444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Austria life insurance market represents a mature and sophisticated financial services sector that has evolved significantly over the past decade. This market encompasses various life insurance products including term life, whole life, universal life, and unit-linked insurance policies designed to provide financial protection and investment opportunities for Austrian consumers. The market demonstrates steady growth patterns with increasing consumer awareness about financial planning and retirement security driving demand across different demographic segments.

Market dynamics in Austria reflect broader European trends while maintaining distinct characteristics shaped by local regulatory frameworks and consumer preferences. The Austrian life insurance sector benefits from a stable economic environment, robust regulatory oversight, and a population increasingly focused on long-term financial planning. Digital transformation initiatives have accelerated product innovation and distribution channel optimization, enabling insurers to reach broader customer segments more effectively.

Regulatory compliance remains a cornerstone of market operations, with Austrian insurers adhering to stringent European Union directives and local regulatory requirements. The market exhibits strong competitive dynamics among domestic and international players, fostering innovation in product design, pricing strategies, and customer service delivery. Growth projections indicate a compound annual growth rate of 4.2% over the forecast period, driven by demographic trends and evolving consumer financial planning needs.

The Austria life insurance market refers to the comprehensive ecosystem of life insurance products, services, and distribution channels operating within Austria’s financial services sector. This market encompasses traditional life insurance policies that provide death benefits to beneficiaries, as well as modern investment-linked products that combine insurance protection with wealth accumulation opportunities. Life insurance products in Austria serve dual purposes of risk mitigation and long-term financial planning, addressing consumer needs for family protection and retirement income security.

Market participants include established Austrian insurance companies, international insurers with local operations, bancassurance providers, and independent insurance brokers. The market structure reflects a mature insurance ecosystem with well-developed distribution networks, comprehensive product portfolios, and sophisticated underwriting capabilities. Product categories range from basic term life policies to complex unit-linked insurance plans that offer investment flexibility and tax advantages.

Consumer demographics span various age groups and income levels, with particular strength in middle-income segments seeking comprehensive financial protection. The market serves both individual consumers and corporate clients requiring group life insurance coverage for employees. Distribution channels include traditional agent networks, bancassurance partnerships, direct sales platforms, and increasingly popular digital channels that provide convenient access to insurance products and services.

Austria’s life insurance market demonstrates remarkable resilience and growth potential within the European insurance landscape. The market benefits from favorable demographic trends, increasing consumer awareness about financial planning, and supportive regulatory frameworks that encourage long-term savings and investment. Key market drivers include an aging population seeking retirement income solutions, growing middle-class wealth, and evolving consumer preferences for flexible insurance products that combine protection with investment opportunities.

Market segmentation reveals strong performance across multiple product categories, with unit-linked insurance policies gaining 35% market share due to their investment flexibility and tax advantages. Traditional whole life and term life products maintain significant market presence, particularly among conservative investors seeking guaranteed benefits. Distribution channel evolution shows increasing adoption of digital platforms, with online sales representing 18% of new policy acquisitions in recent periods.

Competitive landscape features both domestic Austrian insurers and international companies competing across price, product innovation, and customer service dimensions. Market leaders focus on developing comprehensive product portfolios that address diverse consumer needs while maintaining strong financial stability ratings. Future growth prospects remain positive, supported by demographic trends, regulatory stability, and ongoing digital transformation initiatives that enhance market accessibility and operational efficiency.

Consumer behavior analysis reveals several important trends shaping the Austrian life insurance market. Austrian consumers demonstrate increasing sophistication in financial planning, with growing preference for products that offer both protection and investment components. This trend reflects broader economic awareness and desire for financial security in uncertain times.

Demographic transformation serves as a primary driver for Austria’s life insurance market growth. The country’s aging population creates substantial demand for retirement income solutions and long-term care insurance products. Life expectancy increases necessitate longer-term financial planning, driving consumer interest in life insurance products that provide both protection and investment growth potential over extended periods.

Economic stability in Austria provides a favorable environment for life insurance market expansion. Consistent GDP growth, low unemployment rates, and stable inflation create conditions conducive to long-term financial planning and insurance product adoption. Disposable income growth among middle-class consumers enables increased spending on financial protection and investment products, supporting market expansion across various demographic segments.

Regulatory support through tax incentives and favorable treatment of life insurance products encourages consumer adoption. Austrian tax policies provide advantages for certain life insurance products, making them attractive alternatives to traditional savings and investment vehicles. Government initiatives promoting private retirement savings complement public pension systems, creating additional demand for life insurance products that address retirement income needs.

Digital transformation accelerates market accessibility and operational efficiency. Technology adoption enables insurers to streamline underwriting processes, enhance customer service delivery, and develop innovative product features. Mobile applications and online platforms provide convenient access to insurance products and services, particularly appealing to younger consumer segments who prefer digital interactions over traditional agent-based sales processes.

Economic uncertainty periodically impacts consumer confidence and spending on discretionary financial products including life insurance. Economic downturns, inflation concerns, and employment instability can reduce consumer willingness to commit to long-term insurance premiums, particularly for investment-linked products that involve market risk exposure.

Regulatory complexity creates operational challenges for insurance companies operating in Austria. Compliance with evolving EU insurance directives, local regulatory requirements, and consumer protection standards requires significant investment in systems, processes, and personnel. Regulatory changes can impact product design, pricing strategies, and distribution approaches, creating uncertainty for market participants and potentially affecting growth trajectories.

Low interest rate environment challenges traditional life insurance product profitability and attractiveness. Prolonged periods of low interest rates reduce investment returns on insurance company portfolios and make guaranteed benefit products less competitive compared to alternative investment options. Yield pressures force insurers to adjust product designs, pricing structures, and investment strategies to maintain profitability while meeting consumer expectations.

Competition from alternative financial products limits life insurance market growth potential. Banking products, mutual funds, pension schemes, and other investment vehicles compete for consumer attention and financial resources. Product substitution occurs when consumers perceive alternative financial products as offering better value, higher returns, or greater flexibility than traditional life insurance offerings.

Digital innovation presents significant opportunities for market expansion and operational improvement. Advanced technologies including artificial intelligence, machine learning, and data analytics enable insurers to develop more sophisticated underwriting models, personalized product offerings, and enhanced customer service capabilities. Insurtech partnerships provide access to innovative technologies and business models that can accelerate digital transformation initiatives.

Product diversification opportunities exist in emerging market segments including sustainable investing, health and wellness integration, and specialized coverage for evolving lifestyle needs. ESG-focused products appeal to environmentally conscious consumers while addressing regulatory expectations for sustainable business practices. Integration of health monitoring technologies and wellness programs creates opportunities for risk-based pricing and enhanced customer engagement.

Market penetration potential remains substantial among underinsured demographic segments. Young professionals, women, and immigrant populations represent growth opportunities for targeted product development and marketing initiatives. Financial literacy programs can increase awareness of life insurance benefits and drive adoption among previously underserved market segments.

Cross-border expansion within the European Union provides growth opportunities for Austrian insurers with strong domestic market positions. EU regulatory harmonization facilitates expansion into neighboring markets while leveraging existing operational capabilities and product expertise. Strategic partnerships with international insurers can provide access to broader distribution networks and enhanced product portfolios.

Supply and demand dynamics in Austria’s life insurance market reflect complex interactions between consumer needs, regulatory requirements, and competitive pressures. Demand patterns show increasing consumer preference for flexible products that combine insurance protection with investment opportunities, driving insurers to develop hybrid offerings that address multiple financial planning objectives simultaneously.

Competitive intensity varies across market segments, with established players maintaining strong positions in traditional product categories while newer entrants focus on digital distribution and innovative product features. Market consolidation trends include strategic acquisitions and partnerships that enable companies to achieve scale economies and expand distribution capabilities. Competition drives continuous improvement in product design, pricing competitiveness, and customer service quality.

Technology adoption accelerates across all market participants, with digital transformation initiatives reshaping customer interactions, operational processes, and product development approaches. Data analytics capabilities enable more sophisticated risk assessment, personalized pricing, and targeted marketing strategies. Automation technologies improve operational efficiency while reducing processing costs and enhancing customer experience quality.

Regulatory evolution continues influencing market dynamics through updated consumer protection standards, capital adequacy requirements, and product disclosure obligations. Compliance investments represent significant operational costs while ensuring market stability and consumer confidence. Regulatory harmonization across European markets creates opportunities for standardized product development and cross-border expansion strategies.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Austria’s life insurance market dynamics. Primary research includes structured interviews with industry executives, regulatory officials, and consumer focus groups to gather firsthand perspectives on market trends, challenges, and opportunities. Survey methodologies capture quantitative data on consumer preferences, purchasing behaviors, and satisfaction levels across different market segments.

Secondary research incorporates analysis of regulatory filings, industry reports, financial statements, and statistical databases maintained by Austrian insurance regulatory authorities. Market data validation involves cross-referencing multiple sources to ensure accuracy and consistency of market size estimates, growth projections, and competitive positioning assessments. Historical trend analysis provides context for understanding market evolution and identifying emerging patterns.

Analytical frameworks include statistical modeling techniques, comparative analysis methodologies, and scenario planning approaches that evaluate potential market developments under different economic and regulatory conditions. Expert consultation with industry specialists, academic researchers, and regulatory experts provides additional validation and insights into complex market dynamics and future growth prospects.

Data collection protocols ensure compliance with privacy regulations and industry standards while maintaining research quality and objectivity. Quality assurance processes include peer review, data verification, and methodology validation to ensure research findings meet professional standards for accuracy, reliability, and relevance to market participants and stakeholders.

Vienna metropolitan area represents the largest concentration of life insurance market activity, accounting for approximately 42% of total market premium volume. The capital region benefits from higher income levels, greater financial services infrastructure, and concentrated corporate headquarters that drive both individual and group life insurance demand. Urban consumers demonstrate higher adoption rates for investment-linked products and digital distribution channels compared to rural areas.

Eastern Austria regions including Lower Austria and Burgenland show steady market growth supported by proximity to Vienna and increasing economic development. These regions exhibit traditional product preferences with strong demand for whole life and term life insurance products. Rural areas maintain preference for agent-based distribution channels and conservative investment approaches, though digital adoption is gradually increasing.

Western Austria markets including Tyrol, Vorarlberg, and Salzburg demonstrate robust economic conditions that support life insurance market growth. These regions benefit from tourism industry strength, cross-border economic activity, and higher disposable income levels. Market penetration rates in western regions reach 68% of eligible households, reflecting strong insurance awareness and financial planning culture.

Central Austria regions including Upper Austria and Styria show balanced market development with diverse economic bases supporting steady insurance demand. Industrial activity, agricultural sectors, and service industries create varied consumer segments with different insurance needs. Regional distribution networks remain important for market access, though digital channels are gaining acceptance among younger demographics.

Market leadership in Austria’s life insurance sector is distributed among several established players with strong domestic market positions and comprehensive product portfolios. Competitive dynamics reflect both domestic Austrian insurers and international companies that have established significant local operations through acquisitions, partnerships, or organic growth strategies.

Competitive strategies focus on product innovation, distribution channel optimization, and customer service excellence. Market leaders invest significantly in digital transformation initiatives while maintaining traditional distribution networks that serve diverse customer preferences. Strategic partnerships with banks, financial advisors, and technology companies enhance market reach and operational capabilities.

Product segmentation in Austria’s life insurance market reflects diverse consumer needs and risk preferences across different demographic and income segments. Traditional life insurance products including term life and whole life policies maintain significant market share, particularly among conservative consumers seeking guaranteed benefits and predictable premium structures.

By Product Type:

By Distribution Channel:

Unit-linked insurance policies demonstrate the strongest growth momentum within Austria’s life insurance market, driven by consumer demand for investment flexibility and tax-advantaged savings vehicles. These products appeal particularly to affluent consumers and younger demographics seeking long-term wealth accumulation combined with life insurance protection. Market penetration of unit-linked products reaches 28% of total life insurance policies in force, with continued growth expected as financial literacy increases.

Traditional whole life insurance maintains stable market position among conservative consumers prioritizing guaranteed benefits and predictable premium structures. These products serve customers seeking financial security and estate planning solutions without market risk exposure. Whole life insurance represents approximately 31% of total premium volume, reflecting continued demand for traditional insurance approaches despite growing interest in investment-linked alternatives.

Term life insurance experiences steady demand from young families, mortgage holders, and individuals seeking affordable protection during specific life stages. Product innovations include renewable and convertible features that provide flexibility as consumer needs evolve. Online distribution of term life products grows rapidly, with digital channels accounting for 25% of new term life policy sales due to simplified underwriting and competitive pricing.

Group life insurance through employer-sponsored programs represents a significant market segment driven by corporate employee benefit strategies and regulatory requirements. Workplace benefits integration creates opportunities for insurers to reach large employee populations while providing cost-effective coverage solutions. Group life insurance penetration reaches 45% of eligible employees across Austrian companies with comprehensive benefit programs.

Insurance companies benefit from Austria’s stable regulatory environment, sophisticated consumer base, and growing demand for financial protection products. Market opportunities include product innovation, digital transformation initiatives, and expansion into underserved demographic segments. Strong regulatory frameworks provide consumer confidence while enabling sustainable business growth and profitability.

Consumers gain access to comprehensive life insurance products that address diverse financial planning needs including family protection, retirement income, and wealth accumulation objectives. Product variety enables customized solutions tailored to individual circumstances, risk preferences, and financial goals. Competitive market dynamics ensure reasonable pricing and continuous improvement in product features and customer service quality.

Distribution partners including agents, brokers, and bancassurance providers benefit from strong consumer demand and diverse product portfolios that support revenue growth and customer relationship development. Technology investments by insurance companies enhance distribution efficiency and provide better tools for customer service and policy management.

Regulatory authorities benefit from a well-functioning insurance market that provides consumer protection, financial stability, and economic growth contribution. Market development supports broader financial services sector objectives while ensuring adequate consumer protection and systemic risk management. Industry compliance with regulatory standards maintains market integrity and consumer confidence.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization acceleration transforms customer interactions, policy administration, and claims processing across Austria’s life insurance market. Mobile applications and online platforms provide convenient access to policy information, premium payments, and customer service functions. Digital-first insurers challenge traditional players by offering streamlined processes and competitive pricing through technology-enabled operations.

Personalization trends drive development of customized insurance products tailored to individual customer needs, risk profiles, and life circumstances. Data analytics enable insurers to offer personalized pricing, product recommendations, and service experiences that enhance customer satisfaction and retention. Modular product designs allow customers to adjust coverage levels and features as their needs evolve over time.

Sustainability integration influences product development, investment strategies, and corporate governance practices across the insurance industry. ESG considerations become increasingly important for consumers and regulators, driving demand for sustainable investment options within life insurance products. Green insurance products and carbon-neutral operations appeal to environmentally conscious consumers and support corporate sustainability objectives.

Health and wellness integration creates opportunities for innovative product features that reward healthy behaviors and provide additional value beyond traditional insurance protection. Wearable technology integration enables risk-based pricing and wellness program participation that can reduce premiums while promoting healthier lifestyles. Preventive health services and wellness coaching become differentiating factors in competitive market positioning.

Regulatory harmonization across European Union markets continues advancing through updated insurance directives and standardized consumer protection requirements. Solvency II implementation ensures adequate capital reserves while enabling risk-based approaches to regulatory compliance. Cross-border insurance operations benefit from harmonized regulatory frameworks that reduce compliance complexity and operational costs.

Technology partnerships between traditional insurers and fintech companies accelerate innovation in product development, distribution channels, and customer service delivery. Insurtech collaborations provide access to advanced technologies including artificial intelligence, blockchain, and advanced analytics that enhance operational capabilities and customer experience quality.

Market consolidation through strategic acquisitions and mergers creates larger, more efficient insurance organizations with enhanced scale economies and broader product portfolios. Partnership strategies enable companies to access new distribution channels, customer segments, and technological capabilities without full acquisition investments.

Product innovation focuses on hybrid offerings that combine traditional insurance protection with modern investment features, health and wellness benefits, and digital service capabilities. Modular product designs provide flexibility for customers to customize coverage while enabling insurers to address diverse market segments with standardized platform approaches. According to MarkWide Research analysis, product innovation initiatives drive 15% of new policy acquisitions in recent market periods.

Strategic recommendations for Austria’s life insurance market participants emphasize the importance of balanced approaches to digital transformation, product innovation, and customer relationship management. Investment priorities should focus on technology infrastructure that enhances operational efficiency while maintaining high-quality customer service standards that differentiate companies in competitive market conditions.

Product development strategies should emphasize flexibility, personalization, and value-added services that address evolving consumer needs and preferences. Hybrid product offerings that combine insurance protection with investment opportunities and wellness benefits can attract younger demographics while serving traditional customer segments. Risk-based pricing models enabled by advanced analytics can improve profitability while offering competitive rates to low-risk customers.

Distribution channel optimization requires balanced investment in digital platforms and traditional agent networks to serve diverse customer preferences effectively. Omnichannel approaches that integrate online and offline touchpoints provide seamless customer experiences while maximizing market reach and operational efficiency. Training and support for distribution partners ensure consistent service quality and product knowledge across all channels.

Market expansion opportunities exist in underserved demographic segments, specialized product categories, and cross-border operations within the European Union. Strategic partnerships with banks, employers, and technology companies can provide access to new customer segments while leveraging existing operational capabilities and market expertise. MWR projections indicate that targeted expansion strategies can achieve 12% higher growth rates compared to traditional market approaches.

Long-term growth prospects for Austria’s life insurance market remain positive, supported by demographic trends, regulatory stability, and ongoing innovation in product development and distribution channels. Market evolution will likely emphasize digital transformation, personalized products, and integrated financial services that address comprehensive consumer financial planning needs beyond traditional insurance protection.

Technology adoption will continue reshaping market dynamics through artificial intelligence, machine learning, and advanced data analytics that enable more sophisticated risk assessment, pricing models, and customer service capabilities. Digital-native consumers will drive demand for seamless online experiences and innovative product features that integrate with broader financial planning and lifestyle management platforms.

Regulatory developments will likely focus on consumer protection enhancement, sustainability requirements, and cross-border market integration that facilitates competition and innovation while maintaining market stability. Capital adequacy standards will continue evolving to address emerging risks while enabling sustainable business growth and market expansion opportunities.

Market projections indicate sustained growth momentum with annual growth rates of 4.5% expected over the next five-year period. MarkWide Research forecasts suggest that digital channel adoption will reach 35% of total market transactions by 2028, while unit-linked products may achieve 40% market share as consumer preferences continue shifting toward investment-oriented insurance solutions. Successful market participants will be those that effectively balance innovation with operational excellence while maintaining strong customer relationships and regulatory compliance.

Austria’s life insurance market represents a mature and dynamic sector with substantial growth potential driven by demographic trends, technological innovation, and evolving consumer preferences. The market benefits from stable regulatory frameworks, sophisticated distribution networks, and strong consumer awareness of financial planning importance. Competitive dynamics foster continuous improvement in product offerings, pricing strategies, and customer service quality while maintaining market stability and consumer protection.

Future success in this market will depend on companies’ ability to balance traditional insurance expertise with digital innovation, personalized product development, and comprehensive customer relationship management. Strategic investments in technology infrastructure, distribution channel optimization, and product innovation will be essential for maintaining competitive positioning and capturing growth opportunities in evolving market conditions.

Market participants that effectively address changing consumer needs through flexible product designs, convenient distribution channels, and value-added services will be best positioned to achieve sustainable growth and profitability. The Austria life insurance market continues offering significant opportunities for both established players and new entrants willing to invest in innovation and customer-centric business strategies that address the comprehensive financial planning needs of Austrian consumers.

What is Life Insurance?

Life insurance is a financial product that provides a monetary benefit to beneficiaries upon the death of the insured individual. It serves as a safety net for families, ensuring financial stability in the event of a loss, and can also include savings or investment components.

What are the key players in the Austria Life Insurance Market?

Key players in the Austria Life Insurance Market include companies such as Uniqa Insurance Group, Vienna Insurance Group, and Generali Group, among others. These companies offer a range of life insurance products tailored to meet the needs of consumers in Austria.

What are the growth factors driving the Austria Life Insurance Market?

The Austria Life Insurance Market is driven by factors such as increasing awareness of financial security, a growing aging population, and the rising demand for retirement planning solutions. Additionally, innovations in insurance products are attracting more consumers.

What challenges does the Austria Life Insurance Market face?

Challenges in the Austria Life Insurance Market include regulatory changes, intense competition among insurers, and the need for digital transformation to meet consumer expectations. These factors can impact profitability and market dynamics.

What opportunities exist in the Austria Life Insurance Market?

Opportunities in the Austria Life Insurance Market include the potential for product diversification, the introduction of technology-driven solutions, and the growing interest in sustainable investment options. Insurers can leverage these trends to attract new customers.

What trends are shaping the Austria Life Insurance Market?

Trends in the Austria Life Insurance Market include the increasing adoption of digital platforms for policy management, a focus on personalized insurance products, and the integration of health and wellness initiatives into life insurance offerings. These trends are reshaping how consumers interact with insurers.

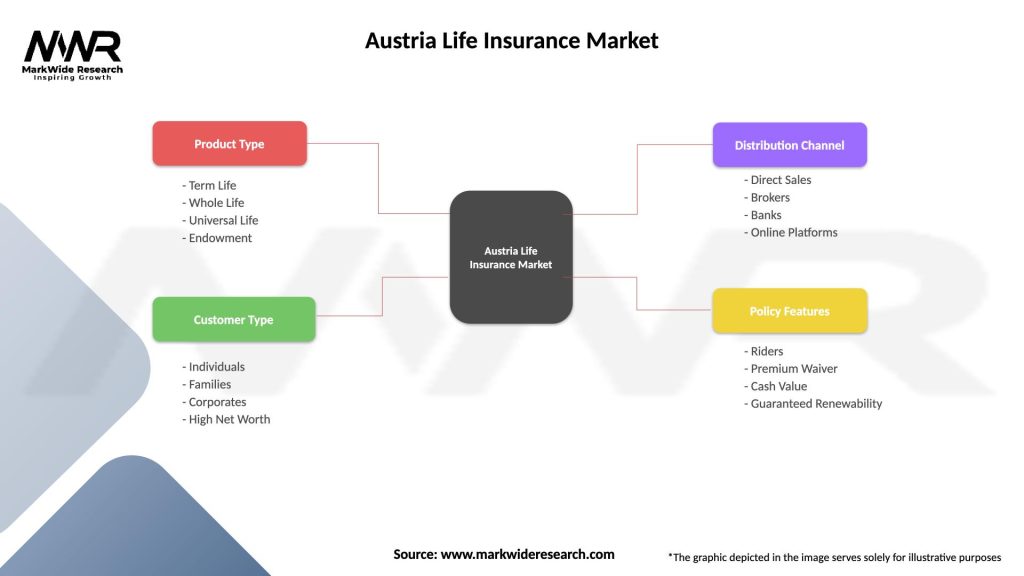

Austria Life Insurance Market

| Segmentation Details | Description |

|---|---|

| Product Type | Term Life, Whole Life, Universal Life, Endowment |

| Customer Type | Individuals, Families, Corporates, High Net Worth |

| Distribution Channel | Direct Sales, Brokers, Banks, Online Platforms |

| Policy Features | Riders, Premium Waiver, Cash Value, Guaranteed Renewability |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Austria Life Insurance Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.