444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Brazil data center cooling market represents a critical infrastructure segment experiencing unprecedented growth as digital transformation accelerates across Latin America’s largest economy. Data center cooling systems have become essential for maintaining optimal operating temperatures in facilities housing servers, networking equipment, and storage systems that power Brazil’s expanding digital ecosystem.

Market dynamics indicate robust expansion driven by increasing cloud adoption, growing internet penetration reaching 82% of the population, and substantial investments in hyperscale data centers. The cooling infrastructure market encompasses various technologies including air conditioning systems, liquid cooling solutions, and free cooling technologies designed to optimize energy efficiency while maintaining critical temperature control.

Regional growth patterns show concentrated development in major metropolitan areas including São Paulo, Rio de Janeiro, and emerging tech hubs like Campinas and Belo Horizonte. The market demonstrates strong correlation with Brazil’s digital economy expansion, supported by government initiatives promoting Industry 4.0 and smart city development programs.

Technology adoption trends reveal increasing preference for energy-efficient cooling solutions, with precision air conditioning systems gaining 45% market share among enterprise deployments. The integration of artificial intelligence and IoT monitoring systems is transforming traditional cooling approaches, enabling predictive maintenance and optimized energy consumption patterns.

The Brazil data center cooling market refers to the comprehensive ecosystem of thermal management solutions, technologies, and services designed to maintain optimal operating temperatures within data center facilities across Brazilian territories. This market encompasses hardware, software, and service components essential for preventing equipment overheating and ensuring continuous operational reliability.

Cooling infrastructure includes multiple technology categories ranging from traditional computer room air conditioning (CRAC) units to advanced liquid cooling systems and innovative immersion cooling technologies. The market definition extends beyond hardware to include monitoring systems, maintenance services, and energy management solutions that optimize cooling efficiency while minimizing operational costs.

Market scope covers various facility types including enterprise data centers, colocation facilities, hyperscale cloud infrastructure, and edge computing deployments. The cooling solutions serve diverse industry verticals including financial services, telecommunications, government, healthcare, and emerging sectors like fintech and e-commerce platforms.

Brazil’s data center cooling market demonstrates exceptional growth momentum driven by accelerating digital transformation initiatives and increasing demand for cloud-based services across multiple industry sectors. The market landscape reflects significant infrastructure investments from both domestic and international players establishing presence in strategic Brazilian locations.

Key market drivers include expanding internet connectivity, growing adoption of artificial intelligence and machine learning applications, and increasing regulatory requirements for data localization. The cooling infrastructure segment benefits from Brazil’s favorable geographic location and climate conditions that enable implementation of free cooling technologies in certain regions.

Technology trends show strong preference for energy-efficient solutions with liquid cooling systems experiencing 38% adoption growth among hyperscale deployments. The market demonstrates increasing integration of smart monitoring systems and predictive analytics to optimize cooling performance and reduce energy consumption.

Competitive dynamics reveal active participation from global technology leaders alongside emerging Brazilian companies developing localized solutions. The market structure supports both large-scale enterprise deployments and distributed edge computing infrastructure requirements across Brazil’s diverse geographic regions.

Strategic market insights reveal several critical trends shaping Brazil’s data center cooling landscape:

Digital transformation acceleration serves as the primary catalyst driving Brazil’s data center cooling market expansion. Organizations across multiple sectors are migrating critical workloads to cloud platforms, creating substantial demand for robust cooling infrastructure capable of supporting increased server densities and computational requirements.

Cloud adoption momentum continues accelerating with Brazilian enterprises embracing hybrid cloud strategies and multi-cloud deployments. This trend necessitates sophisticated cooling solutions that can adapt to varying workload patterns and maintain optimal performance across diverse computing environments.

Government digitization initiatives including e-government programs and smart city projects are generating significant infrastructure investments. These programs require reliable data center facilities with advanced cooling systems to ensure continuous service availability and regulatory compliance.

Regulatory requirements for data localization under Brazil’s General Data Protection Law (LGPD) are compelling international companies to establish local data center presence. This regulatory driver creates sustained demand for cooling infrastructure supporting new facility deployments and capacity expansions.

Energy cost optimization pressures motivate organizations to invest in energy-efficient cooling technologies that reduce operational expenses while maintaining performance standards. The focus on sustainable operations aligns with corporate environmental commitments and regulatory expectations.

High capital investment requirements present significant barriers for organizations considering advanced cooling infrastructure deployments. The substantial upfront costs associated with precision cooling systems and liquid cooling technologies can delay implementation timelines and limit market penetration among smaller enterprises.

Technical complexity challenges associated with designing and implementing sophisticated cooling solutions require specialized expertise that may be limited in certain Brazilian regions. The shortage of qualified cooling system engineers and maintenance technicians constrains market growth potential.

Energy infrastructure limitations in some Brazilian regions create constraints for power-intensive cooling systems. Inconsistent electrical grid reliability and capacity limitations can impact cooling system performance and increase operational risks for data center operators.

Economic volatility and currency fluctuations affect international technology procurement costs, making it challenging for organizations to budget for cooling infrastructure investments. Exchange rate variations can significantly impact project economics and implementation decisions.

Regulatory complexity surrounding environmental standards and energy efficiency requirements creates compliance challenges for cooling system deployments. Navigating multiple regulatory frameworks can increase project timelines and implementation costs.

Sustainable cooling innovation presents substantial opportunities for companies developing environmentally friendly solutions that align with Brazil’s climate commitments and corporate sustainability goals. The growing emphasis on carbon neutrality creates demand for innovative cooling technologies with reduced environmental impact.

Edge computing expansion offers significant growth potential as 5G networks and IoT applications drive demand for distributed computing infrastructure. This trend creates opportunities for compact, efficient cooling solutions designed for edge data center deployments in diverse geographic locations.

Artificial intelligence integration enables development of smart cooling systems that optimize performance through predictive analytics and automated adjustments. Companies developing AI-powered cooling management solutions can capture growing market demand for intelligent infrastructure.

Service market expansion creates opportunities for specialized providers offering cooling system maintenance, performance optimization, and energy efficiency consulting services. The growing complexity of cooling infrastructure drives demand for expert service support.

Regional development initiatives in emerging Brazilian markets present opportunities for cooling infrastructure providers to establish presence in underserved areas experiencing digital growth. Government incentives for technology infrastructure development support market expansion efforts.

Supply chain dynamics in Brazil’s data center cooling market reflect increasing localization efforts as international manufacturers establish regional production capabilities and distribution networks. This trend reduces import dependencies while improving service responsiveness and cost competitiveness for Brazilian customers.

Technology evolution patterns show accelerating adoption of liquid cooling solutions with market penetration increasing by 42% annually among high-performance computing deployments. The shift toward higher server densities and advanced processors drives demand for more sophisticated cooling approaches.

Competitive dynamics demonstrate intensifying rivalry between established global players and emerging Brazilian companies developing specialized solutions for local market conditions. This competition drives innovation while improving solution affordability and accessibility for diverse customer segments.

Customer behavior trends reveal increasing preference for integrated cooling solutions that combine hardware, software, and services in comprehensive packages. Organizations seek simplified procurement and management approaches that reduce complexity while ensuring optimal performance.

Investment patterns show growing venture capital and private equity interest in Brazilian cooling technology companies developing innovative solutions for emerging market requirements. This financial support accelerates technology development and market expansion capabilities.

Comprehensive market analysis employed multiple research methodologies to ensure accurate and reliable insights into Brazil’s data center cooling market dynamics. The research approach combined quantitative data collection with qualitative analysis to provide holistic market understanding.

Primary research activities included structured interviews with industry executives, technology vendors, data center operators, and end-user organizations across Brazil’s major metropolitan areas. These interviews provided direct insights into market trends, challenges, and growth opportunities from key stakeholder perspectives.

Secondary research analysis incorporated extensive review of industry reports, government publications, regulatory documents, and company financial statements to validate primary findings and identify additional market trends. This approach ensured comprehensive coverage of market dynamics and competitive landscape factors.

Data validation processes employed triangulation techniques comparing multiple data sources to ensure accuracy and reliability of market insights. Cross-verification of findings through different research channels strengthened the overall analysis quality and credibility.

Market modeling techniques utilized statistical analysis and trend projection methods to develop growth forecasts and market size estimations. These quantitative approaches provided foundation for strategic recommendations and future outlook assessments.

São Paulo metropolitan region dominates Brazil’s data center cooling market with approximately 55% market concentration driven by high enterprise density, robust telecommunications infrastructure, and proximity to major financial and technology companies. The region benefits from established supplier networks and technical expertise availability.

Rio de Janeiro market represents the second-largest regional segment with growing investments in government data centers and oil & gas industry computing infrastructure. The region’s strategic location and improving connectivity infrastructure support continued cooling market expansion.

Southern Brazil regions including Porto Alegre and Curitiba demonstrate emerging growth potential driven by expanding technology sectors and favorable climate conditions for free cooling implementations. These markets show increasing adoption of energy-efficient cooling solutions.

Northeast Brazil presents developing opportunities as telecommunications infrastructure improvements and government digitization initiatives drive data center investments. The region’s growing population and economic development create foundation for cooling market expansion.

Central-West regions including Brasília show steady growth supported by government data center requirements and expanding agricultural technology applications. The region benefits from strategic location advantages for serving multiple Brazilian markets.

Market leadership in Brazil’s data center cooling sector features diverse participation from global technology giants and specialized regional providers. The competitive environment demonstrates healthy rivalry driving innovation and customer value creation.

Competitive strategies focus on technology innovation, local partnership development, and comprehensive service offerings that address specific Brazilian market requirements and regulatory compliance needs.

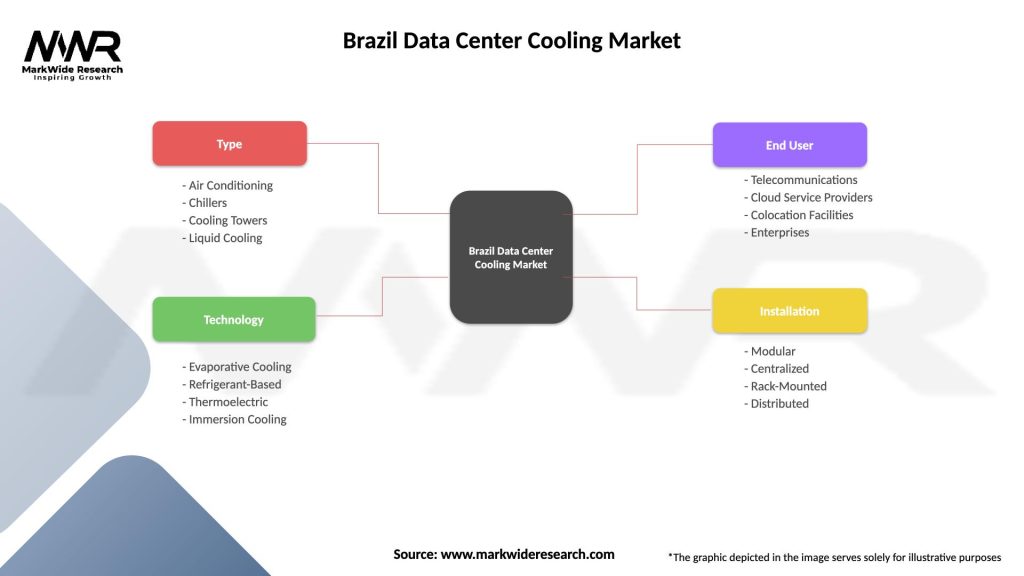

Technology-based segmentation reveals diverse cooling solution categories serving different data center requirements and performance specifications:

By Cooling Technology:

By Application Segment:

By End-User Industry:

Air conditioning systems maintain dominant market position with 62% adoption rate among Brazilian data centers, driven by proven reliability, established supplier networks, and comprehensive service support availability. These systems excel in moderate-density computing environments and retrofit applications.

Liquid cooling technologies demonstrate rapid growth trajectory with increasing adoption among high-performance computing and artificial intelligence applications. The technology category benefits from superior cooling efficiency and reduced energy consumption compared to traditional air-based systems.

Free cooling solutions gain traction in Brazilian regions with favorable climate conditions, enabling significant energy cost reductions through ambient air utilization. These systems show particular promise in southern Brazilian locations with moderate temperature profiles.

Hybrid cooling approaches emerge as preferred solutions for complex data center environments requiring flexible thermal management capabilities. These integrated systems optimize performance across varying workload conditions while maintaining energy efficiency standards.

Smart cooling systems incorporating IoT sensors and AI-driven optimization represent the fastest-growing category segment, driven by demand for predictive maintenance and automated performance optimization capabilities.

Data center operators benefit from advanced cooling solutions through improved operational efficiency, reduced energy costs, and enhanced equipment reliability. Modern cooling systems enable higher server densities while maintaining optimal performance standards and extending hardware lifecycles.

Technology vendors gain competitive advantages through innovative cooling solution development that addresses specific Brazilian market requirements. Companies offering localized solutions and comprehensive service support capture growing market opportunities while building sustainable customer relationships.

End-user organizations achieve significant value through reliable cooling infrastructure that ensures continuous service availability, regulatory compliance, and optimized total cost of ownership. Advanced cooling systems support digital transformation initiatives while minimizing operational risks.

Service providers capitalize on growing demand for specialized cooling system maintenance, optimization, and consulting services. The increasing complexity of cooling infrastructure creates sustainable revenue opportunities for companies with technical expertise and local market knowledge.

Government stakeholders benefit from robust data center cooling infrastructure supporting digital economy development, improved public services, and enhanced national competitiveness in technology sectors. Reliable cooling systems enable critical government applications and citizen services.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration emerges as a dominant trend with organizations prioritizing energy-efficient cooling solutions that align with environmental commitments and regulatory requirements. This trend drives adoption of green cooling technologies and renewable energy integration for data center operations.

Artificial intelligence adoption transforms cooling system management through predictive analytics, automated optimization, and intelligent monitoring capabilities. AI-powered cooling systems demonstrate 25% efficiency improvements compared to traditional management approaches.

Edge computing proliferation creates demand for compact, efficient cooling solutions designed for distributed deployment scenarios. This trend requires innovative approaches to thermal management in space-constrained and remote locations across Brazil’s diverse geography.

Liquid cooling mainstream adoption accelerates as organizations deploy high-density computing infrastructure supporting artificial intelligence, machine learning, and high-performance computing applications requiring advanced thermal management capabilities.

Service model evolution shows increasing preference for cooling-as-a-service offerings that provide comprehensive thermal management solutions through subscription-based models. This trend reduces capital investment requirements while ensuring optimal performance.

Technology partnerships between global cooling system manufacturers and Brazilian system integrators strengthen local market presence and service capabilities. These collaborations enhance solution accessibility while providing localized support for diverse customer requirements.

Innovation investments in next-generation cooling technologies including immersion cooling systems and advanced liquid cooling solutions demonstrate industry commitment to addressing evolving data center requirements. According to MarkWide Research analysis, these investments show 35% annual growth in research and development spending.

Regulatory developments including updated energy efficiency standards and environmental compliance requirements influence cooling system design and implementation approaches. These regulations drive adoption of more sustainable and efficient cooling technologies.

Market consolidation activities through strategic acquisitions and partnerships reshape competitive dynamics while expanding solution portfolios and geographic coverage. These developments strengthen market participants’ capabilities to serve diverse customer segments.

Infrastructure investments by major cloud service providers establishing Brazilian data center presence create substantial demand for advanced cooling solutions. These deployments demonstrate commitment to local market development and regulatory compliance.

Strategic positioning recommendations emphasize the importance of developing comprehensive cooling solutions that address specific Brazilian market conditions including climate variations, infrastructure constraints, and regulatory requirements. Companies should focus on localized solution development and service capabilities.

Technology investment priorities should emphasize energy-efficient solutions, AI-powered optimization, and sustainable cooling technologies that align with market trends and customer requirements. Organizations investing in these areas position themselves for long-term growth and competitive advantage.

Partnership strategies prove essential for market success, particularly collaborations with local system integrators, service providers, and technology distributors. These partnerships enhance market reach while providing essential local expertise and customer relationships.

Service capability development represents critical success factors as customers increasingly demand comprehensive support including installation, maintenance, optimization, and consulting services. Companies with strong service capabilities differentiate themselves in competitive markets.

Market timing considerations suggest optimal opportunities for market entry and expansion as digital transformation initiatives accelerate and infrastructure investments increase. Early market participants can establish competitive positions and customer relationships.

Growth trajectory projections indicate sustained market expansion driven by continued digital transformation, cloud adoption, and emerging technology deployments across Brazilian industries. MWR forecasts suggest compound annual growth rates exceeding industry averages through the next decade.

Technology evolution patterns point toward increasing adoption of liquid cooling systems with market penetration expected to reach 40% by 2030 among high-performance computing applications. This shift reflects growing computational density requirements and energy efficiency priorities.

Market maturation indicators suggest transition from basic cooling infrastructure to sophisticated thermal management ecosystems incorporating AI optimization, predictive maintenance, and integrated monitoring capabilities. This evolution creates opportunities for technology innovation and service differentiation.

Regional development prospects show expanding opportunities beyond traditional metropolitan centers as digital infrastructure investments reach emerging Brazilian markets. This geographic expansion creates new growth avenues for cooling solution providers.

Sustainability imperatives will increasingly influence cooling technology selection and implementation decisions as organizations prioritize carbon footprint reduction and environmental compliance. This trend favors energy-efficient and environmentally friendly cooling solutions.

Brazil’s data center cooling market presents exceptional growth opportunities driven by accelerating digital transformation, expanding cloud adoption, and increasing computational requirements across diverse industry sectors. The market demonstrates strong fundamentals supported by government digitization initiatives, regulatory requirements for data localization, and growing emphasis on sustainable technology solutions.

Technology trends favor advanced cooling solutions including liquid cooling systems, AI-powered optimization, and energy-efficient technologies that address evolving data center requirements while minimizing environmental impact. The shift toward higher server densities and emerging computing applications creates sustained demand for sophisticated thermal management capabilities.

Competitive dynamics encourage innovation and customer value creation as global technology leaders compete alongside emerging Brazilian companies developing specialized solutions for local market conditions. This competitive environment benefits customers through improved solution quality, service capabilities, and cost competitiveness.

Strategic success factors emphasize the importance of localized solution development, comprehensive service capabilities, and strategic partnerships that enhance market reach and customer relationships. Organizations investing in these areas position themselves for sustainable growth and competitive advantage in Brazil’s expanding data center cooling market.

What is Data Center Cooling?

Data Center Cooling refers to the methods and technologies used to maintain optimal temperature and humidity levels in data centers, ensuring the efficient operation of servers and IT equipment. Effective cooling is crucial for preventing overheating and ensuring reliability in data center operations.

What are the key players in the Brazil Data Center Cooling Market?

Key players in the Brazil Data Center Cooling Market include Schneider Electric, Vertiv, and Stulz, which provide a range of cooling solutions tailored for data centers. These companies focus on innovative cooling technologies and energy efficiency, among others.

What are the main drivers of the Brazil Data Center Cooling Market?

The main drivers of the Brazil Data Center Cooling Market include the increasing demand for data storage and processing, the growth of cloud computing, and the need for energy-efficient cooling solutions. These factors contribute to the expansion of data centers across various industries.

What challenges does the Brazil Data Center Cooling Market face?

The Brazil Data Center Cooling Market faces challenges such as high energy costs, the complexity of cooling system integration, and the need for regular maintenance. Additionally, environmental regulations may impact cooling technologies and practices.

What opportunities exist in the Brazil Data Center Cooling Market?

Opportunities in the Brazil Data Center Cooling Market include the adoption of advanced cooling technologies like liquid cooling and the integration of renewable energy sources. As data centers evolve, there is potential for innovative solutions that enhance efficiency and sustainability.

What trends are shaping the Brazil Data Center Cooling Market?

Trends shaping the Brazil Data Center Cooling Market include the shift towards modular cooling systems, the use of artificial intelligence for monitoring and optimization, and the increasing focus on sustainability. These trends reflect the industry’s response to growing energy demands and environmental concerns.

Brazil Data Center Cooling Market

| Segmentation Details | Description |

|---|---|

| Type | Air Conditioning, Chillers, Cooling Towers, Liquid Cooling |

| Technology | Evaporative Cooling, Refrigerant-Based, Thermoelectric, Immersion Cooling |

| End User | Telecommunications, Cloud Service Providers, Colocation Facilities, Enterprises |

| Installation | Modular, Centralized, Rack-Mounted, Distributed |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Brazil Data Center Cooling Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.