444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Chile container glass market represents a dynamic and evolving sector within the country’s packaging industry, driven by increasing demand from beverage, food, pharmaceutical, and cosmetic industries. Container glass manufacturing in Chile has experienced significant transformation over recent years, with local producers adapting to changing consumer preferences and sustainability requirements. The market demonstrates robust growth potential, supported by Chile’s strong wine industry, expanding food processing sector, and growing emphasis on sustainable packaging solutions.

Market dynamics indicate that Chile’s container glass industry benefits from abundant raw material availability and strategic geographic positioning for both domestic consumption and export opportunities. The sector has witnessed increased investment in modern manufacturing technologies, with companies focusing on energy-efficient production processes and enhanced product quality. Growth rates in the Chilean container glass market have shown resilience, with the industry experiencing approximately 4.2% annual growth over the past five years, driven primarily by the wine packaging segment and expanding food preservation needs.

Regional positioning plays a crucial role in Chile’s container glass market development, as the country serves as a key supplier to neighboring South American markets while maintaining strong domestic demand. The market structure encompasses both large-scale industrial producers and specialized manufacturers focusing on premium glass containers for Chile’s renowned wine industry. Technological advancement and environmental considerations continue to shape market evolution, with manufacturers increasingly adopting recycled glass content and implementing circular economy principles in their operations.

The Chile container glass market refers to the comprehensive ecosystem of glass container manufacturing, distribution, and consumption within Chilean territory, encompassing all forms of glass packaging solutions used across various industries. This market includes the production of bottles, jars, vials, and other glass containers designed for packaging beverages, food products, pharmaceuticals, cosmetics, and industrial applications. Container glass specifically denotes hollow glass products manufactured through automated processes, distinguished from flat glass or specialty glass applications.

Market scope encompasses the entire value chain from raw material procurement and glass manufacturing to final product distribution and end-user consumption. The Chilean container glass market includes both primary packaging solutions, where glass containers directly contact the product, and secondary packaging applications. Industry participants range from large-scale manufacturers with integrated production facilities to specialized converters and distributors serving specific market segments.

Technological aspects of the market involve various glass forming techniques, including blow-and-blow, press-and-blow, and narrow neck press-and-blow processes, each optimized for different container types and applications. The market also encompasses related services such as glass decoration, labeling, and custom design solutions that add value to basic container glass products.

Chile’s container glass market demonstrates strong fundamentals supported by diverse end-user industries and favorable economic conditions. The market benefits from Chile’s position as a leading wine producer, creating substantial demand for premium glass bottles, while also serving growing food processing and pharmaceutical sectors. Market performance has been characterized by steady expansion, with the wine packaging segment accounting for approximately 45% of total container glass consumption in the country.

Key growth drivers include increasing consumer preference for glass packaging due to its premium image and recyclability, expanding export-oriented food and beverage industries, and rising health consciousness driving demand for glass containers in pharmaceutical and nutraceutical applications. The market has shown resilience during economic fluctuations, supported by essential product categories and export demand. Innovation trends focus on lightweight glass designs, enhanced barrier properties, and sustainable manufacturing processes.

Competitive landscape features both international glass manufacturers with local operations and domestic companies specializing in regional market needs. The market structure supports healthy competition while maintaining quality standards required for premium applications, particularly in the wine industry where container quality directly impacts product perception and export success.

Strategic insights reveal several critical factors shaping the Chile container glass market’s trajectory and competitive dynamics:

Primary market drivers propelling growth in Chile’s container glass market stem from both domestic consumption patterns and export-oriented industries. The country’s thriving wine industry serves as the most significant driver, with Chilean wine exports requiring high-quality glass bottles that meet international standards and consumer expectations. Wine production growth of approximately 3.5% annually directly translates to increased demand for premium glass containers, supporting market expansion and technological investment.

Consumer preferences increasingly favor glass packaging due to its perceived premium quality, health benefits, and environmental sustainability. This trend particularly impacts the food and beverage sectors, where glass containers are associated with product purity and extended shelf life. Health consciousness among consumers drives demand for glass packaging in pharmaceutical and nutraceutical applications, where container inertness and barrier properties are critical for product integrity.

Environmental regulations and sustainability initiatives create additional market drivers as governments and corporations seek to reduce plastic packaging usage. Glass containers offer complete recyclability and reduced environmental impact, aligning with circular economy objectives and corporate sustainability commitments. The growing emphasis on sustainable packaging solutions positions container glass favorably against alternative packaging materials.

Economic factors including Chile’s stable economy, growing middle class, and expanding food processing industry contribute to sustained market growth. Export opportunities to regional markets provide additional growth avenues, particularly as neighboring countries develop their premium food and beverage industries and seek high-quality packaging solutions.

Significant challenges facing the Chile container glass market include high energy costs associated with glass manufacturing processes, which can impact production economics and competitive positioning. Glass furnaces require substantial energy inputs, and fluctuating energy prices can affect profitability and pricing strategies. Energy intensity of glass production remains a persistent concern, particularly as manufacturers seek to balance cost efficiency with environmental sustainability objectives.

Competition from alternative packaging materials, particularly lightweight plastics and aluminum containers, poses ongoing challenges to market growth. While glass offers premium positioning and sustainability benefits, alternative materials often provide cost advantages and reduced transportation costs due to lighter weight. Cost considerations become particularly relevant for price-sensitive market segments and bulk packaging applications.

Transportation costs and logistics challenges affect market dynamics, especially for export-oriented applications where glass weight increases shipping expenses. The fragile nature of glass containers requires specialized handling and packaging, adding to overall logistics costs and complexity. Supply chain considerations become critical factors in market competitiveness and customer satisfaction.

Raw material availability and quality consistency can impact production planning and cost management. While Chile has good access to basic raw materials, specialized additives and colorants may require importation, creating potential supply chain vulnerabilities and cost fluctuations that affect market stability.

Emerging opportunities in the Chile container glass market center on expanding applications in premium food packaging, pharmaceutical containers, and specialty glass products. The growing demand for artisanal and craft beverages creates opportunities for specialized glass containers with unique designs and enhanced functionality. Craft beer production and premium spirits markets offer potential for growth in specialized bottle designs and limited-edition packaging solutions.

Export market expansion presents significant opportunities as Chilean glass manufacturers can leverage their quality reputation and competitive positioning to serve regional markets. Countries throughout South America and beyond seek reliable suppliers of high-quality glass containers, particularly for premium product applications. Market penetration in neighboring countries could increase export volumes by approximately 25-30% over the next five years.

Sustainability initiatives create opportunities for manufacturers to differentiate their products through enhanced recycled content, reduced environmental impact, and circular economy participation. Green packaging solutions command premium pricing and align with corporate sustainability commitments, offering potential for margin improvement and market expansion.

Technology advancement opportunities include investment in smart glass technologies, enhanced barrier properties, and specialized coatings that extend product shelf life and improve functionality. Innovation in glass formulations and manufacturing processes can create competitive advantages and open new market segments, particularly in pharmaceutical and high-value food applications.

Complex market dynamics shape the Chile container glass market through interactions between supply-side factors, demand patterns, and competitive forces. Supply chain integration plays a crucial role, with successful manufacturers maintaining control over raw material sourcing, production processes, and distribution networks. The market demonstrates cyclical patterns aligned with seasonal demand from wine and food processing industries, requiring flexible production planning and inventory management.

Demand fluctuations reflect both domestic consumption patterns and export market conditions, with wine industry performance significantly influencing overall market dynamics. Economic cycles affect premium product demand, while essential food and pharmaceutical applications provide market stability during economic downturns. The market shows resilience through diversified end-user applications and geographic market exposure.

Competitive dynamics involve both price competition and quality differentiation, with manufacturers seeking optimal positioning between cost efficiency and premium product offerings. Innovation cycles drive market evolution as companies invest in new technologies, sustainable practices, and specialized product development to maintain competitive advantages.

Regulatory influences impact market dynamics through food safety requirements, environmental standards, and trade policies affecting both domestic operations and export opportunities. Market consolidation trends may reshape competitive landscape as companies seek economies of scale and enhanced market positioning through strategic partnerships or acquisitions.

Comprehensive research methodology employed for analyzing the Chile container glass market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability of market insights. Primary research involves direct engagement with industry participants including glass manufacturers, raw material suppliers, end-user companies, and distribution partners to gather firsthand market intelligence and validate secondary research findings.

Secondary research encompasses analysis of industry reports, government statistics, trade association data, and company financial statements to establish market baselines and identify trends. Data triangulation methods ensure consistency across different information sources and enhance the reliability of market assessments and projections.

Quantitative analysis includes statistical modeling of market trends, demand patterns, and competitive positioning using historical data and forward-looking indicators. Qualitative assessment incorporates expert interviews, industry surveys, and market observation to capture nuanced market dynamics and emerging trends that quantitative data alone cannot reveal.

Market segmentation analysis employs multiple classification criteria including end-user applications, product types, geographic regions, and customer categories to provide detailed market understanding. Validation processes include cross-referencing findings with industry experts and conducting sensitivity analysis to test key assumptions and projections.

Geographic distribution of Chile’s container glass market reflects the country’s industrial concentration and economic development patterns. Central Chile dominates market activity, encompassing the Santiago metropolitan region and surrounding industrial areas where major glass manufacturing facilities are located. This region accounts for approximately 60% of total container glass production and consumption, benefiting from proximity to major end-user industries and transportation infrastructure.

Wine-producing regions including the Central Valley, Maipo Valley, and Colchagua Valley represent critical market segments due to their concentration of wineries requiring premium glass bottles. These regions demonstrate seasonal demand patterns aligned with harvest cycles and export shipping schedules. Regional specialization in wine production creates opportunities for localized glass manufacturing and specialized product offerings.

Northern Chile presents opportunities in mining-related applications and industrial packaging, while also serving as a potential export gateway to neighboring countries. The region’s industrial development and mining activities create demand for specialized glass containers and industrial applications. Southern regions show growing potential in food processing and aquaculture-related packaging applications.

Export corridors through major ports including Valparaíso, San Antonio, and Antofagasta facilitate regional market access and international trade opportunities. Transportation infrastructure connecting production centers with export facilities influences market competitiveness and cost structures, particularly for export-oriented manufacturers.

Market competition in Chile’s container glass industry features a mix of international corporations with local operations and domestic manufacturers specializing in regional market needs. The competitive landscape demonstrates healthy rivalry while maintaining quality standards essential for premium applications, particularly in wine packaging where container quality directly impacts product perception and market success.

Leading market participants include:

Competitive strategies emphasize quality differentiation, technological innovation, and customer service excellence. Market positioning varies from cost-competitive bulk suppliers to premium specialty manufacturers serving high-value applications. Companies invest in modern equipment, sustainable practices, and technical capabilities to maintain competitive advantages.

Strategic partnerships between glass manufacturers and major end-users, particularly in the wine industry, create stable demand relationships and opportunities for product innovation. Vertical integration strategies help manufacturers control costs and quality while ensuring reliable supply chain performance.

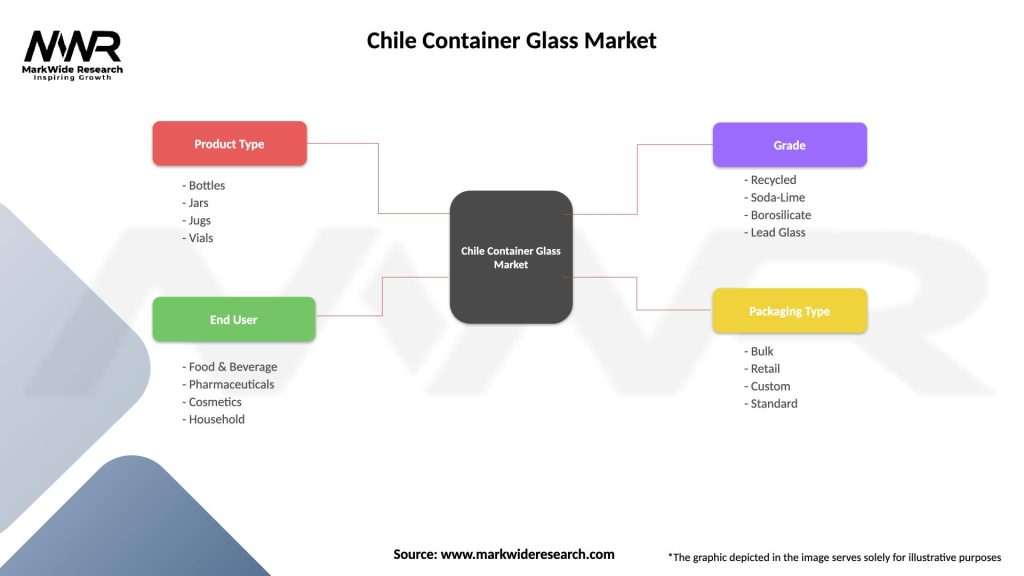

Market segmentation of Chile’s container glass industry reveals distinct categories based on application, product type, and end-user requirements. By Application, the market divides into beverage containers, food packaging, pharmaceutical containers, cosmetic packaging, and industrial applications, each with specific quality requirements and market dynamics.

Beverage Segment Analysis:

By Product Type:

Geographic segmentation reflects regional industrial concentration and end-user distribution, with central Chile dominating production and consumption while wine regions drive specialized demand patterns.

Wine Container Category represents the most significant and sophisticated segment of Chile’s container glass market, driven by the country’s position as a major wine exporter. This category demands exceptional quality standards, precise dimensional tolerances, and aesthetic appeal to support premium product positioning. Technical requirements include specific glass compositions for optimal wine preservation, UV protection capabilities, and compatibility with various closure systems.

Food Packaging Category encompasses diverse applications from preserved foods to specialty products, with growing emphasis on extended shelf life and product visibility. Market trends favor glass containers for premium food products, organic foods, and artisanal products where packaging quality reinforces product positioning. This segment shows steady growth aligned with expanding food processing industry and export opportunities.

Pharmaceutical Category requires the highest quality standards and regulatory compliance, focusing on container inertness, barrier properties, and contamination prevention. Growth potential in this category reflects Chile’s developing pharmaceutical industry and increasing health consciousness among consumers. Specialized glass formulations and precision manufacturing are essential for market success.

Industrial Applications include chemical containers, laboratory glassware, and specialized industrial packaging. This category values durability, chemical resistance, and cost efficiency. Market opportunities exist in mining-related applications and industrial chemical packaging, leveraging Chile’s strong industrial base.

Manufacturers in Chile’s container glass market benefit from stable demand from established industries, particularly the wine sector, providing predictable revenue streams and long-term business relationships. Operational advantages include access to quality raw materials, established supply chains, and proximity to major end-user industries. The market supports both high-volume production and specialized manufacturing, allowing companies to optimize their operational strategies.

End-user industries benefit from reliable supply of high-quality glass containers that enhance product presentation, extend shelf life, and support premium positioning. Wine producers particularly benefit from local glass manufacturing capabilities that understand specific quality requirements and can provide responsive service. The availability of diverse container options supports product differentiation and market positioning strategies.

Economic stakeholders including investors, suppliers, and service providers benefit from the market’s stability and growth potential. Employment opportunities in glass manufacturing and related industries contribute to regional economic development. The sector’s export potential creates foreign exchange earnings and supports Chile’s industrial competitiveness.

Environmental benefits include the circular economy potential of glass recycling, reduced packaging waste, and sustainable manufacturing practices. Consumer benefits encompass product quality preservation, health safety, and environmental responsibility through choosing recyclable packaging options.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration emerges as the dominant trend shaping Chile’s container glass market, with manufacturers increasingly incorporating recycled glass content and implementing circular economy principles. Environmental consciousness drives both regulatory requirements and consumer preferences, creating market advantages for companies demonstrating strong sustainability credentials. This trend influences product development, manufacturing processes, and marketing strategies across the industry.

Lightweighting initiatives represent another significant trend as manufacturers develop thinner, lighter glass containers that maintain strength and quality while reducing material usage and transportation costs. Technical innovation in glass formulations and manufacturing processes enables weight reductions of 10-15% without compromising container performance, addressing both cost and environmental concerns.

Customization and premiumization trends reflect growing demand for unique container designs that support brand differentiation and premium positioning. Wine industry requirements particularly drive innovation in bottle shapes, colors, and decorative elements that enhance product appeal and market positioning. This trend supports higher value-added manufacturing and improved profit margins.

Digital integration and smart manufacturing technologies increasingly influence production processes, quality control, and supply chain management. Industry 4.0 concepts including predictive maintenance, automated quality inspection, and real-time production optimization enhance operational efficiency and product consistency.

Recent industry developments in Chile’s container glass market reflect ongoing modernization and strategic positioning for future growth. MarkWide Research analysis indicates significant investment in furnace modernization and energy efficiency improvements across major manufacturing facilities. These developments focus on reducing environmental impact while improving production economics and product quality.

Technology upgrades include implementation of advanced forming equipment, automated inspection systems, and digital process control technologies. Manufacturing efficiency improvements of approximately 12-18% have been achieved through these technological investments, enhancing competitiveness and enabling expansion into new market segments.

Sustainability initiatives encompass increased recycled glass usage, renewable energy adoption, and waste reduction programs. Several manufacturers have committed to achieving carbon neutrality goals within the next decade, driving continued investment in clean technologies and sustainable practices.

Market expansion activities include new product development for emerging applications, strategic partnerships with major end-users, and export market development initiatives. Capacity expansion projects are underway to meet growing demand and support export opportunities, particularly in specialized glass container segments.

Regulatory developments include updated food safety standards, environmental compliance requirements, and trade facilitation measures supporting export growth. These developments create both challenges and opportunities for market participants seeking to maintain compliance while expanding market presence.

Strategic recommendations for Chile container glass market participants emphasize the importance of balancing traditional strengths with emerging market opportunities. Wine industry relationships should be maintained and strengthened while simultaneously diversifying into other high-growth segments to reduce market concentration risks. Companies should leverage their quality reputation and technical capabilities to expand into premium applications across multiple industries.

Investment priorities should focus on energy efficiency improvements, sustainable manufacturing practices, and advanced production technologies that enhance competitiveness and environmental performance. MWR analysis suggests that companies investing in modern furnace technology and automation systems achieve 15-20% operational cost reductions while improving product quality and consistency.

Market expansion strategies should prioritize regional export opportunities while maintaining strong domestic market positions. Export development requires investment in quality certifications, customer relationship building, and logistics optimization to compete effectively in international markets. Strategic partnerships with distributors and end-users can facilitate market entry and growth.

Innovation focus should emphasize sustainable products, lightweighting technologies, and specialized applications that command premium pricing. Research and development investments in new glass formulations, decorative techniques, and functional enhancements can create competitive differentiation and support margin improvement.

Risk management strategies should address energy cost volatility, raw material supply security, and market diversification to reduce dependence on any single industry or customer segment. Financial planning should account for cyclical demand patterns and economic sensitivity while maintaining investment capacity for growth opportunities.

Long-term prospects for Chile’s container glass market appear positive, supported by fundamental demand drivers and strategic positioning advantages. Market growth is projected to continue at a steady pace, with the wine industry maintaining its role as the primary demand driver while other segments contribute increasing proportions of total market volume. MarkWide Research projections indicate potential market expansion of 5-7% annually over the next five years, driven by export growth and domestic market development.

Sustainability trends will increasingly influence market dynamics, creating opportunities for companies that successfully integrate environmental considerations into their business strategies. Circular economy principles and recycled content requirements will become standard market expectations, driving continued investment in sustainable manufacturing practices and recycling infrastructure.

Technology evolution will continue reshaping manufacturing processes, quality control systems, and product development capabilities. Digital transformation and smart manufacturing technologies will become essential for maintaining competitiveness and meeting evolving customer requirements. Companies that successfully integrate these technologies will achieve significant operational advantages.

Market consolidation may occur as companies seek economies of scale and enhanced market positioning through strategic partnerships or acquisitions. Regional integration opportunities will expand as South American markets develop and demand for high-quality glass containers increases. Export market development will become increasingly important for achieving optimal growth and profitability.

Innovation opportunities in specialized applications, premium products, and sustainable solutions will create new market segments and value-added opportunities. Customer collaboration and co-development projects will become more important for creating differentiated products and maintaining competitive advantages in an evolving market landscape.

Chile’s container glass market represents a mature yet dynamic industry with strong foundations and promising growth prospects. The market benefits from established relationships with key end-user industries, particularly the wine sector, while demonstrating potential for diversification and expansion into new applications and geographic markets. Strategic positioning as a quality supplier with sustainable manufacturing practices positions Chilean glass manufacturers favorably for future market development.

Market fundamentals including raw material availability, technical expertise, and geographic advantages provide solid foundations for continued growth and competitiveness. The industry’s focus on quality, sustainability, and innovation aligns with global market trends and customer requirements, supporting long-term market viability and expansion opportunities.

Future success will depend on companies’ ability to balance traditional strengths with emerging market opportunities, invest in modern technologies and sustainable practices, and develop new market segments while maintaining excellence in core applications. The container glass market in Chile is well-positioned to capitalize on growing demand for sustainable packaging solutions and premium product applications, offering attractive opportunities for industry participants and stakeholders committed to long-term market development and value creation.

What is Container Glass?

Container glass refers to glass products designed for packaging and storing various goods, including beverages, food, and pharmaceuticals. It is known for its durability, recyclability, and ability to preserve the quality of its contents.

What are the key players in the Chile Container Glass Market?

Key players in the Chile Container Glass Market include companies like Cristalerías de Chile, Owens-Illinois, and Verallia, which are known for their production of glass containers for food and beverage industries, among others.

What are the growth factors driving the Chile Container Glass Market?

The Chile Container Glass Market is driven by increasing consumer demand for sustainable packaging solutions, the growth of the beverage industry, and a rising preference for glass over plastic due to health and environmental concerns.

What challenges does the Chile Container Glass Market face?

Challenges in the Chile Container Glass Market include high production costs, competition from alternative packaging materials, and the need for significant energy consumption during manufacturing processes.

What opportunities exist in the Chile Container Glass Market?

Opportunities in the Chile Container Glass Market include the expansion of eco-friendly packaging initiatives, innovations in glass recycling technologies, and the growing trend of premium packaging in the food and beverage sectors.

What trends are shaping the Chile Container Glass Market?

Trends in the Chile Container Glass Market include the increasing use of lightweight glass containers, advancements in manufacturing technologies, and a shift towards personalized packaging solutions to enhance consumer experience.

Chile Container Glass Market

| Segmentation Details | Description |

|---|---|

| Product Type | Bottles, Jars, Jugs, Vials |

| End User | Food & Beverage, Pharmaceuticals, Cosmetics, Household |

| Grade | Recycled, Soda-Lime, Borosilicate, Lead Glass |

| Packaging Type | Bulk, Retail, Custom, Standard |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Chile Container Glass Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.