444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Canada food service market represents a dynamic and rapidly evolving sector that encompasses restaurants, cafeterias, catering services, and institutional food providers across the nation. This comprehensive market serves millions of consumers daily through diverse dining establishments ranging from quick-service restaurants to fine dining venues, institutional cafeterias, and specialized catering operations. Market dynamics indicate robust growth driven by changing consumer preferences, urbanization trends, and increasing demand for convenient dining solutions.

Growth trajectories within the Canadian food service landscape demonstrate remarkable resilience and adaptability, particularly following recent industry transformations. The sector has experienced a 6.2% annual growth rate in digital ordering adoption, while delivery services have captured 28% market penetration across major metropolitan areas. Regional distribution shows Ontario and Quebec commanding the largest market shares, collectively representing approximately 65% of total industry activity.

Industry transformation continues to reshape traditional food service models, with technology integration, sustainability initiatives, and health-conscious menu offerings driving competitive differentiation. The market encompasses various segments including full-service restaurants, limited-service establishments, institutional food services, and mobile food vendors, each responding to distinct consumer demands and operational requirements.

The Canada food service market refers to the comprehensive ecosystem of businesses and organizations that prepare, serve, and deliver food and beverages to consumers outside their homes. This market encompasses all commercial and institutional establishments that provide ready-to-eat meals, beverages, and related services to customers through various service models and distribution channels.

Market scope includes traditional restaurants, fast-food chains, coffee shops, bars, institutional cafeterias in schools and hospitals, catering companies, food trucks, and emerging digital-first dining concepts. The sector serves as a critical component of Canada’s hospitality industry, supporting employment, tourism, and local economic development while adapting to evolving consumer lifestyles and preferences.

Service delivery models within this market range from dine-in experiences to takeout, delivery, catering, and hybrid concepts that combine multiple service approaches. The industry’s definition has expanded significantly to include ghost kitchens, meal kit services, and technology-enabled dining solutions that blur traditional boundaries between food retail and food service operations.

Strategic positioning of Canada’s food service market reflects a mature yet innovative industry experiencing significant transformation driven by technological advancement, changing consumer behaviors, and evolving market dynamics. The sector demonstrates strong fundamentals with consistent growth patterns, despite periodic challenges from economic fluctuations and external disruptions.

Key performance indicators reveal encouraging trends across multiple market segments, with quick-service restaurants maintaining 42% market share while full-service establishments adapt through enhanced digital capabilities and diversified revenue streams. Consumer spending patterns show increased preference for convenience-oriented dining solutions, premium ingredients, and sustainable food options.

Market leadership remains distributed among established chains, independent operators, and emerging digital-native brands, creating a competitive landscape that fosters innovation and customer-centric service improvements. The industry’s resilience and adaptability position it favorably for continued expansion, supported by favorable demographic trends and increasing urbanization across Canadian markets.

Investment flows into technology infrastructure, sustainability initiatives, and workforce development indicate strong confidence in the sector’s long-term prospects, while regulatory support for small business development and food safety standards maintains operational stability and consumer trust.

Consumer behavior analysis reveals fundamental shifts in dining preferences, with increased emphasis on health-conscious options, locally sourced ingredients, and customizable menu offerings. These trends drive menu innovation and operational adjustments across all market segments, from quick-service to fine dining establishments.

Market segmentation demonstrates clear differentiation between service categories, with each segment developing specialized capabilities to address specific consumer needs and preferences. Cross-segment competition intensifies as traditional boundaries blur through hybrid service models and innovative dining concepts.

Demographic trends serve as primary growth catalysts for Canada’s food service market, with urbanization, population growth, and changing household compositions creating sustained demand for convenient dining solutions. Millennial and Gen Z consumers demonstrate strong preferences for experiential dining, diverse cuisine options, and technology-enabled service interactions.

Economic prosperity in major metropolitan areas supports discretionary spending on food service experiences, while rising disposable incomes enable consumers to prioritize convenience and quality over price considerations. Tourism growth contributes additional demand through visitor spending on local dining experiences and cultural food exploration.

Lifestyle changes including longer working hours, dual-income households, and reduced home cooking frequency drive consistent demand for prepared food options. Health consciousness creates opportunities for establishments offering nutritious, transparent, and customizable menu options that align with wellness-focused lifestyles.

Technology advancement enables operational efficiencies, enhanced customer experiences, and new service delivery models that expand market reach and improve profitability. Digital payment systems, mobile ordering platforms, and delivery aggregation services reduce friction in the customer journey while providing valuable data insights for business optimization.

Labor shortages present significant operational challenges across the food service industry, with recruitment and retention difficulties affecting service quality and expansion capabilities. Wage inflation pressures profit margins while competition for skilled workers intensifies among employers seeking to maintain adequate staffing levels.

Regulatory compliance requirements including food safety standards, health regulations, and employment legislation create ongoing operational costs and administrative burdens, particularly for smaller independent operators. Municipal licensing and zoning restrictions limit location flexibility and expansion opportunities in desirable markets.

Supply chain volatility affects ingredient costs, availability, and quality consistency, requiring sophisticated procurement strategies and vendor relationship management. Food cost inflation challenges menu pricing strategies while consumer price sensitivity limits operators’ ability to pass through increased costs.

Market saturation in established urban areas intensifies competition and reduces profitability for new entrants, while real estate costs in prime locations create significant barriers to entry and expansion. Economic uncertainty affects consumer discretionary spending patterns and business investment decisions throughout the industry.

Digital transformation creates substantial opportunities for food service operators to enhance customer engagement, streamline operations, and develop new revenue streams through technology-enabled services. Ghost kitchen concepts and delivery-only operations offer cost-effective expansion models with reduced real estate requirements and operational complexity.

Sustainability initiatives present competitive differentiation opportunities while addressing growing consumer environmental consciousness. Local sourcing partnerships, waste reduction programs, and eco-friendly packaging solutions create brand value and operational efficiencies that appeal to environmentally aware customers.

Franchise development enables rapid market expansion while leveraging proven business models and brand recognition. International cuisine concepts capitalize on Canada’s cultural diversity and consumers’ interest in authentic global dining experiences, creating niche market opportunities for specialized operators.

Health and wellness positioning addresses growing consumer demand for nutritious, functional, and dietary-specific food options. Plant-based alternatives, allergen-free preparations, and nutritionally enhanced menu items create premium pricing opportunities while expanding addressable market segments.

Competitive intensity continues to escalate across all food service segments, driving innovation in menu development, service delivery, and customer experience design. Market consolidation occurs alongside the emergence of new independent concepts, creating a dynamic landscape where established chains compete with agile startup operations.

Consumer expectations evolve rapidly, requiring continuous adaptation in service standards, menu offerings, and operational capabilities. Social media influence amplifies the importance of visual presentation, brand storytelling, and customer experience quality in driving business success and market positioning.

Supply chain relationships become increasingly strategic as operators seek to ensure ingredient quality, cost stability, and supply security. Vertical integration opportunities allow some operators to control key supply chain elements while reducing dependency on external suppliers and improving margin structures.

Technology integration accelerates across operational functions, from kitchen automation and inventory management to customer relationship management and financial analytics. Data-driven decision making enables more precise market targeting, menu optimization, and operational efficiency improvements throughout the industry.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Canada’s food service market dynamics. Primary research includes extensive surveys of industry participants, consumer behavior studies, and in-depth interviews with key stakeholders across various market segments.

Secondary research incorporates analysis of industry reports, government statistics, trade association data, and academic studies to provide comprehensive market context and historical trend analysis. MarkWide Research methodology emphasizes cross-validation of data sources to ensure accuracy and reliability of market insights and projections.

Quantitative analysis utilizes statistical modeling, trend analysis, and forecasting techniques to project market developments and identify growth opportunities. Qualitative assessment includes expert interviews, focus group discussions, and observational research to understand consumer motivations and industry dynamics.

Market segmentation analysis employs demographic, geographic, and behavioral criteria to identify distinct market segments and their respective characteristics. Competitive landscape assessment includes detailed analysis of key market participants, their strategies, and market positioning to understand competitive dynamics and industry structure.

Ontario market leadership reflects the province’s large population base, economic diversity, and concentration of urban centers that support robust food service demand. Toronto metropolitan area serves as a key innovation hub with 35% provincial market share, featuring diverse dining options and high consumer spending on food service experiences.

Quebec’s distinctive market characteristics include strong cultural preferences for local cuisine, artisanal food preparation, and unique regulatory requirements that influence operational strategies. Montreal’s vibrant food scene contributes significantly to provincial food service activity, with particular strength in casual dining and specialty cuisine segments.

Western Canada expansion demonstrates strong growth potential, with Alberta and British Columbia showing 8.5% annual growth rates in food service establishments. Calgary and Vancouver lead regional development through diverse population growth, tourism activity, and strong economic fundamentals supporting discretionary spending.

Atlantic provinces present unique market characteristics with emphasis on seafood specialties, tourism-driven seasonal demand, and strong community-oriented dining traditions. Regional cuisine authenticity creates competitive advantages for local operators while attracting culinary tourism and supporting local economic development initiatives.

Market leadership remains distributed among several categories of operators, each with distinct competitive advantages and market positioning strategies. Established chain restaurants leverage brand recognition, operational scale, and marketing resources to maintain market presence across multiple locations and service formats.

Independent operators compete through specialized cuisine offerings, local market knowledge, and personalized customer service that creates strong community connections. Emerging digital-native brands leverage technology platforms and delivery-focused models to capture market share without traditional real estate investments.

Regional chains balance operational scale with local market adaptation, creating competitive positions that combine brand consistency with regional relevance and customer familiarity.

Service format segmentation reveals distinct market categories with unique operational characteristics, customer bases, and growth trajectories. Quick-service restaurants maintain the largest market segment through convenience positioning, standardized operations, and broad geographic coverage that serves diverse consumer needs.

By Service Type:

By Cuisine Type:

Quick-service dominance continues through operational efficiency, brand recognition, and convenience positioning that aligns with contemporary consumer lifestyles. Drive-through capabilities and mobile ordering integration enhance accessibility while reducing labor requirements and improving customer throughput during peak periods.

Full-service restaurants adapt through enhanced value propositions, experiential dining concepts, and technology integration that improves service efficiency without compromising hospitality quality. Casual dining segments show particular resilience through family-friendly positioning and diverse menu offerings that appeal to broad demographic groups.

Institutional food service demonstrates steady growth through healthcare expansion, educational facility development, and corporate catering demand. Contract food service providers leverage operational expertise and purchasing scale to serve large institutional clients while maintaining quality standards and cost efficiency.

Specialty segments including food trucks, pop-up concepts, and niche cuisine providers create market diversity while serving specific consumer preferences and dietary requirements. Artisanal food preparation and locally sourced ingredients command premium pricing in selective market segments focused on quality and authenticity.

Operational stakeholders benefit from comprehensive market insights that inform strategic planning, location selection, and competitive positioning decisions. Investment opportunities become more apparent through detailed analysis of growth segments, emerging trends, and market gaps that present development potential.

Franchise development benefits from market analysis that identifies optimal expansion territories, demographic targets, and competitive landscapes for successful brand extension. Supplier relationships improve through understanding of industry demand patterns, quality requirements, and procurement trends that influence supply chain strategies.

Financial institutions gain valuable insights for lending decisions, investment evaluations, and risk assessment related to food service business opportunities. Real estate developers utilize market intelligence to optimize retail space planning, tenant mix strategies, and location development priorities.

Technology providers identify market opportunities for solutions addressing operational efficiency, customer experience enhancement, and digital transformation requirements across various food service segments. Regulatory bodies benefit from industry trend analysis that informs policy development and regulatory framework adaptation.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital-first strategies transform traditional food service operations through mobile ordering, contactless payment, and delivery integration that enhances customer convenience while improving operational efficiency. Ghost kitchen proliferation enables cost-effective market entry and expansion without traditional real estate constraints.

Sustainability initiatives gain prominence as consumers increasingly value environmental responsibility in their dining choices. Local sourcing programs, compostable packaging, and waste reduction efforts become competitive differentiators while supporting operational cost management and brand positioning.

Health-conscious menu development responds to growing consumer awareness of nutrition and dietary requirements. Plant-based alternatives, allergen-free options, and transparent ingredient labeling create market opportunities while addressing diverse consumer needs and preferences.

Experience-driven concepts emphasize unique dining environments, interactive elements, and social media-worthy presentations that encourage customer engagement and word-of-mouth marketing. Personalization capabilities through technology enable customized menu recommendations and tailored service experiences that build customer loyalty.

Technology adoption acceleration includes widespread implementation of point-of-sale systems, inventory management software, and customer relationship management platforms that improve operational efficiency and data-driven decision making. Artificial intelligence integration enables predictive analytics for demand forecasting and menu optimization.

Delivery ecosystem expansion through third-party platforms and proprietary delivery services creates new revenue streams while expanding market reach beyond traditional geographic boundaries. MWR analysis indicates that delivery services now represent a significant portion of total food service transactions across major metropolitan areas.

Workforce development initiatives address labor shortages through enhanced training programs, competitive compensation packages, and career advancement opportunities that improve employee retention and service quality. Automation investments in kitchen equipment and service processes reduce labor dependency while maintaining operational consistency.

Regulatory adaptations include updated food safety protocols, accessibility requirements, and environmental standards that influence operational procedures and facility design. Municipal support programs for small business development create opportunities for independent operators and local economic development.

Strategic positioning should emphasize differentiation through unique value propositions, whether through cuisine specialization, service innovation, or customer experience enhancement. Market research indicates that successful operators focus on specific customer segments rather than attempting to serve all market demographics equally.

Technology investment priorities should include customer-facing solutions that improve convenience and engagement, as well as back-office systems that enhance operational efficiency and data analytics capabilities. Digital marketing strategies become increasingly important for customer acquisition and retention in competitive markets.

Financial management requires careful attention to cost control, particularly labor and food costs, while maintaining quality standards and customer satisfaction. Revenue diversification through multiple service channels reduces dependency on single revenue streams and improves business resilience.

Partnership development with suppliers, technology providers, and delivery platforms creates operational advantages and market opportunities. Community engagement builds local market presence and customer loyalty while supporting long-term business sustainability and growth.

Growth projections for Canada’s food service market remain optimistic, supported by favorable demographic trends, continued urbanization, and evolving consumer preferences that favor convenient dining solutions. Technology integration will continue driving operational improvements and customer experience enhancements across all market segments.

Market evolution toward more sustainable, health-conscious, and personalized dining experiences creates opportunities for operators who successfully adapt to changing consumer expectations. MarkWide Research forecasts continued growth in delivery services, with penetration rates expected to reach 40% of total transactions in major urban markets within the next five years.

Innovation cycles will accelerate as competition intensifies and consumer preferences continue evolving. Successful operators will demonstrate agility in menu development, service delivery, and technology adoption while maintaining operational efficiency and profitability.

Regional expansion opportunities exist in underserved markets, while established urban areas will see continued competition and market share battles. Consolidation trends may emerge as smaller operators seek scale advantages through acquisition or franchise relationships with established brands.

Canada’s food service market demonstrates remarkable resilience and adaptability, positioning itself for continued growth despite various operational challenges and competitive pressures. The industry’s ability to embrace technological innovation, respond to changing consumer preferences, and maintain operational excellence creates a foundation for sustained market expansion and development.

Strategic opportunities abound for operators who successfully balance traditional hospitality values with modern convenience expectations, while maintaining focus on quality, sustainability, and customer satisfaction. The market’s diversity across service formats, cuisine types, and regional preferences ensures multiple pathways for business success and growth.

Future success will depend on operators’ ability to adapt quickly to market changes, invest strategically in technology and workforce development, and maintain strong customer relationships through exceptional service delivery. The Canadian food service market’s continued evolution promises exciting opportunities for industry participants who embrace innovation while honoring the fundamental principles of hospitality and customer service excellence.

What is Canada Food Service?

Canada Food Service refers to the sector that encompasses businesses providing food and beverage services to consumers outside of their homes, including restaurants, cafes, catering services, and institutional food services.

What are the key players in the Canada Food Service Market?

Key players in the Canada Food Service Market include companies like Restaurant Brands International, Tim Hortons, and A&W Food Services of Canada, among others.

What are the main drivers of growth in the Canada Food Service Market?

The main drivers of growth in the Canada Food Service Market include increasing consumer demand for convenience, the rise of food delivery services, and a growing trend towards dining out and experiencing diverse cuisines.

What challenges does the Canada Food Service Market face?

Challenges in the Canada Food Service Market include rising food costs, labor shortages, and increased competition from fast-casual dining options and delivery services.

What opportunities exist in the Canada Food Service Market?

Opportunities in the Canada Food Service Market include the expansion of plant-based menu options, the integration of technology for online ordering, and the potential for growth in health-conscious dining experiences.

What trends are shaping the Canada Food Service Market?

Trends shaping the Canada Food Service Market include a focus on sustainability, the use of locally sourced ingredients, and the increasing popularity of food trucks and pop-up dining experiences.

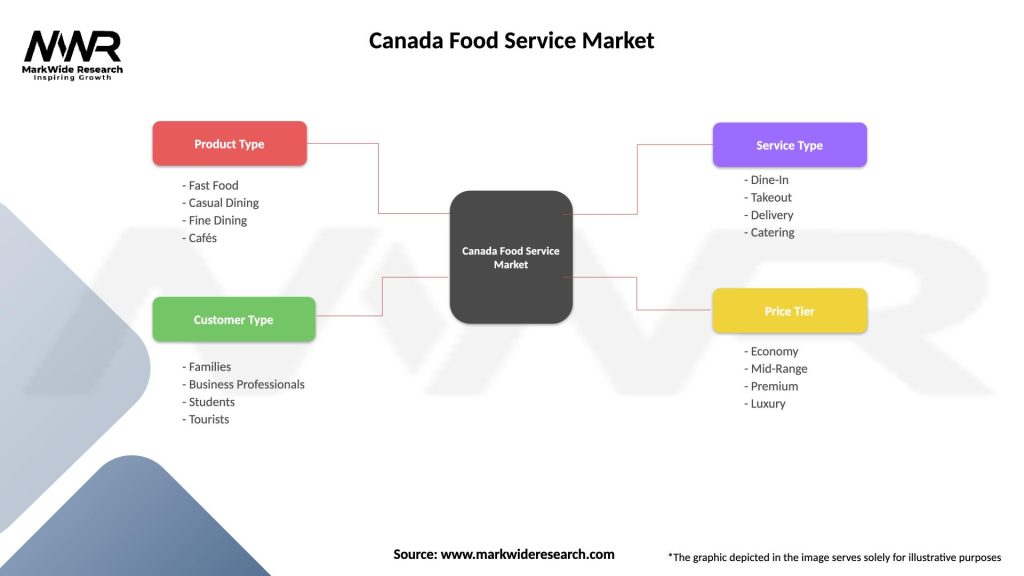

Canada Food Service Market

| Segmentation Details | Description |

|---|---|

| Product Type | Fast Food, Casual Dining, Fine Dining, Cafés |

| Customer Type | Families, Business Professionals, Students, Tourists |

| Service Type | Dine-In, Takeout, Delivery, Catering |

| Price Tier | Economy, Mid-Range, Premium, Luxury |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Canada Food Service Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.