The virtual cards market in Australia is witnessing rapid growth driven by the increasing adoption of digital payment solutions, the shift towards contactless transactions, and the demand for secure and convenient payment methods. Virtual cards, also known as digital cards or e-cards, are electronic payment instruments that enable users to make online purchases, manage expenses, and streamline payment processes. With the rise of e-commerce, mobile banking, and digital wallets, virtual cards offer a versatile and cost-effective alternative to traditional payment methods, driving their popularity among consumers and businesses alike.

Meaning

Virtual cards are digital payment cards issued by financial institutions or payment service providers, allowing users to conduct transactions electronically without the need for a physical plastic card. These cards are typically associated with a specific account or funding source and can be used for online purchases, subscriptions, recurring payments, and corporate expenses. Virtual cards are often generated dynamically, with unique card numbers, expiration dates, and security codes for each transaction, enhancing security and reducing the risk of fraud. They offer benefits such as real-time transaction tracking, expense management features, and enhanced security controls, making them an attractive payment solution for individuals, businesses, and financial institutions in Australia.

Executive Summary

The virtual cards market in Australia is experiencing significant growth driven by factors such as digital transformation, the proliferation of e-commerce, and the need for efficient payment solutions. The market offers opportunities for financial institutions, fintech companies, and payment service providers to innovate and expand their product offerings, catering to the evolving needs of consumers and businesses. However, challenges such as security concerns, regulatory compliance, and competition from traditional payment methods require market players to address effectively to capitalize on the growing demand for virtual cards in Australia.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Digital Payment Adoption: The widespread adoption of digital payment solutions in Australia, driven by smartphone penetration, mobile banking apps, and contactless payment technology, is fueling the demand for virtual cards among consumers and businesses.

E-commerce Growth: The booming e-commerce sector in Australia, coupled with the shift towards online shopping and digital transactions, is driving the adoption of virtual cards as a convenient and secure payment method for online purchases.

Expense Management: Virtual cards offer advanced expense management features such as transaction categorization, spending limits, and real-time reporting, making them a preferred choice for businesses looking to streamline payment processes and control expenses.

Security Enhancements: Virtual cards incorporate advanced security features such as tokenization, encryption, and dynamic card data, reducing the risk of fraud and unauthorized transactions compared to traditional plastic cards.

Market Drivers

Convenience and Flexibility: Virtual cards offer users the convenience of making secure payments online without the need for a physical card, providing flexibility and ease of use for both consumers and businesses.

Security and Fraud Prevention: The enhanced security features of virtual cards, including unique card numbers and transaction-specific data, help mitigate the risk of fraud and unauthorized transactions, enhancing trust and confidence among users.

Expense Management Solutions: Virtual cards enable businesses to track expenses, manage budgets, and control spending effectively, offering robust expense management solutions for corporate payments and employee reimbursements.

Contactless Payment Trends: The growing trend towards contactless payments, driven by factors such as hygiene concerns, convenience, and speed, is driving the adoption of virtual cards as a preferred payment method for online and in-store transactions.

Market Restraints

Security Concerns: Despite advancements in security features, virtual cards are still susceptible to cyber threats such as data breaches, identity theft, and account takeover, posing concerns for users and businesses about the safety of their financial information.

Regulatory Compliance: Compliance with regulatory requirements such as anti-money laundering (AML), know your customer (KYC), and data protection regulations presents challenges for virtual card issuers and payment service providers in Australia, requiring robust compliance measures and oversight.

Consumer Adoption Barriers: Limited awareness, trust issues, and reluctance to adopt new payment technologies may hinder the widespread adoption of virtual cards among consumers, especially older demographics and those accustomed to traditional payment methods.

Competition from Traditional Banks: Traditional banks and financial institutions may pose stiff competition to fintech companies and payment startups offering virtual card solutions, leveraging their existing customer base, brand recognition, and infrastructure to retain market share.

Market Opportunities

Partnerships and Collaborations: Collaborations between fintech startups, payment service providers, and traditional financial institutions offer opportunities to innovate and expand the virtual cards market in Australia, leveraging complementary strengths and resources.

Enhanced Security Solutions: Investment in advanced security technologies such as biometrics, artificial intelligence (AI), and machine learning (ML) can enhance the security and fraud prevention capabilities of virtual cards, boosting consumer confidence and trust.

Targeted Marketing Strategies: Targeted marketing campaigns, educational initiatives, and incentives can increase awareness and adoption of virtual cards among specific demographic segments, such as millennials, digital natives, and small businesses.

Integration with Digital Wallets: Integration with popular digital wallets and mobile payment platforms such as Apple Pay, Google Pay, and Samsung Pay can expand the reach and usability of virtual cards, offering seamless and convenient payment experiences for users.

Market Dynamics

The virtual cards market in Australia is characterized by dynamic trends, evolving consumer preferences, and technological innovations that shape market dynamics and drive growth opportunities. Market players must adapt to changing market conditions, regulatory requirements, and competitive pressures to succeed in the dynamic landscape of digital payments.

Regional Analysis

The virtual cards market in Australia exhibits regional variations in terms of market demand, adoption rates, and regulatory frameworks across different states and territories. Key metropolitan areas such as Sydney, Melbourne, and Brisbane serve as major hubs for fintech innovation, digital payments, and e-commerce activity, driving the adoption of virtual cards among urban populations and businesses.

Competitive Landscape

Leading Companies in the Australia Virtual Cards Market:

Commonwealth Bank of Australia (CBA)

Westpac Banking Corporation

Australia and New Zealand Banking Group Limited (ANZ)

National Australia Bank (NAB)

Macquarie Group Limited

HSBC Bank Australia Limited

Bendigo and Adelaide Bank Limited

Citibank Australia

Suncorp Group Limited

Bank of Queensland Limited

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

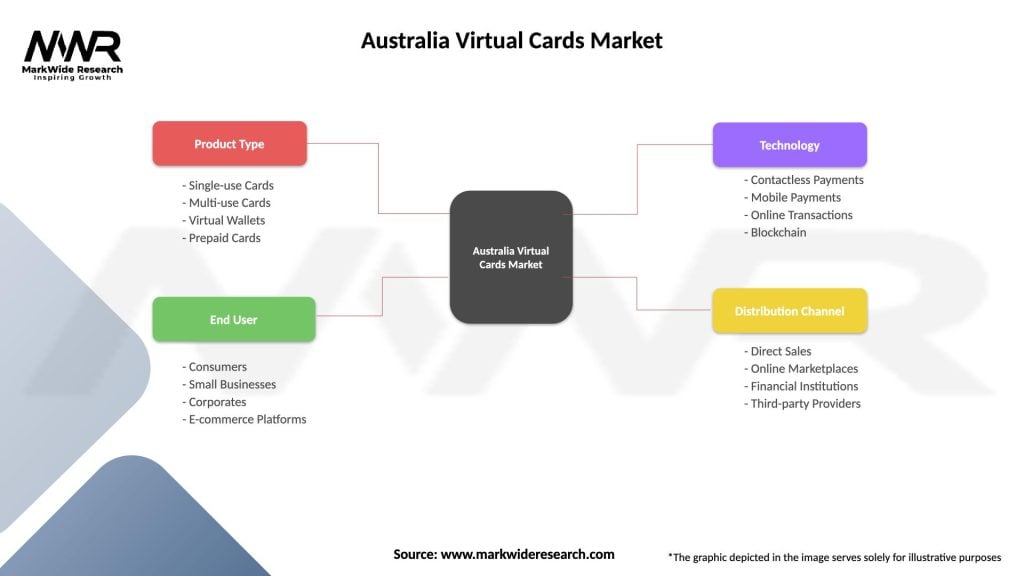

The virtual cards market in Australia can be segmented based on various factors such as:

User Type: Segmentation by user type includes individual consumers, businesses, corporate clients, and government organizations.

Use Case: Segmentation by use case includes personal payments, business expenses, corporate travel, online shopping, and subscription services.

Industry Vertical: Segmentation by industry vertical encompasses sectors such as retail, e-commerce, banking, financial services, insurance, healthcare, and travel.

Technology Platform: Segmentation by technology platform includes virtual card solutions integrated with digital wallets, mobile banking apps, and online payment gateways.

Segmentation enables market players to tailor their products, marketing strategies, and value propositions to specific customer segments, industry verticals, and use cases, maximizing market penetration and revenue opportunities.

Category-wise Insights

Consumer Virtual Cards: Consumer virtual cards offer individuals secure and convenient payment solutions for online shopping, subscription services, and personal expenses, with features such as spending controls, transaction monitoring, and rewards programs.

Business Expense Cards: Business expense cards cater to corporate clients and small businesses, providing expense management tools, employee spending controls, and integration with accounting software for streamlined financial management and reporting.

Corporate Travel Cards: Corporate travel cards facilitate employee travel expenses, accommodation bookings, and transportation payments, offering travel perks, insurance coverage, and travel assistance services for business travelers.

Supplier Payment Solutions: Virtual cards for supplier payments enable businesses to manage vendor payments, invoice processing, and procurement transactions efficiently, with features such as vendor onboarding, invoice matching, and payment reconciliation.

Key Benefits for Industry Participants and Stakeholders

Convenience and Accessibility: Virtual cards offer users the convenience of making payments anytime, anywhere, without the need for physical cards or cash, enhancing accessibility and usability for consumers and businesses.

Expense Management: Virtual cards provide robust expense management solutions for businesses, allowing them to track spending, control budgets, and automate reconciliation processes, improving financial visibility and control.

Security and Fraud Prevention: The enhanced security features of virtual cards, including tokenization, encryption, and transaction controls, help mitigate fraud risks, unauthorized transactions, and data breaches, enhancing trust and confidence among users.

Cost Savings: Virtual cards offer cost-saving benefits for businesses by reducing administrative overhead, eliminating paper-based processes, and optimizing payment workflows, resulting in operational efficiencies and financial savings.

Digital Transformation: Adopting virtual cards facilitates the digital transformation of payment processes, enabling businesses to embrace digital technologies, streamline operations, and enhance customer experiences in an increasingly digital economy.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the virtual cards market in Australia:

Strengths:

Enhanced security features

Convenience and usability

Expense management capabilities

Integration with digital wallets

Weaknesses:

Security concerns and fraud risks

Limited adoption among older demographics

Regulatory compliance challenges

Reliance on technology infrastructure

Opportunities:

Partnerships and collaborations

Enhanced security solutions

Targeted marketing strategies

Integration with digital ecosystems

Threats:

Competition from traditional banks

Regulatory changes and compliance requirements

Cybersecurity threats and data breaches

Consumer adoption barriers

Understanding these factors through a SWOT analysis helps market players identify their competitive advantages, address weaknesses, capitalize on opportunities, and mitigate potential threats in the dynamic landscape of digital payments.

Market Key Trends

Contactless Payment Adoption: The growing trend towards contactless payments, accelerated by the COVID-19 pandemic, is driving the adoption of virtual cards as a preferred payment method for in-store and online transactions, offering convenience, speed, and hygiene benefits.

Embedded Finance Solutions: Embedded finance solutions, including virtual cards embedded within fintech apps, e-commerce platforms, and digital wallets, are gaining traction, offering seamless and integrated payment experiences for users across various digital platforms.

Open Banking Initiatives: Open banking initiatives and regulatory reforms are promoting innovation and competition in the financial services sector, enabling fintech startups and third-party providers to leverage banking APIs and offer innovative virtual card solutions to consumers and businesses.

Subscription Economy: The rise of subscription-based business models in sectors such as media streaming, software-as-a-service (SaaS), and online subscriptions drives the demand for virtual cards as a convenient and secure payment solution for recurring payments and subscription renewals.

Covid-19 Impact

The COVID-19 pandemic has accelerated the adoption of virtual cards in Australia, driven by factors such as remote work, digital transformation, and the shift towards contactless payments. Some key impacts of COVID-19 on the virtual cards market include:

Remote Work and Digital Payments: The transition to remote work arrangements and digital business operations during the pandemic increases the demand for virtual cards as a secure and efficient payment solution for remote employees, online purchases, and corporate expenses.

E-commerce Growth and Contactless Payments: The surge in e-commerce activity and the preference for contactless payments amidst health and safety concerns drive the adoption of virtual cards as a preferred payment method for online shopping, subscription services, and digital transactions.

Expense Management Solutions: Virtual cards offer robust expense management solutions for businesses navigating the financial challenges of the pandemic, allowing them to track spending, control budgets, and automate payment processes in a remote work environment.

Regulatory Compliance and Security: Compliance with regulatory requirements such as PCI DSS, GDPR, and PSD2 becomes increasingly important amidst heightened security concerns, data breaches, and fraud risks during the pandemic, driving the demand for secure and compliant virtual card solutions.

Key Industry Developments

Mobile Wallet Integration: Virtual cards are increasingly integrated with mobile wallets such as Apple Pay, Google Pay, and Samsung Pay, enabling users to add virtual cards to their digital wallets and make contactless payments using their smartphones or wearable devices.

Biometric Authentication: Biometric authentication methods such as fingerprint recognition, facial recognition, and voice recognition are integrated into virtual card apps and payment platforms to enhance security and authentication for users, reducing the risk of unauthorized transactions and fraud.

Expense Tracking Features: Virtual card providers offer advanced expense tracking features, real-time spending alerts, and budgeting tools within their apps and platforms, empowering users to monitor their spending, track transactions, and manage their finances more effectively.

Virtual Card Marketplaces: Virtual card marketplaces and platforms emerge, offering a wide range of virtual card products, issuers, and features to consumers and businesses, facilitating comparison shopping, customization, and integration with digital ecosystems.

Analyst Suggestions

Enhance Security and Compliance: Market players should prioritize security and compliance initiatives, investing in advanced authentication methods, encryption technologies, and regulatory compliance frameworks to mitigate fraud risks and ensure data protection.

Improve User Experience: Focusing on user experience design, interface usability, and customer support services can enhance the adoption and retention of virtual card users, providing intuitive and seamless payment experiences across digital channels and devices.

Expand Value-added Services: Offering value-added services such as rewards programs, cashback incentives, and personalized offers can increase user engagement, loyalty, and retention, providing additional benefits and incentives for virtual card users.

Innovate with Technology: Continuous innovation in technology platforms, payment solutions, and security features is essential for market players to stay competitive and meet the evolving needs of consumers and businesses in the dynamic landscape of digital payments.

Future Outlook

The virtual cards market in Australia is poised for continued growth and innovation, driven by factors such as digital transformation, e-commerce expansion, and the demand for secure and convenient payment solutions. Market players that innovate with technology, enhance security and compliance measures, and prioritize user experience design will be well-positioned to capitalize on emerging opportunities and maintain a competitive edge in the evolving landscape of digital payments.

Conclusion

The virtual cards market in Australia is experiencing rapid growth and evolution, driven by the increasing adoption of digital payment solutions, the shift towards contactless transactions, and the demand for secure and convenient payment methods. Market players must navigate regulatory challenges, address security concerns, and innovate with technology to capitalize on the growing demand for virtual cards among consumers and businesses. By enhancing security measures, improving user experiences, and expanding value-added services, virtual card providers can unlock new opportunities, drive market growth, and contribute to the digital transformation of the payments industry in Australia.

What is Virtual Cards?

Virtual cards are digital payment cards that allow users to make online transactions without the need for a physical card. They provide a secure way to shop online by generating unique card numbers for each transaction, enhancing privacy and reducing fraud risk.

What are the key players in the Australia Virtual Cards Market?

Key players in the Australia Virtual Cards Market include companies like Visa, Mastercard, and American Express, which offer virtual card solutions for consumers and businesses. Additionally, fintech companies such as Revolut and Afterpay are also significant contributors to this market, among others.

What are the growth factors driving the Australia Virtual Cards Market?

The growth of the Australia Virtual Cards Market is driven by the increasing adoption of online shopping, the rise in digital payment solutions, and the growing need for enhanced security in online transactions. Additionally, the convenience of virtual cards for budgeting and managing expenses is also a contributing factor.

What challenges does the Australia Virtual Cards Market face?

The Australia Virtual Cards Market faces challenges such as regulatory compliance issues, potential cybersecurity threats, and the need for consumer education regarding the use of virtual cards. These factors can hinder widespread adoption and trust in virtual card solutions.

What opportunities exist in the Australia Virtual Cards Market?

Opportunities in the Australia Virtual Cards Market include the potential for partnerships between traditional banks and fintech companies to enhance service offerings. Additionally, the growing trend of subscription services and digital wallets presents new avenues for virtual card integration.

What trends are shaping the Australia Virtual Cards Market?

Trends shaping the Australia Virtual Cards Market include the increasing use of contactless payments, the integration of virtual cards with mobile wallets, and the rise of personalized financial services. These trends reflect a shift towards more flexible and user-friendly payment solutions.

Leading Companies in the Australia Virtual Cards Market:

Commonwealth Bank of Australia (CBA)

Westpac Banking Corporation

Australia and New Zealand Banking Group Limited (ANZ)

National Australia Bank (NAB)

Macquarie Group Limited

HSBC Bank Australia Limited

Bendigo and Adelaide Bank Limited

Citibank Australia

Suncorp Group Limited

Bank of Queensland Limited

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.