The business income insurance market in China serves as a critical component of risk management strategies for businesses across various sectors. This insurance product provides financial protection to companies against income loss resulting from unexpected disruptions to their operations, such as natural disasters, fires, or other covered perils. As China’s economy continues to grow and businesses face increasing risks and uncertainties, the demand for business income insurance has been on the rise, driving market expansion and innovation in the insurance sector.

Meaning

Business income insurance, also known as business interruption insurance, is designed to safeguard companies from financial losses incurred due to interruptions in their normal business operations. This type of insurance typically covers lost revenue, ongoing expenses, and additional costs incurred during the period of restoration following a covered incident. By providing financial stability during times of crisis, business income insurance enables companies in China to mitigate the impact of unforeseen events and maintain business continuity.

Executive Summary

The business income insurance market in China is witnessing robust growth, driven by increasing awareness of risk management practices among businesses, regulatory reforms aimed at strengthening insurance penetration, and the growing recognition of the importance of business continuity planning. With the support of insurers, brokers, and government initiatives, the market is poised for further expansion, offering opportunities for insurers to innovate products, enhance service offerings, and cater to the evolving needs of businesses across different industries.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Risk Awareness: Businesses in China are becoming increasingly aware of the importance of risk management and business continuity planning, driving demand for business income insurance as a key risk mitigation tool.

Regulatory Support: Regulatory reforms aimed at promoting insurance penetration and enhancing risk management practices in China have created a conducive environment for the growth of the business income insurance market.

Industry Collaboration: Collaboration between insurers, brokers, risk management professionals, and government agencies is facilitating knowledge sharing, best practices, and innovation in the business income insurance market in China.

Digital Transformation: The adoption of digital technologies, such as artificial intelligence, data analytics, and blockchain, is transforming the insurance industry in China, enabling insurers to improve operational efficiency, enhance customer experience, and offer innovative insurance solutions.

Market Drivers

Economic Growth and Development: China’s rapid economic growth and industrial development have led to increased demand for business income insurance among companies seeking financial protection against operational disruptions and revenue losses.

Regulatory Requirements: Regulatory mandates and industry standards requiring businesses to have adequate insurance coverage, including business income insurance, have driven market growth and compliance efforts among businesses in China.

Increasing Business Risks: The growing complexity of business risks, including natural disasters, cyber threats, supply chain disruptions, and regulatory changes, has heightened the need for comprehensive risk management solutions, including business income insurance, in China.

Globalization and Supply Chain Interdependencies: China’s integration into the global economy and its role as a key manufacturing and trading hub have exposed businesses to supply chain risks, making business income insurance essential for managing supply chain disruptions and mitigating financial losses.

Market Restraints

Underinsurance: Despite the growing awareness of risk management, many businesses in China remain underinsured or lack adequate coverage for business income losses, highlighting the need for education, awareness campaigns, and risk assessment services.

Affordability Concerns: Affordability constraints and budgetary considerations may deter some businesses, particularly small and medium-sized enterprises (SMEs), from purchasing comprehensive business income insurance coverage, limiting market penetration and growth potential.

Data Privacy and Security Risks: Concerns about data privacy, cybersecurity, and information security may deter businesses from sharing sensitive information with insurers or adopting digital solutions, posing challenges for insurers in underwriting and pricing business income insurance policies.

Complexity of Claims Processing: The complexity of claims processing, valuation methods, and coverage determinations for business income insurance policies can lead to disputes, delays, and challenges in claims settlement, impacting customer satisfaction and insurer profitability.

Market Opportunities

Product Innovation: Insurers in China have opportunities to innovate and diversify their product offerings by developing customized business income insurance solutions tailored to the unique needs of different industries, business sectors, and risk profiles.

Digital Transformation: The adoption of digital technologies, such as online platforms, mobile applications, and data analytics tools, presents opportunities for insurers to streamline underwriting, claims processing, and customer interactions, enhancing efficiency and service quality.

Risk Management Services: Insurers can differentiate themselves by offering value-added risk management services, such as risk assessments, loss prevention programs, and business continuity planning, to help businesses identify, mitigate, and transfer risks more effectively.

Market Education and Awareness: Education and awareness initiatives aimed at promoting the importance of business income insurance, risk management best practices, and disaster preparedness can create opportunities for insurers to expand market reach and increase insurance penetration among businesses in China.

Market Dynamics

The business income insurance market in China operates in a dynamic environment shaped by factors such as economic trends, regulatory developments, technological advancements, and industry dynamics. These dynamics influence market growth, competition, product innovation, and customer preferences, requiring insurers to adapt their strategies and offerings to meet evolving market demands and opportunities.

Regional Analysis

The business income insurance market in China exhibits regional variations in terms of market maturity, industry composition, regulatory environment, and risk profiles. Key regions, such as Guangdong, Shanghai, Beijing, and Jiangsu, with concentrations of manufacturing, financial services, technology, and commercial activities, present significant opportunities for insurers to expand their presence and market share.

Competitive Landscape

Leading Companies in China Business Income Insurance Market:

Ping An Insurance (Group) Company of China, Ltd.

China Life Insurance Company Limited

China Pacific Insurance (Group) Co., Ltd.

PICC Property and Casualty Company Limited

People’s Insurance Company of China Limited

China Taiping Insurance Group Ltd.

China Continent Property & Casualty Insurance Co., Ltd.

China Reinsurance (Group) Corporation

Sunshine Property and Casualty Insurance Co., Ltd.

Huatai Insurance Group Co., Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

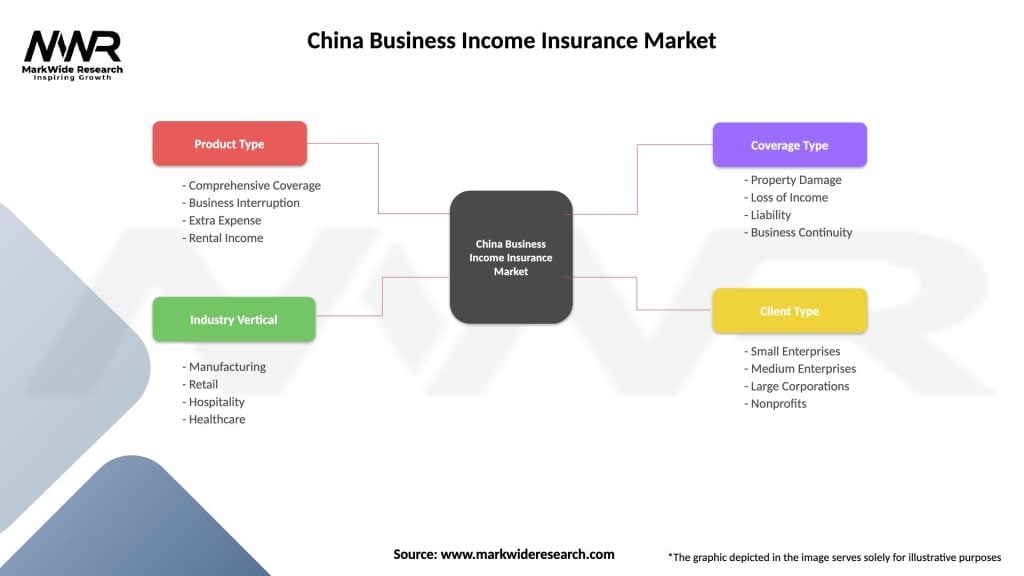

The business income insurance market in China can be segmented based on various factors, including industry verticals, business sizes, geographic regions, coverage types, and policy features. Segmenting the market enables insurers to target specific customer segments, customize insurance solutions, and optimize distribution channels to meet the diverse needs of businesses across different sectors and regions.

Category-wise Insights

Industry Verticals: Business income insurance solutions can be tailored to meet the unique needs of various industry verticals, including manufacturing, retail, hospitality, healthcare, technology, and financial services, providing specialized coverage options and risk management services.

Business Sizes: Insurers offer business income insurance solutions for businesses of all sizes, including small and medium-sized enterprises (SMEs), large corporations, and multinational companies, with flexible coverage limits, deductible options, and premium structures to accommodate different business needs and budgets.

Geographic Regions: Regional variations in economic development, industry composition, regulatory requirements, and risk profiles influence the demand for business income insurance across different provinces, municipalities, and economic zones in China, creating opportunities for insurers to customize products and services for regional markets.

Coverage Types: Business income insurance policies can include various coverage types, such as gross earnings coverage, extra expense coverage, contingent business interruption coverage, civil authority coverage, and extended period of indemnity coverage, depending on the specific risks and exposures faced by businesses in China.

Key Benefits for Industry Participants and Stakeholders

The adoption of business income insurance offers several benefits for industry participants and stakeholders in China:

Financial Protection: Business income insurance provides financial protection to businesses against income loss and operational disruptions caused by covered perils, helping them recover and resume normal operations more quickly after a disaster or unforeseen event.

Business Continuity: By mitigating the financial impact of business interruptions, business income insurance helps maintain business continuity, preserve customer relationships, and safeguard long-term viability and competitiveness in the market.

Risk Management: Business income insurance forms an integral part of a comprehensive risk management strategy, enabling businesses to identify, assess, mitigate, and transfer risks more effectively, enhancing resilience and preparedness for future contingencies.

Peace of Mind: Knowing that they have financial protection in place in the event of a business interruption or revenue loss provides business owners and stakeholders with peace of mind, enabling them to focus on core business activities and strategic initiatives with confidence.

SWOT Analysis

A SWOT analysis of the business income insurance market in China provides insights into its strengths, weaknesses, opportunities, and threats:

Strengths:

Strong demand for risk management solutions

Regulatory support for insurance penetration

Growing awareness of business continuity planning

Diverse industry composition and market potential

Weaknesses:

Underinsurance and low insurance penetration rates

Affordability constraints for small businesses

Complexity of claims processing and coverage determinations

Lack of standardized risk assessment practices

Opportunities:

Product innovation and customization

Digital transformation and technology adoption

Market education and awareness initiatives

Collaboration and partnerships with industry stakeholders

Threats:

Economic uncertainties and market volatility

Regulatory changes and compliance requirements

Cybersecurity risks and data privacy concerns

Competition from domestic and international insurers

Understanding these factors through a SWOT analysis helps insurers identify market opportunities, address challenges, and formulate strategies to capitalize on the strengths and opportunities while mitigating risks and threats in the business income insurance market in China.

Market Key Trends

Technology Integration: The integration of digital technologies, such as artificial intelligence, big data analytics, and cloud computing, into business income insurance processes is a key trend, enabling insurers to streamline operations, enhance underwriting efficiency, and improve customer experiences in China’s insurance market.

Product Differentiation: Insurers are differentiating their business income insurance products through innovative coverage options, value-added services, and customized solutions tailored to the unique needs of different industries, businesses, and risk profiles in China.

Risk Mitigation Strategies: Insurers and risk management professionals are collaborating to develop proactive risk mitigation strategies, such as risk assessments, loss prevention programs, and business continuity planning services, to help businesses identify, assess, and manage risks more effectively in China.

Regulatory Compliance: Regulatory compliance requirements, including solvency regulations, capital adequacy standards, and market conduct rules, are driving insurers to enhance compliance frameworks, risk management practices, and governance structures to meet regulatory expectations and maintain market competitiveness in China.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the business income insurance market in China, highlighting the importance of risk management, business continuity planning, and insurance protection for businesses facing unprecedented challenges and uncertainties. Key impacts of COVID-19 on the business income insurance market in China include:

Increased Awareness and Demand: The pandemic has raised awareness of the need for business income insurance coverage among businesses in China, driving increased demand for financial protection against income loss and operational disruptions caused by the pandemic-related closures, restrictions, and supply chain disruptions.

Claims and Losses: Insurers have experienced a surge in claims and losses related to business interruption, contingent business interruption, supply chain disruptions, and other pandemic-related perils, leading to increased scrutiny of policy wordings, coverage interpretations, and claims settlement processes in China.

Digital Transformation: The pandemic has accelerated the adoption of digital technologies, online platforms, and remote service delivery models by insurers and brokers to maintain business operations, enhance customer interactions, and support claims processing and underwriting activities in China’s insurance market.

Regulatory Response: Regulatory authorities have introduced measures to support insurers, policyholders, and the insurance industry during the pandemic, including regulatory relief measures, premium payment extensions, and policyholder assistance programs to help businesses cope with the financial impact of COVID-19 in China.

Key Industry Developments

Digital Innovation: Insurers are investing in digital innovation, technology partnerships, and InsurTech collaborations to enhance product distribution, customer engagement, claims processing, and risk management capabilities in China’s insurance market.

Customer-Centric Solutions: Insurers are focusing on customer-centric solutions, personalized service offerings, and omnichannel distribution strategies to improve customer experiences, increase customer loyalty, and differentiate themselves in the competitive insurance market in China.

Regulatory Compliance: Insurers are enhancing regulatory compliance frameworks, risk management practices, and governance structures to meet evolving regulatory requirements, market standards, and industry best practices in China’s insurance sector.

Sustainability Initiatives: Insurers are integrating environmental, social, and governance (ESG) considerations into their business strategies, product offerings, and investment decisions to support sustainability goals, address climate risks, and promote responsible insurance practices in China.

Analyst Suggestions

Customer-Centric Approach: Insurers should adopt a customer-centric approach, focusing on understanding customer needs, preferences, and pain points, and delivering personalized solutions, seamless experiences, and responsive services to enhance customer satisfaction and loyalty in China’s insurance market.

Digital Transformation: Insurers should accelerate digital transformation initiatives, embrace emerging technologies, and invest in digital capabilities to improve operational efficiency, enhance underwriting accuracy, streamline claims processing, and optimize distribution channels in China’s insurance industry.

Risk Management Partnerships: Insurers should strengthen partnerships with risk management professionals, industry associations, and government agencies to develop proactive risk mitigation strategies, promote best practices, and raise awareness of the importance of risk management and insurance protection among businesses in China.

Sustainable Practices: Insurers should integrate environmental, social, and governance (ESG) considerations into their business strategies, product development processes, and investment decisions to support sustainability goals, address climate risks, and meet evolving regulatory expectations in China’s insurance market.

Future Outlook

The business income insurance market in China is poised for continued growth and innovation, driven by factors such as economic expansion, regulatory reforms, technological advancements, and evolving customer expectations. While challenges such as underinsurance, affordability constraints, and regulatory compliance requirements remain, opportunities for insurers to expand market reach, enhance product offerings, and strengthen customer relationships are abundant. By embracing digital transformation, fostering risk management partnerships, and prioritizing sustainability initiatives, insurers can position themselves for long-term success and leadership in China’s dynamic insurance market.

Conclusion

The business income insurance market in China plays a vital role in protecting businesses against income loss and operational disruptions caused by unforeseen events and disasters. With the growing awareness of risk management, regulatory reforms, and technological advancements, the market presents significant opportunities for insurers to innovate, differentiate, and expand their presence. By focusing on customer needs, embracing digital transformation, and promoting sustainable practices, insurers can build resilience, enhance competitiveness, and contribute to the resilience and growth of China’s economy and business landscape.

What is Business Income Insurance?

Business Income Insurance is a type of coverage that protects businesses from loss of income due to disruptions, such as natural disasters or other unforeseen events. It helps cover operating expenses and lost profits during the period of recovery.

What are the key players in the China Business Income Insurance Market?

Key players in the China Business Income Insurance Market include Ping An Insurance, China Life Insurance, and China Pacific Insurance, among others. These companies offer various insurance products tailored to meet the needs of businesses across different sectors.

What are the main drivers of growth in the China Business Income Insurance Market?

The main drivers of growth in the China Business Income Insurance Market include the increasing awareness of risk management among businesses, the rise in natural disasters, and the expansion of small and medium-sized enterprises seeking financial protection.

What challenges does the China Business Income Insurance Market face?

The China Business Income Insurance Market faces challenges such as regulatory complexities, competition from alternative risk transfer solutions, and the need for better understanding of insurance products among business owners.

What opportunities exist in the China Business Income Insurance Market?

Opportunities in the China Business Income Insurance Market include the potential for product innovation, the growing demand for customized insurance solutions, and the increasing adoption of digital platforms for insurance services.

What trends are shaping the China Business Income Insurance Market?

Trends shaping the China Business Income Insurance Market include the integration of technology in underwriting processes, the rise of parametric insurance products, and a focus on sustainability in insurance offerings.

Leading Companies in China Business Income Insurance Market:

Ping An Insurance (Group) Company of China, Ltd.

China Life Insurance Company Limited

China Pacific Insurance (Group) Co., Ltd.

PICC Property and Casualty Company Limited

People’s Insurance Company of China Limited

China Taiping Insurance Group Ltd.

China Continent Property & Casualty Insurance Co., Ltd.

China Reinsurance (Group) Corporation

Sunshine Property and Casualty Insurance Co., Ltd.

Huatai Insurance Group Co., Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.