data center growth driven by cloud computing and artificial intelligence applications creates demand for efficient power management semiconductors. Server power supplies and voltage regulation modules require advanced discrete semiconductors for optimal performance and energy efficiency.

Internet of Things device proliferation creates opportunities for low-power discrete semiconductors optimized for battery-operated applications. Smart city initiatives and infrastructure modernization projects require various discrete semiconductors for sensing, communication, and control functions.

Export opportunities continue to expand as Chinese discrete semiconductor manufacturers improve quality and cost competitiveness. Belt and Road Initiative countries represent potential markets for Chinese discrete semiconductor products and technologies.

Complex interactions between supply and demand factors, technological developments, and regulatory influences shape China’s discrete semiconductors market dynamics. Demand patterns reflect the country’s industrial structure and economic development priorities, with strong growth in high-technology sectors driving premium product demand.

Supply dynamics show increasing domestic production capabilities alongside continued reliance on international suppliers for certain specialized components. Manufacturing capacity expansion continues through both greenfield investments and facility upgrades, with companies achieving production efficiency improvements of 18% through automation and process optimization.

Technology evolution drives market dynamics as new discrete semiconductor technologies enable improved performance and new applications. Product lifecycle management becomes increasingly important as technology advancement accelerates and customer requirements evolve rapidly.

Competitive dynamics intensify as domestic and international companies compete for market share through innovation, cost reduction, and customer service excellence. Partnership strategies become crucial for accessing complementary technologies and market channels.

Regulatory influences continue to shape market dynamics through environmental regulations, quality standards, and trade policies. Sustainability requirements drive demand for energy-efficient discrete semiconductors and environmentally friendly manufacturing processes.

Comprehensive research approach employed for analyzing China’s discrete semiconductors market combines primary and secondary research methodologies to ensure accuracy and completeness. Primary research includes extensive interviews with industry executives, technology experts, and end-users across various application segments.

Secondary research encompasses analysis of industry reports, company financial statements, patent filings, and regulatory documents. Market data validation occurs through cross-referencing multiple sources and expert verification to ensure reliability and accuracy.

Quantitative analysis utilizes statistical modeling and forecasting techniques to project market trends and growth patterns. Qualitative insights provide context and explanation for quantitative findings through expert interviews and industry analysis.

Technology assessment includes evaluation of current and emerging discrete semiconductor technologies, manufacturing processes, and application requirements. Competitive analysis examines market positioning, strategic initiatives, and performance metrics of key industry participants.

Regional analysis considers geographic variations in demand patterns, manufacturing capabilities, and regulatory environments across different Chinese provinces and municipalities. End-user analysis provides insights into application-specific requirements and growth drivers across various industry sectors.

Geographic distribution of China’s discrete semiconductors market reflects the country’s industrial concentration patterns and regional development strategies. Eastern coastal regions dominate both production and consumption, with Jiangsu, Guangdong, and Shanghai provinces leading in manufacturing capabilities and market activity.

Yangtze River Delta region accounts for approximately 38% of national production capacity, benefiting from established industrial infrastructure, skilled workforce, and proximity to major end-user markets. Shanghai serves as a major hub for discrete semiconductor design and advanced manufacturing, hosting numerous domestic and international companies.

Pearl River Delta region, centered around Shenzhen and Guangzhou, represents a significant consumer electronics manufacturing cluster driving discrete semiconductor demand. Supply chain integration in this region enables efficient component sourcing and rapid product development cycles.

Beijing-Tianjin-Hebei region focuses on research and development activities, hosting major universities and research institutions contributing to discrete semiconductor innovation. Government support for high-technology industries in this region creates favorable conditions for advanced discrete semiconductor development.

Central and western regions show increasing importance as manufacturing costs rise in coastal areas and government policies encourage inland development. Chengdu and Xi’an emerge as important secondary manufacturing hubs with growing discrete semiconductor capabilities.

Market competition in China’s discrete semiconductors sector involves both established international players and rapidly growing domestic companies. Competitive positioning varies significantly across different product categories and application segments.

Leading companies in the Chinese discrete semiconductors market include:

Competitive strategies focus on technology innovation, cost optimization, and customer service excellence. Market differentiation occurs through specialized product offerings, application-specific solutions, and superior technical support capabilities.

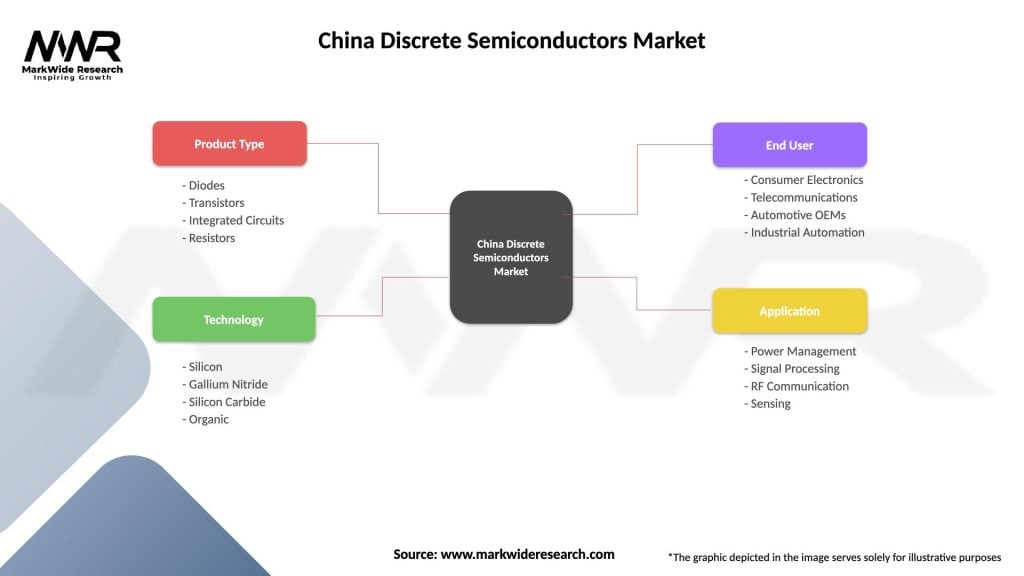

Market segmentation of China’s discrete semiconductors market occurs across multiple dimensions, including product type, application, and end-user industry. Product segmentation represents the primary classification method for market analysis and strategic planning.

By Product Type:

By Application:

Power discrete semiconductors represent the largest and fastest-growing category within China’s discrete semiconductors market. MOSFET devices dominate this segment, accounting for 45% of power discrete semiconductor consumption due to their efficiency advantages and versatile applications across multiple industries.

Automotive applications drive significant growth in power discrete semiconductors, particularly for electric vehicle powertrains and charging systems. Silicon carbide (SiC) devices gain increasing adoption in high-performance automotive applications despite higher costs, offering superior efficiency and thermal performance.

Signal discrete semiconductors maintain steady demand from consumer electronics and telecommunications applications. RF discrete semiconductors experience strong growth driven by 5G infrastructure deployment and expanding wireless communication requirements.

Standard discrete semiconductors face intense price competition but maintain substantial volume demand from cost-sensitive applications. Chinese manufacturers achieve strong competitive positions in this category through cost optimization and manufacturing scale advantages.

Specialty discrete semiconductors for niche applications offer higher margins and growth potential. Automotive-grade devices require extensive qualification processes but provide stable, long-term revenue opportunities for qualified suppliers.

Substantial benefits accrue to various stakeholders participating in China’s discrete semiconductors market ecosystem. Manufacturers benefit from access to the world’s largest electronics manufacturing base and rapidly growing domestic demand across multiple application segments.

Technology companies gain opportunities to leverage China’s extensive research and development capabilities, skilled workforce, and government support for innovation activities. Cost advantages in manufacturing and assembly operations enable competitive positioning in global markets.

End-users benefit from improved product availability, competitive pricing, and localized technical support services. Supply chain proximity reduces logistics costs and enables faster response to changing requirements and market conditions.

Investors find attractive opportunities in a rapidly growing market supported by favorable government policies and strong fundamental demand drivers. Market diversification across multiple application segments provides risk mitigation and growth stability.

Research institutions benefit from industry collaboration opportunities, funding support, and access to practical application challenges driving innovation requirements. Talent development programs create career opportunities for engineers and researchers in semiconductor technologies.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends shaping China’s discrete semiconductors market reflect broader technological and economic developments. Wide bandgap semiconductor adoption accelerates as applications requiring higher efficiency and performance drive demand for silicon carbide and gallium nitride devices.

Automotive electrification continues as the dominant trend, with electric vehicle production driving unprecedented demand for power discrete semiconductors. Battery management systems and motor control applications require increasingly sophisticated discrete semiconductor solutions with efficiency improvements of 15-20% compared to traditional technologies.

Industry 4.0 implementation drives demand for discrete semiconductors in industrial automation applications. Smart manufacturing systems require advanced power management and control capabilities, creating opportunities for specialized discrete semiconductor solutions.

Sustainability focus influences product development and manufacturing processes, with companies investing in energy-efficient discrete semiconductors and environmentally friendly production methods. Circular economy principles drive initiatives for semiconductor recycling and material recovery.

Supply chain localization accelerates as companies seek to reduce dependencies and improve resilience. Domestic sourcing preferences increase, creating opportunities for Chinese discrete semiconductor manufacturers to capture market share from international suppliers.

Significant developments within China’s discrete semiconductors industry demonstrate the sector’s dynamic evolution and strategic importance. Manufacturing capacity expansion continues through major investments in new fabrication facilities and equipment upgrades by both domestic and international companies.

Technology partnerships between Chinese companies and international technology leaders facilitate knowledge transfer and capability development. Joint ventures and strategic alliances enable access to advanced technologies while supporting market expansion objectives.

Research and development investments reach record levels as companies compete for technological leadership in emerging discrete semiconductor categories. MWR data indicates that leading companies allocate 12-15% of revenue to innovation activities, focusing on wide bandgap semiconductors and advanced packaging technologies.

Acquisition activity increases as companies seek to acquire complementary technologies, manufacturing capabilities, and market access. Industry consolidation continues as smaller companies merge with larger players to achieve scale advantages and technological capabilities.

Government initiatives provide substantial support through the National Integrated Circuit Industry Development Fund and various provincial-level incentive programs. Policy support includes tax incentives, research grants, and infrastructure development funding for semiconductor manufacturing facilities.

Strategic recommendations for stakeholders in China’s discrete semiconductors market emphasize the importance of technology advancement, market diversification, and supply chain optimization. Investment priorities should focus on emerging technologies such as wide bandgap semiconductors and advanced packaging solutions.

Market positioning strategies should emphasize differentiation through specialized applications and superior customer service rather than competing solely on price. Quality improvement initiatives remain crucial for establishing credibility in high-reliability applications and premium market segments.

Partnership development with automotive OEMs and Tier 1 suppliers provides access to the rapidly growing electric vehicle market. Long-term relationships with key customers enable collaborative product development and secure revenue streams.

Supply chain diversification reduces risks associated with single-source dependencies and geopolitical uncertainties. Domestic sourcing development should balance cost considerations with quality and reliability requirements.

Talent acquisition and development programs ensure access to skilled engineers and researchers necessary for technology advancement and innovation activities. University partnerships provide access to emerging talent and research capabilities.

Long-term prospects for China’s discrete semiconductors market remain highly positive, supported by strong fundamental demand drivers and continued government support for industry development. Market expansion is expected to continue at robust growth rates, with the automotive and industrial segments leading demand growth.

Technology evolution will drive market transformation as wide bandgap semiconductors gain broader adoption and new applications emerge. Silicon carbide and gallium nitride devices are projected to achieve market penetration rates of 25-30% in high-performance applications by 2030.

Manufacturing capabilities will continue expanding through both capacity increases and technology upgrades. Domestic production is expected to achieve greater self-sufficiency in standard discrete semiconductors while building capabilities in advanced technologies.

Export opportunities will expand as Chinese discrete semiconductor manufacturers improve quality and cost competitiveness. MarkWide Research projections indicate that Chinese companies could achieve 20-25% global market share in certain discrete semiconductor categories within the next decade.

Sustainability initiatives will become increasingly important as environmental regulations tighten and customer requirements evolve. Energy-efficient products and environmentally friendly manufacturing processes will provide competitive advantages in global markets.

China’s discrete semiconductors market represents a dynamic and rapidly evolving sector with substantial growth potential and strategic importance for the global semiconductor industry. Strong fundamentals including robust domestic demand, expanding manufacturing capabilities, and supportive government policies create favorable conditions for continued market expansion.

Key success factors for market participants include technology innovation, quality improvement, and strategic positioning in high-growth application segments such as automotive electronics and industrial automation. Market opportunities in emerging technologies like wide bandgap semiconductors and specialized applications provide pathways for differentiation and premium positioning.

Challenges remain in areas such as technology gaps, supply chain dependencies, and competitive pressures, but these are being addressed through increased investment, strategic partnerships, and government support initiatives. Industry consolidation and capability building continue to strengthen the competitive position of Chinese discrete semiconductor companies.

Future outlook remains highly positive, with continued growth expected across multiple application segments and geographic markets. Strategic focus on innovation, quality, and customer service will determine long-term success in this competitive and rapidly evolving market environment. The China discrete semiconductors market is well-positioned to play an increasingly important role in the global semiconductor ecosystem while supporting the country’s broader technology advancement and economic development objectives.

What is Discrete Semiconductors?

Discrete semiconductors are individual semiconductor devices that perform specific functions, such as rectification, amplification, or switching. They are essential components in various electronic applications, including consumer electronics, automotive systems, and industrial machinery.

What are the key players in the China Discrete Semiconductors Market?

Key players in the China Discrete Semiconductors Market include companies like ON Semiconductor, Infineon Technologies, and STMicroelectronics, which are known for their innovative products and extensive market reach, among others.

What are the growth factors driving the China Discrete Semiconductors Market?

The growth of the China Discrete Semiconductors Market is driven by the increasing demand for consumer electronics, the rise of electric vehicles, and advancements in industrial automation technologies. These factors contribute to a robust market environment for discrete semiconductor applications.

What challenges does the China Discrete Semiconductors Market face?

The China Discrete Semiconductors Market faces challenges such as supply chain disruptions, fluctuating raw material prices, and intense competition among manufacturers. These factors can impact production efficiency and market stability.

What opportunities exist in the China Discrete Semiconductors Market?

Opportunities in the China Discrete Semiconductors Market include the growing adoption of renewable energy technologies, the expansion of the Internet of Things (IoT), and the increasing integration of smart technologies in various sectors. These trends are expected to enhance market growth.

What trends are shaping the China Discrete Semiconductors Market?

Trends shaping the China Discrete Semiconductors Market include the shift towards energy-efficient devices, the development of advanced packaging technologies, and the increasing focus on miniaturization of electronic components. These trends are influencing product design and manufacturing processes.

China Discrete Semiconductors Market

| Segmentation Details | Description |

|---|---|

| Product Type | Diodes, Transistors, Integrated Circuits, Resistors |

| Technology | Silicon, Gallium Nitride, Silicon Carbide, Organic |

| End User | Consumer Electronics, Telecommunications, Automotive OEMs, Industrial Automation |

| Application | Power Management, Signal Processing, RF Communication, Sensing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the China Discrete Semiconductors Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.