444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Brazil oral anti-diabetic drug market represents a critical segment of the nation’s pharmaceutical landscape, addressing the growing prevalence of diabetes mellitus across the country. Brazil’s healthcare system faces mounting pressure to provide effective diabetes management solutions as the condition affects millions of citizens nationwide. The market encompasses various therapeutic classes including metformin, sulfonylureas, DPP-4 inhibitors, SGLT-2 inhibitors, and combination therapies that serve as first-line and adjunctive treatments for type 2 diabetes.

Market dynamics indicate robust growth driven by increasing diabetes prevalence, with approximately 16.8 million adults currently diagnosed with diabetes in Brazil. The oral anti-diabetic segment benefits from enhanced accessibility compared to injectable alternatives, making these medications the preferred initial treatment approach for most patients. Healthcare infrastructure improvements and expanded insurance coverage through Brazil’s Unified Health System (SUS) have significantly increased patient access to essential diabetes medications.

Pharmaceutical innovation continues to reshape the therapeutic landscape, with newer drug classes offering improved efficacy profiles and reduced side effects. The market demonstrates strong adoption of combination therapies that provide enhanced glycemic control while simplifying dosing regimens for patients. Generic drug penetration remains substantial, accounting for approximately 78% of total prescriptions, reflecting Brazil’s cost-conscious healthcare approach and regulatory support for biosimilar medications.

The Brazil oral anti-diabetic drug market refers to the comprehensive pharmaceutical sector focused on manufacturing, distributing, and commercializing oral medications specifically designed to manage blood glucose levels in diabetic patients throughout Brazil. This market encompasses prescription medications that work through various mechanisms including insulin sensitization, glucose absorption inhibition, insulin secretion enhancement, and incretin pathway modulation.

Therapeutic classifications within this market include biguanides like metformin, sulfonylureas such as glimepiride, thiazolidinediones including pioglitazone, DPP-4 inhibitors like sitagliptin, SGLT-2 inhibitors such as empagliflozin, and alpha-glucosidase inhibitors including acarbose. Combination products represent an increasingly important segment, offering fixed-dose combinations that improve patient adherence while providing synergistic therapeutic benefits.

Brazil’s oral anti-diabetic drug market demonstrates exceptional growth potential driven by demographic shifts, lifestyle changes, and improved healthcare access. The market benefits from a large patient population requiring long-term medication management, creating sustained demand for effective oral therapies. Government initiatives supporting diabetes care through public health programs and medication subsidies have expanded treatment accessibility across diverse socioeconomic segments.

Key market drivers include rising diabetes prevalence, with incidence rates increasing by approximately 3.2% annually among adults aged 20-79 years. The market experiences strong demand for newer therapeutic classes that offer improved safety profiles and cardiovascular benefits. Healthcare digitization and telemedicine adoption have enhanced patient monitoring capabilities, supporting better medication adherence and treatment outcomes.

Competitive dynamics feature both multinational pharmaceutical companies and domestic manufacturers competing across price segments. The market shows increasing preference for personalized treatment approaches that consider individual patient characteristics, comorbidities, and lifestyle factors. Regulatory support from ANVISA continues to facilitate market access for innovative therapies while maintaining rigorous safety standards.

Strategic market insights reveal several critical trends shaping Brazil’s oral anti-diabetic drug landscape:

Diabetes prevalence escalation serves as the primary market driver, with Brazil ranking among the top five countries globally for diabetes burden. Lifestyle factors including urbanization, dietary changes, and reduced physical activity contribute to increasing type 2 diabetes incidence across all age groups. The condition’s chronic nature requires lifelong medication management, creating sustained market demand for effective oral therapies.

Healthcare infrastructure development expands treatment accessibility through improved primary care networks and specialized diabetes clinics. Government health initiatives including the National Diabetes Program provide medication subsidies and patient education resources, reducing financial barriers to treatment access. Insurance coverage expansion through both public and private systems increases patient affordability for newer, more expensive therapeutic options.

Pharmaceutical innovation drives market growth through development of more effective medications with improved safety profiles. Combination therapies address multiple pathophysiological mechanisms simultaneously, offering superior glycemic control compared to monotherapy approaches. Patient preference for oral medications over injectable alternatives supports continued market expansion, particularly among newly diagnosed patients seeking convenient treatment options.

Healthcare professional education and clinical guideline updates promote evidence-based prescribing practices that optimize patient outcomes. Digital health integration enables better patient monitoring and medication adherence support, improving treatment effectiveness and reducing complications. Economic factors including healthcare cost containment efforts favor oral therapies due to their generally lower acquisition costs compared to newer injectable alternatives.

Economic constraints significantly impact market growth, particularly affecting patient access to newer, more expensive therapeutic options. Healthcare budget limitations within Brazil’s public health system restrict formulary inclusion of innovative medications, limiting treatment options for economically disadvantaged populations. Currency fluctuations affect imported pharmaceutical pricing, creating affordability challenges for patients requiring specific branded medications.

Regulatory complexities can delay market entry for new therapeutic options, limiting physician prescribing choices and patient access to innovative treatments. ANVISA approval processes require extensive clinical data demonstrating safety and efficacy in Brazilian populations, potentially extending time-to-market for new medications. Pricing negotiations between manufacturers and government agencies can result in lengthy delays before new therapies become commercially available.

Healthcare infrastructure limitations in rural and remote regions restrict patient access to specialized diabetes care and medication distribution networks. Physician shortage in certain geographic areas limits proper diabetes management and medication optimization, potentially reducing treatment effectiveness. Patient education gaps regarding proper medication use and lifestyle modifications can compromise treatment outcomes and medication adherence rates.

Side effect profiles of certain oral anti-diabetic medications may limit their use in specific patient populations, particularly those with cardiovascular or renal comorbidities. Drug interactions with commonly prescribed medications can restrict therapeutic options for patients with multiple chronic conditions. Generic quality concerns occasionally arise, potentially affecting physician and patient confidence in lower-cost therapeutic alternatives.

Emerging therapeutic classes present significant growth opportunities, particularly medications offering cardiovascular and renal protective benefits beyond glycemic control. Personalized medicine approaches enable tailored treatment selection based on individual patient characteristics, genetic factors, and comorbidity profiles. Digital therapeutics integration creates opportunities for comprehensive diabetes management platforms combining medication therapy with lifestyle interventions and remote monitoring capabilities.

Rural market expansion offers substantial growth potential through improved distribution networks and telemedicine-supported care delivery models. Preventive care initiatives targeting pre-diabetic populations could expand the addressable market while reducing long-term healthcare costs. Combination therapy development continues to present opportunities for innovative fixed-dose formulations that improve patient convenience and adherence rates.

Healthcare technology integration enables development of smart medication delivery systems and adherence monitoring solutions. Public-private partnerships can facilitate expanded access to innovative therapies while maintaining cost-effectiveness for healthcare systems. Medical education programs targeting healthcare professionals can improve prescribing practices and optimize patient outcomes across diverse therapeutic options.

Biosimilar development for complex oral anti-diabetic medications presents opportunities to reduce treatment costs while maintaining therapeutic efficacy. Patient support programs can improve medication adherence and treatment persistence, ultimately enhancing clinical outcomes and reducing diabetes-related complications. International collaboration in clinical research can accelerate development of therapies specifically designed for Brazilian patient populations and healthcare system requirements.

Supply chain dynamics within Brazil’s oral anti-diabetic drug market reflect complex interactions between international pharmaceutical manufacturers, domestic producers, and distribution networks. Manufacturing capabilities have expanded significantly, with several multinational companies establishing local production facilities to reduce costs and improve supply chain reliability. Distribution networks continue evolving to better serve diverse geographic regions, with particular focus on improving rural accessibility.

Pricing dynamics demonstrate ongoing tension between innovation incentives and affordability requirements. Government price controls through CMED (Medication Market Regulation Chamber) influence manufacturer pricing strategies while ensuring patient access to essential medications. Generic competition intensifies as patents expire on major branded products, creating opportunities for cost savings while maintaining therapeutic effectiveness.

Prescribing patterns show increasing sophistication as healthcare professionals adopt evidence-based treatment algorithms considering patient-specific factors. Clinical guidelines from Brazilian diabetes societies influence prescribing practices, promoting optimal therapeutic selection based on individual patient characteristics and comorbidities. Patient preferences increasingly factor into treatment decisions, with convenience and side effect profiles playing important roles in medication selection.

Regulatory dynamics continue evolving to balance innovation promotion with patient safety requirements. ANVISA initiatives streamline approval processes for medications addressing unmet medical needs while maintaining rigorous safety standards. Pharmacovigilance systems monitor real-world medication safety and effectiveness, providing valuable data for ongoing therapeutic optimization and regulatory decision-making.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Brazil’s oral anti-diabetic drug market. Primary research includes extensive interviews with key stakeholders including healthcare professionals, pharmaceutical executives, regulatory officials, and patient advocacy groups. Healthcare provider surveys capture prescribing patterns, treatment preferences, and perceived barriers to optimal diabetes management across diverse clinical settings.

Secondary research incorporates analysis of government health databases, pharmaceutical sales data, clinical literature, and regulatory filings. Market intelligence gathering includes monitoring of competitor activities, product launches, pricing changes, and strategic partnerships within the Brazilian pharmaceutical landscape. Patient databases provide insights into treatment patterns, medication adherence rates, and clinical outcomes across different therapeutic approaches.

Quantitative analysis employs statistical modeling to project market trends, growth rates, and competitive dynamics. Qualitative research explores underlying market drivers, barriers, and opportunities through in-depth stakeholder interviews and focus group discussions. Regulatory analysis examines policy changes, reimbursement decisions, and their potential impact on market access and competitive positioning.

Data validation processes ensure accuracy and reliability through triangulation of multiple information sources and expert review. Market modeling incorporates demographic trends, epidemiological data, and healthcare utilization patterns to project future market evolution. Scenario analysis evaluates potential market outcomes under different regulatory, economic, and competitive conditions to provide comprehensive strategic insights.

Southeast region dominates Brazil’s oral anti-diabetic drug market, accounting for approximately 45% of total consumption due to high population density and advanced healthcare infrastructure. São Paulo state leads in both patient volume and pharmaceutical distribution networks, benefiting from proximity to major manufacturing facilities and research institutions. Rio de Janeiro demonstrates strong market presence with well-established diabetes care centers and comprehensive insurance coverage supporting patient access to innovative therapies.

Northeast region represents significant growth potential with approximately 28% market share and rapidly improving healthcare infrastructure. Bahia and Pernambuco show increasing diabetes prevalence rates correlating with urbanization and lifestyle changes. Government investment in regional healthcare facilities and medication distribution networks supports expanding access to oral anti-diabetic therapies across diverse socioeconomic populations.

South region maintains 18% market share with high-quality healthcare systems and strong physician education programs promoting evidence-based diabetes management. Rio Grande do Sul demonstrates particularly high adoption rates for newer therapeutic classes, reflecting advanced clinical practices and patient education initiatives. Regional pharmaceutical manufacturing capabilities support local supply chain efficiency and competitive pricing for generic medications.

Central-West region shows 6% market share with growing opportunities driven by agricultural prosperity and healthcare infrastructure development. Brasília’s federal district benefits from government employee health insurance programs providing comprehensive diabetes medication coverage. North region represents 3% market share with significant accessibility challenges but substantial growth potential as infrastructure improvements continue expanding healthcare reach to remote populations.

Market leadership reflects diverse competitive dynamics between multinational pharmaceutical companies and domestic manufacturers across different therapeutic segments. Key market participants demonstrate varying strategies focused on innovation, cost-effectiveness, and market access optimization:

Competitive strategies emphasize differentiation through clinical outcomes, patient support programs, and healthcare professional education initiatives. Market access capabilities including government relations and reimbursement expertise significantly influence competitive positioning. Innovation pipelines focus on combination therapies, improved formulations, and patient convenience enhancements to maintain competitive advantages in evolving market conditions.

Therapeutic class segmentation reveals distinct market dynamics across different medication categories:

By Drug Class:

By Patient Demographics:

By Healthcare Setting:

Metformin category maintains dominant market position due to established efficacy, safety profile, and cost-effectiveness. Extended-release formulations show increasing adoption rates as they improve patient tolerability and adherence compared to immediate-release versions. Generic competition remains intense with multiple manufacturers offering bioequivalent formulations at competitive pricing points.

DPP-4 inhibitor category demonstrates steady growth driven by weight-neutral effects and low hypoglycemia risk. Combination products with metformin show particularly strong adoption among treatment-experienced patients requiring intensified therapy. Patent expirations create opportunities for generic entry, potentially expanding access through reduced pricing.

SGLT-2 inhibitor category experiences rapid expansion due to cardiovascular and renal protective benefits beyond glycemic control. Clinical evidence supporting reduced hospitalization rates drives adoption among high-risk patient populations. Reimbursement coverage improvements facilitate broader access despite higher acquisition costs compared to traditional therapies.

Sulfonylurea category maintains stable market presence despite newer alternatives, particularly in cost-conscious healthcare settings. Second-generation agents like glimepiride demonstrate improved safety profiles compared to older formulations. Generic availability ensures continued accessibility for economically disadvantaged patient populations requiring effective glucose-lowering therapy.

Combination therapy category shows accelerating growth as clinical guidelines increasingly recommend dual therapy approaches for optimal glycemic control. Fixed-dose combinations improve patient adherence while reducing pill burden and healthcare costs. Customized combinations enable personalized treatment approaches addressing individual patient characteristics and comorbidities.

Pharmaceutical manufacturers benefit from sustained market demand driven by chronic disease management requirements and expanding patient populations. Revenue stability results from long-term treatment needs and established therapeutic relationships with healthcare providers. Innovation opportunities enable differentiation through improved formulations, combination products, and patient support services.

Healthcare providers gain access to diverse therapeutic options enabling personalized treatment approaches for individual patient needs. Clinical outcomes improvement results from evidence-based medication selection and optimized treatment algorithms. Practice efficiency benefits from simplified dosing regimens and reduced monitoring requirements with newer therapeutic classes.

Patients experience improved quality of life through effective glucose control and reduced diabetes-related complications. Treatment convenience from oral formulations eliminates injection requirements and simplifies medication management. Cost savings through generic availability and insurance coverage reduce financial barriers to essential diabetes medications.

Healthcare systems achieve cost-effectiveness through prevention of expensive diabetes complications and hospitalizations. Resource optimization results from improved medication adherence and reduced need for intensive interventions. Population health benefits emerge from expanded access to effective diabetes management across diverse socioeconomic groups.

Regulatory agencies fulfill public health mandates through ensuring medication safety, efficacy, and accessibility. Healthcare policy objectives advance through evidence-based formulary decisions and reimbursement strategies. Economic benefits include reduced healthcare expenditures and improved productivity from better diabetes management outcomes.

Strengths:

Weaknesses:

Opportunities:

Threats:

Personalized medicine adoption represents a transformative trend enabling tailored treatment selection based on individual patient characteristics, genetic factors, and comorbidity profiles. Pharmacogenomic testing increasingly influences medication selection, optimizing therapeutic effectiveness while minimizing adverse reactions. Precision dosing approaches consider patient-specific factors to maximize clinical outcomes and reduce side effects.

Digital therapeutics integration combines traditional oral medications with technology-enabled interventions including mobile applications, continuous glucose monitoring, and telemedicine consultations. Artificial intelligence applications support clinical decision-making and medication optimization based on real-world patient data. Remote monitoring capabilities enable proactive medication adjustments and adherence support.

Combination therapy evolution focuses on fixed-dose formulations addressing multiple pathophysiological mechanisms simultaneously. Triple combination products emerge as treatment intensification options for patients requiring comprehensive glucose control. Customized combinations enable personalized approaches considering individual patient response patterns and tolerability profiles.

Value-based healthcare models increasingly influence prescribing decisions and reimbursement policies based on clinical outcomes and cost-effectiveness. Real-world evidence generation supports medication value demonstration through patient registries and outcomes databases. Risk-sharing agreements between manufacturers and payers align incentives around patient outcomes and healthcare cost management.

Sustainability initiatives drive pharmaceutical companies toward environmentally responsible manufacturing and packaging practices. Green chemistry approaches reduce environmental impact while maintaining medication quality and effectiveness. Circular economy principles influence supply chain optimization and waste reduction strategies across the pharmaceutical value chain.

Regulatory approvals for innovative oral anti-diabetic medications continue expanding treatment options for Brazilian patients. ANVISA fast-track designations accelerate access to breakthrough therapies addressing unmet medical needs. Biosimilar approvals increase competition and reduce treatment costs while maintaining therapeutic equivalence to reference products.

Manufacturing investments by multinational pharmaceutical companies strengthen local production capabilities and supply chain resilience. Technology transfers to Brazilian facilities enhance manufacturing efficiency and reduce dependence on imported medications. Quality improvements in domestic manufacturing meet international standards while supporting cost-effective medication production.

Strategic partnerships between pharmaceutical companies and healthcare organizations improve patient access and clinical outcomes. Public-private collaborations expand diabetes care programs and medication accessibility across underserved populations. Research partnerships with Brazilian academic institutions advance clinical understanding and therapeutic development for local patient populations.

Digital health initiatives integrate medication management with comprehensive diabetes care platforms. Telemedicine expansion improves healthcare access in remote regions while supporting medication optimization and adherence monitoring. Electronic prescribing systems enhance medication safety and reduce prescribing errors across healthcare settings.

Market access agreements between manufacturers and government agencies facilitate patient access to innovative therapies while managing healthcare costs. Pricing negotiations balance innovation incentives with affordability requirements for essential diabetes medications. Formulary inclusions expand coverage for newer therapeutic classes based on clinical evidence and cost-effectiveness analyses.

Market expansion strategies should prioritize rural and underserved regions where significant unmet medical needs exist. Distribution network optimization can improve medication accessibility while reducing supply chain costs and delivery times. Local manufacturing investments offer opportunities to reduce costs, improve supply reliability, and support Brazilian economic development objectives.

Innovation focus should emphasize combination therapies and patient-centric formulations that improve adherence and clinical outcomes. Digital health integration presents opportunities to differentiate products through comprehensive diabetes management solutions. Real-world evidence generation supports value demonstration and reimbursement negotiations with healthcare payers.

Stakeholder engagement with healthcare professionals, patient organizations, and regulatory agencies builds support for market access and adoption. Educational initiatives targeting both healthcare providers and patients improve treatment optimization and medication adherence rates. Policy advocacy supports favorable regulatory and reimbursement environments for innovative diabetes therapies.

Competitive positioning should leverage unique product attributes, clinical evidence, and patient support services to differentiate from generic alternatives. Pricing strategies must balance profitability with accessibility requirements in Brazil’s cost-conscious healthcare environment. Partnership opportunities with local companies can accelerate market penetration and reduce regulatory complexities.

According to MarkWide Research analysis, companies should invest in comprehensive market access strategies that address both clinical and economic value propositions. Long-term sustainability requires balancing innovation investments with cost-effectiveness to maintain competitive positioning as patents expire and generic competition intensifies.

Market evolution indicates continued growth driven by demographic trends, lifestyle factors, and healthcare infrastructure improvements. Diabetes prevalence projections suggest sustained demand for oral anti-diabetic medications with growth rates of approximately 4.2% annually through the next decade. Treatment paradigm shifts toward personalized medicine and combination therapies will reshape competitive dynamics and clinical practices.

Technological advancement will increasingly integrate digital health solutions with traditional oral medications, creating comprehensive diabetes management ecosystems. Artificial intelligence applications will optimize treatment selection and dosing based on individual patient characteristics and real-world outcomes data. Precision medicine approaches will enable more targeted therapeutic interventions with improved efficacy and reduced side effects.

Regulatory environment evolution will likely emphasize value-based assessments and real-world evidence requirements for market access and reimbursement decisions. ANVISA modernization initiatives may streamline approval processes while maintaining rigorous safety standards. International harmonization efforts could facilitate faster access to global innovations for Brazilian patients.

Healthcare system transformation toward preventive care and chronic disease management will expand the addressable market beyond diagnosed diabetes patients. Pre-diabetes interventions and risk reduction programs may create new therapeutic opportunities. Integrated care models will emphasize comprehensive diabetes management combining medications, lifestyle interventions, and technology solutions.

MWR projections indicate that successful market participants will need to adapt to evolving healthcare delivery models while maintaining focus on patient outcomes and cost-effectiveness. Sustainability considerations will increasingly influence pharmaceutical development and manufacturing decisions, creating opportunities for environmentally responsible companies to gain competitive advantages in socially conscious healthcare markets.

Brazil’s oral anti-diabetic drug market represents a dynamic and evolving landscape characterized by substantial growth opportunities and complex challenges. The market benefits from a large and expanding patient population, supportive government policies, and improving healthcare infrastructure that facilitates medication access across diverse socioeconomic segments. Innovation continues to drive market evolution through development of more effective therapeutic options, combination products, and patient-centric treatment approaches.

Competitive dynamics reflect the interplay between multinational pharmaceutical companies and domestic manufacturers, with generic competition playing a crucial role in ensuring medication affordability and accessibility. Regulatory support from ANVISA and government health programs creates a favorable environment for both innovation and competition, ultimately benefiting patients through expanded treatment options and improved outcomes.

Future success in this market will require strategic focus on value demonstration, patient outcomes, and cost-effectiveness while adapting to evolving healthcare delivery models and technological integration. Companies that effectively balance innovation with accessibility, leverage digital health opportunities, and build strong stakeholder relationships will be best positioned to capitalize on the significant growth potential within Brazil’s oral anti-diabetic drug market over the coming decade.

What is Oral Anti-Diabetic Drug?

Oral anti-diabetic drugs are medications used to manage blood sugar levels in individuals with diabetes. They work by various mechanisms, including increasing insulin sensitivity, stimulating insulin secretion, or reducing glucose production in the liver.

What are the key players in the Brazil Oral Anti-Diabetic Drug Market?

Key players in the Brazil Oral Anti-Diabetic Drug Market include companies like Novo Nordisk, Sanofi, and Merck, which are known for their innovative diabetes treatments and extensive product portfolios, among others.

What are the growth factors driving the Brazil Oral Anti-Diabetic Drug Market?

The growth of the Brazil Oral Anti-Diabetic Drug Market is driven by increasing diabetes prevalence, rising awareness about diabetes management, and advancements in drug formulations that enhance patient compliance.

What challenges does the Brazil Oral Anti-Diabetic Drug Market face?

Challenges in the Brazil Oral Anti-Diabetic Drug Market include regulatory hurdles, the high cost of new drug development, and competition from alternative therapies such as insulin and non-pharmacological treatments.

What opportunities exist in the Brazil Oral Anti-Diabetic Drug Market?

Opportunities in the Brazil Oral Anti-Diabetic Drug Market include the development of novel drug classes, increasing investment in diabetes research, and the potential for personalized medicine approaches to improve treatment outcomes.

What trends are shaping the Brazil Oral Anti-Diabetic Drug Market?

Trends in the Brazil Oral Anti-Diabetic Drug Market include the rise of combination therapies, the integration of digital health solutions for diabetes management, and a focus on patient-centric drug development.

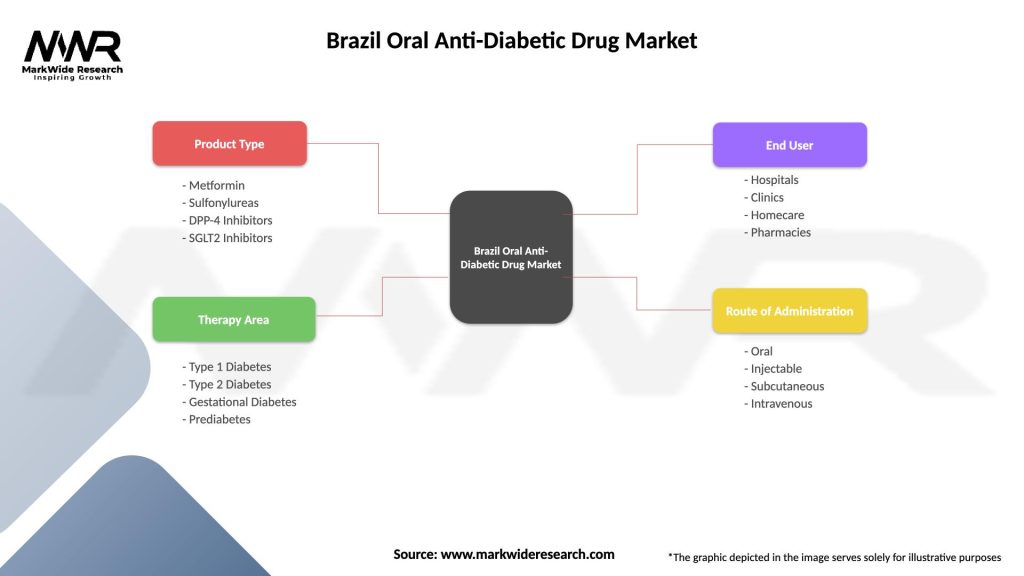

Brazil Oral Anti-Diabetic Drug Market

| Segmentation Details | Description |

|---|---|

| Product Type | Metformin, Sulfonylureas, DPP-4 Inhibitors, SGLT2 Inhibitors |

| Therapy Area | Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, Prediabetes |

| End User | Hospitals, Clinics, Homecare, Pharmacies |

| Route of Administration | Oral, Injectable, Subcutaneous, Intravenous |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Brazil Oral Anti-Diabetic Drug Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.