444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Central and Eastern Europe (CEE) facility management market represents a rapidly evolving sector that encompasses comprehensive property and infrastructure management services across diverse industries. This dynamic market spans multiple countries including Poland, Czech Republic, Hungary, Slovakia, Romania, Bulgaria, Croatia, Slovenia, and the Baltic states, each contributing unique characteristics to the regional landscape. Facility management services in the CEE region have experienced substantial growth driven by increasing urbanization, foreign direct investment, and the modernization of commercial real estate infrastructure.

Market dynamics indicate that the CEE facility management sector is expanding at a compound annual growth rate (CAGR) of 8.2%, significantly outpacing many Western European markets. This growth trajectory reflects the region’s economic development, increasing adoption of outsourced facility management solutions, and rising demand for integrated property services. Commercial real estate development, particularly in major metropolitan areas like Warsaw, Prague, Budapest, and Bucharest, has created substantial opportunities for facility management providers to establish comprehensive service portfolios.

Service integration has become a defining characteristic of the CEE facility management market, with providers offering end-to-end solutions encompassing maintenance, security, cleaning, catering, and energy management. The market demonstrates strong potential for continued expansion as businesses increasingly recognize the strategic value of professional facility management in optimizing operational efficiency and reducing overhead costs.

The Central and Eastern Europe facility management market refers to the comprehensive ecosystem of professional services designed to ensure optimal functionality, comfort, safety, and efficiency of built environments across the CEE region. This market encompasses a wide range of integrated services including property maintenance, space management, security services, cleaning operations, energy management, and support services that enable organizations to focus on their core business activities while ensuring their facilities operate at peak performance.

Facility management in the CEE context involves the strategic coordination of workplace environments, infrastructure, and support services to enhance organizational productivity and employee satisfaction. The market includes both hard services such as mechanical and electrical maintenance, HVAC systems management, and building repairs, as well as soft services including cleaning, catering, reception services, and waste management. Integrated facility management (IFM) has emerged as a preferred approach, combining multiple services under single contracts to deliver cost efficiencies and streamlined operations.

Regional characteristics of the CEE facility management market include adaptation to local regulations, cultural preferences, and economic conditions while maintaining international service standards. The market serves diverse sectors including commercial offices, retail spaces, industrial facilities, healthcare institutions, educational establishments, and government buildings, each requiring specialized facility management approaches tailored to specific operational requirements and regulatory compliance standards.

Strategic positioning of the Central and Eastern Europe facility management market reflects a mature yet rapidly evolving sector characterized by increasing consolidation, technological integration, and service sophistication. The market has transitioned from basic maintenance services to comprehensive facility management solutions that incorporate smart building technologies, sustainability initiatives, and data-driven optimization strategies. Market penetration varies significantly across CEE countries, with Poland, Czech Republic, and Hungary leading adoption rates at approximately 45% of commercial properties utilizing professional facility management services.

Competitive dynamics demonstrate a healthy mix of international facility management giants and regional specialists, creating diverse service offerings and competitive pricing structures. The market benefits from strong economic fundamentals, continued foreign investment, and modernization of commercial real estate portfolios. Technology adoption has accelerated significantly, with 62% of facility management providers implementing IoT-enabled solutions and digital platforms to enhance service delivery and operational transparency.

Growth drivers include increasing outsourcing trends, regulatory compliance requirements, sustainability mandates, and the need for cost optimization in facility operations. The market demonstrates resilience and adaptability, having successfully navigated economic uncertainties while maintaining steady growth trajectories. Future prospects remain highly favorable, supported by continued urbanization, commercial real estate development, and increasing recognition of facility management as a strategic business function rather than a cost center.

Market segmentation reveals distinct patterns across the CEE facility management landscape, with several key insights emerging from comprehensive analysis:

Economic development across the CEE region serves as a fundamental driver for facility management market expansion. Sustained GDP growth, increasing foreign direct investment, and modernization of business infrastructure create substantial demand for professional facility management services. Commercial real estate development in major metropolitan areas has accelerated significantly, with new office complexes, retail centers, and industrial facilities requiring comprehensive facility management solutions from project inception through operational phases.

Outsourcing trends continue to gain momentum as organizations recognize the strategic advantages of focusing on core business activities while delegating facility management responsibilities to specialized providers. This shift reflects growing understanding that professional facility management delivers cost efficiencies, operational improvements, and risk mitigation benefits that exceed in-house capabilities. Cost optimization pressures drive organizations to seek integrated solutions that consolidate multiple services under single contracts, reducing administrative overhead and improving service coordination.

Regulatory compliance requirements have become increasingly complex across CEE countries, necessitating specialized expertise in areas such as health and safety, environmental regulations, and building codes. Sustainability mandates and energy efficiency requirements create additional demand for facility management providers with green building expertise and environmental management capabilities. Technology integration demands, including smart building systems, IoT implementations, and data analytics platforms, require sophisticated technical expertise that many organizations prefer to outsource rather than develop internally.

Workforce dynamics also contribute to market growth, as organizations face challenges in recruiting and retaining skilled facility management personnel. Professional facility management providers offer access to trained specialists, career development opportunities, and operational expertise that individual organizations struggle to maintain independently.

Economic volatility remains a significant constraint for the CEE facility management market, as regional economies remain sensitive to global economic fluctuations and geopolitical uncertainties. Currency fluctuations and inflation pressures can impact contract profitability and pricing strategies, particularly for international facility management providers operating across multiple CEE countries with different currencies and economic conditions.

Skilled workforce shortages present ongoing challenges for facility management providers seeking to expand operations and maintain service quality standards. The technical nature of modern facility management requires specialized skills in areas such as building automation systems, energy management, and digital technologies. Training and development costs associated with workforce preparation can strain operational budgets and limit growth potential for smaller facility management companies.

Regulatory complexity across different CEE countries creates operational challenges for facility management providers seeking regional expansion. Varying building codes, safety regulations, environmental requirements, and labor laws necessitate significant investment in local expertise and compliance systems. Cultural differences and language barriers can complicate service delivery and client relationship management, particularly for international providers entering new CEE markets.

Technology investment requirements continue to escalate as clients demand increasingly sophisticated facility management solutions incorporating IoT sensors, predictive maintenance systems, and integrated management platforms. Capital intensity of these technology investments can strain smaller facility management providers and create barriers to market entry. Additionally, cybersecurity concerns associated with connected building systems require ongoing investment in security infrastructure and expertise.

Digital transformation initiatives present substantial opportunities for facility management providers to differentiate their services and create additional value for clients. The integration of Internet of Things (IoT) technologies, artificial intelligence, and predictive analytics enables facility management companies to offer proactive maintenance, energy optimization, and space utilization services that deliver measurable operational improvements and cost savings.

Sustainability consulting represents a rapidly growing opportunity as organizations across the CEE region face increasing pressure to reduce environmental impact and achieve green building certifications. Facility management providers with expertise in energy management, waste reduction, and sustainable operations can command premium pricing while helping clients meet environmental objectives. Carbon footprint reduction services and renewable energy integration present additional revenue streams for forward-thinking facility management companies.

Healthcare sector expansion offers significant growth potential as CEE countries invest in healthcare infrastructure modernization and capacity expansion. Specialized facility management services for hospitals, clinics, and medical facilities require unique expertise in infection control, medical equipment maintenance, and regulatory compliance. Educational facility management also presents opportunities as universities and schools seek to optimize operational efficiency while maintaining safe, conducive learning environments.

Smart city initiatives across major CEE metropolitan areas create opportunities for facility management providers to participate in large-scale infrastructure projects incorporating advanced building management systems and integrated service delivery models. Public-private partnerships in facility management for government buildings, transportation hubs, and public facilities offer stable, long-term revenue opportunities for qualified providers.

Competitive intensity within the CEE facility management market has increased significantly as both international and regional players vie for market share in this attractive growth market. Market consolidation trends have emerged as larger facility management companies acquire regional specialists to expand geographic coverage and service capabilities. This consolidation creates opportunities for improved service integration and operational efficiency while potentially reducing competitive pricing pressures.

Client expectations continue to evolve toward more sophisticated, technology-enabled facility management solutions that provide real-time visibility into building performance, energy consumption, and operational metrics. Performance-based contracting models are gaining popularity, with facility management providers accepting responsibility for achieving specific operational outcomes rather than simply delivering prescribed services. This shift requires facility management companies to invest in advanced monitoring systems and data analytics capabilities.

Supply chain dynamics have become increasingly important as facility management providers seek to optimize procurement processes and leverage economies of scale across multiple client sites. Vendor management capabilities and strategic supplier relationships provide competitive advantages in delivering cost-effective services while maintaining quality standards. Risk management considerations have also gained prominence, with facility management providers implementing comprehensive insurance coverage, safety protocols, and business continuity planning to protect client operations.

Innovation cycles are accelerating as facility management providers compete to offer cutting-edge solutions that deliver measurable value to clients. Collaboration platforms and mobile applications enhance communication between facility management teams and building occupants, improving service responsiveness and user satisfaction.

Comprehensive market analysis of the Central and Eastern Europe facility management market employs a multi-faceted research approach combining primary and secondary research methodologies to ensure accuracy and depth of insights. Primary research involves extensive interviews with facility management executives, industry experts, and key stakeholders across major CEE markets to gather firsthand perspectives on market trends, challenges, and opportunities.

Secondary research encompasses analysis of industry reports, government publications, regulatory documents, and company financial statements to establish market sizing, growth trends, and competitive dynamics. Data triangulation methods validate findings across multiple sources to ensure reliability and accuracy of market insights. Regional analysis considers country-specific factors including economic conditions, regulatory environments, and cultural preferences that influence facility management market development.

Quantitative analysis incorporates statistical modeling and trend analysis to project market growth trajectories and identify emerging opportunities. Qualitative assessment examines market dynamics, competitive positioning, and strategic implications for industry participants. Expert validation processes involve review of findings by industry specialists and MarkWide Research analysts to ensure comprehensive coverage and analytical rigor.

Market segmentation analysis examines facility management services across multiple dimensions including service type, industry vertical, company size, and geographic region. Competitive landscape assessment evaluates market positioning, service offerings, and strategic initiatives of leading facility management providers operating in the CEE region.

Poland represents the largest facility management market within the CEE region, accounting for approximately 32% of regional market activity. The Polish market benefits from a mature commercial real estate sector, strong economic growth, and high levels of foreign investment. Warsaw, Krakow, and Gdansk serve as primary hubs for facility management activity, with comprehensive service offerings across all major industry verticals. Polish facility management providers have achieved significant scale and sophistication, competing effectively with international players while maintaining competitive cost structures.

Czech Republic maintains the second-largest facility management market in the region, representing approximately 18% of total market activity. Prague serves as the dominant market center, with significant facility management activity in Brno and Ostrava. The Czech market demonstrates high adoption rates for integrated facility management solutions and advanced technology implementations. Regulatory stability and business-friendly policies support continued market growth and international investment.

Hungary accounts for approximately 14% of regional facility management activity, with Budapest serving as the primary market center. The Hungarian market has experienced steady growth driven by automotive industry expansion, shared services center development, and commercial real estate modernization. Government initiatives supporting business development and EU funding for infrastructure projects create additional opportunities for facility management providers.

Romania and Bulgaria represent emerging markets with significant growth potential, collectively accounting for 16% of regional activity. These markets demonstrate rapid adoption of professional facility management services as commercial real estate sectors mature and international businesses establish operations. Bucharest and Sofia lead market development, with expanding opportunities in secondary cities as economic development spreads beyond capital regions.

Market leadership in the CEE facility management sector reflects a diverse competitive environment featuring international facility management giants, regional specialists, and emerging local providers. The competitive landscape demonstrates healthy dynamics with opportunities for companies across different scales and service specializations.

Competitive differentiation strategies include technology integration, sustainability expertise, industry specialization, and geographic coverage. Strategic partnerships between international providers and local specialists enable market entry and service expansion while leveraging regional expertise and relationships.

Service-based segmentation reveals distinct market dynamics across different facility management service categories:

Hard Services:

Soft Services:

Industry vertical segmentation demonstrates varying facility management requirements and growth opportunities across different sectors:

Integrated Facility Management (IFM) has emerged as the fastest-growing category within the CEE market, representing a comprehensive approach that combines multiple facility management services under single contracts. IFM solutions deliver operational efficiencies, cost savings, and simplified vendor management for clients while enabling facility management providers to achieve economies of scale and improved profit margins. The category demonstrates strong growth potential as organizations seek to streamline facility operations and reduce administrative complexity.

Technical Services category encompasses specialized facility management services requiring advanced technical expertise, including building automation systems, energy management, and mechanical maintenance. This category commands premium pricing due to skill requirements and critical nature of services. Predictive maintenance and condition monitoring services within this category are experiencing rapid growth as organizations seek to optimize asset performance and reduce unplanned downtime.

Workplace Services category focuses on enhancing employee experience and productivity through services such as space management, catering, reception services, and workplace technology support. This category has gained importance as organizations recognize the connection between workplace environment and employee satisfaction, retention, and productivity. Flexible workspace solutions and activity-based working concepts are driving innovation within this category.

Sustainability Services represent an emerging category addressing environmental compliance, energy efficiency, and green building certification requirements. This category demonstrates strong growth potential as regulatory requirements tighten and organizations commit to environmental sustainability objectives. Carbon footprint management and renewable energy integration services are experiencing particularly strong demand.

Cost optimization represents the primary benefit for organizations utilizing professional facility management services, with typical cost savings ranging from 15% to 25% compared to in-house facility management operations. These savings result from economies of scale, specialized expertise, and optimized procurement processes that facility management providers leverage across multiple client sites. Operational efficiency improvements enable organizations to redirect resources toward core business activities while maintaining or improving facility performance standards.

Risk mitigation benefits include comprehensive insurance coverage, regulatory compliance expertise, and professional liability protection that facility management providers offer. Business continuity planning and emergency response capabilities ensure minimal disruption to client operations during unexpected events. Technology access enables clients to benefit from advanced facility management systems and digital platforms without significant capital investment or technical expertise development.

Scalability advantages allow organizations to adjust facility management services based on changing business requirements, expansion plans, or market conditions. Flexibility in service delivery models accommodates diverse organizational needs and preferences. Performance transparency through advanced reporting and analytics platforms provides clients with detailed insights into facility performance, cost trends, and optimization opportunities.

Expertise access provides organizations with specialized knowledge in areas such as sustainability, regulatory compliance, and emerging technologies that would be difficult and expensive to develop internally. Innovation benefits include access to cutting-edge facility management solutions and best practices developed across diverse client portfolios and market segments.

Strengths:

Weaknesses:

Opportunities:

Threats:

Smart building integration has become a dominant trend within the CEE facility management market, with providers increasingly incorporating IoT sensors, building automation systems, and predictive analytics into their service offerings. Data-driven facility management enables proactive maintenance, energy optimization, and space utilization improvements that deliver measurable value to clients. This trend requires facility management providers to invest in technology platforms and develop analytical capabilities to interpret and act upon building performance data.

Sustainability focus continues to intensify as organizations across the CEE region face increasing pressure to reduce environmental impact and achieve green building certifications. Energy efficiency optimization, waste reduction programs, and carbon footprint management have become standard components of comprehensive facility management contracts. Renewable energy integration and sustainable procurement practices are emerging as additional service areas for environmentally-focused facility management providers.

Workplace experience enhancement has gained prominence as organizations recognize the connection between facility management and employee satisfaction, productivity, and retention. Activity-based working concepts, flexible space management, and workplace technology support are becoming integral components of modern facility management services. Health and wellness considerations, including indoor air quality management and ergonomic workspace design, are increasingly important in facility management service delivery.

Service integration trends continue toward comprehensive facility management solutions that combine multiple service categories under single contracts. Partnership-based relationships between facility management providers and clients are replacing traditional vendor relationships, with shared objectives and performance-based contracting models becoming more common.

Technology partnerships have emerged as a significant development trend, with facility management providers forming strategic alliances with technology companies to enhance service capabilities and digital transformation offerings. These partnerships enable facility management companies to access cutting-edge solutions without significant internal development investment while providing technology companies with market access and implementation expertise.

Acquisition activity has accelerated as larger facility management providers seek to expand geographic coverage and service capabilities through strategic acquisitions of regional specialists and niche service providers. Market consolidation trends create opportunities for improved operational efficiency and enhanced service integration while potentially reducing competitive pricing pressures in certain market segments.

Regulatory developments across CEE countries are creating new requirements for facility management providers, particularly in areas such as environmental compliance, health and safety standards, and data protection. Professional certification programs and industry standards are being developed to ensure service quality and regulatory compliance across the facility management sector.

Innovation initiatives include development of mobile applications for facility management communication, implementation of artificial intelligence for predictive maintenance, and integration of renewable energy systems into facility management operations. Pilot programs for autonomous cleaning systems, drone-based facility inspections, and virtual reality training platforms demonstrate the industry’s commitment to technological advancement and service innovation.

Strategic positioning recommendations for facility management providers operating in the CEE market emphasize the importance of technology integration, sustainability expertise, and regional market knowledge. MarkWide Research analysis suggests that successful facility management companies should invest in digital platforms that provide real-time visibility into building performance and enable predictive maintenance capabilities. Differentiation strategies should focus on specialized expertise in high-growth sectors such as healthcare, education, and sustainable facility management.

Geographic expansion strategies should consider the varying maturity levels across CEE markets, with established providers potentially focusing on market share growth in mature markets like Poland and Czech Republic while exploring opportunities in emerging markets such as Romania and Bulgaria. Partnership approaches with local specialists can facilitate market entry and provide cultural and regulatory expertise necessary for successful operations.

Service portfolio development should prioritize integrated facility management solutions that combine multiple service categories under comprehensive contracts. Technology investment priorities should include IoT platforms, data analytics capabilities, and mobile applications that enhance service delivery and client communication. Sustainability capabilities should be developed to address growing demand for environmental compliance and green building expertise.

Workforce development initiatives should address skill shortages in technical specialties and emerging technology areas. Training programs and professional development opportunities can help facility management providers attract and retain qualified personnel while building capabilities in high-demand service areas.

Growth projections for the Central and Eastern Europe facility management market remain highly favorable, with continued expansion expected across all major service categories and geographic markets. Market maturation will likely accelerate as organizations increasingly recognize facility management as a strategic business function rather than a cost center. Technology integration will continue to drive service innovation and operational efficiency improvements, creating new opportunities for differentiation and value creation.

Sustainability requirements are expected to become increasingly stringent, creating substantial opportunities for facility management providers with environmental expertise and green building capabilities. MWR projections indicate that sustainability-focused facility management services will experience growth rates exceeding 12% annually as regulatory requirements tighten and corporate environmental commitments intensify.

Digital transformation initiatives will accelerate across the facility management sector, with smart building technologies, predictive analytics, and automated systems becoming standard components of comprehensive facility management solutions. Artificial intelligence and machine learning applications will enable more sophisticated predictive maintenance and energy optimization capabilities.

Market consolidation trends are expected to continue as larger facility management providers seek to achieve economies of scale and expand service capabilities through strategic acquisitions. Regional integration will likely increase as successful facility management companies expand across multiple CEE markets to serve multinational clients and achieve operational efficiencies.

The Central and Eastern Europe facility management market represents a dynamic and rapidly evolving sector with substantial growth potential driven by economic development, technological advancement, and increasing recognition of facility management as a strategic business function. Market fundamentals remain strong across the region, supported by continued commercial real estate development, foreign investment, and modernization of business infrastructure.

Competitive dynamics demonstrate healthy market conditions with opportunities for providers across different scales and service specializations. The successful integration of technology, sustainability expertise, and comprehensive service offerings will determine market leadership in the coming years. Regional diversity across CEE countries creates both challenges and opportunities for facility management providers seeking to establish comprehensive market coverage.

Future success in the CEE facility management market will depend on providers’ ability to adapt to evolving client expectations, integrate advanced technologies, and deliver measurable value through comprehensive facility management solutions. The market’s continued evolution toward integrated, technology-enabled, and sustainability-focused services positions it for sustained growth and development across the Central and Eastern Europe region.

What is Facility Management?

Facility Management refers to the integrated approach to maintaining and managing buildings and their services, including maintenance, security, and space management. It plays a crucial role in ensuring operational efficiency and enhancing the user experience within facilities.

What are the key players in the Central and Eastern Europe (CEE) Facility Management Market?

Key players in the Central and Eastern Europe (CEE) Facility Management Market include companies like ISS Facility Services, CBRE Group, and Sodexo, which provide a range of services from cleaning and maintenance to security and property management, among others.

What are the main drivers of growth in the Central and Eastern Europe (CEE) Facility Management Market?

The growth of the Central and Eastern Europe (CEE) Facility Management Market is driven by increasing urbanization, the rise in demand for efficient building management solutions, and the growing emphasis on sustainability and energy efficiency in facilities.

What challenges does the Central and Eastern Europe (CEE) Facility Management Market face?

Challenges in the Central and Eastern Europe (CEE) Facility Management Market include the need for skilled labor, the complexity of integrating new technologies, and the varying regulatory environments across different countries in the region.

What opportunities exist in the Central and Eastern Europe (CEE) Facility Management Market?

Opportunities in the Central and Eastern Europe (CEE) Facility Management Market include the adoption of smart building technologies, the increasing focus on sustainability practices, and the potential for growth in the outsourcing of facility management services.

What trends are shaping the Central and Eastern Europe (CEE) Facility Management Market?

Trends in the Central and Eastern Europe (CEE) Facility Management Market include the rise of digital transformation in facility management, the integration of IoT for enhanced operational efficiency, and a growing focus on health and safety standards in response to recent global events.

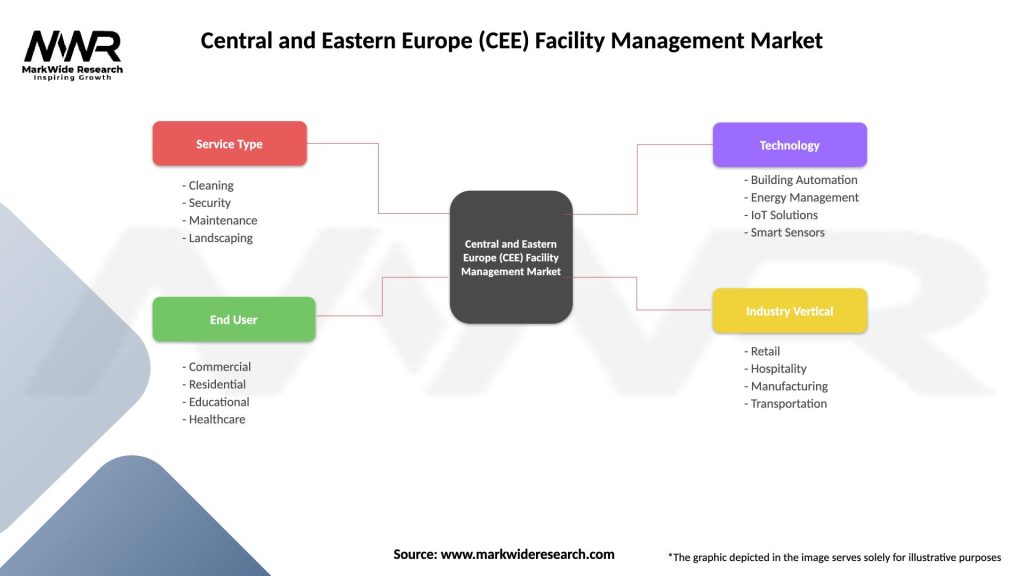

Central and Eastern Europe (CEE) Facility Management Market

| Segmentation Details | Description |

|---|---|

| Service Type | Cleaning, Security, Maintenance, Landscaping |

| End User | Commercial, Residential, Educational, Healthcare |

| Technology | Building Automation, Energy Management, IoT Solutions, Smart Sensors |

| Industry Vertical | Retail, Hospitality, Manufacturing, Transportation |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Central and Eastern Europe (CEE) Facility Management Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.