444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Australia data center power market represents a critical infrastructure segment experiencing unprecedented growth driven by digital transformation, cloud adoption, and increasing data consumption across the continent. Australia’s data center power infrastructure has evolved significantly to support the nation’s growing digital economy, with power systems becoming increasingly sophisticated and efficient to meet rising computational demands.

Market dynamics in Australia’s data center power sector reflect the country’s strategic position as a regional hub for digital services and cloud computing. The market encompasses various power solutions including uninterruptible power supplies (UPS), power distribution units (PDUs), generators, and advanced power management systems. Growth rates in this sector have been particularly robust, with the market expanding at a compound annual growth rate (CAGR) of 8.2% over recent years.

Regional distribution shows concentrated activity in major metropolitan areas, with Sydney and Melbourne accounting for approximately 65% of total market activity. The increasing focus on renewable energy integration and sustainability initiatives has further accelerated market development, positioning Australia as a leader in green data center power solutions within the Asia-Pacific region.

The Australia data center power market refers to the comprehensive ecosystem of electrical infrastructure, power management systems, and energy solutions specifically designed to support data center operations across Australian territories. This market encompasses all power-related components, services, and technologies required to ensure reliable, efficient, and scalable electrical supply to data processing facilities.

Data center power systems include primary power distribution, backup power generation, uninterruptible power supplies, power monitoring and management software, cooling system power requirements, and energy efficiency optimization solutions. The market serves various stakeholders including hyperscale cloud providers, colocation facilities, enterprise data centers, and edge computing installations throughout Australia’s diverse geographic landscape.

Australia’s data center power market demonstrates exceptional growth potential driven by accelerating digitalization, cloud migration, and the expansion of edge computing infrastructure. The market benefits from Australia’s stable political environment, robust telecommunications infrastructure, and strategic geographic position serving the Asia-Pacific region.

Key market drivers include the proliferation of 5G networks, increasing adoption of artificial intelligence and machine learning applications, and the growing demand for low-latency services. Government initiatives promoting digital infrastructure development have contributed to a 45% increase in data center power capacity over the past three years.

Sustainability considerations play an increasingly important role, with renewable energy adoption in data centers reaching 38% penetration rates across major facilities. The market landscape features both international technology providers and domestic specialists, creating a competitive environment that drives innovation and cost optimization.

Strategic insights reveal several critical trends shaping Australia’s data center power market evolution:

Digital transformation initiatives across Australian enterprises serve as the primary catalyst for data center power market expansion. Organizations are migrating critical workloads to cloud platforms, necessitating robust power infrastructure to support increased computational demands. The acceleration of remote work and digital services adoption has further intensified these requirements.

Government digitalization programs contribute significantly to market growth, with public sector organizations modernizing their IT infrastructure and adopting cloud-first strategies. These initiatives require substantial data center capacity expansion, directly driving power infrastructure investment.

5G network deployment creates substantial demand for edge computing facilities, requiring distributed power solutions across urban and regional areas. The low-latency requirements of 5G applications necessitate geographically dispersed data centers with reliable power systems.

Artificial intelligence and machine learning workloads demand high-performance computing infrastructure with specialized power requirements. The growing adoption of AI applications across industries drives the need for power systems capable of supporting GPU-intensive computing environments.

High capital investment requirements present significant barriers for market entry and expansion. Data center power infrastructure demands substantial upfront investment in equipment, installation, and ongoing maintenance, which can limit participation from smaller operators.

Skilled workforce shortages in specialized power systems engineering and maintenance create operational challenges. The technical complexity of modern data center power systems requires highly trained personnel, and the limited availability of such expertise can constrain market growth.

Regulatory complexity surrounding energy efficiency standards, environmental compliance, and grid connection requirements can slow project development timelines. Navigating multiple regulatory frameworks across different Australian states and territories adds complexity to large-scale deployments.

Grid infrastructure limitations in certain regional areas may restrict data center development opportunities. While major metropolitan areas have robust electrical grid infrastructure, some locations lack the power capacity necessary to support large-scale data center operations.

Renewable energy integration presents substantial opportunities for innovative power solutions. Australia’s abundant solar and wind resources create potential for data centers to achieve energy independence while reducing operational costs and environmental impact.

Edge computing expansion offers significant growth potential as 5G networks mature and Internet of Things (IoT) applications proliferate. The need for distributed computing infrastructure creates opportunities for specialized power solutions tailored to smaller, distributed facilities.

Energy storage integration represents an emerging opportunity as battery technology costs decline and grid stability becomes increasingly important. Advanced energy storage systems can provide both backup power and grid services, creating additional revenue streams for data center operators.

International expansion opportunities exist as Australian companies leverage their expertise to serve growing markets throughout the Asia-Pacific region. The country’s reputation for reliable infrastructure and technical expertise positions local providers for regional expansion.

Supply and demand dynamics in Australia’s data center power market reflect the rapid pace of digital infrastructure development. Demand consistently outpaces supply capacity, creating opportunities for both established providers and new market entrants. MarkWide Research analysis indicates that power infrastructure utilization rates have reached 78% across major metropolitan areas.

Technology evolution drives continuous market transformation, with advances in power efficiency, monitoring capabilities, and integration with renewable energy sources reshaping competitive dynamics. Providers must continuously innovate to maintain market position and meet evolving customer requirements.

Competitive intensity varies across market segments, with hyperscale facilities demanding highly specialized solutions while smaller enterprise data centers focus on cost-effective, standardized offerings. This segmentation creates opportunities for providers to specialize in specific market niches.

Investment patterns show increasing focus on sustainability and long-term operational efficiency rather than purely capital cost considerations. This shift influences technology selection and drives adoption of more sophisticated power management solutions.

Comprehensive market analysis employs multiple research methodologies to ensure accuracy and completeness of findings. Primary research includes extensive interviews with industry stakeholders, including data center operators, power system providers, and technology vendors across Australia’s major markets.

Secondary research incorporates analysis of industry reports, government publications, regulatory filings, and company financial statements to validate primary findings and identify market trends. This approach ensures comprehensive coverage of market dynamics and competitive landscape factors.

Data validation processes include cross-referencing multiple sources, statistical analysis of market trends, and expert review of findings to ensure reliability and accuracy. Quantitative analysis focuses on market sizing, growth projections, and segmentation analysis.

Industry expert consultation provides qualitative insights into market dynamics, technology trends, and future outlook. These consultations help validate quantitative findings and provide context for market developments and competitive dynamics.

New South Wales dominates the Australian data center power market, accounting for approximately 42% of total market activity. Sydney’s position as Australia’s financial and technology hub drives substantial demand for data center services, supported by robust power infrastructure and proximity to submarine cable landing points.

Victoria represents the second-largest regional market with 28% market share, driven by Melbourne’s role as a major business center and the state’s progressive renewable energy policies. The region benefits from competitive electricity markets and strong government support for digital infrastructure development.

Queensland shows rapid growth potential, particularly in Brisbane and the Gold Coast, with increasing focus on serving Asia-Pacific markets. The state’s tropical climate creates unique cooling challenges but also opportunities for innovative power and cooling integration solutions.

Western Australia presents emerging opportunities driven by the mining sector’s digital transformation and Perth’s growing role as a regional technology hub. The state’s abundant renewable energy resources create potential for sustainable data center development.

South Australia and Tasmania offer niche opportunities, particularly for renewable energy-powered facilities. These regions benefit from competitive electricity costs and strong renewable energy resources, attracting environmentally conscious data center operators.

Market leadership in Australia’s data center power sector features a mix of international technology giants and specialized local providers. The competitive environment encourages innovation and drives continuous improvement in power efficiency and reliability.

Competitive strategies focus on technological innovation, service excellence, and sustainability credentials. Providers increasingly offer comprehensive solutions combining power systems with monitoring, maintenance, and optimization services.

By Power Rating:

By Component:

UPS Systems segment represents the largest component category, driven by increasing reliability requirements and power quality concerns. Modern UPS systems incorporate advanced features including lithium-ion batteries, modular designs, and intelligent monitoring capabilities. The segment benefits from 12% annual growth rates as data centers prioritize uptime and power quality.

Power Distribution category shows steady growth driven by data center expansion and modernization projects. Advanced power distribution units (PDUs) with remote monitoring and control capabilities are increasingly popular, enabling better power management and operational efficiency.

Backup Generator segment experiences strong demand driven by grid reliability concerns and regulatory requirements. Natural gas generators are gaining popularity due to environmental considerations and fuel availability, while diesel generators remain dominant for critical applications.

Monitoring and Management systems represent the fastest-growing category as operators seek to optimize power efficiency and reduce operational costs. Advanced analytics and artificial intelligence integration enable predictive maintenance and automated power optimization.

Data Center Operators benefit from improved reliability, reduced operational costs, and enhanced sustainability credentials through advanced power solutions. Modern power systems enable better capacity planning, predictive maintenance, and energy efficiency optimization.

Technology Providers gain access to a rapidly growing market with substantial investment potential and opportunities for innovation. The market rewards providers who can deliver integrated solutions combining power, cooling, and monitoring capabilities.

End Users benefit from improved service reliability, reduced downtime, and better performance for their digital applications. Advanced power infrastructure enables data centers to offer higher service level agreements and better customer experiences.

Government and Regulators benefit from improved digital infrastructure supporting economic development and competitiveness. Sustainable power solutions contribute to environmental goals and energy security objectives.

Local Communities benefit from job creation, economic development, and improved digital services availability. Data center investments often catalyze broader technology sector development and infrastructure improvements.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration emerges as the dominant trend, with data center operators increasingly prioritizing renewable energy sources and carbon-neutral operations. This trend drives demand for advanced power management systems capable of integrating with solar, wind, and battery storage systems.

Edge computing proliferation creates demand for distributed power solutions optimized for smaller, unmanned facilities. These edge data centers require highly reliable, remotely monitored power systems with minimal maintenance requirements.

Artificial intelligence adoption in power management enables predictive maintenance, automated optimization, and improved efficiency. AI-powered systems can anticipate equipment failures, optimize power distribution, and reduce energy consumption.

Modular design approaches gain popularity as operators seek flexible, scalable solutions that can adapt to changing requirements. Modular power systems enable rapid deployment and easy capacity expansion as demand grows.

Lithium-ion battery adoption accelerates as costs decline and performance improves. These batteries offer advantages including smaller footprint, longer life, and better performance compared to traditional lead-acid batteries.

Major infrastructure investments by global cloud providers continue to reshape the market landscape. Recent announcements of multi-billion dollar data center investments demonstrate confidence in Australia’s market potential and drive demand for advanced power solutions.

Government policy initiatives supporting digital infrastructure development create favorable conditions for market growth. These policies include streamlined approval processes, tax incentives, and support for renewable energy integration.

Technology partnerships between international providers and local companies accelerate innovation and market development. These collaborations combine global expertise with local market knowledge to deliver optimized solutions.

Sustainability certifications become increasingly important as operators seek to demonstrate environmental responsibility. Green building standards and carbon neutrality commitments influence technology selection and procurement decisions.

Supply chain diversification efforts aim to reduce dependence on single-source suppliers and improve resilience. These initiatives include development of local manufacturing capabilities and alternative supplier relationships.

MarkWide Research recommends that market participants focus on developing integrated solutions combining power, cooling, and monitoring capabilities. The convergence of these technologies creates opportunities for providers who can offer comprehensive, optimized systems.

Investment in sustainability capabilities should be prioritized as environmental considerations become increasingly important in procurement decisions. Providers should develop expertise in renewable energy integration and carbon footprint optimization.

Edge computing specialization offers significant growth potential as 5G networks mature and IoT applications proliferate. Developing solutions optimized for distributed, unmanned facilities can capture this emerging market segment.

Local partnership development can help international providers better serve the Australian market while providing local companies access to global technology and expertise. These partnerships can accelerate market penetration and innovation.

Workforce development initiatives should address the growing skills gap in specialized power systems engineering and maintenance. Investment in training and certification programs can ensure adequate technical expertise availability.

Market growth trajectory remains strongly positive, driven by continued digital transformation and cloud adoption across Australian enterprises. The market is expected to maintain robust growth rates exceeding 8% annually over the next five years, supported by increasing data consumption and computational requirements.

Technology evolution will continue to drive market transformation, with advances in power efficiency, renewable energy integration, and intelligent management systems reshaping competitive dynamics. Providers who can adapt to these technological changes will capture the greatest market opportunities.

Sustainability requirements will become increasingly stringent, driving adoption of renewable energy sources and energy-efficient technologies. Data centers achieving carbon neutrality will gain competitive advantages in attracting environmentally conscious customers.

Regional expansion opportunities will emerge as Australian providers leverage their expertise to serve growing markets throughout the Asia-Pacific region. The country’s reputation for reliable infrastructure and technical expertise positions local companies for international growth.

MWR projections indicate that edge computing will represent 25% of total market activity by 2028, driven by 5G deployment and IoT application growth. This shift will create new requirements for distributed power solutions and remote monitoring capabilities.

Australia’s data center power market presents exceptional growth opportunities driven by digital transformation, cloud adoption, and the nation’s strategic position in the Asia-Pacific region. The market benefits from stable political conditions, abundant renewable energy resources, and strong government support for digital infrastructure development.

Key success factors for market participants include technological innovation, sustainability credentials, and the ability to deliver integrated solutions combining power, cooling, and monitoring capabilities. The growing importance of edge computing and renewable energy integration creates new opportunities for specialized providers.

Future market development will be shaped by continued technology evolution, increasing sustainability requirements, and the expansion of 5G networks driving edge computing demand. Organizations that can adapt to these trends while maintaining focus on reliability and efficiency will achieve the greatest success in Australia’s dynamic data center power market.

What is Data Center Power?

Data Center Power refers to the electrical power supply and management systems that support the operation of data centers, which house computer systems and associated components. This includes power distribution, backup systems, and energy efficiency measures.

What are the key players in the Australia Data Center Power Market?

Key players in the Australia Data Center Power Market include companies like NEXTDC, Equinix, and Digital Realty, which provide critical infrastructure and services for data centers. These companies focus on enhancing power efficiency and reliability, among others.

What are the growth factors driving the Australia Data Center Power Market?

The Australia Data Center Power Market is driven by the increasing demand for cloud computing, the rise of big data analytics, and the growing need for data storage solutions. Additionally, advancements in energy-efficient technologies are contributing to market growth.

What challenges does the Australia Data Center Power Market face?

Challenges in the Australia Data Center Power Market include the high energy consumption of data centers, regulatory compliance regarding energy efficiency, and the need for sustainable power sources. These factors can impact operational costs and environmental sustainability.

What opportunities exist in the Australia Data Center Power Market?

Opportunities in the Australia Data Center Power Market include the adoption of renewable energy sources, innovations in energy management systems, and the expansion of edge computing facilities. These trends can enhance operational efficiency and reduce carbon footprints.

What trends are shaping the Australia Data Center Power Market?

Trends in the Australia Data Center Power Market include the increasing integration of artificial intelligence for power management, the shift towards modular data center designs, and the focus on sustainability initiatives. These trends are influencing how data centers operate and consume power.

Australia Data Center Power Market

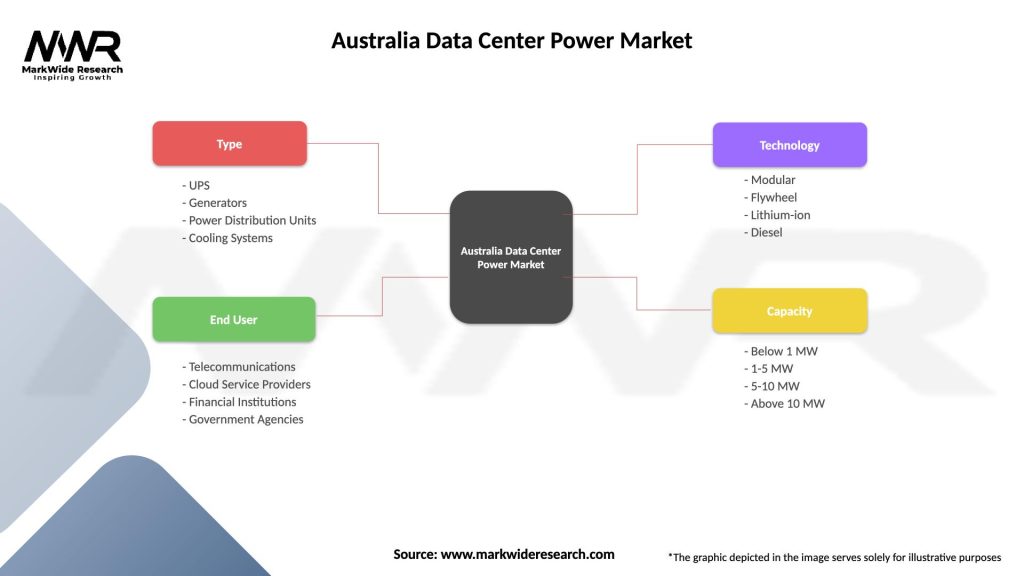

| Segmentation Details | Description |

|---|---|

| Type | UPS, Generators, Power Distribution Units, Cooling Systems |

| End User | Telecommunications, Cloud Service Providers, Financial Institutions, Government Agencies |

| Technology | Modular, Flywheel, Lithium-ion, Diesel |

| Capacity | Below 1 MW, 1-5 MW, 5-10 MW, Above 10 MW |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Australia Data Center Power Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.