444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Australia and New Zealand plastic packaging film market represents a dynamic and rapidly evolving sector within the broader packaging industry. This market encompasses a diverse range of flexible packaging solutions including polyethylene films, polypropylene films, polyester films, and specialized barrier films used across multiple industries. Market dynamics in this region are driven by increasing consumer demand for convenient packaging, growing e-commerce activities, and stringent food safety regulations that require advanced packaging solutions.

Regional characteristics of the Australia and New Zealand market include a strong focus on sustainability initiatives, with both countries implementing progressive environmental policies that influence packaging material choices. The market demonstrates robust growth potential, with industry projections indicating a compound annual growth rate of 4.2% through the forecast period. Key applications span across food and beverage packaging, pharmaceutical packaging, industrial applications, and consumer goods packaging, each segment contributing significantly to overall market expansion.

Technological advancements in film manufacturing processes, including multi-layer extrusion technologies and advanced barrier coating systems, are reshaping the competitive landscape. The market benefits from strong domestic manufacturing capabilities combined with strategic imports of specialized film materials. Consumer preferences increasingly favor packaging solutions that offer extended shelf life, enhanced product protection, and improved sustainability credentials, driving innovation in biodegradable and recyclable film technologies.

The Australia and New Zealand plastic packaging film market refers to the comprehensive ecosystem of flexible plastic film materials designed for packaging applications across both countries. This market encompasses the production, distribution, and consumption of various plastic film types including blown films, cast films, and specialty barrier films used to protect, preserve, and present products across multiple industry sectors.

Market scope includes polyethylene-based films such as LDPE, LLDPE, and HDPE variants, polypropylene films including BOPP and CPP types, polyester films, and emerging bio-based alternatives. These materials serve critical functions in maintaining product integrity, extending shelf life, and providing cost-effective packaging solutions for manufacturers and retailers throughout Australia and New Zealand.

Geographic coverage spans both countries’ diverse economic landscapes, from Australia’s major metropolitan centers and industrial hubs to New Zealand’s agricultural and manufacturing regions. The market definition includes domestic production facilities, import activities, and the entire value chain from raw material suppliers to end-user applications across food processing, pharmaceuticals, industrial packaging, and consumer goods sectors.

Market performance in the Australia and New Zealand plastic packaging film sector demonstrates consistent growth momentum driven by expanding end-user industries and evolving consumer preferences. The market benefits from strong economic fundamentals in both countries, with Australia’s diverse industrial base and New Zealand’s robust agricultural sector providing stable demand foundations for packaging film applications.

Key growth drivers include the rapid expansion of e-commerce activities, which has increased demand for protective packaging films by approximately 28% over the past three years. The food and beverage sector remains the largest application segment, accounting for 45% of total market consumption, followed by industrial applications and pharmaceutical packaging. Sustainability initiatives are increasingly influencing purchasing decisions, with recyclable and bio-based films gaining market traction.

Competitive dynamics feature a mix of international players and regional specialists, with market consolidation trends evident as companies seek to enhance their technological capabilities and geographic reach. Innovation focuses on developing high-performance barrier films, improving recyclability characteristics, and reducing material thickness while maintaining protective properties. Regulatory compliance with food contact regulations and environmental standards continues to shape product development strategies across the market.

Strategic market insights reveal several critical trends shaping the Australia and New Zealand plastic packaging film landscape. The following key observations provide essential understanding of market dynamics:

Primary market drivers propelling growth in the Australia and New Zealand plastic packaging film market stem from multiple interconnected factors across economic, technological, and consumer preference dimensions. The expanding food and beverage industry represents the most significant growth catalyst, with increasing demand for processed and packaged foods driving substantial consumption of flexible packaging films.

E-commerce expansion continues to generate robust demand for protective packaging solutions, with online retail growth creating new requirements for films that provide product protection during shipping and handling. The pharmaceutical sector’s growth, particularly in aging population demographics, drives demand for specialized barrier films that ensure product integrity and compliance with regulatory standards. Technological innovations in film manufacturing enable the development of lighter, stronger, and more sustainable packaging solutions that meet evolving market requirements.

Regulatory support for food safety and quality standards creates consistent demand for high-performance packaging films that extend shelf life and maintain product freshness. The growing awareness of food waste reduction drives adoption of advanced packaging technologies that help preserve product quality throughout the supply chain. Industrial applications across construction, agriculture, and manufacturing sectors provide additional growth momentum, with specialized films serving diverse protective and functional requirements.

Market constraints affecting the Australia and New Zealand plastic packaging film sector include environmental concerns and regulatory pressures related to plastic waste management. Increasing scrutiny of single-use plastics creates challenges for traditional packaging film applications, with governments implementing policies that restrict certain plastic packaging types and promote alternative materials.

Raw material price volatility represents a significant operational challenge, with petroleum-based feedstock costs fluctuating based on global energy markets and supply chain disruptions. These price variations impact manufacturing costs and profit margins, particularly affecting smaller regional producers with limited pricing power. Competition from alternative materials including paper-based packaging, metal foils, and bio-based alternatives creates pressure on traditional plastic film applications.

Technical limitations in recycling infrastructure pose challenges for circular economy initiatives, with limited processing capabilities for certain film types affecting end-of-life management options. Consumer perception issues regarding plastic packaging sustainability create market resistance in certain segments, requiring significant investment in education and product development. Supply chain complexities including transportation costs and logistics challenges, particularly for New Zealand’s geographic isolation, impact market accessibility and cost structures.

Emerging opportunities in the Australia and New Zealand plastic packaging film market center around sustainability innovations and technological advancements that address environmental concerns while maintaining packaging performance. The development of biodegradable and compostable films presents significant growth potential, with increasing consumer and regulatory support for environmentally responsible packaging solutions.

Advanced barrier technologies offer opportunities to develop ultra-thin films that provide superior protection with reduced material usage, addressing both cost and environmental objectives. The growing demand for smart packaging solutions incorporating sensors, indicators, and interactive features creates new market segments for specialized film applications. Circular economy initiatives drive opportunities for developing films with enhanced recyclability and compatibility with existing waste management infrastructure.

Export potential to Asia-Pacific markets presents growth opportunities for Australian and New Zealand manufacturers, leveraging regional proximity and established trade relationships. The expansion of premium food and beverage segments creates demand for high-performance packaging films that support product differentiation and brand positioning. Industrial applications in renewable energy, construction, and agriculture sectors offer diversification opportunities beyond traditional packaging markets, with specialized films serving unique performance requirements.

Market dynamics in the Australia and New Zealand plastic packaging film sector reflect complex interactions between supply-side capabilities, demand-side requirements, and regulatory influences. The competitive landscape features established international players alongside regional specialists, creating a diverse ecosystem that serves varied market segments with different performance and cost requirements.

Supply chain dynamics involve raw material sourcing from both domestic and international suppliers, with polyethylene and polypropylene resins representing the primary feedstock materials. Manufacturing operations utilize advanced extrusion technologies to produce films with specific thickness, barrier, and mechanical properties tailored to end-user applications. Distribution networks span both countries through established packaging distributors and direct manufacturer relationships.

Demand patterns vary significantly across application segments, with food packaging showing seasonal fluctuations related to agricultural cycles and consumer consumption patterns. Industrial applications demonstrate more consistent demand profiles, while pharmaceutical packaging growth correlates with healthcare sector expansion. Price dynamics reflect raw material costs, manufacturing efficiency improvements, and competitive pressures, with market participants continuously optimizing cost structures while maintaining quality standards.

Research methodology for analyzing the Australia and New Zealand plastic packaging film market employs comprehensive primary and secondary research approaches to ensure accurate market assessment and reliable insights. Primary research activities include structured interviews with industry executives, manufacturers, distributors, and end-users across both countries to gather firsthand market intelligence and validate secondary research findings.

Secondary research encompasses analysis of industry publications, government statistics, trade association reports, and company financial statements to establish market baselines and identify trends. Data collection covers production statistics, import/export data, consumption patterns, and regulatory developments affecting the packaging film industry. Market sizing methodologies utilize both top-down and bottom-up approaches to ensure comprehensive coverage and cross-validation of market estimates.

Analytical frameworks include competitive landscape mapping, value chain analysis, and market segmentation studies to provide detailed understanding of market structure and dynamics. Quality assurance processes involve data triangulation, expert validation, and peer review to ensure research accuracy and reliability. Forecasting models incorporate historical trends, economic indicators, and industry-specific drivers to project future market development scenarios across different time horizons.

Regional analysis reveals distinct market characteristics between Australia and New Zealand, with each country demonstrating unique demand patterns, competitive dynamics, and growth opportunities. Australia represents the larger market segment, accounting for approximately 78% of combined regional consumption, driven by its larger population base, diverse industrial sector, and extensive food processing capabilities.

Australian market dynamics feature strong manufacturing presence in major industrial centers including Melbourne, Sydney, and Brisbane, with established production facilities serving both domestic and export markets. The country’s diverse economy supports broad-based demand across food processing, mining, agriculture, and manufacturing sectors. New Zealand’s market profile emphasizes agricultural and food processing applications, with the country’s strong dairy and meat processing industries driving significant packaging film consumption.

Geographic distribution patterns show concentration in major metropolitan areas and industrial regions, with rural areas representing important agricultural packaging applications. Cross-border trade between Australia and New Zealand facilitates market integration, with specialized products and technologies shared across both countries. Regional growth rates vary by application segment, with New Zealand showing stronger growth in agricultural packaging applications while Australia demonstrates broader industrial market expansion.

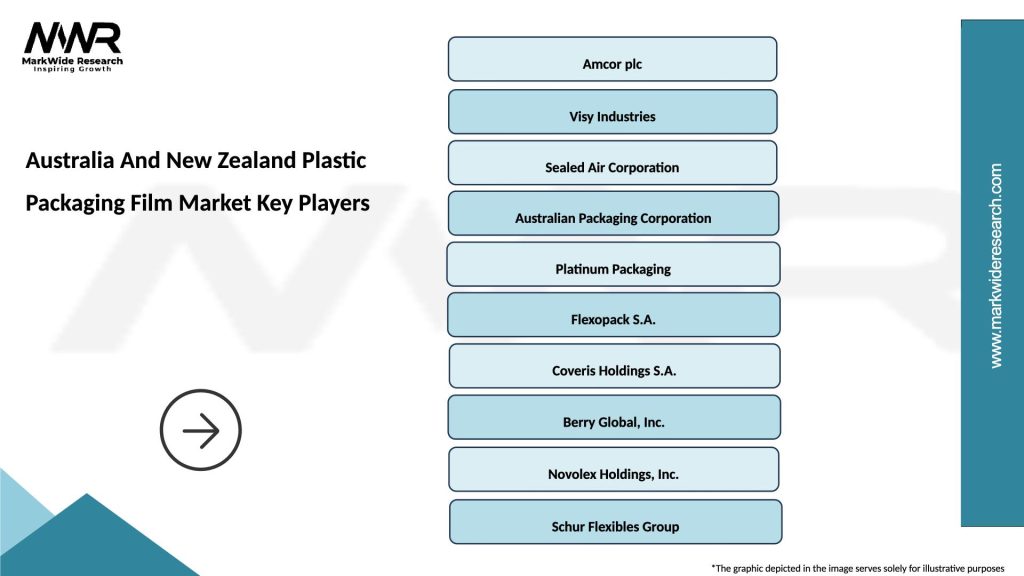

Competitive landscape in the Australia and New Zealand plastic packaging film market features a diverse mix of international corporations, regional manufacturers, and specialized converters serving different market segments. Market leadership positions vary by application segment and geographic region, with companies competing on factors including product quality, technical innovation, customer service, and cost competitiveness.

Major market participants include established players with comprehensive product portfolios and extensive distribution networks:

Competitive strategies emphasize product innovation, sustainability initiatives, and customer relationship development to maintain market position and drive growth in an increasingly competitive environment.

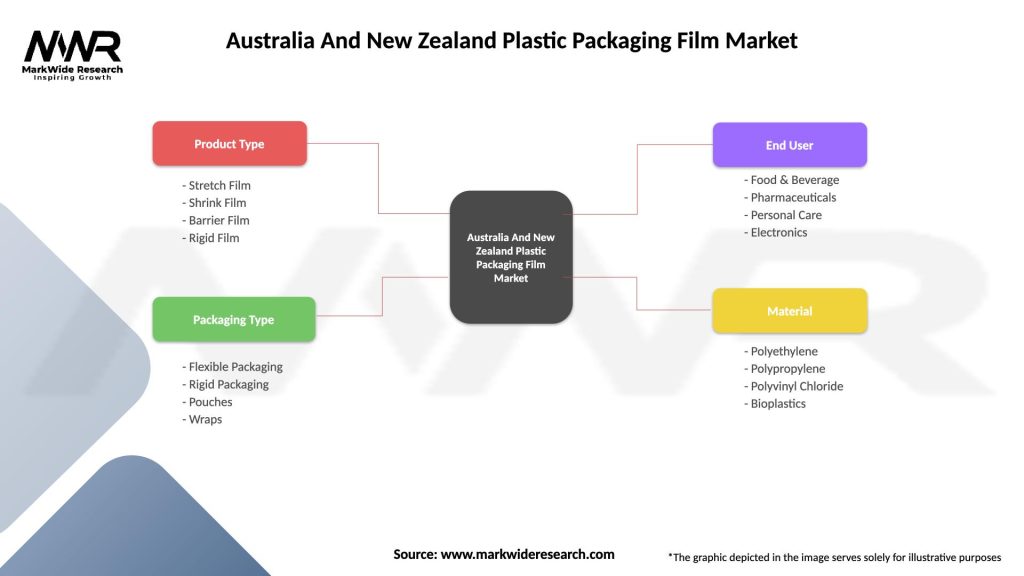

Market segmentation analysis reveals multiple classification approaches that provide comprehensive understanding of the Australia and New Zealand plastic packaging film market structure. Segmentation by material type, application, end-user industry, and technology enables detailed market analysis and strategic planning for industry participants.

By Material Type:

By Application:

By Technology:

Food packaging applications dominate the Australia and New Zealand plastic packaging film market, representing the largest consumption segment with consistent growth driven by expanding food processing industries and evolving consumer preferences. This category benefits from stringent food safety regulations that require high-performance packaging solutions to ensure product integrity and extended shelf life.

Fresh produce packaging shows particular strength in both countries, with advanced films enabling extended freshness and reduced food waste. The dairy industry, especially prominent in New Zealand, drives significant demand for specialized barrier films that protect product quality during distribution and storage. Processed food packaging continues expanding with convenience food trends and portion control requirements driving innovation in resealable and easy-open film technologies.

Industrial packaging applications demonstrate steady growth across construction, mining, and agricultural sectors, with films serving protective and functional roles in harsh operating environments. The pharmaceutical segment shows robust growth potential, driven by aging populations and expanding healthcare sectors in both countries. Sustainability considerations increasingly influence category development, with bio-based and recyclable films gaining market share across all application segments, representing approximately 18% of total market volume and growing at 12% annually.

Industry participants in the Australia and New Zealand plastic packaging film market benefit from multiple value creation opportunities across the supply chain. Manufacturers gain from strong domestic demand, established distribution networks, and opportunities for export expansion to Asia-Pacific markets. Technological capabilities in both countries support innovation in sustainable packaging solutions, enabling companies to differentiate their offerings and capture premium market segments.

Stakeholder benefits extend throughout the value chain, with raw material suppliers benefiting from consistent demand and opportunities for specialty resin development. Converters and distributors gain from diverse application segments that provide stability and growth opportunities across economic cycles. End-users benefit from access to high-quality packaging solutions that enhance product protection, extend shelf life, and support brand differentiation strategies.

Economic benefits include job creation in manufacturing and related service sectors, with the packaging film industry supporting thousands of direct and indirect employment opportunities. Environmental benefits emerge from ongoing sustainability initiatives, including development of recyclable and biodegradable films that reduce environmental impact. Innovation ecosystems in both countries foster collaboration between industry, research institutions, and government agencies to advance packaging technology and sustainability objectives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping the Australia and New Zealand plastic packaging film market, with companies investing heavily in developing recyclable, biodegradable, and bio-based film alternatives. This trend reflects both regulatory pressures and consumer demand for environmentally responsible packaging solutions, driving innovation across the entire value chain.

Smart packaging integration emerges as a key technology trend, with films incorporating sensors, indicators, and interactive features that provide real-time information about product condition and authenticity. These advanced solutions serve growing demand for food safety assurance and supply chain transparency. Lightweighting initiatives continue advancing, with manufacturers developing thinner films that maintain performance while reducing material usage and environmental impact.

Customization and personalization trends drive demand for specialized films that support brand differentiation and consumer engagement. Digital printing technologies enable cost-effective short-run production of customized packaging films, supporting niche market applications and premium product positioning. Circular economy adoption accelerates with improved recycling technologies and infrastructure development, enabling closed-loop packaging systems that reduce waste and resource consumption. According to MarkWide Research analysis, these sustainability-focused trends are expected to influence 75% of packaging decisions by industry participants over the next five years.

Recent industry developments highlight significant investments in sustainable packaging technologies and manufacturing capacity expansion across the Australia and New Zealand market. Major manufacturers have announced substantial capital commitments to develop biodegradable film production capabilities and enhance recycling infrastructure to support circular economy objectives.

Technology partnerships between packaging companies and research institutions accelerate innovation in advanced barrier films and smart packaging applications. These collaborations focus on developing next-generation materials that combine superior performance with environmental responsibility. Regulatory developments include updated food contact regulations and extended producer responsibility programs that influence packaging design and material selection decisions.

Market consolidation activities continue with strategic acquisitions and partnerships aimed at expanding geographic reach and technological capabilities. International companies increase their regional presence through local partnerships and manufacturing investments, while regional players seek scale advantages through consolidation. Sustainability certifications gain importance as companies pursue third-party validation of their environmental claims and circular economy contributions. Infrastructure investments in recycling facilities and collection systems support the transition toward more sustainable packaging systems across both countries.

Strategic recommendations for industry participants in the Australia and New Zealand plastic packaging film market emphasize the critical importance of sustainability integration and innovation investment. Companies should prioritize development of recyclable and bio-based film alternatives to address regulatory requirements and consumer preferences while maintaining competitive positioning in traditional market segments.

Investment priorities should focus on advanced manufacturing technologies that enable production of high-performance, lightweight films with reduced environmental impact. Partnerships with recycling infrastructure providers and waste management companies can create competitive advantages in circular economy applications. Market diversification strategies should explore emerging applications in smart packaging, pharmaceutical applications, and industrial specialties to reduce dependence on traditional commodity segments.

Operational excellence initiatives should emphasize supply chain optimization, cost management, and quality assurance to maintain competitiveness in price-sensitive market segments. Companies should invest in customer education and technical support services to drive adoption of sustainable packaging solutions. Export development strategies should leverage regional proximity to Asia-Pacific markets, with focus on high-value specialty films and sustainable packaging solutions where Australian and New Zealand companies can differentiate their offerings. MWR analysis suggests that companies implementing comprehensive sustainability strategies achieve 23% higher customer retention rates compared to traditional approaches.

Future market prospects for the Australia and New Zealand plastic packaging film sector appear positive, with sustained growth expected across multiple application segments despite environmental challenges and regulatory pressures. The market is projected to maintain steady expansion, driven by continued economic growth, population increases, and evolving consumer preferences for convenient packaging solutions.

Sustainability transformation will accelerate over the forecast period, with bio-based and recyclable films expected to capture increasing market share as production costs decline and performance characteristics improve. Smart packaging applications will emerge as a significant growth driver, particularly in food safety and pharmaceutical applications where real-time monitoring capabilities provide substantial value. Technology advancement will enable development of ultra-thin, high-performance films that address both cost and environmental objectives.

Market structure evolution will likely feature continued consolidation as companies seek scale advantages and technological capabilities to compete in an increasingly sophisticated market environment. Export opportunities to Asia-Pacific markets will expand as regional trade relationships strengthen and demand for high-quality packaging solutions grows. Regulatory landscape will continue evolving toward greater sustainability requirements, creating both challenges and opportunities for industry participants. The market is expected to achieve a compound annual growth rate of 4.8% over the next five years, with sustainable packaging solutions growing at 9.2% annually as they gain mainstream adoption across all application segments.

The Australia and New Zealand plastic packaging film market stands at a critical juncture, balancing traditional growth drivers with emerging sustainability imperatives that will shape future development. The market demonstrates resilient fundamentals supported by diverse end-user industries, established manufacturing capabilities, and strong economic foundations in both countries.

Key success factors for industry participants include embracing sustainability innovation, investing in advanced manufacturing technologies, and developing comprehensive strategies that address both performance and environmental requirements. The transition toward circular economy principles presents both challenges and opportunities, requiring significant investment in new technologies and business models while creating potential for market differentiation and premium positioning.

Market outlook remains positive despite regulatory pressures and environmental concerns, with continued growth expected across most application segments. The industry’s ability to successfully navigate the sustainability transformation while maintaining cost competitiveness and performance standards will determine long-term success. Companies that proactively address environmental concerns through innovation and strategic partnerships are positioned to capture the greatest opportunities in this evolving market landscape, contributing to both economic growth and environmental stewardship across the Australia and New Zealand region.

What is Plastic Packaging Film?

Plastic packaging film refers to thin, flexible sheets made from various types of plastic, used primarily for packaging products. These films are widely utilized in food packaging, consumer goods, and industrial applications due to their lightweight and protective properties.

What are the key players in the Australia And New Zealand Plastic Packaging Film Market?

Key players in the Australia And New Zealand Plastic Packaging Film Market include Amcor, Sealed Air Corporation, and Visy Industries, among others. These companies are known for their innovative packaging solutions and extensive distribution networks.

What are the growth factors driving the Australia And New Zealand Plastic Packaging Film Market?

The growth of the Australia And New Zealand Plastic Packaging Film Market is driven by increasing demand for convenient packaging solutions, the rise of e-commerce, and a growing focus on food safety and shelf life extension. Additionally, the trend towards sustainable packaging options is influencing market dynamics.

What challenges does the Australia And New Zealand Plastic Packaging Film Market face?

The Australia And New Zealand Plastic Packaging Film Market faces challenges such as environmental concerns regarding plastic waste, regulatory pressures for sustainable materials, and competition from alternative packaging solutions. These factors can impact market growth and innovation.

What opportunities exist in the Australia And New Zealand Plastic Packaging Film Market?

Opportunities in the Australia And New Zealand Plastic Packaging Film Market include the development of biodegradable films, advancements in recycling technologies, and increasing consumer preference for eco-friendly packaging. These trends can lead to new product innovations and market expansion.

What trends are shaping the Australia And New Zealand Plastic Packaging Film Market?

Trends shaping the Australia And New Zealand Plastic Packaging Film Market include the shift towards sustainable packaging solutions, the integration of smart packaging technologies, and the growing demand for customized packaging designs. These trends are influencing how companies approach product development and consumer engagement.

Australia And New Zealand Plastic Packaging Film Market

| Segmentation Details | Description |

|---|---|

| Product Type | Stretch Film, Shrink Film, Barrier Film, Rigid Film |

| Packaging Type | Flexible Packaging, Rigid Packaging, Pouches, Wraps |

| End User | Food & Beverage, Pharmaceuticals, Personal Care, Electronics |

| Material | Polyethylene, Polypropylene, Polyvinyl Chloride, Bioplastics |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Australia And New Zealand Plastic Packaging Film Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.