444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview:

The China bunker fuel market is a critical component of the nation’s maritime industry. Bunker fuel, also known as marine fuel, plays a vital role in powering ships and vessels. It is a heavy fuel oil derived from crude oil refining processes and is primarily used in large ocean-going ships. As the world’s leading exporter and importer of goods, China’s maritime activities heavily rely on bunker fuel for transportation, making the bunker fuel market an essential aspect of the country’s economic growth.

Meaning:

Bunker fuel is named after the fuel storage areas or “bunkers” on ships where it is stored. It serves as the primary source of power for marine engines and is graded based on its viscosity, sulfur content, and other properties. Bunker fuel is classified into various types, with the most common being IFO (Intermediate Fuel Oil) and MGO (Marine Gas Oil). The choice of bunker fuel depends on the type of vessel and its intended use.

Executive Summary:

The China bunker fuel market has witnessed significant growth over the years, driven by the nation’s booming maritime trade and shipping industry. The market’s outlook remains promising, considering China’s continuous efforts to enhance its maritime infrastructure and trade relations. However, like any other market, the bunker fuel sector also faces challenges and uncertainties. To stay ahead in this competitive landscape, companies need to strategize and adapt to market dynamics efficiently.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Several essential insights shape the China bunker fuel market:

Market Drivers:

Several factors drive the growth of the China bunker fuel market:

Market Restraints:

Certain challenges hinder the China bunker fuel market’s seamless growth:

Market Opportunities:

Amidst the challenges, several opportunities arise for the China bunker fuel market:

Market Dynamics:

The China bunker fuel market operates in a dynamic environment influenced by various factors, including regulatory changes, geopolitical events, and technological advancements. The market’s growth is intricately tied to the country’s maritime trade and shipping industry, with fluctuating demand patterns and emerging fuel preferences shaping its future trajectory. As the industry adapts to changing market dynamics, key players need to stay agile and responsive to remain competitive and sustainable.

Regional Analysis:

China’s bunker fuel market is primarily concentrated in major port cities along its extensive coastline. Ports such as Shanghai, Shenzhen, Ningbo-Zhoushan, and Qingdao play pivotal roles in fuel supply and distribution due to their strategic locations and high maritime traffic. Additionally, the development of the “Greater Bay Area” initiative, encompassing Guangdong, Hong Kong, and Macau, further strengthens the region’s maritime trade and bunker fuel demand.

Competitive Landscape:

Leading Companies in the China Bunker Fuel Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

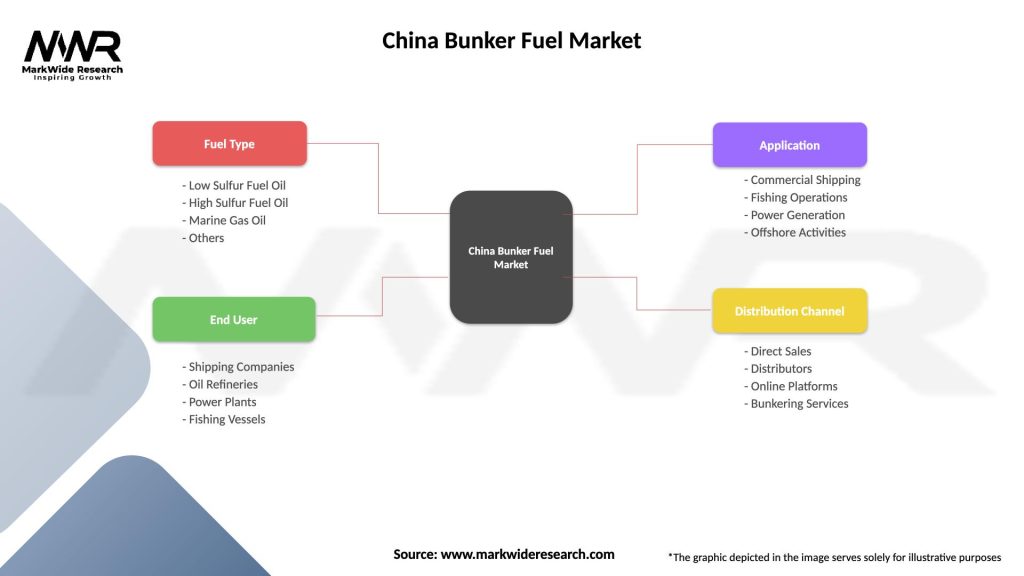

Segmentation:

The China bunker fuel market can be segmented based on fuel type, sulfur content, and end-users. The common segmentation includes:

Category-wise Insights:

Each category in the China bunker fuel market offers unique insights:

Key Benefits for Industry Participants and Stakeholders:

Industry participants and stakeholders can reap several benefits from the China bunker fuel market:

SWOT Analysis:

A SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis of the China bunker fuel market reveals the following:

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends:

Several key trends shape the China bunker fuel market:

Covid-19 Impact:

The Covid-19 pandemic had a substantial impact on the global economy, including the maritime industry. The initial outbreak led to a decline in shipping activity, affecting bunker fuel demand. However, as economies recovered and trade resumed, the demand for bunker fuel rebounded, though the industry had to face challenges related to crew changes, port restrictions, and supply chain disruptions. The pandemic also highlighted the importance of a resilient supply chain and sustainable practices, prompting the industry to adapt and innovate.

Key Industry Developments:

Several notable industry developments have shaped the China bunker fuel market:

Analyst Suggestions: Industry analysts offer the following suggestions for stakeholders in the China bunker fuel market:

Future Outlook:

The future outlook for the China bunker fuel market remains optimistic, driven by the nation’s position as a global trade leader and continuous efforts to enhance its maritime infrastructure. However, the industry must address environmental concerns and adapt to the energy transition towards cleaner fuels. Investments in sustainable practices, technology, and strategic collaborations will play a pivotal role in shaping the industry’s future.

Conclusion:

The China bunker fuel market is a critical component of the nation’s maritime industry, supporting the extensive trade activities that drive the country’s economic growth. While facing challenges related to environmental regulations and volatile crude oil prices, the industry offers ample opportunities for growth and innovation. By embracing sustainable practices, investing in cleaner fuel alternatives, and adapting to market dynamics, industry participants can thrive in this competitive landscape. As China continues to enhance its maritime infrastructure and maintain its position as a global trade giant, the outlook for the bunker fuel market remains promising, making it an attractive prospect for investors and stakeholders alike.

What is Bunker Fuel?

Bunker fuel refers to the fuel used aboard ships, primarily for propulsion and power generation. It is a crucial component in the maritime industry, impacting shipping operations and costs.

What are the key players in the China Bunker Fuel Market?

Key players in the China Bunker Fuel Market include Sinopec, China National Petroleum Corporation, and CNOOC, among others. These companies are involved in the production, distribution, and supply of bunker fuel across various ports in China.

What are the main drivers of the China Bunker Fuel Market?

The main drivers of the China Bunker Fuel Market include the growth of international trade, increasing shipping activities, and the expansion of the maritime logistics sector. Additionally, regulatory changes aimed at reducing emissions are influencing fuel choices.

What challenges does the China Bunker Fuel Market face?

The China Bunker Fuel Market faces challenges such as stringent environmental regulations, fluctuating crude oil prices, and competition from alternative fuels. These factors can impact supply stability and pricing strategies.

What opportunities exist in the China Bunker Fuel Market?

Opportunities in the China Bunker Fuel Market include the development of low-sulfur fuels and the adoption of cleaner technologies. The shift towards sustainable shipping practices is also creating new avenues for growth.

What trends are shaping the China Bunker Fuel Market?

Trends shaping the China Bunker Fuel Market include the increasing use of LNG as a marine fuel, advancements in fuel efficiency technologies, and a growing emphasis on sustainability. These trends are driving innovation and investment in the sector.

China Bunker Fuel Market

| Segmentation Details | Description |

|---|---|

| Fuel Type | Low Sulfur Fuel Oil, High Sulfur Fuel Oil, Marine Gas Oil, Others |

| End User | Shipping Companies, Oil Refineries, Power Plants, Fishing Vessels |

| Application | Commercial Shipping, Fishing Operations, Power Generation, Offshore Activities |

| Distribution Channel | Direct Sales, Distributors, Online Platforms, Bunkering Services |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the China Bunker Fuel Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.