Auto compulsory insurance, also known as mandatory auto insurance or compulsory third-party liability insurance, is a type of insurance coverage required by law in many countries to protect against financial losses resulting from bodily injury or property damage caused by a vehicle. This insurance is mandatory for all vehicle owners and drivers to ensure that victims of accidents involving motor vehicles receive compensation for their injuries or damages. The auto compulsory insurance market plays a crucial role in promoting road safety, protecting individuals and their assets, and mitigating the financial risks associated with motor vehicle accidents.

Meaning

Auto compulsory insurance refers to the legal requirement for vehicle owners and drivers to carry insurance coverage that provides compensation to third parties for bodily injury or property damage resulting from accidents involving their vehicles. This insurance typically covers medical expenses, lost wages, property repair or replacement costs, and legal fees incurred by victims of accidents. Auto compulsory insurance laws vary by jurisdiction but aim to ensure that all road users have adequate insurance coverage to protect against the financial consequences of accidents.

Executive Summary

The auto compulsory insurance market is a fundamental component of the motor vehicle regulatory framework, designed to protect individuals and society from the financial risks associated with motor vehicle accidents. This market is governed by laws and regulations that mandate minimum insurance requirements for vehicle owners and drivers, ensuring that victims of accidents receive timely compensation for their losses. While auto compulsory insurance provides essential protection, it also raises challenges related to affordability, accessibility, and enforcement, which require careful consideration by policymakers, insurers, and stakeholders.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Legal Requirement: Auto compulsory insurance is a legal requirement in many countries, mandating that all vehicle owners and drivers carry insurance coverage to protect against liability for bodily injury or property damage caused by their vehicles. These laws are intended to ensure that victims of accidents receive fair compensation for their losses.

Minimum Coverage: Auto compulsory insurance laws typically specify minimum coverage limits for bodily injury and property damage liability. These minimum requirements vary by jurisdiction but serve as a baseline level of protection for accident victims.

Enforcement Mechanisms: Governments employ various enforcement mechanisms to ensure compliance with auto compulsory insurance laws, such as requiring proof of insurance for vehicle registration, conducting random roadside checks, and imposing penalties for non-compliance, including fines, license suspension, or vehicle impoundment.

Insurance Market Dynamics: The auto compulsory insurance market is influenced by factors such as insurance premiums, claims frequency and severity, regulatory changes, market competition, and consumer behavior. Insurers must balance risk assessment, pricing, and underwriting practices to remain competitive and financially viable in the market.

Market Drivers

Road Safety: Auto compulsory insurance laws play a vital role in promoting road safety by ensuring that all vehicles on the road are covered by insurance, thereby providing financial protection for accident victims and incentivizing responsible driving behavior.

Victim Protection: Auto compulsory insurance laws protect accident victims by guaranteeing compensation for their injuries or damages, regardless of the financial resources or insurance coverage of the at-fault party. This helps mitigate the financial hardships faced by victims and their families following accidents.

Social Responsibility: Mandating auto compulsory insurance reflects a society’s commitment to social responsibility and the principle of collective risk-sharing, whereby all vehicle owners contribute to a common pool of funds to provide financial support for accident victims.

Legal Compliance: Auto compulsory insurance laws ensure legal compliance and accountability among vehicle owners and drivers, reducing the incidence of uninsured driving, hit-and-run accidents, and disputes over liability and compensation.

Market Restraints

Affordability: The cost of auto compulsory insurance premiums can be a barrier to compliance for some vehicle owners, particularly those with limited financial means or high-risk driving profiles. Affordability concerns may lead to non-compliance or lapses in coverage, undermining the effectiveness of mandatory insurance laws.

Accessibility: Access to auto compulsory insurance coverage may be limited in certain regions or markets, particularly in rural or underserved areas with fewer insurance providers or higher premiums. Limited accessibility can exacerbate disparities in insurance coverage and leave some drivers uninsured or underinsured.

Fraud and Abuse: The auto compulsory insurance market is susceptible to fraud and abuse, including staged accidents, exaggerated injury claims, and insurance scams. Fraudulent activities can drive up insurance costs, erode trust in the system, and undermine the financial stability of insurers.

Enforcement Challenges: Enforcing auto compulsory insurance laws poses challenges for government agencies and law enforcement authorities, particularly in jurisdictions with high levels of non-compliance or fraudulent activities. Limited resources, administrative burdens, and legal complexities may hinder effective enforcement efforts.

Market Opportunities

Risk Mitigation Strategies: Insurers can develop innovative risk mitigation strategies to manage claims costs, reduce fraud, and improve the financial sustainability of auto compulsory insurance programs. These strategies may include data analytics, predictive modeling, telematics, and fraud detection technologies.

Affordability Initiatives: Policymakers and insurers can collaborate to implement affordability initiatives, such as premium subsidies, discounts for safe driving behaviors, flexible payment options, and financial assistance programs for low-income drivers.

Education and Awareness: Education and awareness campaigns can help inform vehicle owners and drivers about the importance of auto compulsory insurance, their legal obligations, available coverage options, and the consequences of non-compliance. Empowering consumers with knowledge can foster compliance and responsible insurance practices.

Technology Adoption: Embracing technology and digital solutions can streamline insurance processes, enhance customer experience, and improve access to auto compulsory insurance coverage. Online platforms, mobile apps, and digital tools can simplify policy management, claims processing, and communication between insurers and policyholders.

Market Dynamics

The auto compulsory insurance market operates within a dynamic regulatory, economic, and social environment characterized by evolving insurance laws, changing consumer preferences, technological advancements, and market competition. These dynamics shape insurance products, pricing strategies, distribution channels, and customer relationships, driving innovation and adaptation among insurers and stakeholders.

Regional Analysis

The auto compulsory insurance market exhibits regional variations influenced by factors such as insurance regulations, legal frameworks, socio-economic conditions, cultural norms, and market dynamics. While some regions may have well-established insurance systems with high levels of compliance and consumer protection, others may face challenges related to enforcement, affordability, and accessibility.

Competitive Landscape

Leading Companies in the Auto Compulsory Insurance Market:

PICC Property and Casualty Company Limited

Ping An Insurance (Group) Company of China, Ltd.

China Pacific Insurance (Group) Co., Ltd.

People’s Insurance Company of China Limited

Generali Group

Zurich Insurance Group Ltd.

Allianz SE

State Farm Mutual Automobile Insurance Company

Berkshire Hathaway Inc. (Geico)

Progressive Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

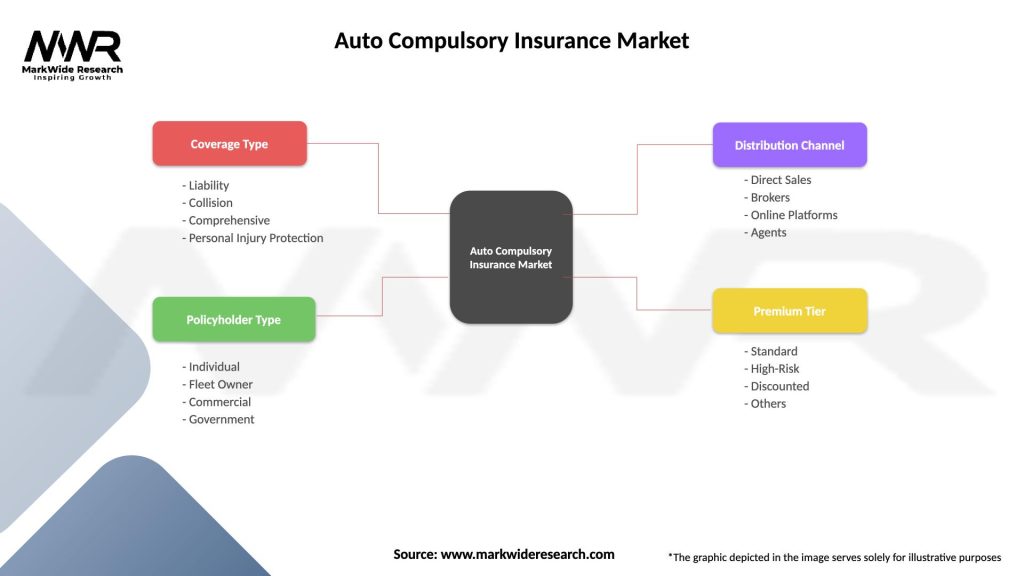

The auto compulsory insurance market can be segmented based on various factors such as:

Coverage Type: Segmentation by coverage type includes liability insurance, personal injury protection, uninsured/underinsured motorist coverage, and property damage coverage.

Vehicle Type: Segmentation by vehicle type includes passenger cars, commercial vehicles, motorcycles, and recreational vehicles, each with unique insurance needs and risk profiles.

Geographic Location: Segmentation by geographic location considers regional differences in insurance regulations, market dynamics, socio-economic factors, and consumer preferences.

Category-wise Insights

Liability Insurance: Liability insurance covers bodily injury and property damage caused by the insured vehicle to third parties. It is a core component of auto compulsory insurance and provides financial protection for accident victims.

Personal Injury Protection: Personal injury protection (PIP) coverage pays for medical expenses, lost wages, and other related costs incurred by the insured driver and passengers in the event of an accident, regardless of fault.

Uninsured/Underinsured Motorist Coverage: Uninsured/underinsured motorist coverage protects insured drivers and passengers from financial losses resulting from accidents caused by uninsured or underinsured motorists who lack adequate insurance coverage.

Property Damage Coverage: Property damage coverage pays for the repair or replacement of the third party’s property damaged by the insured vehicle in an accident, such as vehicles, buildings, fences, and other structures.

Key Benefits for Industry Participants and Stakeholders

Risk Management: Auto compulsory insurance provides a mechanism for insurers to manage and transfer the financial risks associated with motor vehicle accidents, ensuring that claims are promptly settled and victims receive compensation for their losses.

Consumer Protection: Auto compulsory insurance laws protect consumers by guaranteeing access to insurance coverage, promoting fair compensation for accident victims, and enforcing legal accountability among vehicle owners and drivers.

Market Stability: Mandatory auto insurance requirements contribute to market stability by reducing uncertainty, promoting risk-sharing, and enhancing the financial solvency of insurers through a broad and diversified pool of policyholders.

Social Welfare: Auto compulsory insurance laws promote social welfare by supporting accident victims, reducing the burden on public health and social welfare systems, and fostering a culture of responsibility and accountability among road users.

SWOT Analysis

Strengths:

Legal Requirement: Auto compulsory insurance laws establish a legal framework for insurance coverage, ensuring that all drivers carry minimum liability protection and victims of accidents receive compensation for their losses.

Risk Sharing: Mandatory auto insurance promotes risk-sharing among vehicle owners and drivers, spreading the financial costs of accidents across a broad pool of policyholders and preventing individual drivers from bearing the full burden of liability.

Consumer Protection: Auto compulsory insurance laws protect consumers by guaranteeing access to insurance coverage, establishing minimum standards of protection, and enforcing compliance with legal requirements through regulatory oversight.

Road Safety: Mandatory auto insurance laws contribute to road safety by incentivizing responsible driving behavior, reducing the incidence of uninsured driving, and ensuring that accident victims receive timely medical care and financial support.

Weaknesses:

Affordability Concerns: The cost of auto compulsory insurance premiums may be prohibitive for some drivers, particularly those with limited financial means or high-risk driving profiles, leading to non-compliance or lapses in coverage.

Enforcement Challenges: Enforcing auto compulsory insurance laws poses challenges for government agencies and law enforcement authorities, particularly in jurisdictions with high levels of non-compliance, fraud, or administrative inefficiencies.

Limited Coverage: Auto compulsory insurance may provide limited coverage for certain types of accidents, injuries, or property damage, leaving accident victims with inadequate compensation or recourse for their losses.

Regulatory Complexity: The regulatory framework governing auto compulsory insurance can be complex and subject to frequent changes, creating compliance burdens, administrative costs, and legal uncertainties for insurers and consumers alike.

Opportunities:

Technology Integration: Integrating technology solutions such as telematics, artificial intelligence, and digital platforms can streamline insurance processes, enhance customer experience, and improve risk assessment and pricing practices in the auto compulsory insurance market.

Affordability Initiatives: Implementing affordability initiatives such as premium subsidies, discounts for safe driving behaviors, and financial assistance programs can make auto compulsory insurance more accessible and affordable for low-income drivers and underserved communities.

Education and Awareness: Education and awareness campaigns can help inform consumers about their rights and responsibilities under auto compulsory insurance laws, raise awareness about available coverage options, and promote responsible insurance practices.

Regulatory Reform: Reforming auto compulsory insurance regulations to address affordability concerns, streamline administrative processes, and enhance consumer protections can improve the effectiveness and efficiency of mandatory insurance requirements.

Threats:

Fraud and Abuse: The auto compulsory insurance market is susceptible to fraud and abuse, including staged accidents, fraudulent claims, and insurance scams, which can drive up insurance costs, erode trust in the system, and undermine the financial stability of insurers.

Legal Challenges: Legal challenges to auto compulsory insurance laws, regulations, or enforcement practices may arise from various stakeholders, including insurers, consumers, advocacy groups, and policymakers, leading to litigation, regulatory changes, or legislative reforms.

Economic Volatility: Economic downturns, recessions, or financial crises can impact consumer purchasing power, insurance affordability, claims frequency, and insurer profitability, posing risks to the financial stability and sustainability of the auto compulsory insurance market.

Technological Disruption: Technological disruptions such as autonomous vehicles, shared mobility, and alternative transportation modes may reshape the landscape of the auto compulsory insurance market, altering risk profiles, pricing models, and insurance coverage needs.

Market Key Trends

Digital Transformation: The auto compulsory insurance market is undergoing digital transformation, with insurers investing in digital platforms, mobile apps, and online portals to enhance customer engagement, streamline insurance processes, and improve accessibility and convenience.

Usage-Based Insurance: Usage-based insurance (UBI) programs, also known as pay-as-you-drive or pay-how-you-drive insurance, are gaining popularity in the auto compulsory insurance market, offering personalized pricing based on driving behaviors, mileage, and risk factors.

Telematics and IoT: Telematics devices and Internet of Things (IoT) technologies are being integrated into auto compulsory insurance products to collect real-time data on driving behaviors, vehicle performance, and accident risks, enabling insurers to offer more accurate pricing and personalized coverage options.

Regulatory Reforms: Regulatory reforms aimed at enhancing consumer protections, promoting market competition, and addressing affordability concerns are shaping the regulatory landscape of the auto compulsory insurance market, influencing insurance laws, regulations, and enforcement practices.

Covid-19 Impact

The Covid-19 pandemic has had a multifaceted impact on the auto compulsory insurance market, influencing insurance demand, claims trends, regulatory responses, and consumer behaviors. Some key impacts of Covid-19 on the market include:

Changes in Driving Patterns: Lockdowns, travel restrictions, and remote work arrangements have led to changes in driving patterns, including reduced vehicle miles traveled, shifts in commute behaviors, and fluctuations in traffic congestion levels, affecting insurance risk profiles and claims frequency.

Economic Uncertainty: Economic uncertainty, job losses, and financial hardships resulting from the pandemic have impacted consumer purchasing power, insurance affordability, and premium payments, leading to changes in insurance coverage levels, policy cancellations, or lapses in coverage.

Claims Management: Insurers have faced challenges in claims management, including delays in claims processing, disruptions in repair and replacement services, and increased claims complexity due to Covid-19-related factors such as health concerns, medical care access, and supply chain disruptions.

Regulatory Responses: Regulators and policymakers have responded to the pandemic by implementing temporary measures such as premium relief programs, grace periods for premium payments, and flexibility in compliance requirements to support consumers and insurers during times of crisis.

Key Industry Developments

Digitalization and Remote Services: Insurers are accelerating digitalization efforts and offering remote services such as online policy purchasing, claims filing, virtual inspections, and customer support to adapt to changing consumer preferences and public health measures.

Flexible Coverage Options: Insurers are introducing flexible coverage options and payment plans to accommodate evolving customer needs, financial circumstances, and usage patterns, including temporary adjustments to coverage levels, premium discounts, and policy extensions.

Risk Management Strategies: Insurers are implementing risk management strategies to mitigate Covid-19-related risks, including adjustments to underwriting practices, claims reserves, reinsurance arrangements, and investment portfolios to maintain financial stability and solvency.

Customer Engagement Initiatives: Insurers are launching customer engagement initiatives such as educational campaigns, wellness programs, and community outreach efforts to support policyholders, enhance brand loyalty, and build resilience during challenging times.

Analyst Suggestions

Adaptability and Resilience: Insurers should remain adaptable and resilient in responding to evolving market dynamics, regulatory changes, and customer needs during and after the Covid-19 pandemic, focusing on innovation, agility, and customer-centricity.

Customer Support and Communication: Insurers should prioritize customer support and communication, providing clear and transparent information about insurance coverage, claims processes, premium relief options, and regulatory updates to build trust and confidence among policyholders.

Digital Transformation: Insurers should accelerate digital transformation initiatives, investing in technology, data analytics, and digital platforms to enhance operational efficiency, customer experience, risk management, and competitive advantage in the post-pandemic era.

Collaboration and Partnerships: Insurers should collaborate with regulators, industry stakeholders, and technology partners to address common challenges, share best practices, and foster innovation, resilience, and sustainability in the auto compulsory insurance market.

Future Outlook

The future outlook for the auto compulsory insurance market is influenced by factors such as regulatory reforms, technological advancements, economic recovery, and societal changes. While the Covid-19 pandemic has presented challenges and uncertainties, it has also accelerated digital transformation, innovation, and resilience in the insurance industry, paving the way for new opportunities, business models, and value propositions. By embracing change, adapting to market dynamics, and prioritizing customer needs, insurers can navigate the evolving landscape of the auto compulsory insurance market and emerge stronger and more resilient in the post-pandemic era.

Conclusion

The auto compulsory insurance market is a critical component of the motor vehicle regulatory framework, providing essential protection for vehicle owners, drivers, and accident victims. While the market faces challenges such as affordability, accessibility, fraud, and enforcement, it also offers opportunities for innovation, collaboration, and regulatory reform. By addressing these challenges and seizing opportunities, insurers can enhance the effectiveness, efficiency, and inclusivity of auto compulsory insurance programs, promoting road safety, financial security, and social welfare for all stakeholders.

What is Auto Compulsory Insurance?

Auto Compulsory Insurance refers to the mandatory insurance coverage required by law for vehicle owners. It typically covers liability for bodily injury and property damage resulting from accidents involving the insured vehicle.

What are the key players in the Auto Compulsory Insurance Market?

Key players in the Auto Compulsory Insurance Market include companies like State Farm, Allstate, Geico, and Progressive, among others. These companies offer various policies to meet the legal requirements for auto insurance.

What are the main drivers of the Auto Compulsory Insurance Market?

The main drivers of the Auto Compulsory Insurance Market include increasing vehicle ownership, rising awareness of road safety, and stringent government regulations mandating insurance coverage. These factors contribute to the growing demand for compulsory insurance policies.

What challenges does the Auto Compulsory Insurance Market face?

The Auto Compulsory Insurance Market faces challenges such as fraudulent claims, regulatory changes, and competition among insurers. These issues can impact profitability and the overall stability of the market.

What opportunities exist in the Auto Compulsory Insurance Market?

Opportunities in the Auto Compulsory Insurance Market include the integration of technology for better customer service, the rise of telematics-based insurance policies, and the potential for expanding coverage options to include electric and autonomous vehicles.

What trends are shaping the Auto Compulsory Insurance Market?

Trends shaping the Auto Compulsory Insurance Market include the increasing use of digital platforms for policy management, the adoption of usage-based insurance models, and a growing focus on customer-centric services. These trends are transforming how insurance is offered and managed.

Leading Companies in the Auto Compulsory Insurance Market:

PICC Property and Casualty Company Limited

Ping An Insurance (Group) Company of China, Ltd.

China Pacific Insurance (Group) Co., Ltd.

People’s Insurance Company of China Limited

Generali Group

Zurich Insurance Group Ltd.

Allianz SE

State Farm Mutual Automobile Insurance Company

Berkshire Hathaway Inc. (Geico)

Progressive Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.