444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The blockchain technology has gained significant attention in various industries, and the retail banking sector is no exception. The integration of blockchain in retail banking has the potential to revolutionize the way financial transactions are conducted, improving efficiency, security, and transparency. Blockchain, essentially a decentralized and distributed ledger, allows for the recording and verification of transactions without the need for intermediaries such as banks. This technology has the power to streamline banking processes, reduce costs, and enhance the customer experience.

Meaning

Blockchain technology refers to a decentralized and transparent digital ledger that records and verifies transactions. In the context of retail banking, blockchain can be utilized to facilitate secure and efficient financial transactions, such as payments, remittances, and identity verification. Unlike traditional banking systems that rely on centralized databases, blockchain operates on a distributed network of computers, ensuring transparency, immutability, and resilience against fraud and hacking attempts.

Executive Summary

The integration of blockchain in retail banking holds immense potential for transforming the industry. By leveraging blockchain technology, retail banks can enhance operational efficiency, reduce costs, mitigate fraud, and provide customers with a seamless and secure banking experience. This executive summary provides a comprehensive overview of the blockchain in retail banking market, highlighting key insights, drivers, restraints, opportunities, and future outlook.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The blockchain in retail banking market is characterized by rapid technological advancements, increasing competition, and evolving customer expectations. Retail banks are embracing blockchain to stay ahead in a digital-first world, improve customer experience, and achieve operational excellence. The market dynamics are influenced by factors such as technological innovation, regulatory developments, partnerships, and strategic investments.

Regional Analysis

Competitive Landscape

Leading Companies in the Blockchain In Retail Banking Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

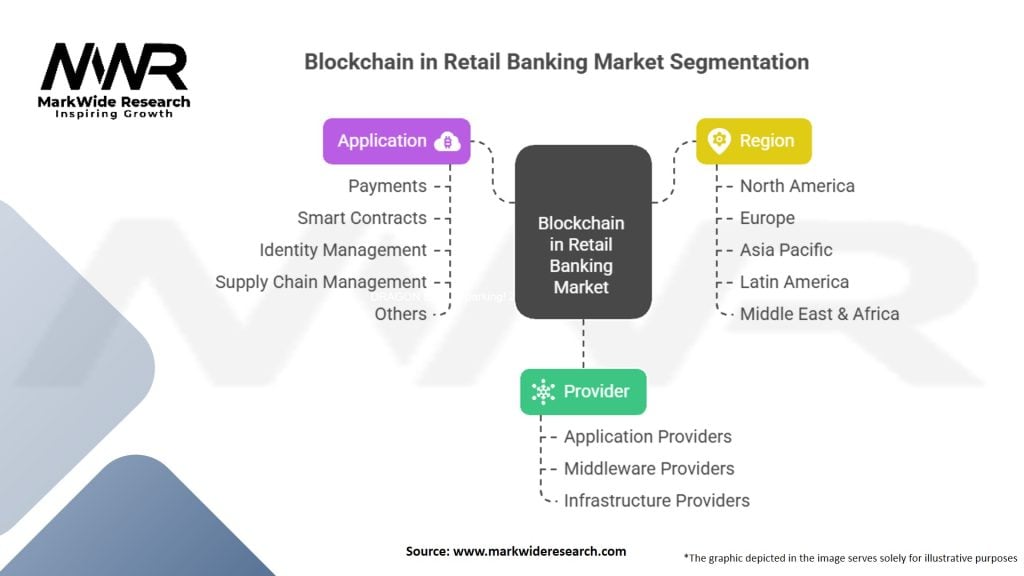

Segmentation

The blockchain in retail banking market can be segmented based on the following factors:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has accelerated the adoption of digital technologies, including blockchain, in the retail banking sector. Banks have realized the importance of resilient and efficient systems to cope with the challenges posed by the pandemic. Blockchain technology offers secure remote transactions, contactless payments, and improved supply chain visibility, aligning with the changing consumer behaviors and requirements in a post-pandemic world.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future of blockchain in retail banking looks promising, with the technology poised to disrupt traditional banking systems. As blockchain continues to mature, scalability issues will be addressed, interoperability among different platforms will improve, and regulatory frameworks will become more defined. The adoption of blockchain in retail banking will increase, resulting in enhanced security, improved efficiency, cost reduction, and innovative service offerings. Collaboration, innovation, and strategic partnerships will play a key role in shaping the future landscape of blockchain in retail banking.

Conclusion

Blockchain technology holds immense potential for transforming the retail banking sector. By leveraging blockchain, retail banks can enhance security, improve operational efficiency, reduce costs, and offer innovative services to their customers. Despite challenges such as regulatory uncertainties and scalability limitations, the market for blockchain in retail banking is witnessing significant growth globally. The integration of blockchain technology in retail banking is a strategic imperative for banks to stay competitive in an increasingly digital world. As the technology continues to evolve and overcome its limitations, the future of blockchain in retail banking looks promising, offering a secure, efficient, and customer-centric banking experience.

What is Blockchain In Retail Banking?

Blockchain In Retail Banking refers to the use of blockchain technology to enhance various banking processes, including transactions, record-keeping, and customer verification. It aims to improve security, transparency, and efficiency in banking operations.

Which companies are leading in the Blockchain In Retail Banking Market?

Leading companies in the Blockchain In Retail Banking Market include JPMorgan Chase, HSBC, and Bank of America, among others. These institutions are exploring blockchain for applications such as cross-border payments and smart contracts.

What are the key drivers of growth in the Blockchain In Retail Banking Market?

Key drivers of growth in the Blockchain In Retail Banking Market include the increasing demand for secure and transparent transactions, the need for cost reduction in banking operations, and the rising adoption of digital currencies.

What challenges does the Blockchain In Retail Banking Market face?

Challenges in the Blockchain In Retail Banking Market include regulatory uncertainties, the need for interoperability between different blockchain systems, and concerns regarding data privacy and security.

What future opportunities exist in the Blockchain In Retail Banking Market?

Future opportunities in the Blockchain In Retail Banking Market include the potential for decentralized finance (DeFi) applications, enhanced customer identity verification processes, and the integration of blockchain with artificial intelligence for improved decision-making.

What trends are shaping the Blockchain In Retail Banking Market?

Trends shaping the Blockchain In Retail Banking Market include the increasing collaboration between banks and fintech companies, the rise of central bank digital currencies (CBDCs), and the growing focus on sustainability through green blockchain initiatives.

Blockchain In Retail Banking Market

| Segmentation | Details |

|---|---|

| Provider | Application Providers, Middleware Providers, Infrastructure Providers |

| Application | Payments, Smart Contracts, Identity Management, Supply Chain Management, Others |

| Region | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Blockchain In Retail Banking Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA