444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Bulgaria container glass market represents a dynamic and evolving sector within the country’s manufacturing landscape, characterized by robust growth and increasing demand across multiple industries. Container glass manufacturing in Bulgaria has experienced significant transformation over the past decade, driven by expanding beverage industries, pharmaceutical applications, and sustainable packaging trends. The market demonstrates strong fundamentals with annual growth rates reaching approximately 6.2% CAGR, positioning Bulgaria as an emerging hub for glass container production in Southeast Europe.

Market dynamics indicate substantial opportunities for both domestic and international players, with the country’s strategic location providing advantageous access to European and Middle Eastern markets. The Bulgarian container glass industry benefits from abundant raw materials, skilled workforce, and supportive government policies promoting manufacturing excellence. Key applications span across beverage bottles, food jars, pharmaceutical containers, and specialty glass packaging solutions.

Industrial infrastructure supporting container glass production has undergone modernization, with several facilities implementing advanced furnace technologies and automated production lines. The market’s resilience stems from diverse end-user segments, including alcoholic beverages, soft drinks, food preservation, and pharmaceutical packaging, each contributing to sustained demand growth.

The Bulgaria container glass market refers to the comprehensive ecosystem encompassing the production, distribution, and consumption of glass containers manufactured within Bulgarian territory for various packaging applications. This market includes all forms of hollow glass products designed for containing liquids, solids, and other materials across industrial, commercial, and consumer segments.

Container glass manufacturing involves the transformation of raw materials including silica sand, soda ash, limestone, and cullet through high-temperature melting processes to create bottles, jars, vials, and specialized containers. The Bulgarian market specifically encompasses domestic production facilities, import-export activities, and the entire value chain from raw material sourcing to end-user delivery.

Market scope extends beyond traditional beverage containers to include pharmaceutical vials, cosmetic bottles, food preservation jars, and industrial containers. The definition encompasses both clear and colored glass varieties, with varying sizes, shapes, and technical specifications tailored to specific industry requirements and consumer preferences.

Bulgaria’s container glass market demonstrates exceptional growth potential, driven by expanding beverage consumption, pharmaceutical industry development, and increasing preference for sustainable packaging solutions. The market benefits from strategic geographical positioning, competitive manufacturing costs, and growing export opportunities to neighboring European markets.

Key market drivers include rising demand for premium alcoholic beverages, expanding soft drink consumption, and pharmaceutical industry growth requiring specialized glass containers. The market shows particular strength in beer bottle production, wine packaging, and pharmaceutical vials, with beverage applications representing approximately 72% market share of total container glass demand.

Competitive landscape features both domestic manufacturers and international players establishing production facilities to serve regional markets. Investment in modern furnace technologies and automated production systems has enhanced quality standards and production efficiency, positioning Bulgarian manufacturers competitively in European markets.

Future prospects remain highly favorable, with projected growth driven by sustainability trends, circular economy initiatives, and expanding export opportunities. The market’s evolution toward premium packaging solutions and specialized applications presents significant opportunities for value-added growth and market expansion.

Strategic market insights reveal several critical factors shaping the Bulgaria container glass market’s trajectory and competitive positioning:

Primary market drivers propelling the Bulgaria container glass market include robust beverage industry expansion, pharmaceutical sector growth, and increasing consumer preference for sustainable packaging solutions. The alcoholic beverage segment particularly drives demand, with Bulgaria’s wine and beer industries experiencing significant growth and requiring quality glass containers for premium product positioning.

Sustainability trends represent a fundamental driver, as consumers and businesses increasingly prioritize environmentally responsible packaging options. Glass containers offer complete recyclability and premium product presentation, making them preferred choices for quality-conscious brands. The circular economy movement has strengthened glass packaging adoption across multiple industries.

Export opportunities serve as major growth catalysts, with Bulgarian manufacturers leveraging competitive production costs and strategic location to serve European markets. The country’s EU membership facilitates trade relationships and market access, enabling manufacturers to compete effectively in regional markets.

Pharmaceutical industry expansion creates specialized demand for high-quality glass containers, including vials, ampoules, and bottles meeting stringent regulatory requirements. This segment offers higher value-added opportunities and stable long-term demand patterns, contributing to market diversification and profitability enhancement.

Market restraints affecting the Bulgaria container glass market include intense competition from alternative packaging materials, energy cost fluctuations, and regulatory compliance requirements. Plastic packaging alternatives continue challenging glass containers in certain applications, particularly where weight and transportation costs are primary considerations.

Energy costs represent significant operational challenges, as glass manufacturing requires substantial energy inputs for furnace operations. Fluctuating energy prices impact production costs and profit margins, requiring manufacturers to implement energy efficiency measures and explore alternative energy sources.

Raw material availability and pricing volatility create operational uncertainties, particularly for specialized glass types requiring specific material compositions. Supply chain disruptions and transportation costs can affect production schedules and competitive positioning in price-sensitive market segments.

Environmental regulations impose compliance costs and operational requirements, though they simultaneously create opportunities for sustainable packaging solutions. Manufacturers must invest in emission control technologies and waste management systems to meet evolving environmental standards.

Significant market opportunities exist in premium packaging segments, pharmaceutical applications, and export market expansion. The growing demand for premium alcoholic beverages creates opportunities for specialized bottle designs and high-quality glass containers that enhance product presentation and brand positioning.

Pharmaceutical sector growth presents substantial opportunities for manufacturers capable of meeting stringent quality requirements and regulatory standards. This segment offers higher margins and stable demand patterns, making it attractive for long-term business development and market diversification strategies.

Export market development represents major growth potential, with Bulgarian manufacturers well-positioned to serve European markets through competitive pricing and quality products. Strategic partnerships and distribution agreements can facilitate market entry and expansion in target regions.

Sustainability initiatives create opportunities for innovation in recycled content utilization, energy-efficient production processes, and circular economy solutions. Companies investing in sustainable technologies can differentiate themselves and capture environmentally conscious market segments while potentially accessing green financing and incentives.

Market dynamics in the Bulgaria container glass sector reflect complex interactions between supply-side capabilities, demand-side requirements, and external economic factors. Production efficiency improvements through technological advancement have enhanced competitiveness, with manufacturers achieving productivity gains of approximately 15-20% through automation and process optimization.

Demand patterns show seasonal variations aligned with beverage consumption cycles, requiring manufacturers to optimize production planning and inventory management. The market demonstrates resilience through diversified application segments, reducing dependence on any single industry vertical.

Competitive dynamics involve both domestic and international players, with market consolidation trends creating opportunities for strategic partnerships and acquisitions. MarkWide Research analysis indicates increasing collaboration between manufacturers and end-users to develop customized packaging solutions meeting specific market requirements.

Supply chain optimization has become critical for maintaining competitive advantages, with manufacturers investing in logistics infrastructure and raw material sourcing strategies. The integration of digital technologies in production planning and quality control systems enhances operational efficiency and customer satisfaction.

Research methodology for analyzing the Bulgaria container glass market employs comprehensive data collection techniques, including primary research through industry interviews, secondary research from authoritative sources, and quantitative analysis of market trends and patterns.

Primary research activities include structured interviews with key industry stakeholders, including manufacturers, suppliers, distributors, and end-users. These interactions provide insights into market dynamics, competitive positioning, and future growth prospects from multiple perspectives across the value chain.

Secondary research encompasses analysis of industry reports, government statistics, trade association data, and company financial information. This approach ensures comprehensive coverage of market factors and validation of primary research findings through multiple data sources.

Quantitative analysis involves statistical modeling of market trends, growth projections, and segment analysis. Data validation processes ensure accuracy and reliability of market insights, supporting strategic decision-making for industry participants and stakeholders.

Regional analysis of the Bulgaria container glass market reveals concentrated production activities in key industrial zones, with Sofia region accounting for approximately 35% of production capacity, followed by Plovdiv and Varna regions contributing significantly to overall market output.

Sofia metropolitan area benefits from proximity to major beverage manufacturers and pharmaceutical companies, creating synergistic relationships between glass container producers and end-users. The region’s infrastructure advantages include transportation networks, skilled workforce availability, and access to raw materials.

Plovdiv region demonstrates strong manufacturing capabilities with several established glass production facilities serving both domestic and export markets. The area’s industrial heritage and technical expertise support continued growth in container glass manufacturing activities.

Coastal regions including Varna and Burgas offer strategic advantages for export-oriented operations, with port facilities enabling efficient product distribution to international markets. These areas show increasing investment in glass manufacturing infrastructure to support export growth initiatives.

Competitive landscape in the Bulgaria container glass market features both established domestic manufacturers and international companies with local operations. The market structure supports healthy competition while enabling collaboration opportunities for technology transfer and market development.

Market competition drives continuous innovation in product design, production efficiency, and customer service. Companies differentiate through quality certifications, technical capabilities, and specialized applications serving specific industry requirements.

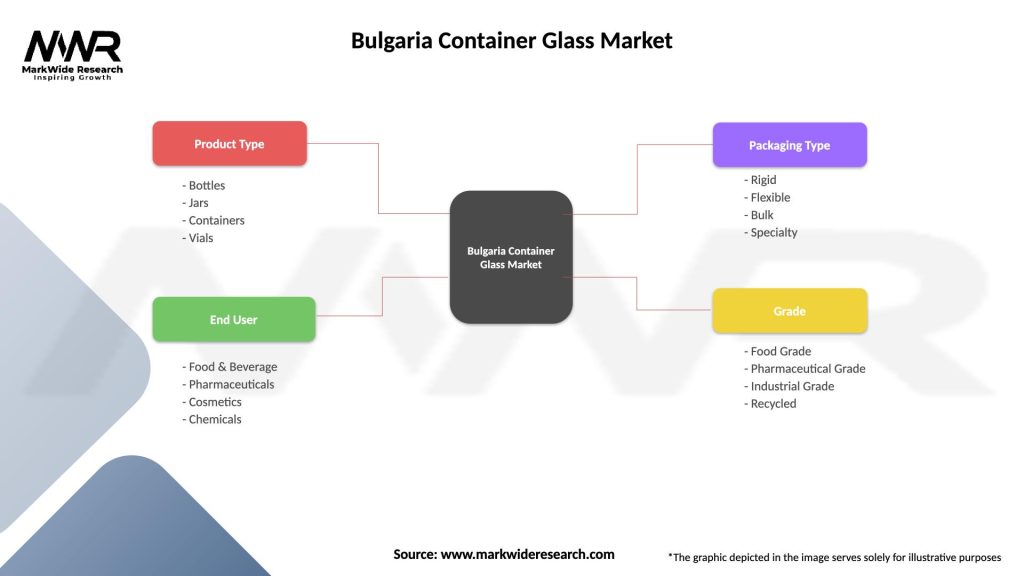

Market segmentation of the Bulgaria container glass market encompasses multiple classification criteria, including product type, application, end-user industry, and distribution channel. This comprehensive segmentation enables targeted analysis and strategic planning for market participants.

By Product Type:

By Application:

Beverage containers dominate the Bulgaria container glass market, with beer bottles representing approximately 45% of beverage segment demand. This category benefits from Bulgaria’s growing beer consumption and export activities, requiring consistent quality and competitive pricing to maintain market position.

Wine packaging shows strong growth potential, aligned with Bulgaria’s expanding wine industry and increasing international recognition of Bulgarian wines. Premium wine bottles require specialized glass characteristics and aesthetic appeal, creating opportunities for value-added manufacturing.

Pharmaceutical containers represent a high-value segment with stringent quality requirements and regulatory compliance needs. This category offers stable demand patterns and higher profit margins, making it attractive for manufacturers with appropriate technical capabilities and certifications.

Food packaging applications demonstrate steady growth driven by processed food consumption and preservation requirements. Jars and specialty containers for food applications require specific glass compositions and manufacturing standards to ensure product safety and quality.

Industry participants in the Bulgaria container glass market benefit from strategic geographical positioning, competitive manufacturing costs, and access to both domestic and international markets. Manufacturers leverage skilled workforce availability, established infrastructure, and supportive business environment to achieve operational efficiency and market competitiveness.

End-users benefit from reliable supply chains, quality products meeting international standards, and competitive pricing structures. The proximity of manufacturing facilities to major consumption centers reduces transportation costs and enables responsive customer service.

Investors find attractive opportunities in market growth potential, export expansion possibilities, and increasing demand for sustainable packaging solutions. The market’s diversification across multiple application segments reduces investment risks while providing multiple growth avenues.

Government stakeholders benefit from industrial development, employment creation, and export revenue generation. The container glass industry contributes to economic development while supporting environmental sustainability through recyclable packaging solutions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration represents the most significant trend shaping the Bulgaria container glass market, with manufacturers increasing recycled content utilization by approximately 25-30% in recent years. This trend aligns with circular economy principles and consumer preferences for environmentally responsible packaging solutions.

Automation advancement continues transforming production processes, with manufacturers implementing robotic systems and digital quality control technologies. These investments enhance production efficiency, reduce labor costs, and improve product consistency meeting international quality standards.

Premium packaging demand shows strong growth, particularly in alcoholic beverage and cosmetic applications. Consumers increasingly associate glass packaging with product quality and brand prestige, driving demand for specialized designs and high-quality finishes.

Export market expansion represents a key strategic trend, with Bulgarian manufacturers developing distribution networks and partnerships in European markets. MWR data indicates growing export volumes reflecting improved quality recognition and competitive positioning in international markets.

Recent industry developments highlight significant investments in production capacity expansion and technology modernization. Several manufacturers have announced facility upgrades incorporating advanced furnace technologies and automated production systems to enhance competitiveness and quality standards.

Strategic partnerships between Bulgarian manufacturers and international companies have facilitated technology transfer and market access opportunities. These collaborations enable knowledge sharing and best practice implementation while expanding market reach and customer base.

Sustainability initiatives include investments in energy-efficient production technologies and increased utilization of recycled glass materials. These developments align with environmental regulations and market demands for sustainable packaging solutions.

Market consolidation activities involve mergers and acquisitions aimed at achieving economies of scale and expanding product portfolios. These developments strengthen competitive positioning while enabling investment in advanced technologies and market development initiatives.

Strategic recommendations for Bulgaria container glass market participants emphasize the importance of export market development, technology investment, and sustainability integration. MarkWide Research analysis suggests focusing on premium packaging segments and specialized applications to achieve higher value-added growth.

Technology modernization should prioritize energy efficiency improvements and automation systems to enhance competitiveness and reduce operational costs. Investment in digital technologies and Industry 4.0 solutions can provide significant competitive advantages in quality control and production optimization.

Market diversification strategies should explore pharmaceutical and specialty applications offering higher margins and stable demand patterns. Building technical capabilities and quality certifications for these segments can create sustainable competitive advantages.

Sustainability leadership presents opportunities for market differentiation and customer loyalty development. Companies investing in circular economy solutions and environmental responsibility can capture growing market segments while potentially accessing green financing and incentives.

Future outlook for the Bulgaria container glass market remains highly positive, with projected growth driven by expanding export opportunities, sustainability trends, and increasing demand for premium packaging solutions. The market is expected to maintain steady growth rates of approximately 5-7% annually over the next five years.

Export expansion will likely drive significant growth, with Bulgarian manufacturers well-positioned to serve European markets through competitive pricing and improving quality standards. Strategic partnerships and distribution agreements will facilitate market entry and expansion in target regions.

Technology advancement will continue transforming production processes, with increased automation and digital integration enhancing efficiency and quality. Investment in sustainable technologies will become increasingly important for market competitiveness and regulatory compliance.

Market evolution toward premium and specialized applications will create opportunities for value-added growth and differentiation. Companies successfully adapting to changing market requirements and customer preferences will achieve sustainable competitive advantages and profitable growth.

The Bulgaria container glass market represents a vital component of the country’s packaging industry, driven by beverage production growth, food processing expansion, and increasing demand for sustainable packaging solutions across domestic and export markets. Market dynamics demonstrate steady growth potential supported by wine industry development, craft beverage sector emergence, and pharmaceutical packaging requirements throughout Bulgaria. Manufacturing capabilities and strategic geographic positioning continue supporting both local market service and regional export opportunities across Southeast Europe and neighboring markets.

Strategic positioning in this established market requires understanding diverse application requirements, quality standards, and sustainability expectations from beverage producers, food manufacturers, and pharmaceutical companies. Companies that prioritize production efficiency, customization capabilities, and environmental responsibility will be best positioned to maintain competitive advantage in this mature sector. Technology modernization and energy-efficient furnace operations have become essential for cost competitiveness and environmental compliance in modern glass manufacturing operations.

Industry excellence in lightweight bottle design, quality consistency, and rapid production changeovers positions Bulgarian manufacturers to serve demanding beverage and food sectors requiring reliable packaging supply. Sustainability initiatives including cullet recycling, renewable energy adoption, and emission reduction programs align with European environmental regulations and corporate responsibility expectations. Market diversification across wine bottles, beer containers, spirits packaging, and specialty food jars provides stability against sector-specific demand fluctuations.

The competitive environment remains influenced by both domestic production capacity and imported container glass from regional manufacturers in neighboring countries. Long-term success will require ongoing investment in furnace modernization, automation technologies, and quality assurance systems to meet evolving customer requirements and maintain cost competitiveness. Customer-focused approaches emphasizing reliable supply, technical support, and collaborative design development will become increasingly important differentiators in this essential and continually evolving Bulgaria container glass market.

What is Container Glass?

Container glass refers to glass products designed for packaging and storing various goods, including beverages, food, and pharmaceuticals. It is known for its durability, recyclability, and ability to preserve the quality of its contents.

What are the key players in the Bulgaria Container Glass Market?

Key players in the Bulgaria Container Glass Market include companies like Stirol, O-I Manufacturing, and Verallia, which are known for their production of glass containers for food and beverage industries, among others.

What are the growth factors driving the Bulgaria Container Glass Market?

The Bulgaria Container Glass Market is driven by increasing consumer demand for sustainable packaging solutions, the growth of the beverage industry, and a rising preference for glass over plastic due to health and environmental concerns.

What challenges does the Bulgaria Container Glass Market face?

Challenges in the Bulgaria Container Glass Market include high production costs, competition from alternative packaging materials, and the need for significant energy consumption during manufacturing processes.

What opportunities exist in the Bulgaria Container Glass Market?

Opportunities in the Bulgaria Container Glass Market include the expansion of the e-commerce sector, which increases demand for packaging, and innovations in glass recycling technologies that enhance sustainability.

What trends are shaping the Bulgaria Container Glass Market?

Trends in the Bulgaria Container Glass Market include a shift towards lightweight glass containers, increased use of decorative glass packaging, and a growing emphasis on eco-friendly production practices.

Bulgaria Container Glass Market

| Segmentation Details | Description |

|---|---|

| Product Type | Bottles, Jars, Containers, Vials |

| End User | Food & Beverage, Pharmaceuticals, Cosmetics, Chemicals |

| Packaging Type | Rigid, Flexible, Bulk, Specialty |

| Grade | Food Grade, Pharmaceutical Grade, Industrial Grade, Recycled |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Bulgaria Container Glass Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.